If you employ even one worker, the IRS expects you to report and pay Federal Unemployment Tax (FUTA) each year. That's where IRS Form 940 instructions come in, they walk you through calculating your FUTA liability, claiming credits for state unemployment taxes paid, and filing your annual return correctly. Get it wrong, and you're looking at penalties, interest, or unwanted IRS attention.

The form itself is only one page, but the rules behind it aren't always straightforward. State credit reductions, exempt wages, multi-state obligations, these details trip up business owners every filing season. At Tax Experts of OC, our CPAs and Enrolled Agents handle payroll tax compliance for small and mid-sized businesses across all 50 states, and Form 940 errors are among the most common issues we help clients resolve.

This guide breaks down Form 940 line by line. You'll learn who needs to file, how to calculate your FUTA tax, when and where to submit the form, and how to avoid the mistakes that trigger IRS notices. Whether you're filing for the first time or double-checking your work, this is the resource to keep open while you complete your return.

What Form 940 covers and who must file

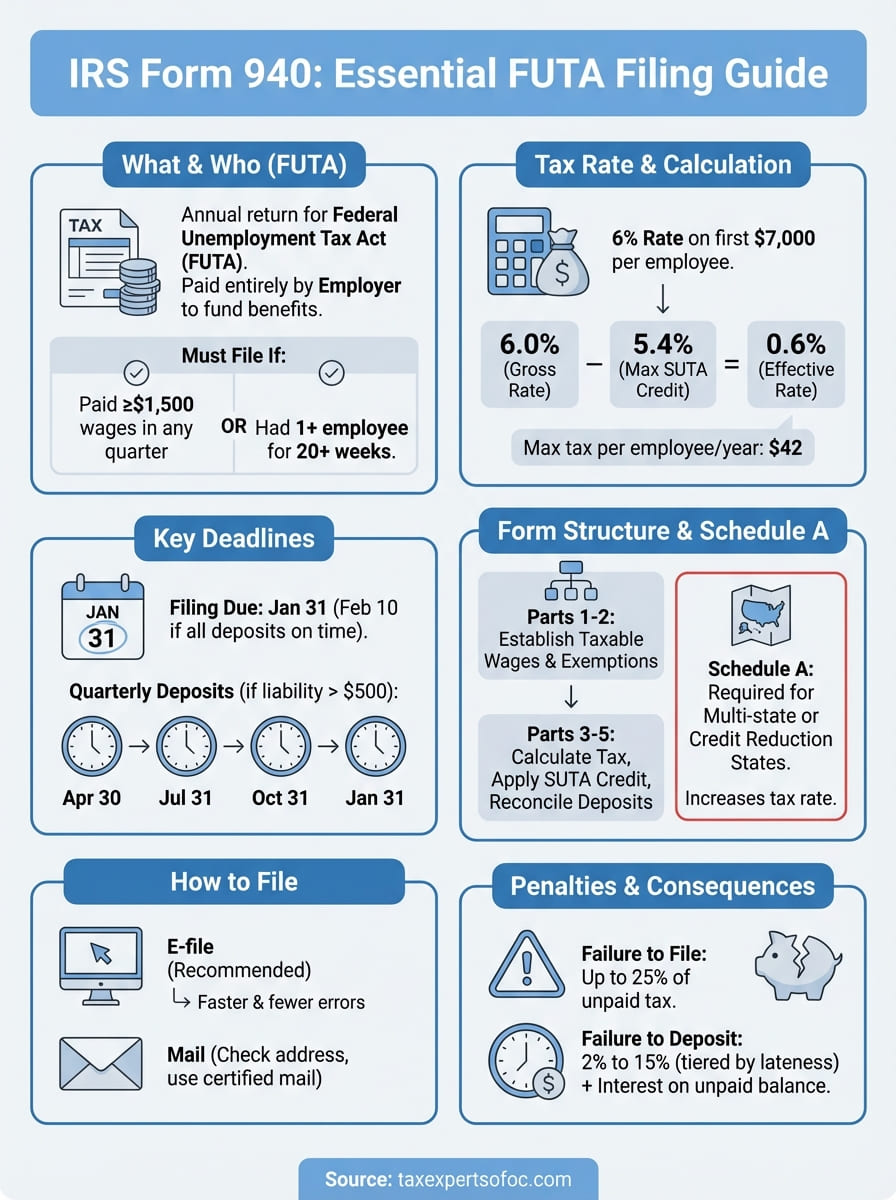

Form 940 is the IRS's annual return for reporting Federal Unemployment Tax Act (FUTA) tax. This tax funds the federal-state unemployment compensation system that pays benefits to workers who lose their jobs through no fault of their own. Unlike payroll taxes such as Social Security and Medicare, FUTA is paid entirely by the employer, not split with employees. The IRS form 940 instructions make clear that this is a reporting and reconciliation form, not just a payment voucher, so you need to complete it accurately even if you already made quarterly deposits throughout the year.

