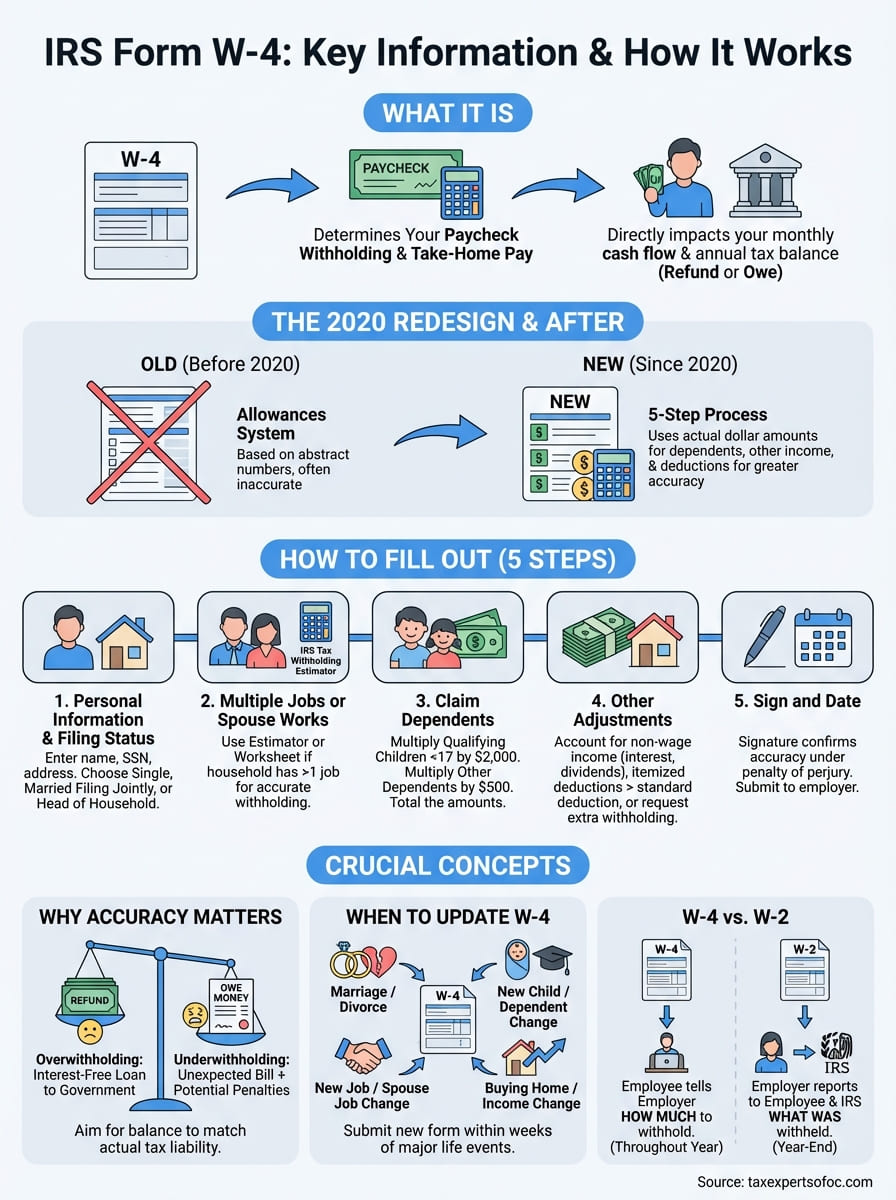

Every time you start a new job or experience a major life change, your employer hands you a form that directly impacts your take-home pay. IRS Form W-4 determines the amount of federal income tax withheld from your paycheck, get it wrong, and you could face an unexpected tax bill or give the government an interest-free loan all year.

The form was redesigned in 2020, and many taxpayers still find it confusing. Without the old "allowances" system, figuring out the right withholding requires understanding your filing status, multiple jobs, dependents, and additional income sources. Filling it out incorrectly can mean owing money at tax time or waiting months for a refund you could have had in your pocket all along.

At Tax Experts of OC, we help clients across all 50 states navigate exactly these kinds of tax questions, from simple W-4 adjustments to complex IRS disputes. This guide walks you through everything you need to know about Form W-4: what it is, how it works, and step-by-step instructions to complete it correctly so your withholding matches your actual tax liability.

