Getting hit with an IRS penalty can feel like a punch to the gut, especially when you believe you had a valid reason for missing a deadline or underpaying. The good news? The IRS does offer relief options, and the IRS penalty abatement form, officially known as Form 843, is your primary tool to request it. Filing this form correctly can mean the difference between paying thousands in penalties or having them reduced or eliminated entirely.

At Tax Experts of OC, our CPAs and Enrolled Agents help clients across all 50 states navigate penalty abatement requests regularly. This guide walks you through Form 843 step by step, from determining your eligibility to submitting a request that actually gets results. Whether you're pursuing first-time abatement or have reasonable cause for your late filing or payment, you'll find everything you need to move forward with confidence.

What Form 843 covers and when to use it

Form 843, officially titled "Claim for Refund and Request for Abatement," is the IRS penalty abatement form you use to request relief from most civil penalties. This form gives you a formal way to explain why the IRS should reduce or eliminate penalties they've already assessed against you. You can file it for penalties related to late filing, late payment, failure to deposit payroll taxes, accuracy issues, and dozens of other penalty types listed in the IRS penalty reference chart.

Types of penalties you can challenge

Form 843 covers nearly every civil tax penalty, but you need to know which penalty code appears on your IRS notice before you start. The most common penalties taxpayers request abatement for include:

- Failure to file penalty (IRC 6651(a)(1)): typically 5% per month, up to 25%

- Failure to pay penalty (IRC 6651(a)(2)): usually 0.5% per month, up to 25%

- Estimated tax penalty (IRC 6654 or 6655): for underpayment of quarterly taxes

- Accuracy-related penalties (IRC 6662): 20% penalty for substantial understatement

- Trust fund recovery penalty (IRC 6672): for unpaid payroll taxes

Form 843 does not apply to interest charges. The IRS only abates interest when they caused the delay through their own error.

When Form 843 is the right tool

You should use Form 843 after the IRS has formally assessed the penalty on your account. If you receive a notice proposing a penalty but haven't received a final assessment yet, you typically respond directly to that notice instead. Form 843 becomes necessary when you see the penalty listed on your account transcript or when the IRS sends a notice demanding payment. Most taxpayers file Form 843 when pursuing first-time abatement or when they have reasonable cause, such as serious illness, natural disaster, or reliance on incorrect professional advice.