FUTA is separate from the state unemployment tax (SUTA) you pay to your state agency. You report both on different forms, but your SUTA payments can reduce what you owe in FUTA.

What FUTA tax actually covers

The FUTA tax rate is 6% on the first $7,000 you pay each employee during the calendar year. Once an employee earns more than $7,000 from you in a given year, the additional wages are exempt from FUTA. In practice, most employers pay far less than 6% because they qualify for a credit of up to 5.4% when they pay state unemployment taxes on time. That brings the effective rate down to 0.6% for most businesses, meaning the maximum FUTA tax per employee per year works out to $42.

The two-part test for who must file

You are required to file Form 940 if your business meets either of the following conditions during the current or previous calendar year:

- You paid $1,500 or more in total wages to employees in any single calendar quarter.

- You had at least one employee for any part of a day in 20 or more different weeks during the year. Those weeks do not need to be consecutive.

If you meet either condition, you must file, even if your actual FUTA tax liability turns out to be zero. Part-time, seasonal, and temporary workers all count toward the 20-week threshold.

Household employers and agricultural employers follow separate rules and use different forms, so Form 940 applies specifically to general business employers. If you run a farm or pay a household worker, check IRS Schedule H or Publication 51 for the relevant guidance before proceeding with Form 940.

Exempt payments that reduce your taxable wages

Not every dollar you hand to an employee counts as FUTA-taxable wages. Understanding these exclusions helps you calculate your taxable payroll correctly and avoid overpaying.

Common payments excluded from FUTA wages include:

| Payment Type | FUTA Treatment |

|---|---|

| Wages above $7,000 per employee | Exempt after the annual wage base is reached |

| Fringe benefits (health insurance premiums) | Generally exempt |

| Dependent care assistance up to $5,000 | Exempt |

| Group-term life insurance premiums | Exempt |

| Retirement and pension plan contributions | Exempt |

Regular cash wages, bonuses, commissions, and most other compensation count as taxable FUTA wages up to the $7,000 wage base. If you're unsure whether a specific payment qualifies as exempt, IRS Publication 15 provides the full breakdown of what counts and what does not.

Key due dates, deposits, and info to gather

Before you open the form, knowing the deadlines and having your records organized saves you from scrambling at the last minute. The IRS form 940 instructions are clear that missing key dates triggers penalties that compound quickly, so a few minutes of preparation now protects you from a larger problem later.

When Form 940 is due

The standard filing deadline for Form 940 is January 31 of the year following the tax year you're reporting. If you're filing for 2024, the return is due January 31, 2025. The IRS grants one extension: if you made all required FUTA deposits on time throughout the year, you have until February 10 to file the return. If January 31 falls on a weekend or federal holiday, the deadline shifts to the next business day.

When to make FUTA deposits

You don't wait until January to pay your FUTA tax. The IRS requires quarterly deposits whenever your cumulative FUTA liability exceeds $500 at the end of a quarter. The four quarterly deadlines are April 30, July 31, October 31, and January 31. If your liability stays at or below $500 after a given quarter, you carry it forward. Once the running total crosses $500, you must deposit by that quarter's deadline.

All FUTA deposits must go through the Electronic Federal Tax Payment System (EFTPS). Mailing a check for a required deposit is not an accepted method.

What to gather before you open the form

Having the right numbers in front of you before you start prevents errors and wasted time. Pull together the following records before working through any line on the form:

- Total wages paid to all employees during the calendar year, broken down by quarter

- State unemployment tax (SUTA) account numbers and total SUTA contributions paid for each state where you have employees

- Individual employee wage records so you can identify when each worker crossed the $7,000 wage base

- Documentation of any exempt payments such as group health insurance premiums or retirement contributions

- FUTA deposit records showing the dates and amounts you already submitted through EFTPS

Fill out Form 940 line by line

Working through the form is straightforward once your records are in order. The irs form 940 instructions organize the return into five numbered parts, and each part builds on the one before it. Move through them in sequence, and you won't need to jump back and forth.