Why IRS Form W-4 matters for your paycheck

Your W-4 sits at the heart of every paycheck you receive. The information you provide on this single form determines exactly how much federal income tax your employer removes from your wages before you ever see the money. This means your W-4 directly shapes your monthly cash flow, your ability to pay bills, and whether you owe money or receive a refund when you file your tax return.

Your W-4 controls how much money you take home

When you complete IRS Form W-4, you tell your employer how to calculate your withholding. Your employer uses the information about your filing status, dependents, and other income to run payroll tax calculations every pay period. The difference between your gross pay and what lands in your bank account depends entirely on what you claimed on this form.

If you claim fewer adjustments or request additional withholding, your employer takes out more tax from each paycheck. You see less money now but likely face a smaller tax bill or larger refund later. Alternatively, claiming more dependents or additional deductions means your employer withholds less, giving you bigger paychecks throughout the year but potentially creating a balance due at tax time.

Your W-4 affects every paycheck you receive for the entire year, making it one of the most important financial forms you fill out.

Incorrect withholding creates two expensive problems

Overwithholding means the IRS holds your money all year without paying you interest. If you receive a large refund every April, you essentially gave the government an interest-free loan instead of using that money for living expenses, debt payments, or investments. The average refund in 2025 exceeded $3,000, representing money that could have been in your account earning interest or reducing credit card balances.

Underwithholding creates the opposite problem. When tax season arrives, you discover you owe money to the IRS, sometimes thousands of dollars you did not budget for. The IRS may also assess underpayment penalties if you withheld too little, typically requiring you to pay at least 90% of your current year's tax liability or 100% of the previous year's tax throughout the year. These penalties add unnecessary costs on top of the tax you already owe.

The math behind your paycheck deduction

Your employer calculates withholding using the IRS tax tables combined with the information you provided on your W-4. The process starts with your gross pay for the period, then factors in your filing status (single, married filing jointly, or head of household) and any adjustments you claimed in Steps 3 through 4 of the form.

For example, a single filer earning $60,000 annually with no dependents might see roughly $600 to $700 withheld per month for federal income tax. Add two qualifying children in Step 3, and that withholding drops by approximately $330 monthly because the form accounts for the Child Tax Credit you will claim. Request an extra $100 withheld in Step 4(c), and your take-home pay decreases by that exact amount each pay period, building a cushion against other taxable income like freelance work or investment gains.

Understanding this relationship helps you make informed decisions about your withholding. You can adjust your W-4 at any time during the year to correct course if your circumstances change, rather than waiting until tax season to discover a problem you could have prevented months earlier.

What IRS Form W-4 is and who must file it

IRS Form W-4 is the official document employees use to tell their employers how much federal income tax to withhold from their paychecks. The form's full name is "Employee's Withholding Certificate," and it serves as your direct communication with your employer about your tax situation. You provide specific information about your filing status, dependents, other income, and deductions so your employer can calculate the correct withholding amount for each pay period.

The official purpose of Form W-4

The IRS created this form to help employees pay their federal income tax liability throughout the year rather than in one lump sum at tax time. Your employer uses the information you provide to calculate withholding based on current tax rates and the projected annual tax you will owe. This system spreads your tax payments across every paycheck, matching your tax obligation as closely as possible to what you actually earn.

Form W-4 only affects federal income tax withholding. Your employer still withholds Social Security and Medicare taxes separately based on fixed rates, regardless of what you claim on your W-4. The form does not change state income tax withholding either, though many states use similar forms for their own tax calculations.

Completing Form W-4 correctly means you pay the right amount of tax throughout the year without overpaying or underpaying.

Who needs to complete this form

You must fill out a W-4 every time you start a new job as a W-2 employee. Your employer cannot process your first paycheck without this form because federal law requires them to withhold income tax from your wages. If you refuse to complete the form, your employer must withhold at the highest rate as if you claimed single status with no adjustments, which typically results in maximum withholding from your paycheck.

Current employees also need to submit a new W-4 whenever their personal circumstances change. Major life events like getting married, having children, buying a home, taking on a second job, or getting divorced all affect your tax situation and require withholding adjustments. You can update your W-4 at any time during the year, and most employers process the change within one or two pay periods.

