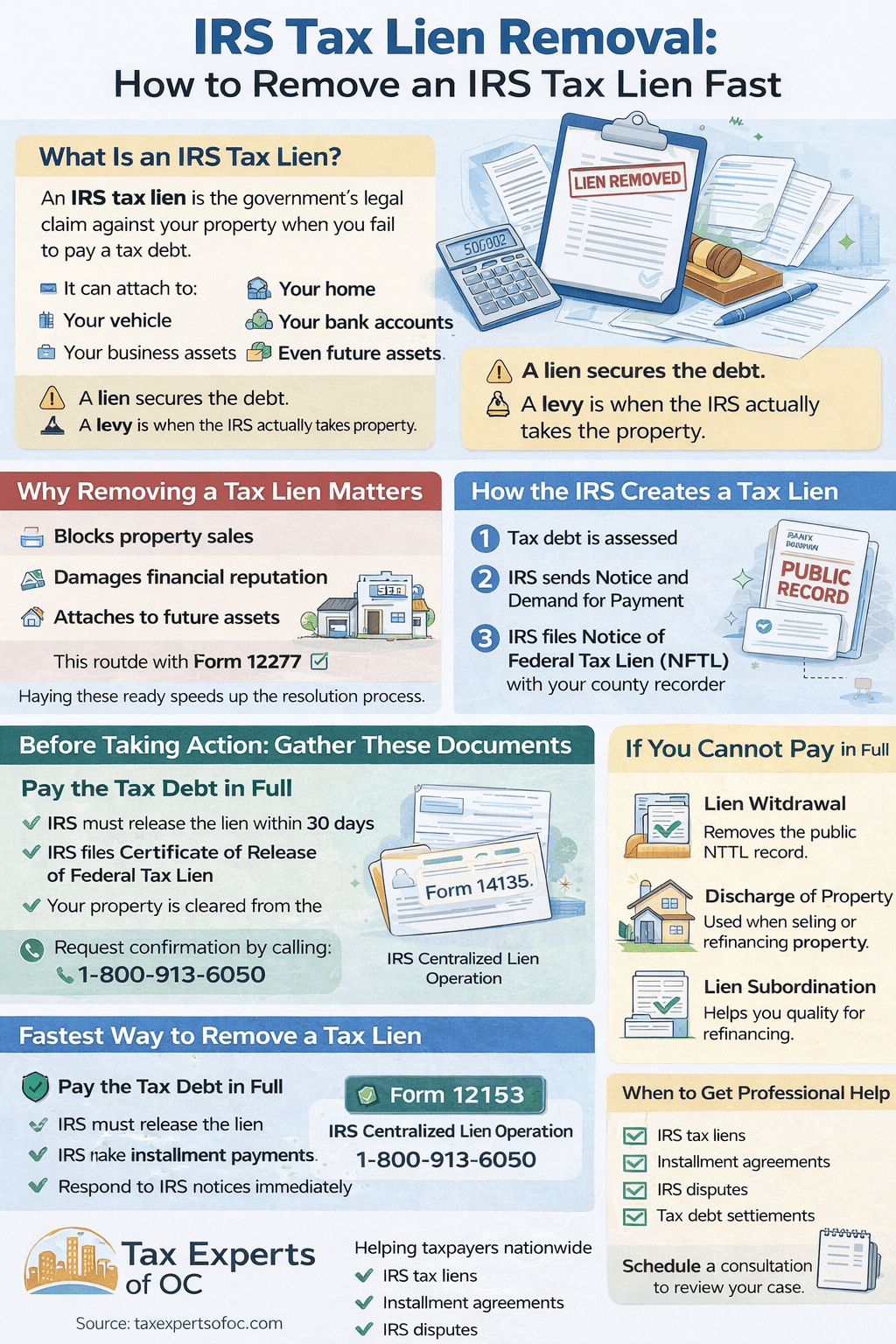

An IRS tax lien attaches to everything you own, your home, your car, your bank accounts, even future assets. It damages your credit, complicates property sales, and signals to lenders that the federal government has a legal claim against your property. If you're dealing with one right now, you probably want to know how to remove an IRS tax lien before it causes more financial damage.

The good news: a tax lien isn't permanent. The IRS has specific procedures for lien release, discharge, subordination, and withdrawal, each with different requirements and timelines. The key is knowing which option fits your situation and acting on it quickly. At Tax Experts of OC, our CPAs and Enrolled Agents help clients across all 50 states resolve exactly these types of IRS disputes, from negotiating lien withdrawals to settling the underlying tax debt.

This guide breaks down each method for removing an IRS tax lien, the forms you'll need, realistic timelines to expect, and the steps you can take right now to get the process started.

What a federal tax lien is and why it matters

A federal tax lien is a legal claim the IRS places against your property when you fail to pay a tax debt after a formal demand. It doesn't mean immediate seizure, but the government now holds a legal interest in everything you own, including real estate, bank accounts, vehicles, and business assets. The lien attaches automatically the moment the IRS assesses the liability, sends you a bill, and you don't pay.

A lien secures the government's interest in your property; a levy is when the IRS actually takes it. They are not the same thing.

How the IRS establishes a lien

The IRS files a Notice of Federal Tax Lien (NFTL) at your county recorder's office to alert creditors and title companies that the government holds a prior claim on your assets. Before filing, you receive a Collection Due Process (CDP) notice, which gives you a short window to respond or request a hearing. Most people miss this opportunity and only learn about the lien when a lender or title search uncovers it.