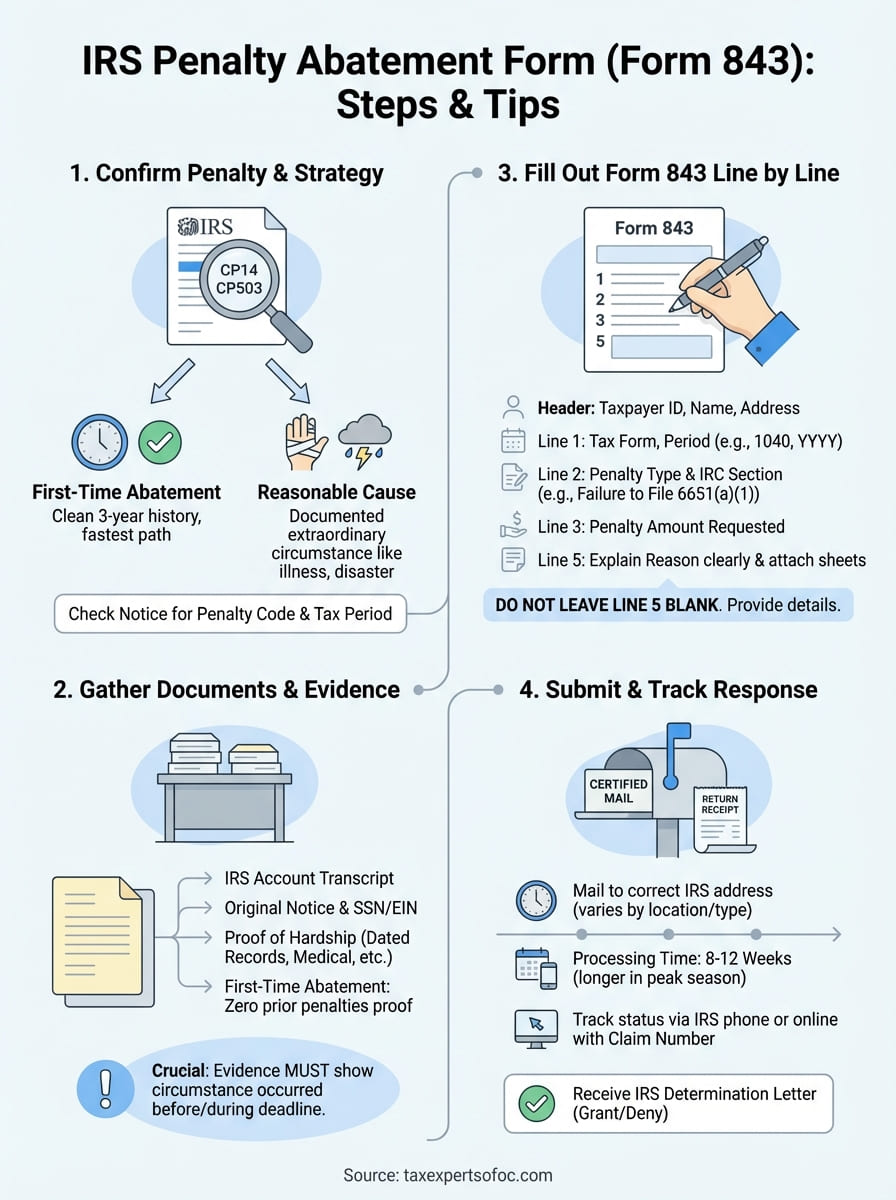

Step 1. Confirm the penalty and your best relief path

Before you touch the IRS penalty abatement form, you need to confirm which penalty the IRS assessed and determine the strongest relief strategy. Filing Form 843 without this clarity wastes time and often leads to rejection. Your IRS notice contains the penalty code and tax period, both of which you'll need to complete the form accurately.

Check your IRS notice for the penalty code

Pull out the IRS notice you received (typically CP14, CP503, or Letter 1058) and locate the penalty description near the bottom of the page. The notice shows the penalty amount, penalty code, and tax year it applies to. Common codes include 6651(a)(1) for failure to file and 6651(a)(2) for failure to pay. Write down this information because you'll reference it multiple times on Form 843. If you can't find the code on your notice, call the IRS at the number listed or request your account transcript through IRS.gov, which shows all assessed penalties.

Choose between first-time abatement and reasonable cause

First-time abatement works if you have a clean compliance history for the prior three years and no current unfiled returns. The IRS grants this relief administratively, making it the fastest path when you qualify. Reasonable cause requires you to prove an extraordinary circumstance prevented timely filing or payment, such as serious illness, death in the family, natural disaster, or IRS error. Choose first-time abatement when your records are clean. Use reasonable cause when you have documented hardship.

First-time abatement eliminates the need to prove hardship, but you can only use it once every three years.

Step 2. Gather what you need before you fill it out

Collecting the right documents before you start the IRS penalty abatement form saves you from incomplete submissions and delays. You need specific records from both the IRS and your own files to complete Form 843 accurately. Missing even one piece of information gives the IRS grounds to reject your request without considering your actual circumstances.

Core IRS documents and account information

Start by pulling your IRS account transcript for the tax period in question. You access this through IRS.gov by creating an account or by calling 800-908-9946. The transcript shows your penalty assessment date, penalty amount, and any payments applied. You also need the original notice that assessed the penalty, your Social Security Number or EIN, and your current mailing address. Write down the exact penalty code from your transcript because Form 843 requires you to specify which penalty you're contesting.

Evidence that supports your abatement reason

Your supporting documents prove why you qualify for relief. For first-time abatement, gather proof of clean filing history such as transcripts showing zero penalties in the prior three years. For reasonable cause, collect medical records, death certificates, natural disaster documentation, or proof of professional advice you relied on. Include dated documentation that shows the circumstance occurred before or during the filing deadline. The IRS rejects vague explanations without concrete proof.

The IRS denies most Form 843 requests that lack specific, dated documentation of the hardship claimed.

Step 3. Fill out Form 843 line by line

Form 843 contains fewer than a dozen active lines, but each one needs precise information matched to your IRS records. You download the current version from IRS.gov (search "Form 843 PDF") and complete it by hand or using a PDF editor. Start at the top and work through each section methodically to avoid processing delays.