Retirees receiving pension income and individuals receiving certain unemployment benefits may also encounter Form W-4 or similar withholding certificates. The same principles apply: you tell the payer how much federal tax to withhold, though these situations may use variations like Form W-4P for pensions or Form W-4V for voluntary withholding.

What changed on the W-4 since 2020 and in 2025

The IRS completely redesigned Form W-4 in 2020, creating the biggest change to the form in decades. If you last filled out a W-4 before 2020, you will find the current version looks and works entirely different from what you remember. The agency made additional adjustments for 2025 to account for inflation, though these changes affect the underlying calculations rather than the form itself.

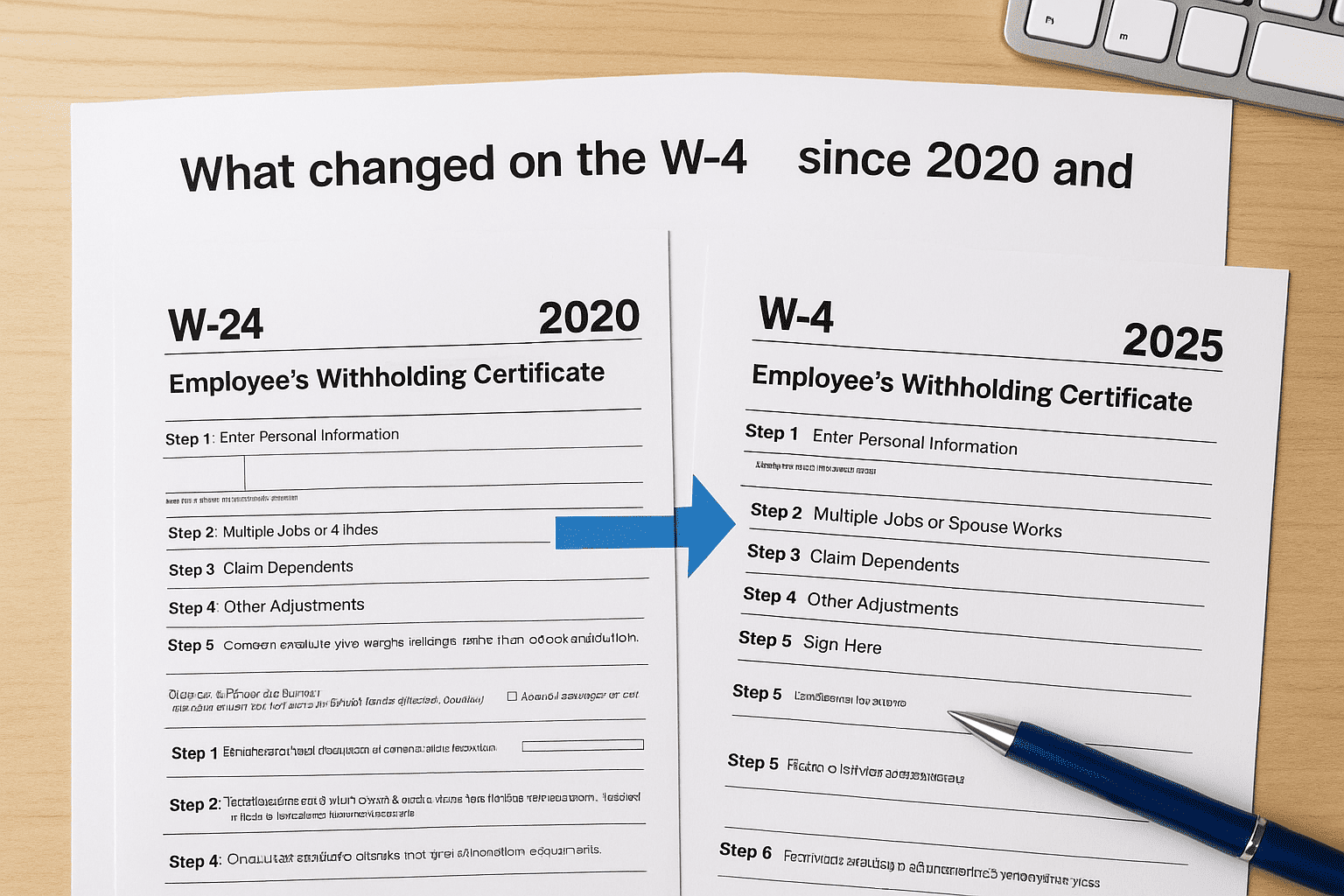

The 2020 redesign eliminated allowances

The old W-4 asked you to claim a specific number of allowances, typically one for yourself, one for your spouse, and one for each dependent. You might have claimed zero allowances for maximum withholding or five or more to significantly reduce what your employer took from your paycheck. This system disappeared completely in 2020 when the IRS released a redesigned form following the Tax Cuts and Jobs Act.