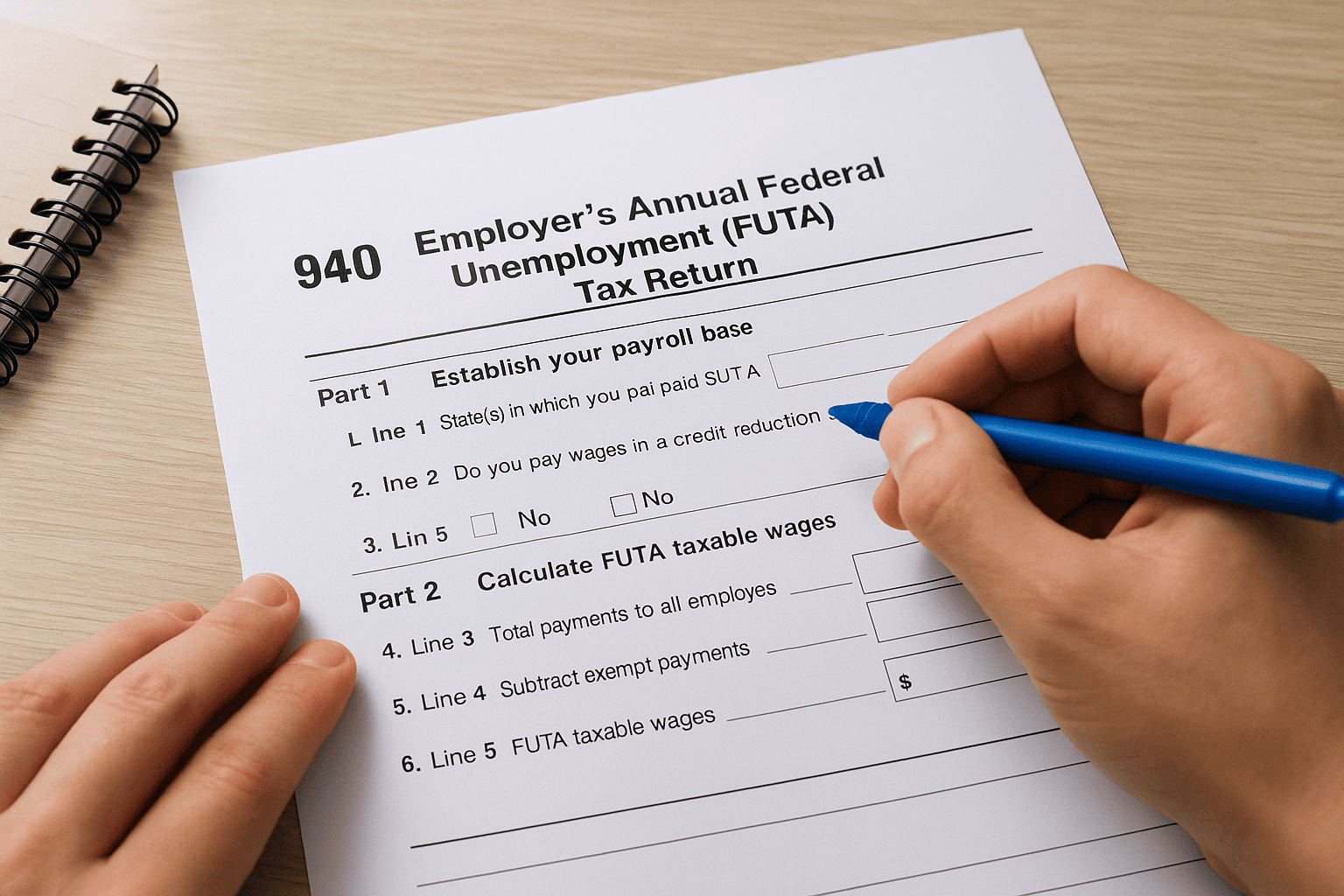

Part 1 and Part 2: Establish your payroll base

Part 1 asks whether you paid SUTA in only one state or multiple states, and whether you paid wages in a credit reduction state. Check the appropriate boxes honestly because your answers determine whether you need to attach Schedule A. Part 2 is where the actual math begins. Line 3 asks for total payments made to all employees. Line 4 captures exempt payments (health insurance premiums, retirement contributions, and similar items). Line 5 subtracts line 4 from line 3 to give you your total taxable wages before the wage base adjustment.

Line 6 accounts for wages paid above the $7,000 per-employee wage base. Enter the total wages that exceed $7,000 across all employees here. Line 7 subtracts that amount, leaving you with your FUTA taxable wages on line 7.

If any employee earned exactly $7,000 from you and nothing more, their entire wage amount is taxable. Only dollars above $7,000 per worker get excluded on line 6.

