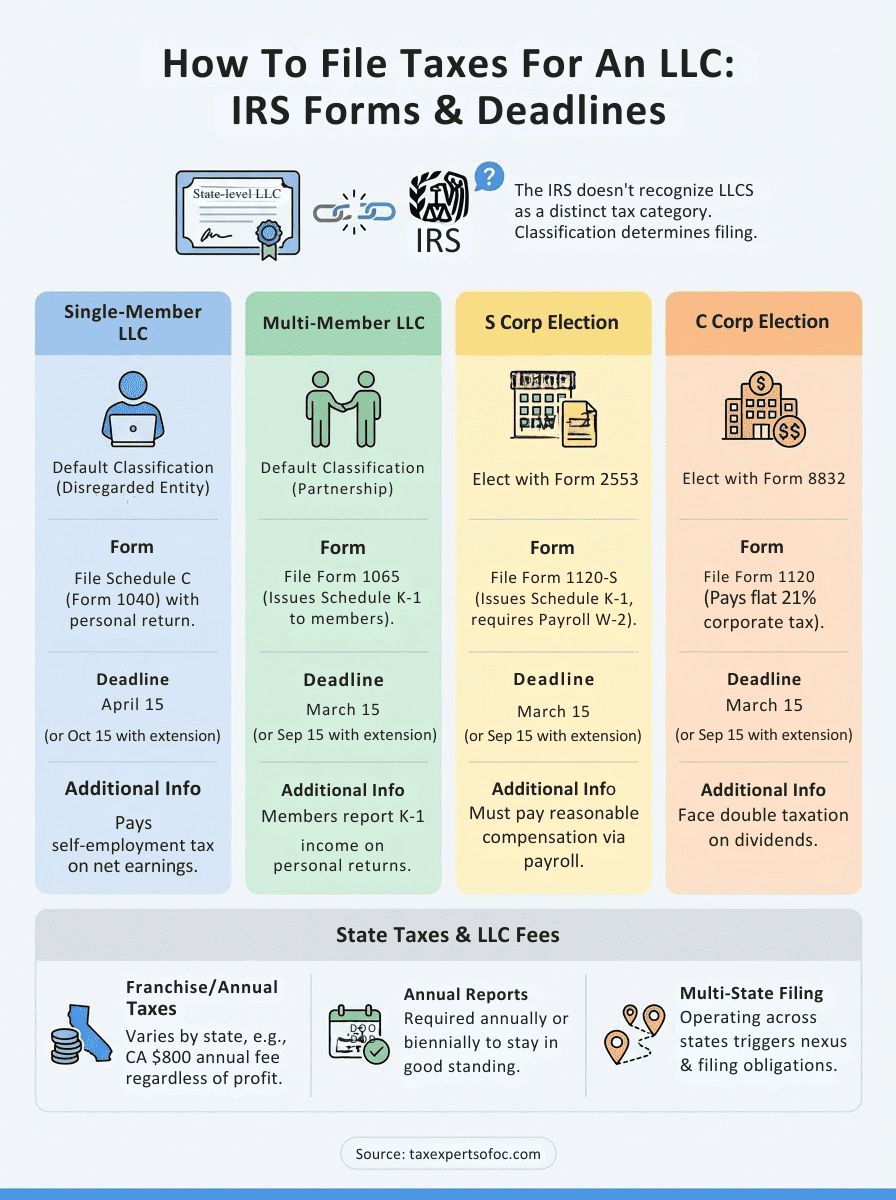

Filing taxes as an LLC owner isn't as straightforward as it might seem. The IRS doesn't recognize LLCs as a distinct tax category, which means how to file taxes for an LLC depends entirely on how your business is classified, whether as a sole proprietorship, partnership, or corporation. Get it wrong, and you're looking at penalties, interest, or an unwanted audit.

The good news: once you understand which forms apply to your specific situation, the process becomes manageable. Single-member LLCs report income on Schedule C, while multi-member LLCs typically file Form 1065 as partnerships. Some LLCs elect corporate taxation, adding Form 1120 or 1120-S to the mix. Each path has different deadlines, different requirements, and different implications for your bottom line.