The new IRS Form W-4 uses a five-step process instead of allowances. Step 1 requires your basic information and filing status. Step 2 applies only if you hold multiple jobs or your spouse works. Step 3 claims dependents and related tax credits. Step 4 adds other income or deductions. Step 5 contains your signature. The form now asks for specific dollar amounts rather than abstract allowance numbers, making it more accurate but requiring you to do more calculation work upfront.

The 2020 redesign means you can no longer use "allowances" to adjust your withholding, forcing you to think in actual dollar amounts instead.

This change reflected the near-doubling of the standard deduction and elimination of personal exemptions under the 2017 tax law. The old allowances system no longer matched how the tax code actually worked, creating widespread under-withholding problems. Your old W-4 remains valid if you filed it before 2020 and never updated it, but any new W-4 you submit must use the current format.

The 2025 updates adjusted for inflation

The 2025 tax year brought inflation adjustments to the tax brackets and standard deduction amounts that affect your withholding calculations, though the form itself did not change structurally. The standard deduction increased to $15,000 for single filers and $30,000 for married couples filing jointly, up from $14,600 and $29,200 in 2024. These increases mean your employer withholds slightly less tax automatically because more of your income falls below the taxable threshold.

Tax bracket thresholds also shifted upward by roughly 2.8 percent for 2025. Your employer's payroll system uses these updated brackets when calculating withholding from your paycheck, even if you never submit a new W-4. However, if you fill out a fresh W-4 in 2025, the calculations you make in Steps 3 and 4 should reflect these current-year figures rather than outdated 2024 or earlier amounts to ensure accurate withholding.

What you need before you start the W-4

Gathering the right information before you open IRS Form W-4 saves time and prevents costly mistakes. You need specific numbers from your tax return, details about your household income, and a clear picture of your deductions and credits. Walking through the form without this information forces you to guess at critical figures, which typically results in incorrect withholding that costs you money throughout the year.

Your previous tax return shows your baseline

Start by locating your most recent tax return, preferably from the previous year. You need to know your total tax liability from Line 24 of Form 1040, which shows the actual amount of federal income tax you owed before credits and withholding. This number gives you a target for what your withholding should accomplish in the current year, assuming your situation remains similar.

Your return also shows the credits you claimed, including the Child Tax Credit and the Credit for Other Dependents. These amounts directly affect Step 3 of the W-4, where you multiply the number of qualifying children and dependents by specific dollar amounts. Knowing whether you qualify for these credits and how many dependents you claimed helps you accurately complete the form without underestimating your entitled benefits.

Your prior year's tax return provides the most reliable baseline for calculating correct withholding in the current year.

Job and income information you need ready

You must know the pay frequency and estimated annual wages for every job in your household. If you work two jobs or your spouse works, the W-4 requires you to account for this additional income in Step 2. Gather recent pay stubs showing your gross pay per period and multiply by the number of pay periods per year to calculate your annual income from each source.

Self-employment income, rental property income, investment gains, and other non-wage income also matter. The IRS expects you to account for these amounts in Step 4(a) so your employer withholds enough to cover the tax on all your income sources combined, not just your wages. Pull statements showing your expected annual amounts from these other sources, or use last year's figures if your situation has not changed significantly.

Dependent and deduction details to gather

List every person who qualifies as your dependent under IRS rules, including their ages. Children under 17 generate different credit amounts than other dependents, so you need to separate these categories when completing Step 3. Verify that each dependent meets the relationship, residency, and support tests before claiming them on your W-4.

Finally, estimate your itemized deductions if you plan to claim them instead of the standard deduction. Mortgage interest, property taxes, charitable contributions, and medical expenses that exceed 7.5% of your income all reduce your taxable income. You enter these amounts in Step 4(b) only if your total itemized deductions exceed the standard deduction amount for your filing status.