Header section and taxpayer identification

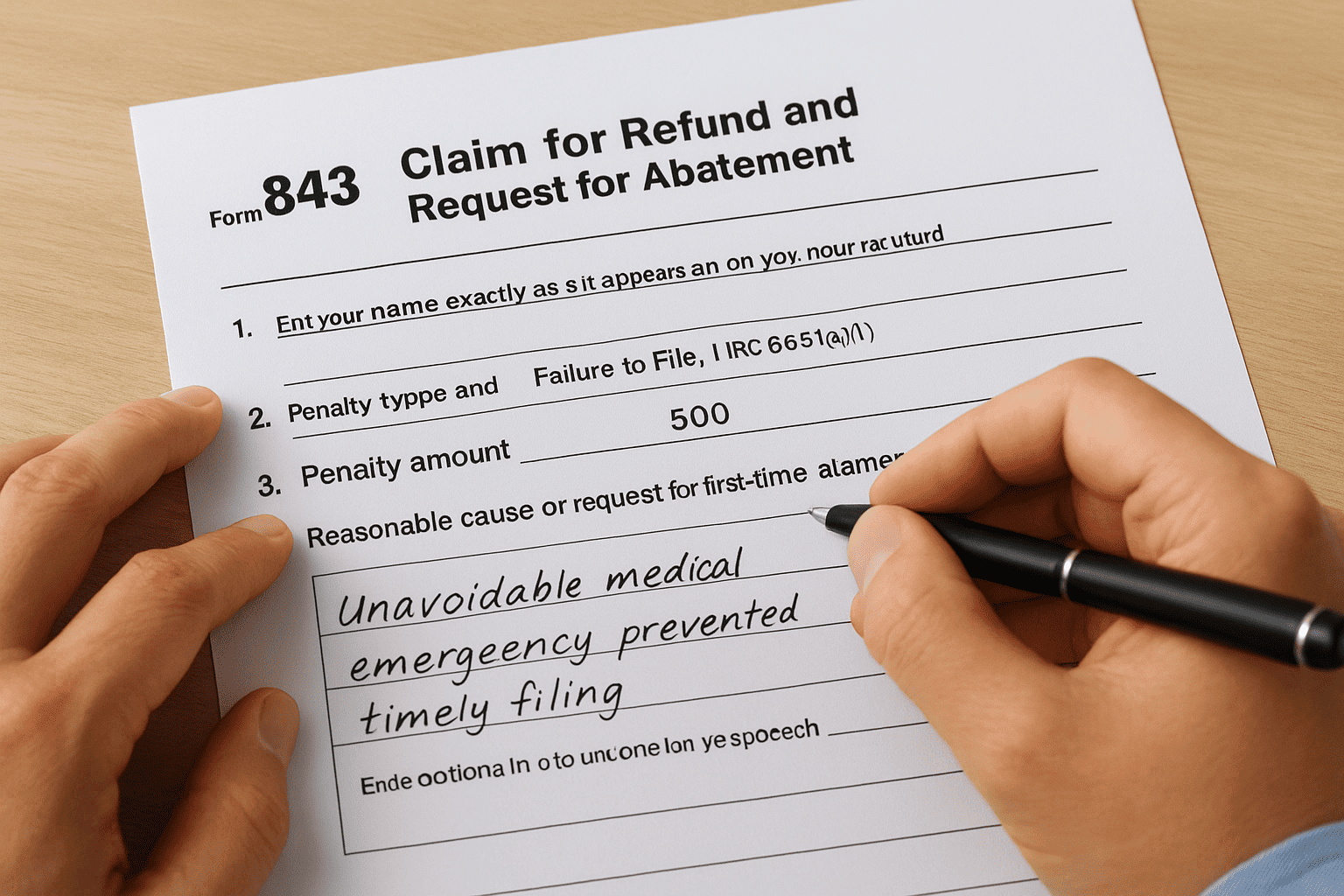

Enter your name exactly as it appears on your tax return in the top box. Business entities use the legal business name. Add your Social Security Number or Employer Identification Number in the designated field. Fill in your current mailing address where the IRS should send their response. If you're filing for a business, include the business address instead of your personal one.

Lines 1-5: Penalty details and tax period

Line 1 requires the tax form number (1040, 1120, 941) and the tax period affected. Use the exact dates from your IRS notice. Line 2 asks for the penalty type and IRC section, such as "Failure to File, IRC 6651(a)(1)." Line 3 needs the penalty amount you're requesting abatement for. Line 5 is critical: this is where you explain your reasonable cause or request first-time abatement in plain language. Attach additional sheets if you need more space to document your circumstances.

The IRS rejects Form 843 requests that leave Line 5 blank or provide vague explanations without supporting facts.