At Tax Experts of OC, our CPAs and Enrolled Agents help LLC owners across all 50 states navigate these distinctions every day. This guide breaks down the exact forms you need, the deadlines you can't miss, and the step-by-step process for filing correctly based on your LLC's tax classification. Whether you're filing for the first time or cleaning up previous years, you'll have a clear roadmap by the end.

Why LLC tax filing feels confusing

The confusion starts with a simple fact: your LLC exists as a legal entity for state purposes, but the IRS treats it as invisible for federal tax purposes. You filed articles of organization, paid state fees, and your business legally operates as an LLC. Then tax season arrives, and you discover the IRS has no specific tax form for LLCs. Instead, the agency slots your business into one of several existing categories based on ownership structure and any elections you've made.

The IRS doesn't see your LLC as a tax entity

When you formed your LLC, you created a legal structure that protects your personal assets from business liabilities. State law recognizes your LLC as a distinct entity, complete with its own operating agreement and legal standing. The IRS ignores this distinction entirely. Federal tax law has no dedicated LLC classification, which means you report income under one of four existing categories: sole proprietorship, partnership, S corporation, or C corporation.

This disconnect forces you to translate your legal structure into a tax classification. A single-member LLC defaults to disregarded entity status, meaning the IRS treats it as if it doesn't exist separately from you as the owner. Multi-member LLCs default to partnership taxation unless you file an election to be treated differently. Neither of these classifications appears anywhere in your LLC formation documents, yet they determine which forms you file and how much you owe.

The IRS doesn't recognize LLCs as a tax category, which creates immediate confusion about which forms apply to your business.

Your state and the IRS work on different systems

Your state collected formation fees, requires annual reports, and may impose franchise taxes or gross receipts taxes on your LLC. These state-level obligations operate independently from your federal tax filing requirements. California charges an $800 annual franchise tax regardless of profitability, while Delaware assesses fees based on your LLC's authorized shares if you're operating as a corporation. Neither amount appears on your federal return, and neither affects how to file taxes for an LLC with the IRS.

State tax agencies also apply their own rules for pass-through entities, withholding requirements, and nexus thresholds. You might owe state income tax in multiple jurisdictions if your LLC operates across state lines, even though your federal return consolidates all income in one place. The compliance burden multiplies when you factor in local business taxes, sales tax obligations, and payroll withholding across different states.

Tax elections create different filing paths

Your LLC's default tax treatment might not serve your financial interests, which is why the IRS allows you to elect different classification by filing Form 2553 for S corporation status or Form 8832 for C corporation status. These elections change everything about your filing process. Single-member LLCs that elect S corp treatment must file Form 1120-S and issue themselves a W-2, transforming a simple Schedule C filing into a corporate return with payroll compliance requirements.

Each election carries distinct deadlines, different forms, and separate requirements for estimated tax payments. S corporations face a March 15 deadline, while C corporations file by April 15. Partnerships split the difference with a March 15 due date. Miss your election deadline, and you're stuck with your current classification for at least a year. File the wrong form because you misunderstood your classification, and you've triggered correspondence from the IRS that takes months to resolve.

Most LLC owners never receive clear guidance on these distinctions when they form their business. You registered your LLC online, received your EIN, and assumed tax filing would follow logically. Instead, you're left piecing together information from multiple sources, trying to determine which scenario applies to your specific situation while deadlines approach and penalties accumulate for non-compliance.

Decide how your LLC gets taxed

Your LLC's tax treatment determines everything about your filing process, from which forms you need to which deadline applies. The IRS assigns a default classification based on the number of members you have, but you can override that default by filing an election. Making the right choice now saves you thousands in taxes and prevents compliance headaches later.

Understanding your default classification

Single-member LLCs operate as disregarded entities unless you file Form 2553 or Form 8832 to change that status. The IRS treats your business income as personal income, which means you report profits and losses on Schedule C attached to your Form 1040. You pay both income tax and self-employment tax on your net earnings, and you don't file a separate business return. This default works well for small operations where simplicity matters more than tax optimization.

Multi-member LLCs automatically fall into partnership taxation. Your LLC files Form 1065 to report total income and expenses, then issues each member a Schedule K-1 showing their share of profits or losses. Each member reports their K-1 income on their personal return and pays self-employment tax on their distributive share. The partnership itself doesn't pay federal income tax, but it must file annually regardless of profitability.