How to fill out IRS Form W-4 step by step

IRS Form W-4 breaks down into five numbered steps, but only Steps 1 and 5 require information from every employee. The middle three steps apply based on your specific situation, and you can skip entire sections if they do not match your circumstances. The form itself includes clear instructions for each step, but understanding what you actually need to do prevents costly withholding mistakes that affect your finances all year.

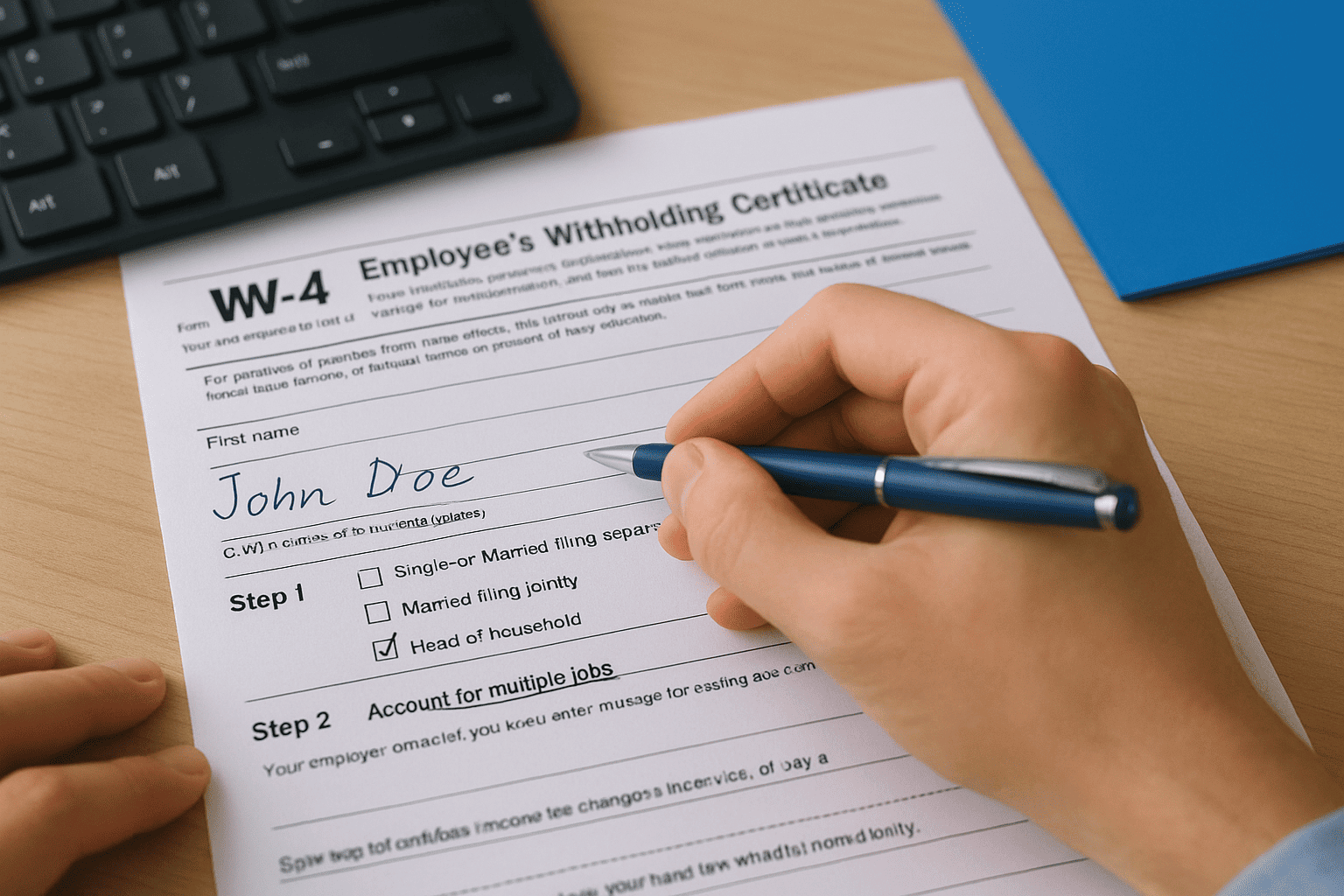

Step 1: Enter your personal information and filing status

You start by writing your full legal name, Social Security number, and current address in the spaces provided at the top of the form. Your employer needs this information to match your withholding records with your Social Security earnings record and to comply with federal reporting requirements.

