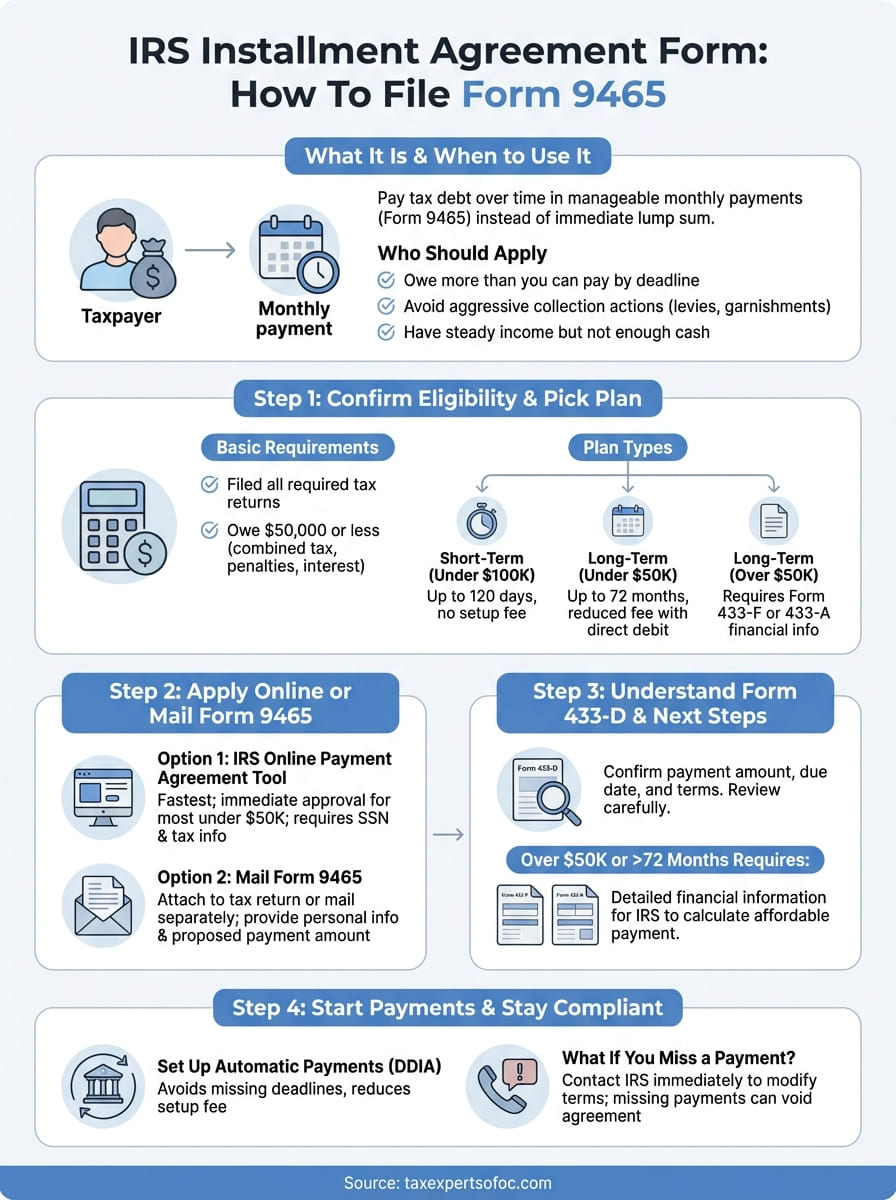

Owing money to the IRS can feel overwhelming, but you don't have to pay it all at once. The IRS installment agreement form, specifically Form 9465, allows you to break your tax debt into manageable monthly payments instead of facing immediate collection actions like wage garnishments or bank levies.

At Tax Experts of OC, we help clients across all 50 states navigate tax resolution, including setting up payment plans with the IRS. Whether you owe $10,000 or $100,000, understanding which forms to use and how to apply correctly can mean the difference between affordable payments and aggressive collection.

This guide walks you through everything you need to know about Form 9465, including when to use it, how to complete it step by step, and alternative application methods like the IRS Online Payment Agreement tool. By the end, you'll have a clear path to resolving your tax debt on terms that work for your financial situation.

What an IRS installment agreement is and when to use it

An IRS installment agreement is a formal payment plan that allows you to pay your tax debt over time instead of in a single lump sum. When you submit the IRS installment agreement form or apply online, you're asking the IRS to accept monthly payments until your balance is fully paid. The agency typically grants these requests if you can demonstrate that paying immediately would cause financial hardship.

Who should apply for an installment agreement

You should consider an installment agreement if you owe more than you can pay by the tax deadline and want to avoid aggressive collection actions. This option works well when you have steady income but can't access enough cash to settle your debt immediately.