Your LLC's default tax classification depends entirely on how many members you have, not on any choice you made during formation.

When to elect S corporation status

S corporation taxation makes sense when your LLC generates substantial profit and you want to reduce self-employment taxes. You file Form 2553 with the IRS, which must be received no later than two months and 15 days after the start of your tax year. Once approved, your LLC files Form 1120-S and you become an employee who receives both W-2 wages and distributions. You only pay self-employment tax on the W-2 portion, not on distributions.

The tradeoff arrives in the form of payroll compliance requirements. You run quarterly payroll, withhold employment taxes, and issue yourself a reasonable salary before taking distributions. This election works best when your net income exceeds $60,000 annually and you can justify the added administrative burden.

When C corporation taxation makes sense

C corporation status suits LLCs planning to retain earnings within the business or seeking outside investment from venture capital. You file Form 8832 to elect corporate taxation, then submit Form 1120 annually. The corporation pays taxes on its profits at the flat 21% corporate rate, and you pay personal income tax again when you receive dividends or distributions. This double taxation sounds punitive, but it allows for strategic income splitting and provides access to certain fringe benefits that pass-through entities can't offer.

Most service-based LLCs skip C corporation status unless they're positioning for acquisition or need to attract institutional investors. Understanding how to file taxes for an llc starts with getting this classification decision right.

Gather the info you need before you file

You can't file accurately without the right documentation in hand. Missing records lead to estimated numbers, which trigger audits and penalty notices when the IRS cross-references your return against third-party information. Gathering everything before you start prevents the need to amend returns later and ensures you claim every deduction you're entitled to take.

Your business records and receipts

Your bank statements, credit card records, and receipts form the foundation of your tax return. Download complete transaction histories for all accounts connected to your business, including any personal accounts where you made business purchases. The IRS expects you to substantiate every expense you claim, which means you need documentation showing the amount paid, the vendor name, the date, and the business purpose.

Separate your expenses into categories that match IRS standards: office supplies, vehicle expenses, professional fees, advertising, insurance, and utilities. Most accounting software generates these reports automatically if you've been categorizing transactions throughout the year. Without software, create a spreadsheet that totals each category and notes where you stored the supporting receipts. You'll reference these totals when completing Schedule C or preparing your partnership or corporate return.

Complete financial records prevent the need for amended returns and support your position if the IRS questions any deduction you claim.

Your income statements and 1099 forms

You receive Form 1099-NEC from any client or customer who paid you $600 or more during the year. These forms arrive by January 31, and you must report every dollar shown even if a client failed to send the form. The IRS receives copies of all 1099s issued with your EIN, and their matching system flags discrepancies between what clients report and what appears on your return.

Reconcile your bank deposits against the 1099 forms you received. Unexplained differences require documentation proving the deposit wasn't business income or explaining why the amount differs from what a client reported. Sales records, invoices, and merchant processor statements help you account for all income sources beyond 1099 clients.

Your EIN and prior year returns

Your employer identification number appears on every form you file, and you need it to access IRS transcripts or resolve any filing issues. Keep your prior year return accessible because many current-year calculations reference last year's figures, particularly for depreciation schedules, capital loss carryforwards, and business asset basis. Understanding how to file taxes for an LLC becomes simpler when you can compare your current numbers against previous years and spot inconsistencies before the IRS does.

How to file taxes for a single-member LLC

The IRS treats your single-member LLC as if it doesn't exist separately from you for tax purposes. You report all business income and expenses on Schedule C, which attaches to your personal Form 1040. No separate business return gets filed unless you elected S corporation or C corporation status. This simplified approach works for most solo operations, but you still face self-employment tax on your net profit in addition to regular income tax.

Your filing requirements as a disregarded entity

Schedule C replaces a dedicated business return for single-member LLCs operating under default classification. You list your business income on Line 1 and subtract ordinary business expenses throughout the form to calculate net profit or loss. This net amount transfers to Line 3 of Schedule 1 on your Form 1040, where it combines with your other income sources like wages, interest, or rental income. Your LLC's financial activity becomes part of your personal tax return rather than standing alone as a separate filing.