Specifically, the IRS follows three steps to establish a lien:

- Assess the tax debt

- Send a Notice and Demand for Payment

- File the NFTL publicly after nonpayment

What the lien does to your finances

Once filed, a tax lien appears as a public record and creates real obstacles across your financial life. Selling your home becomes extremely difficult because title cannot transfer cleanly until the lien is released or discharged. Understanding these consequences is the first step toward knowing how to remove an IRS tax lien in a way that fits your exact situation.

A lien can affect you in several key ways:

- Blocks property sales and refinancing

- Signals financial risk to lenders and creditors

- Attaches to any future assets you acquire during the lien period

Before you start: get the facts and documents

Before you take any action on how to remove an IRS tax lien, you need to know exactly what you're dealing with. The IRS bases every lien decision on the assessed tax balance and your compliance history, so pulling the right records first saves you time and prevents costly mistakes during the resolution process.

Get your IRS account transcript

Your IRS online account at irs.gov gives you direct access to your balance, payment history, and any NFTL filings. Log in and download your Account Transcript for each year in question. These documents confirm the exact amount owed and show whether additional penalties or interest have accrued since the original assessment.

If you find discrepancies between your personal records and the IRS transcript, document them immediately because errors can directly affect your resolution options.

Gather your supporting documents

You also need to collect specific paperwork before contacting the IRS or requesting any lien action. Having everything organized upfront speeds up processing and reduces back-and-forth with IRS representatives:

- Copies of any IRS notices you've received

- Proof of payments already made

- Your most recent tax returns for each affected year

- A copy of the NFTL from your county recorder's office

Fastest path: pay and get the lien released

Paying your tax debt in full is the single fastest method for how to remove an IRS tax lien. Once the IRS confirms your payment, they are legally required to release the lien within 30 days. This path works best if you have access to funds through savings, a personal loan, or a home equity line of credit that covers the full balance owed.

The IRS will not automatically notify every creditor or title company, so you need to request official documentation after the release is filed.

What happens after you pay

After full payment posts to your account, the IRS files a Certificate of Release of Federal Tax Lien with the same county recorder's office where the original NFTL was recorded. This certificate clears the public record and removes the government's legal claim on your assets and property. Verify the release appears in the county records within 30 to 45 days of payment.

How to confirm and document the release

Request a copy of the Certificate of Release directly from the IRS by calling 1-800-913-6050. Keep this document stored securely because lenders and title companies will ask for it during any future property sale or loan application. If the county records have not been updated after 45 days, contact the IRS Centralized Lien Operation office to follow up.

If you can't pay: withdrawal, discharge, subordination

Full payment isn't always an option, but you still have three formal IRS procedures that can reduce the lien's impact while you work toward resolution. Understanding the difference between withdrawal, discharge, and subordination is essential when exploring how to remove an IRS tax lien without a lump-sum payment.

Withdrawal removes the public NFTL filing entirely, while discharge and subordination only limit where the lien applies, not the underlying debt.

Lien Withdrawal

A lien withdrawal removes the Notice of Federal Tax Lien from public records without requiring full payment. You can qualify if you enter a Direct Debit Installment Agreement and have made at least three consecutive on-time payments. Submit Form 12277 to request withdrawal. The IRS will review your compliance history before approving, so any missed filings or payments will work against you.

Discharge and Subordination

Discharge removes the lien from a specific piece of property, which allows you to sell or refinance that asset even though your overall tax debt remains. Submit Form 14135 to apply for a discharge. Subordination lets another creditor move ahead of the IRS lien in priority, making it easier to secure financing. Use Form 14134 for subordination requests. Both options require the IRS to confirm that granting the request won't reduce their ability to collect the full balance owed.

Fix mistakes and protect yourself while you resolve it

IRS errors happen, and catching them early can change your resolution options. If the lien amount is wrong or the liability was assessed incorrectly, request a Collection Due Process (CDP) hearing by filing Form 12153 within 30 days of the CDP notice. Missing that deadline removes your right to appeal in Tax Court.

Treat every IRS notice with a deadline as urgent because late responses permanently eliminate resolution options.

Dispute an incorrect lien amount

Filing Form 12153 triggers a review by the IRS Office of Appeals, an independent body that can reduce or eliminate the underlying balance, which directly affects whether the lien remains valid. Gather supporting documentation before the hearing, including prior returns and payment records.

Common errors worth disputing include:

- Payments the IRS didn't apply to your account

- Assessments made after the collection statute expired

Stay compliant throughout the process

Knowing how to remove an IRS tax lien requires more than filing paperwork. Every unfiled return during the resolution period gives the IRS grounds to deny your withdrawal or discharge request.

File any past-due returns immediately and set up automatic payments if you're on an installment agreement. Consistent compliance signals good faith to the IRS, which strengthens every formal request you submit.

Next steps if you want a pro to handle it

Knowing how to remove an IRS tax lien is one thing; executing the process correctly under deadline pressure is another. A single missed form, late response, or incomplete installment agreement can reset your progress and give the IRS grounds to deny your request. The stakes are too high to guess your way through it.

Working with a CPA or Enrolled Agent gives you direct access to professionals who negotiate with the IRS daily and know exactly which resolution path fits your specific balance, compliance history, and financial situation. At Tax Experts of OC, our team handles lien withdrawals, discharges, installment agreements, and CDP hearings for clients across all 50 states, with transparent pricing and no hidden fees.

If you're ready to stop the lien from damaging your finances further, schedule a free 30-minute consultation with Tax Experts of OC and get a clear plan built around your case.