Common situations where taxpayers use payment plans include:

- You owe between $10,000 and $50,000 and need up to 72 months to pay

- You recently received an IRS notice demanding payment but lack the full amount

- Your business had a difficult year and you can't cover both operating costs and tax debt

- You want to avoid liens, levies, or wage garnishments while making regular payments

- You can afford a consistent monthly amount that will eliminate the debt within six years

The IRS charges setup fees and applies interest and penalties until you pay the balance in full, so the sooner you start, the less you'll ultimately pay.

What happens if you don't set up a payment plan

Ignoring your tax debt triggers the IRS collection process. The agency will send multiple notices demanding payment, and if you don't respond, they can file a federal tax lien against your property, which damages your credit and makes it difficult to sell or refinance assets.

After the lien, the IRS may proceed with levies on your bank accounts or garnish your wages without additional warning. Setting up a payment plan stops these collection actions and gives you breathing room to resolve your debt on manageable terms.

Step 1. Confirm eligibility and pick the right plan

Before you complete the IRS installment agreement form, you need to verify that you qualify and choose the payment plan that matches your debt amount. The IRS offers several plan types based on how much you owe and your ability to pay, so understanding your options prevents wasted time on applications that the agency will reject.

Check if you meet the basic requirements

You can apply for a payment plan if you've filed all required tax returns and owe $50,000 or less in combined tax, penalties, and interest. The IRS automatically denies applications from taxpayers who haven't submitted missing returns, so make sure your filing is current before you request an installment agreement.

If you owe more than $50,000, you'll need to provide detailed financial information and may qualify for a partial payment plan instead.

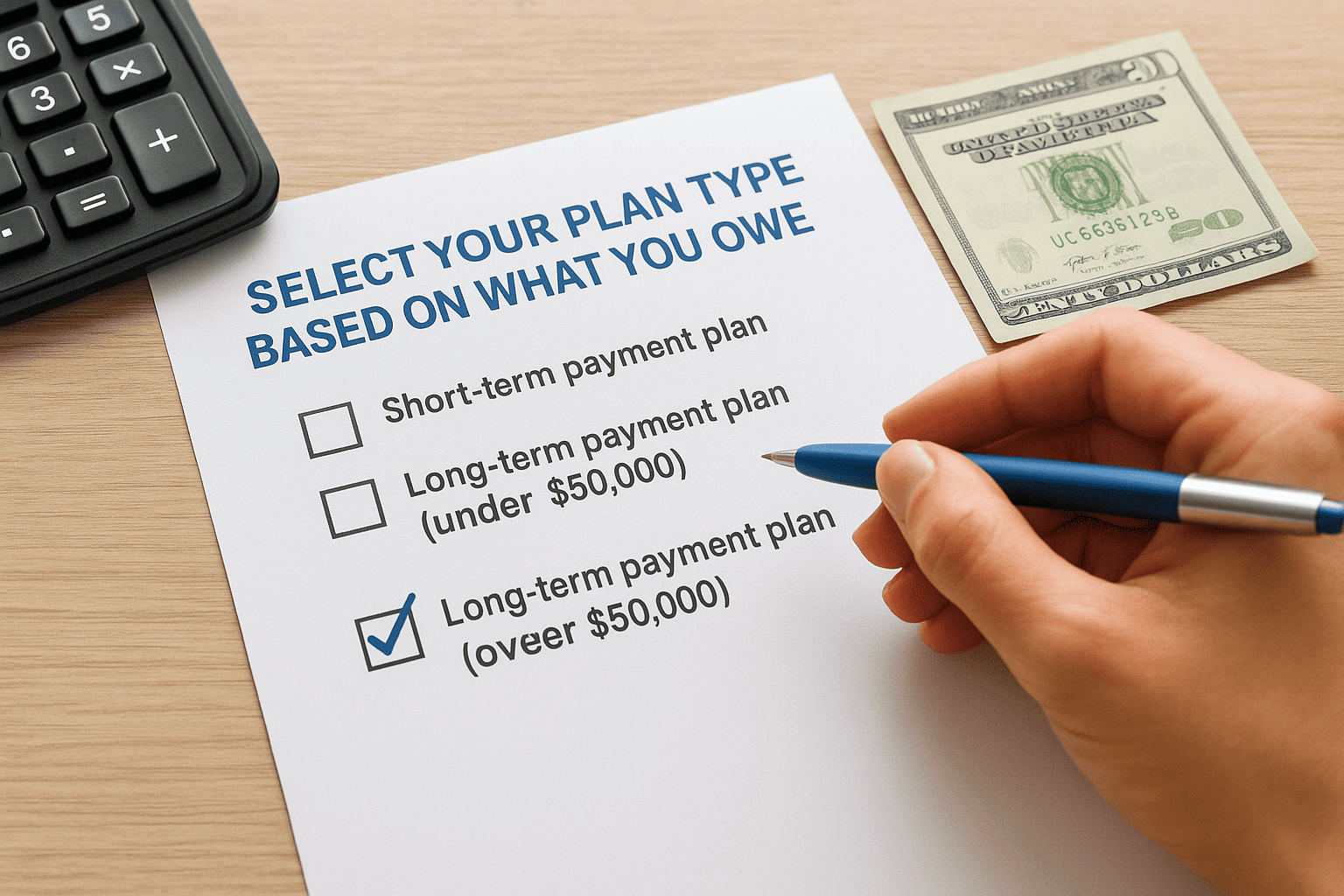

Select your plan type based on what you owe

The amount you owe determines which payment plan applies:

- Short-term payment plan: For debts under $100,000 that you can pay within 120 days (no setup fee)

- Long-term payment plan (under $50,000): Monthly payments spread over up to 72 months with a reduced setup fee if you pay by direct debit

- Long-term payment plan (over $50,000): Requires Form 433-F or 433-A to document your financial situation before approval

Step 2. Apply online or request it with Form 9465

You have two ways to request a payment plan: apply through the IRS Online Payment Agreement tool or submit the IRS installment agreement form by mail. The online method gives you immediate approval for most plans, while Form 9465 requires processing time of up to 30 days. Choose the method that matches your situation and how quickly you need confirmation.

Apply through the IRS Online Payment Agreement tool

The fastest way to set up your payment plan is through the IRS Online Payment Agreement application at irs.gov. You'll need your Social Security number, tax information from your most recent return, and bank account details if you want to set up direct debit payments. The system walks you through each step and confirms your monthly payment amount before you submit.

Most taxpayers who owe less than $50,000 receive instant approval through the online tool without speaking to an IRS agent.

Mail Form 9465 with your tax return or separately

If you prefer paper filing or can't access the online tool, complete Form 9465 and attach it to your tax return when you file. You'll need to provide your personal information, the tax year and form number you're paying for, and your proposed monthly payment amount. Mail the completed form to the address shown on your IRS notice, or include it with your return if you're filing by paper.

Step 3. Understand Form 433-D and what the IRS may ask next

After the IRS approves your IRS installment agreement form, you'll receive Form 433-D (Installment Agreement) in the mail. This document confirms your monthly payment amount, payment due date, and the specific terms you must follow to keep the agreement active. Review it carefully because missing a payment or failing to file future returns on time can void the entire arrangement and restart collection actions.

When the IRS requires additional financial documentation

If you owe more than $50,000 or request a payment term longer than 72 months, the IRS requires Form 433-F (Collection Information Statement) or Form 433-A for individuals before approval. These forms ask for detailed information about your income, monthly expenses, assets, and debts to determine what you can realistically afford to pay each month.

The IRS uses this financial information to calculate a payment amount that won't cause immediate economic hardship while still moving toward full repayment.

What to expect after submitting Form 433-D

Once you sign and return Form 433-D, your payment plan becomes official and the IRS stops most collection actions against you. You'll receive monthly reminders about your payment due date, and the agency will apply your payments to your oldest tax debt first, including accumulated interest and penalties. Keep copies of all payment confirmations in case you need to prove compliance later.

Step 4. Start payments, stay compliant, and fix issues fast

Once the IRS approves your IRS installment agreement form and you receive Form 433-D, you need to make your first payment by the due date shown on the agreement. The IRS expects you to pay on time every month and file all future tax returns by their deadlines. Missing either obligation gives the agency grounds to cancel your payment plan and restart aggressive collection.

Set up automatic payments to avoid missing deadlines

The simplest way to stay compliant is by enrolling in Direct Debit Installment Agreement (DDIA) when you apply. This option automatically withdraws your monthly payment from your checking account on a date you choose, which prevents late payments and reduces your setup fee. You can set up direct debit through the IRS Online Payment Agreement tool or by selecting it on Form 9465.

Automatic payments eliminate the risk of human error and keep your agreement in good standing without monthly reminders.

What to do if you miss a payment or can't afford your monthly amount

Contact the IRS immediately if you miss a payment or realize you can't afford your current monthly amount. You can request a modification by calling the number on your Form 433-D or submitting a new payment plan application. Acting quickly prevents default and gives you options to adjust your terms before the IRS cancels your agreement.

What to do if you want extra help

Filing the IRS installment agreement form correctly the first time prevents delays and reduces the risk of rejection. If your debt exceeds $50,000, you have complex financial circumstances, or you're worried about making a mistake that could trigger collection actions, working with a tax professional gives you an experienced advocate who understands IRS procedures.

Tax Experts of OC helps clients nationwide set up payment plans, negotiate better terms, and resolve tax disputes with the IRS. Our CPA and Enrolled Agent handle everything from completing Form 9465 to responding to IRS requests for financial documentation. We offer a 30-minute free consultation to review your situation and explain your options before you commit to any service.

Contact Tax Experts of OC to schedule your free consultation and get professional help resolving your tax debt with a payment plan that fits your budget.