You must attach Schedule SE to calculate self-employment tax, which covers your Social Security and Medicare contributions. The current self-employment tax rate sits at 15.3% of your net earnings, applied to the first $168,600 of combined wages and self-employment income for 2024. Understanding how to file taxes for an llc as a single-member means accepting this additional tax burden beyond your standard income tax liability.

Single-member LLCs file as disregarded entities by default, which means Schedule C handles all business reporting on your personal return.

Completing Schedule C step by step

Part I of Schedule C requires your gross receipts or sales on Line 1, which should match the total of all 1099-NEC forms you received plus any additional income from cash payments or credit card transactions. Lines 8 through 27 cover deductible business expenses like advertising, vehicle costs, office expenses, and professional fees. You subtract total expenses from gross income to arrive at your net profit on Line 31, which becomes your taxable business income.

Part II asks about your cost of goods sold if you maintain inventory. Most service-based LLCs skip this section entirely. Part III requests information about your vehicle if you claimed mileage or actual expenses. Part IV asks yes/no questions about your business operations, and Part V calculates other expenses not listed in the standard categories.

Deadlines and quarterly estimated payments

Your Schedule C deadline matches your personal return due date of April 15 each year. You can extend this deadline to October 15 by filing Form 4868, but the extension only delays filing, not payment. Pay estimated taxes quarterly using Form 1040-ES if you expect to owe more than $1,000 when you file. These quarterly payments cover both income tax and self-employment tax on your projected annual profit.

How to file taxes for a multi-member LLC

Multi-member LLCs default to partnership taxation unless you've filed an election to change that status. You file Form 1065, which reports the total income and expenses for the business, then issue each member a Schedule K-1 showing their allocated share of profits, losses, and other tax items. The partnership itself pays no federal income tax, but every member reports their K-1 amounts on their personal returns and pays taxes individually on their share of profits, regardless of whether they received actual distributions.

Filing Form 1065 as the partnership return

Form 1065 requires you to report all business income on page 1, lines 1a through 8, which includes gross receipts, returns and allowances, cost of goods sold, and other income sources. You subtract ordinary business deductions on lines 9 through 21 to calculate ordinary business income on line 22. This amount flows to Schedule K, where you add special deductions, credits, and other tax items that pass through to members based on their ownership percentages.

Schedule K breaks down income and deductions by type because members need specific information to complete their personal returns. Capital gains, charitable contributions, and Section 179 deductions each occupy separate lines. Schedule K-1 pulls from Schedule K to show each member's proportionate share of these items. You must file Form 1065 by March 15 each year, and you can request a six-month extension using Form 7004, which moves your deadline to September 15.

Multi-member LLCs file Form 1065 annually regardless of profitability, with each member receiving a Schedule K-1 that determines their personal tax liability.

Preparing and distributing Schedule K-1s

Each member receives their own Schedule K-1 showing their share of partnership income, deductions, and credits based on their ownership percentage or the allocation method specified in your operating agreement. You must provide these K-1s by the partnership's filing deadline so members can complete their personal returns on time. Part III of Schedule K-1 shows the member's share of current-year income, while Part II tracks their capital account, which represents their equity stake in the business.

Tracking each member's basis and capital accounts

Members need to track their adjusted basis in the partnership to determine whether they can deduct partnership losses on their personal returns. Your basis starts with your initial contribution plus any additional capital you invest, then increases with your share of income and decreases with distributions and losses. Understanding how to file taxes for an llc with multiple members requires maintaining accurate capital accounts that reconcile with each member's basis calculations, particularly when members make disproportionate contributions or take unequal distributions during the year.

How to file taxes for an LLC taxed as an S corp

S corporation taxation requires you to file Form 2553 with the IRS to elect out of your default classification. Once approved, your LLC operates as a pass-through entity that files a corporate return while avoiding the double taxation that C corporations face. You become an employee of your own business, which means you must run payroll, withhold taxes, and issue yourself a W-2 before taking any distributions. This structure reduces self-employment taxes but adds compliance requirements that single-member LLCs and partnerships don't face.

Filing Form 1120-S as your corporate return

Form 1120-S reports your LLC's total income and expenses on page 1, lines 1a through 21, calculating ordinary business income that passes through to shareholders. You report gross receipts, cost of goods sold, officer compensation, and standard business deductions to arrive at ordinary business income on line 21. This amount transfers to Schedule K, where you add or subtract special items like capital gains, charitable contributions, and Section 179 deductions that affect each shareholder's tax liability differently.