Next, you check one of three filing status boxes: Single or Married filing separately, Married filing jointly, or Head of household. Your choice here determines which tax brackets and rates your employer applies to your paycheck. Choose the same filing status you plan to use on your actual tax return. Selecting "Married filing jointly" when you will actually file separately creates significant underwithholding because the joint rates assume your income is split with a spouse.

Step 2: Account for multiple jobs

Skip this entire step if you hold only one job and your spouse does not work. Otherwise, you must use one of three methods to account for additional income that affects your total tax liability. The most accurate approach uses the online Tax Withholding Estimator at IRS.gov, which calculates exactly what to enter in Step 2(c) based on all your household jobs and their pay schedules.

Alternatively, you can use the Multiple Jobs Worksheet on page 3 of the W-4 instructions if you prefer to calculate by hand. The third option requires you and your spouse to each check the box in Step 2(c) if you only hold two jobs total. This method works but results in higher withholding than the worksheet approach because it applies a conservative estimate.

Completing Step 2 correctly prevents the surprise of owing thousands in taxes because your combined household income pushed you into higher tax brackets.

Step 3: Claim your dependents

You enter the number of qualifying children under 17 and multiply by $2,000, writing the result in the first line. Add the number of other dependents (children 17 and older or qualifying relatives) multiplied by $500 on the second line. Total both amounts and enter the combined figure in Step 3. Your employer reduces your withholding by this exact amount, spread across your paychecks throughout the year.

This step only works if your total income falls below $200,000 for single filers or $400,000 for married couples. Higher incomes phase out these credits, requiring you to use the worksheet approach instead of the simplified calculation.

Step 4: Make other adjustments

Step 4(a) captures non-wage income like interest, dividends, or retirement distributions. Enter the annual amount you expect, and your employer increases withholding to cover the tax on this additional income. Step 4(b) allows you to claim deductions beyond the standard deduction if you itemize. Subtract your itemized total from the standard deduction and enter the difference, which decreases your withholding.

Step 4(c) requests any extra withholding per pay period. Enter a specific dollar amount if you want additional tax taken from each check, useful if you have irregular income or want to ensure a refund rather than a bill at tax time.

Step 5: Sign and date the form

Your signature confirms the information you provided is accurate and complete to the best of your knowledge. Federal law treats a false W-4 as perjury, carrying significant penalties. Date the form and submit it to your employer's payroll or human resources department, keeping a copy for your records.

How to handle common situations on a W-4

Life rarely follows the simple single-job scenario that makes Form W-4 straightforward. You likely face complications that require special attention to specific sections of the form, and ignoring these situations creates withholding problems that cost you money throughout the year. The good news is that the current W-4 design specifically addresses the most common scenarios employees encounter, as long as you know which steps to complete.

When you hold multiple jobs at once

If you work two or more jobs simultaneously, you must complete Step 2 on the W-4 for your highest-paying position. The simplest approach checks the box in Step 2(c), but this only works if you hold exactly two jobs total and neither you nor your spouse has additional employment. Your employer withholds as if you work only one job at a higher rate, which prevents underwithholding across your combined income.

For three or more jobs, you need to use the Multiple Jobs Worksheet included in the form instructions. This worksheet calculates the extra withholding amount needed from your highest-paying job to cover the tax liability from all your positions combined. Enter the final worksheet result in Step 4(c) of the W-4 for your primary job, and submit a basic W-4 with only Steps 1 and 5 completed to your other employers.

Coordinating your W-4 forms across multiple jobs prevents the sticker shock of owing thousands in taxes because each employer withheld as if theirs was your only income.

When your spouse works or you have non-wage income

Married couples where both spouses earn income face similar challenges to individuals with multiple jobs. Complete Step 2 on one spouse's W-4 using either the estimator tool or the worksheet method to calculate the correct withholding adjustment. The other spouse submits a basic W-4 claiming Married filing jointly status but leaves Steps 2 through 4 blank. This approach concentrates the withholding adjustment on one paycheck rather than splitting it incorrectly.