Part 3, Part 4, and Part 5: Calculate tax, apply credits, and reconcile deposits

Part 3 multiplies your taxable wages from line 7 by 6% (0.060) to produce your FUTA tax before adjustments on line 8. Lines 9 through 11 then apply your state unemployment tax credit. Line 10 is where most employers capture the full 5.4% credit for timely SUTA payments, bringing the effective rate to 0.6%.

Part 4 calculates your total FUTA tax after adjustments. Add any credit reduction amounts from Schedule A here if applicable. Part 5 reconciles your final tax amount against the quarterly deposits you already made through EFTPS. If your deposits exceed your liability, the IRS will apply the difference as a credit or issue a refund. If you owe a balance, you pay it when you file.

| Form 940 Part | What It Does |

|---|---|

| Part 1 | Identifies state filing obligations |

| Part 2 | Calculates FUTA taxable wages |

| Part 3 | Applies SUTA credit and adjustments |

| Part 4 | Produces final tax liability |

| Part 5 | Reconciles deposits against liability |

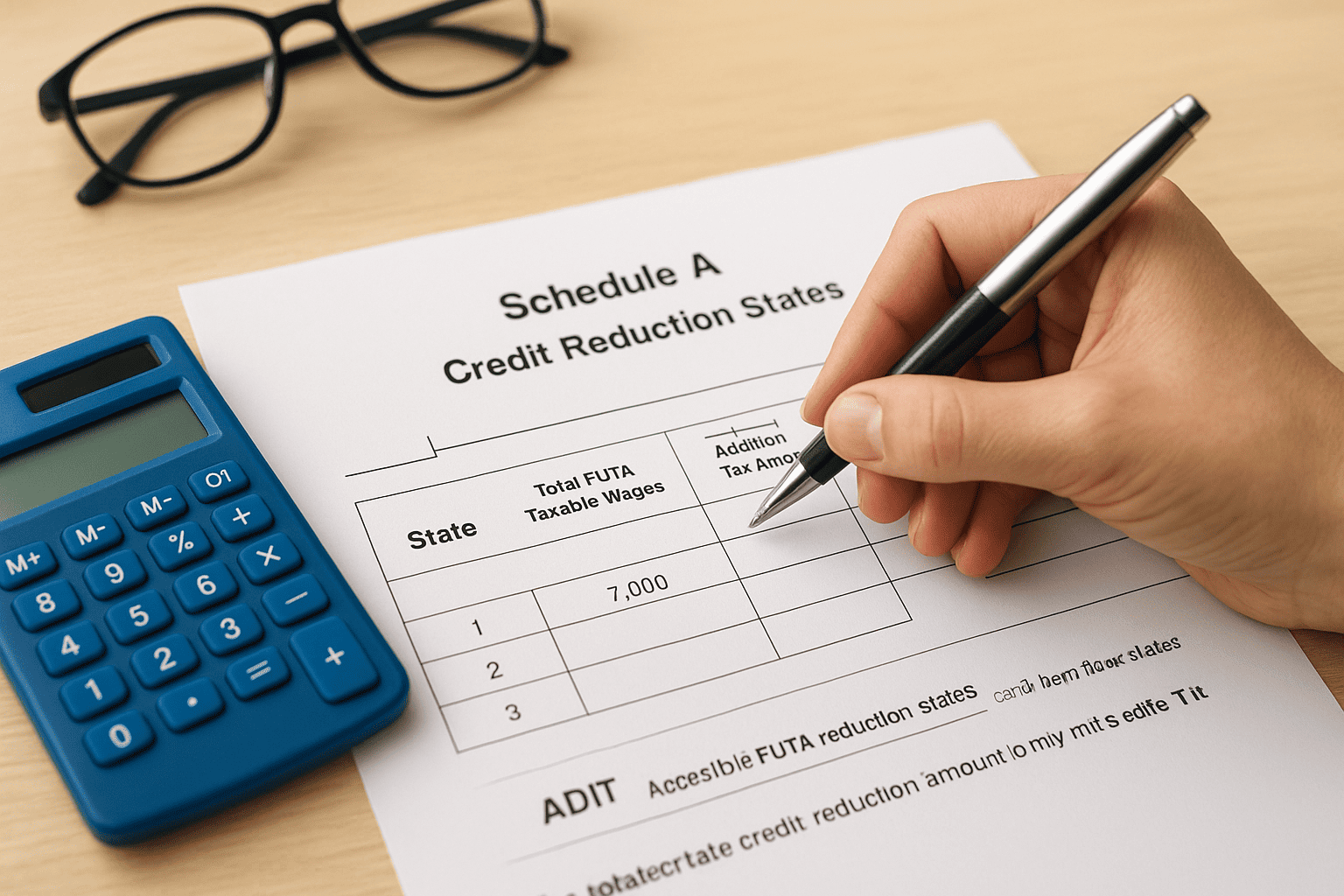

Handle Schedule A and credit reduction states

Schedule A is a one-page attachment that comes into play when you paid wages in more than one state or in any state the IRS has designated a credit reduction state. The standard FUTA credit assumes your state has fully repaid its federal unemployment loans. When a state hasn't repaid those loans on time, the IRS reduces the 5.4% credit for wages paid in that state, which means you owe more FUTA tax than the standard 0.6% effective rate.

What credit reduction means for your FUTA bill

The IRS publishes the list of credit reduction states each November, typically alongside the updated irs form 940 instructions for that tax year. Each affected state carries a specific reduction rate, usually in 0.3% increments, that stacks on top of your normal liability. If a state carries a 0.3% credit reduction, your effective FUTA rate for wages paid in that state rises from 0.6% to 0.9%.

Check the Schedule A instructions for the current tax year before you assume your state is not on the list. States move on and off the list depending on federal loan repayment activity.

Here is how the math works for a single employee earning $7,000 in a credit reduction state:

| Scenario | Rate | FUTA Tax on $7,000 |

|---|---|---|

| No credit reduction | 0.6% | $42.00 |

| 0.3% credit reduction | 0.9% | $63.00 |

| 0.6% credit reduction | 1.2% | $84.00 |

How to complete Schedule A

Schedule A lists every state where you paid wages during the year. For each state, you enter the total FUTA taxable wages paid in that state, not your total gross payroll. If a state appears on the credit reduction list, the form applies the reduction rate to those wages and calculates the additional tax amount automatically. States not on the credit reduction list require no extra calculation, but you still mark them on Schedule A if you paid wages there and are filing a multi-state return.