Schedule K-1 shows each shareholder's proportionate share of income, deductions, and credits based on their ownership percentage. Your LLC must provide K-1s to all shareholders by the filing deadline so they can complete their personal returns. Understanding how to file taxes for an llc with S corp status means filing Form 1120-S by March 15 each year, or September 15 if you requested an extension using Form 7004.

S corporations file Form 1120-S and issue K-1s to shareholders, who then report their share of income on personal returns without paying self-employment tax on distributions.

Paying yourself reasonable compensation

The IRS requires S corporation owners who work in the business to pay themselves reasonable compensation through W-2 wages before taking distributions. You run quarterly payroll using Form 941, withhold federal income tax and FICA taxes, and remit these payments to the IRS. Your salary must reflect fair market value for the services you provide, based on what similar businesses pay for comparable work. The remaining profit after your salary becomes distributions that avoid the 15.3% self-employment tax.

Estimated taxes and shareholder basis

You pay estimated taxes quarterly using Form 1040-ES to cover income tax on your K-1 income. Your basis in the S corporation starts with your initial investment plus any loans you make to the business, then increases with your share of income and decreases with distributions and losses. You can only deduct S corporation losses up to your basis amount, which makes tracking this figure critical for accurate tax reporting and loss limitation calculations.

How to file taxes for an LLC taxed as a C corp

C corporation taxation creates a separate taxable entity that pays taxes at the corporate level before you pay taxes again on any dividends or distributions you receive. You file Form 8832 with the IRS to elect corporate treatment, which removes your LLC from pass-through taxation entirely. Your business files Form 1120 annually and pays the flat 21% corporate tax rate on all profits. This structure makes sense when you plan to retain earnings within the business or need to attract investors who prefer corporate equity over partnership interests.

Filing Form 1120 as a C corporation

Form 1120 requires you to report gross receipts on Line 1a and subtract cost of goods sold, compensation, and ordinary business expenses throughout page 1 to calculate taxable income on Line 30. You apply the 21% corporate tax rate to this amount, subtract any credits, and arrive at the total tax due on Schedule J. Understanding how to file taxes for an llc with C corp status means recognizing that profits stay taxed at the corporate level until you distribute them as dividends, which creates strategic planning opportunities for timing income recognition and managing tax brackets across multiple years.

Your LLC must file Form 1120 by April 15 following the close of your calendar tax year, or the 15th day of the fourth month after your fiscal year ends. You can extend this deadline six months using Form 7004, which moves calendar-year filers to October 15. Corporate returns don't issue K-1 forms to shareholders because profits don't pass through to personal returns the way they do with S corporations and partnerships.

Understanding double taxation and dividend treatment

The defining feature of C corporation taxation shows up when you take profits out of the business. Your LLC pays 21% corporate tax on its earnings, then you pay personal income tax again when you receive dividends or take distributions. Qualified dividends face a maximum 20% rate for high earners, which means you could pay up to 41% total tax on the same dollar of profit when combining both layers.

C corporations pay tax at the entity level, then shareholders pay tax again on dividends, creating double taxation that you must factor into your planning.

Corporate formalities and compliance requirements

C corporation status requires you to maintain formal corporate governance even though your LLC formation documents don't mention directors or officers. You hold annual meetings, document major decisions in corporate minutes, and maintain clear separation between corporate assets and personal finances. Corporate formality prevents piercing the corporate veil and protects the limited liability your LLC structure provides.

Deadlines, extensions, and estimated taxes

Your tax deadline depends entirely on how your LLC gets taxed, and missing these dates costs you money in penalties and interest that compound monthly. Extensions buy you extra time to file but don't postpone your payment obligation, which means you need to estimate what you owe and send payment by the original deadline. Quarterly estimated taxes add another layer of compliance for profitable LLCs, requiring you to prepay throughout the year rather than settling your bill in one lump sum when you file.

When your return must be filed

Single-member LLCs filing Schedule C follow the April 15 personal return deadline, while multi-member LLCs and S corporations must file by March 15. C corporations get until April 15 to submit Form 1120, giving them an extra month compared to pass-through entities. Calendar-year filers use these standard dates, but fiscal-year filers must submit returns by the 15th day of the third or fourth month after their year ends, depending on entity type.