Freelance income, rental properties, and investment gains require attention in Step 4(a) of your IRS Form W-4. Calculate your expected annual amount from these sources, then enter that figure so your employer increases withholding from your regular paycheck to cover the additional tax liability. This prevents quarterly estimated tax payments and the penalties that come with underwithholding on non-wage income.

When you experience major life changes

Marriage, divorce, childbirth, or a spouse starting or stopping work all create immediate W-4 updates. Submit a new form within weeks of the change rather than waiting until year-end. A new baby qualifies you for the Child Tax Credit in Step 3, reducing your withholding by $2,000 annually. Divorce removes your ability to claim Married filing jointly status and may eliminate dependent claims, requiring you to increase withholding to avoid a surprise tax bill the following April.

How to check if your withholding is right

You cannot simply trust that your IRS Form W-4 produced the correct withholding amount. Tax laws change, your income fluctuates, and life events alter your situation throughout the year. Checking your withholding at least twice annually ensures you stay on track to owe nothing and receive no massive refund when you file your return. The IRS provides tools and methods to help you verify that the amount coming out of your paycheck matches your actual tax liability based on your current circumstances.

Check your year-to-date withholding against your actual tax

Pull your most recent pay stub and locate the year-to-date federal income tax withheld. This number shows exactly how much your employer has sent to the IRS on your behalf since January 1. Next, estimate your total annual tax liability by reviewing last year's tax return and adjusting for any income or deduction changes you expect this year. Divide that estimated annual tax by 12 to get your monthly target, then multiply by the number of months that have passed.

Compare your actual year-to-date withholding to your target amount. If you withheld $8,000 by August but your target shows you should have withheld $10,000, you face a $2,000 shortfall that will turn into a tax bill unless you submit a new W-4 requesting extra withholding. The opposite situation means you overwithhold and give the government free use of your money rather than keeping it in your account earning interest.

Use the IRS Tax Withholding Estimator

The IRS maintains a free online calculator at IRS.gov/W4App that walks you through your entire tax situation in about 10 minutes. You enter information about your jobs, spouse's income, dependents, deductions, and other income sources. The tool calculates your expected tax liability and compares it to your current withholding trajectory based on your pay stubs.

The IRS Tax Withholding Estimator provides the most accurate withholding check because it accounts for your specific combination of income sources, deductions, and credits.

At the end, the estimator tells you whether to submit a new W-4 and exactly what to enter in each step. You can run this calculator multiple times throughout the year as your situation changes, making it the single most reliable method to verify your withholding stays correct.

Watch for warning signs in your paycheck

Your withholding likely needs adjustment if your take-home pay changes significantly without a corresponding raise or reduction in hours. This often indicates your employer updated their payroll system with new tax tables, but your W-4 no longer produces appropriate withholding under those tables. Similarly, if you consistently owe more than $1,000 at tax time or receive refunds exceeding $2,000, your withholding misses the mark by substantial margins that cost you money through penalties or lost opportunity.

When to submit a new W-4 and what happens next

You control your withholding by submitting a new W-4 whenever your circumstances change, and you can update it as often as needed throughout the year. Your employer must accept and process any W-4 you submit, though the timing of when changes take effect depends on their payroll processing schedule. Understanding when to update your form and what happens after you submit it helps you maintain accurate withholding that matches your current tax situation rather than last year's circumstances.

Life events that trigger a new W-4

Marriage changes your filing status and potentially doubles your standard deduction, requiring you to submit a new W-4 within weeks of the wedding. Your employer needs to know you now qualify for Married filing jointly status, which typically reduces withholding because the tax brackets widen significantly. Divorce creates the opposite effect, pushing you back to Single or Head of household status and usually requiring increased withholding to avoid owing taxes on income that now faces higher rates.

Having a baby or adopting a child adds a dependent worth $2,000 in Child Tax Credit, which directly reduces your tax liability. Submit a new form immediately to decrease withholding and increase your take-home pay rather than waiting until tax season to claim the credit. Similarly, when your child turns 17, you lose that $2,000 credit and may need to increase withholding to compensate.