Once you finish Schedule A, carry the total credit reduction amount to Part 4 of Form 940. That figure adds directly to your FUTA liability before you reconcile against your deposits in Part 5.

Submit the return and avoid penalties

Once you finish the form and any required Schedule A, you have two options for submitting your return: electronic filing through IRS e-file or mailing a paper return to the IRS. The irs form 940 instructions recommend e-filing whenever possible because it reduces processing errors and provides immediate confirmation that the IRS received your return.

Where and how to file Form 940

You can e-file Form 940 through any IRS-authorized e-file provider or payroll software that supports federal employment tax returns. If you prefer to mail a paper return, the destination address depends on your state and whether you are including a payment. The IRS maintains a current list of mailing addresses in the Form 940 instructions document, and the correct address changes periodically, so always verify before you send. Use certified mail with return receipt if you file by paper so you have documented proof of the submission date.

Never mail your Form 940 to the same address used for income tax returns. The IRS routes employment tax returns to separate processing centers.

Penalties for late filing and late deposits

Filing late or depositing late both carry separate penalties, and they compound fast. The IRS calculates failure-to-file penalties at 5% of the unpaid tax per month, up to 25% total. The failure-to-deposit penalty runs on a tiered scale based on how late the deposit is:

| Days Late | Penalty Rate |

|---|---|

| 1 to 5 days | 2% of the unpaid deposit |

| 6 to 15 days | 5% of the unpaid deposit |

| 16 or more days | 10% of the unpaid deposit |

| More than 10 days after IRS notice | 15% of the unpaid deposit |

Beyond the penalty rates, the IRS charges interest on any unpaid balance from the original due date until the date you pay in full. If you missed a deposit deadline, pay as soon as possible. The IRS does consider first-time penalty abatement requests for taxpayers with a clean compliance history, so that option is worth pursuing if you face a penalty for a one-time mistake.

Wrap-up and what to do next

The irs form 940 instructions cover a lot of ground, but the process follows a clear sequence: confirm you must file, gather your wage records, work through each part of the form, attach Schedule A if needed, and submit before the January 31 deadline. Staying on top of quarterly FUTA deposits throughout the year makes the annual filing straightforward because most of your liability is already paid before you open the return.

FUTA errors rarely fix themselves. If you discover a mistake after filing, you can correct it using Form 940-X, the amended return. If you're dealing with back taxes, IRS notices, or penalties on payroll tax returns, professional help shortens the resolution timeline significantly. The team at Tax Experts of OC includes CPAs and Enrolled Agents who handle payroll tax compliance and IRS resolution for businesses across all 50 states. Schedule a free 30-minute consultation to get clear answers fast.