Your filing deadline changes based on your LLC's tax classification, making it critical to know whether you're operating as a disregarded entity, partnership, or corporation.

Requesting an extension without penalties

Form 4868 extends personal returns including single-member LLC filings to October 15, while Form 7004 pushes partnership and corporate deadlines to September 15. You file these forms by your original due date, and the IRS grants the extension automatically without requiring an explanation. Extensions delay filing but not payment, which means you must estimate your tax liability and pay at least 90% of what you owe by the original deadline to avoid underpayment penalties.

Estimated tax payment schedule

Profitable LLCs pay estimated taxes four times per year using vouchers from Form 1040-ES or through the IRS online payment system. The standard due dates fall on April 15, June 15, September 15, and January 15 of the following year. You calculate each payment by estimating your annual tax liability and dividing by four, then adjusting subsequent payments if your income fluctuates significantly. Understanding how to file taxes for an llc includes knowing that you face underpayment penalties when your total estimated payments fall short of either 90% of your current-year tax or 100% of your prior-year liability, whichever provides the safe harbor amount that protects you from penalties.

Each quarterly payment covers both regular income tax and self-employment tax for pass-through entities. S corporation shareholders and C corporation owners make estimated payments on their personal returns to cover the tax on K-1 income or dividend distributions, separate from any corporate-level tax their LLC pays.

State taxes and LLC fees you might owe

Federal taxes represent only part of your compliance burden when you understand how to file taxes for an llc. Every state imposes its own requirements on LLCs operating within its borders, and these obligations exist separately from your IRS filings. You face annual fees, franchise taxes, gross receipts taxes, and state income tax returns that vary dramatically based on where your LLC formed and where it conducts business. Missing state deadlines triggers penalties that accumulate quickly and can result in administrative dissolution of your LLC.

State income and franchise taxes

Most states with income taxes require pass-through entities to file annual state returns that mirror your federal filing structure. Your single-member LLC files a state version of Schedule C in states like California or New York, while multi-member LLCs submit partnership returns that generate state-specific K-1 forms. S corporations and C corporations file state corporate returns using forms that parallel your federal 1120-S or 1120 submissions, though state tax rates and calculation methods differ from federal rules.

Franchise taxes appear in states like California, Delaware, and Texas regardless of whether your LLC earned any income. California charges $800 annually to most LLCs, while Delaware bases its franchise tax on your authorized shares or assumed par value capital. These taxes represent the cost of maintaining your LLC's legal existence in that state, separate from any income tax you owe on profits.

State franchise taxes and annual fees exist independently from your federal tax obligation, requiring separate payments even when your LLC shows no profit.

Annual report fees and renewal costs

You must file annual or biennial reports with your state's business registry to keep your LLC in good standing. Filing fees range from $50 in Arkansas to $800 in California, with most states charging between $100 and $300. Your LLC faces administrative dissolution if you skip these filings, which terminates your liability protection and requires costly reinstatement procedures to restore your legal status.

Multi-state filing obligations

Operating in multiple states creates nexus that triggers filing requirements in each jurisdiction where you conduct substantial business activity. You owe state taxes in any state where you maintain a physical presence, employ workers, or generate significant revenue beyond casual sales. Some states require withholding on nonresident members' share of partnership income, adding another layer of compliance when your LLC has owners living in different states.

What to do next

Understanding how to file taxes for an LLC requires more than reading a guide. You need to apply these steps to your specific situation, gathering your financial records, selecting the right forms, and meeting deadlines that vary based on your tax classification. The process becomes manageable when you break it into discrete tasks: verify your classification, organize your documentation, calculate your estimated payments, and submit your return on time.

Most LLC owners discover gaps in their knowledge when they actually sit down to file. Missing a state requirement or misclassifying income costs you money in penalties and interest that compound monthly. Professional guidance eliminates guesswork and ensures you claim every deduction while avoiding audit triggers.

Tax Experts of OC provides nationwide LLC tax preparation and resolution services through CPAs and Enrolled Agents who handle returns in all 50 states. Schedule your free 30-minute consultation to review your LLC's tax situation and get a clear filing strategy before your deadline arrives.