Starting a second job or your spouse beginning work requires you to update your W-4 to account for the combined household income pushing you into higher tax brackets. Buying a home, experiencing significant medical expenses, or making large charitable donations may justify updating Step 4(b) if your itemized deductions now exceed the standard deduction.

Submitting a new W-4 within two weeks of a major life event prevents months of incorrect withholding that creates tax bills or excessive refunds you could have avoided.

How your employer processes the form

Your employer reviews your W-4 for completeness and signature, then forwards it to their payroll department or service provider. They keep your form in your personnel file and do not send it to the IRS unless the agency specifically requests it during an audit. The IRS trusts your employer to maintain these records and apply the withholding you requested.

Payroll enters your W-4 information into their system, which automatically calculates the correct federal income tax withholding for each pay period based on your filing status and adjustments. Your employer cannot question your choices or refuse to process your form unless they believe you claimed exemption from withholding fraudulently.

The timing of your withholding changes

Most employers implement your new W-4 within one to two pay periods after you submit it. If you deliver your form on Monday and payday falls that Friday, your employer may not process the change until the following pay period because they already calculated the current paycheck. Companies with biweekly pay schedules typically show withholding changes faster than those paying monthly.

Check your next pay stub after submitting a W-4 to verify your employer applied the changes correctly. Your year-to-date withholding continues to accumulate, but the per-paycheck amount should reflect your new IRS Form W-4 entries. Contact payroll immediately if you see no change after two pay periods, as delays can throw off your annual withholding target.

W-4 vs W-2 and other common tax forms

Tax forms with similar names serve completely different purposes, and confusing them creates problems during tax season. While IRS Form W-4 controls your withholding throughout the year, other W-forms handle reporting, contractor payments, and different employment situations. Understanding which form does what helps you avoid filing the wrong document or missing required paperwork that triggers IRS notices or delays your refund.

How W-4 differs from W-2

You fill out a W-4 when you start a job, telling your employer how much federal income tax to withhold from your paychecks. This form stays with your employer and never gets sent to the IRS unless they specifically request it during an audit. You submit a W-4 whenever your personal situation changes, potentially updating it multiple times throughout a single year.

Your employer gives you a W-2 at the end of the tax year, typically by January 31. This form reports your actual wages earned and the total amount of taxes withheld across all your paychecks. You attach your W-2 to your tax return when you file, and your employer sends copies to both you and the IRS. The W-2 serves as proof of your income and withholding, while the W-4 simply instructs your employer how to calculate that withholding in the first place.

The W-4 controls what comes out of your paycheck during the year, while the W-2 reports what actually happened after the year ends.

How W-4 differs from W-9

The W-9 applies to independent contractors and freelancers rather than employees. When you start working as a contractor, the business hiring you requests a W-9 to collect your taxpayer identification number and confirm you are not subject to backup withholding. Unlike the W-4, a W-9 does not control any tax withholding because contractors receive their full payment without automatic deductions.

Contractors handle their own taxes through quarterly estimated payments rather than paycheck withholding. The business uses your W-9 information to prepare a Form 1099-NEC at year-end, reporting the total amount they paid you. This makes the W-9 fundamentally different from the employee-focused W-4 system.

Other tax forms you encounter

Form W-4P controls withholding from pension and annuity payments, using similar logic to the standard W-4 but applying to retirement income. Form W-4V allows you to request voluntary withholding from unemployment benefits or Social Security payments. Form 1040 serves as your actual tax return where you report all income, claim deductions and credits, and calculate whether you owe money or receive a refund based on what your W-4 withholding accomplished throughout the year.

Next steps

You now understand how IRS Form W-4 controls your paycheck withholding and affects your financial picture throughout the year. Take 10 minutes today to review your most recent pay stub and compare your year-to-date withholding against your expected tax liability. If you spot a mismatch or your circumstances changed since you last updated your form, submit a new W-4 immediately rather than waiting until tax problems develop.

Complex situations like multiple jobs, self-employment income, rental properties, or significant itemized deductions make accurate withholding calculations difficult without professional guidance. Mistakes cost you money through IRS penalties, interest charges, or tying up thousands of dollars in unnecessary refunds. Contact Tax Experts of OC for a free 30-minute consultation where our CPAs and Enrolled Agents review your complete tax situation and calculate the exact withholding amounts you need across all income sources to stay compliant while maximizing your monthly cash flow.