Step 4. Submit Form 843 and track the IRS response

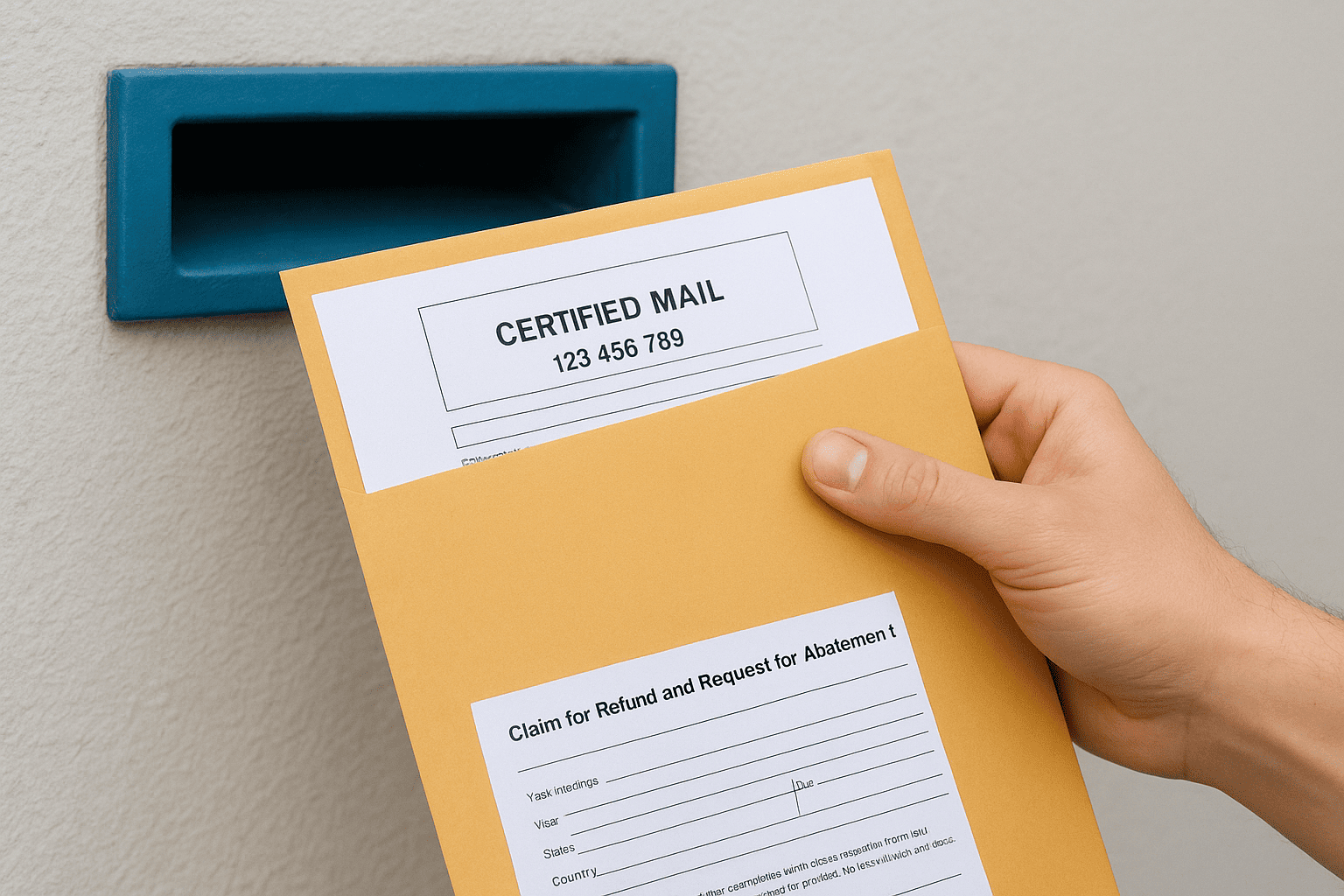

You submit the IRS penalty abatement form by mail to the IRS address that matches your filing location and tax type. The IRS does not accept Form 843 electronically, so you need to send a physical copy with all supporting documents attached. Make copies of everything before you mail it, and use certified mail with return receipt to confirm delivery. The IRS processes these requests in the order received, which means timing matters if you're facing collection actions.

Where to mail your completed Form 843

The mailing address depends on your state and the type of tax return involved. You find the correct address in the Form 843 instructions under "Where to File." Individual income tax penalties go to one address, while business tax penalties often go to another. If you filed your original return in California and you're requesting abatement for a 1040 penalty, you mail Form 843 to the IRS center in Fresno. Business entities typically send Form 843 to the address where they filed their original business return.

Track your request and follow up timing

The IRS takes 8 to 12 weeks to process Form 843 requests during normal periods, longer during peak filing season. You can check your status by calling the IRS at 800-829-1040 and referencing your claim number from your mailing receipt. If you don't receive a response within 90 days, call to verify they received your request and ask for a status update.

The IRS sends a written determination letter that either grants, partially grants, or denies your penalty abatement request.

Next steps

Filing Form 843 correctly gives you a real shot at penalty relief, but the IRS denies most requests that lack proper documentation or technical accuracy. You've now seen how to confirm your penalty, gather supporting evidence, complete each line accurately, and submit your request to the right address. The process works when you match your abatement strategy (first-time or reasonable cause) to your actual situation and back it up with specific, dated proof.

If you're facing multiple penalty years, dealing with collection actions while your request processes, or unsure whether your documentation proves reasonable cause, professional representation makes a measurable difference. Our CPAs and Enrolled Agents at Tax Experts of OC handle IRS penalty abatement form submissions daily and know exactly what documentation the IRS accepts. We offer a free 30-minute consultation to review your specific penalties and determine the strongest path forward. Contact Tax Experts of OC to get started with your penalty relief request today.