Months of unopened bank statements, missing receipts, and unreconciled transactions don't just create a messy desk, they create real tax exposure. If your books haven't been touched in a while, catch up bookkeeping services exist to close that gap and bring your financial records current. Whether you fell behind during a busy season, lost a bookkeeper mid-year, or simply let things slide, the longer your records stay incomplete, the harder (and more expensive) compliance becomes.

At Tax Experts of OC, our CPAs and Enrolled Agents regularly work with individuals and business owners across all 50 states who come to us with months or even years of neglected books. We handle the cleanup alongside tax preparation and resolution, so your updated records feed directly into accurate filings and, when needed, IRS negotiations. That combination matters, clean books without a tax strategy behind them only solve half the problem.

This article breaks down exactly how catch up bookkeeping works, what it typically costs, and how long the process takes from start to finish. You'll also learn what to look for in a provider and how to tell whether your situation calls for a simple cleanup or a more involved financial reconstruction.

What catch up bookkeeping services cover

Catch up bookkeeping services are not a single task but a collection of interconnected processes that rebuild your financial picture from the ground up. Depending on how far behind you are, the scope can range from reconciling a few months of transactions to reconstructing multiple years of records using bank statements, receipts, and third-party data sources. Every project starts with an assessment of the gap between your current records and where they need to be.

Bank and credit card reconciliation

Reconciliation is usually the first and most labor-intensive step. A bookkeeper pulls your bank and credit card statements for every month that is out of date, then matches each transaction to a corresponding entry in your accounting software. Any discrepancies, duplicate entries, or missing records get flagged and resolved before the work moves forward.

Skipping reconciliation and jumping straight to tax prep is one of the most common reasons amended returns become necessary later.

Your reconciled accounts give every downstream calculation a reliable foundation. Without them, profit and loss figures, balance sheets, and tax totals are all built on incomplete data, which creates compounding errors the further back the problem goes.

Transaction categorization and chart of accounts cleanup

Once transactions are reconciled, each one needs to be assigned to the correct account category. Miscategorized expenses can overstate income, understate deductions, or create discrepancies that draw IRS scrutiny. A qualified bookkeeper reviews your chart of accounts, corrects prior misclassifications, and makes sure every line item aligns with standard accounting practices and your specific industry.

This step also catches personal expenses incorrectly recorded as business costs, which is a direct audit risk for sole proprietors and small business owners who run expenses through a single account.

Payroll records, accounts payable, and receivable

If your business has employees or contractors, payroll records need to be brought current alongside the general ledger cleanup. That means verifying payroll tax deposits match what was reported, that contractor payments are properly documented, and that any 1099 obligations are accounted for. Outstanding invoices and unpaid bills also need accurate entries so your financial statements reflect what you actually owe and what others owe you.

A complete catch up project delivers records that a CPA or Enrolled Agent can use directly for tax preparation or audit defense, without reverse-engineering your finances from a partial or inconsistent set of books.

Why getting caught up matters for taxes

Your tax obligations don't pause while your books fall behind. Incomplete records create a direct chain of problems: inaccurate filings, missed deductions, and a much weaker position if the IRS ever questions your returns. Bringing your records current through catch up bookkeeping services isn't just a cleanup exercise, it's what makes defensible tax filings possible in the first place.

Unfiled or inaccurate returns carry real penalties

The IRS charges failure-to-file and failure-to-pay penalties that compound monthly, and interest accrues on any unpaid balance from the original due date. If you've filed returns using estimated or incomplete figures, you may have already understated income or overstated deductions without realizing it. Both scenarios put you at risk for IRS notices, audits, or collection actions that would have been entirely avoidable with accurate books.

The IRS can assess additional taxes, penalties, and interest going back three years on a standard audit, and up to six years if they find a substantial understatement of income.

Missing records cost you legitimate deductions

When your books are incomplete, deductible expenses often get missed entirely. Business mileage, home office costs, equipment purchases, and contractor payments all require proper documentation to survive scrutiny. Without a complete record, your tax preparer has to work from whatever you can piece together, and gaps in that picture almost always mean paying more tax than you actually owe.

Accurate books let your CPA or Enrolled Agent claim every deduction you've earned, match your reported income to third-party documents the IRS already holds, and file returns that stand up to review without revision.

How a catch up bookkeeping project works

Most catch up bookkeeping services follow a structured sequence that moves from document collection to verified, tax-ready records. Understanding how the process unfolds helps you prepare the right materials upfront and set realistic expectations for what your provider needs from you at each stage.

Step 1: Document collection and scope assessment

Your provider starts by identifying exactly how far back your records need to go and which accounts require attention. You'll typically submit bank statements, credit card statements, prior-year tax returns, and any existing accounting files. The scope assessment determines whether you're dealing with a straightforward reconciliation or a more complex reconstruction that requires sourcing records from multiple financial institutions.

The more organized your source documents are at the start, the faster and less expensive the entire project becomes.

Step 2: Reconciliation and categorization

With your documents in hand, the bookkeeper works through each period month by month, reconciling transactions and assigning them to the correct categories. This is where most of the labor is concentrated. Your accountant will flag any missing statements, unexplained transfers, or tax-sensitive entries that need your clarification before the records can be finalized and signed off.

Step 3: Review and delivery

Once the books are clean, your provider prepares a summary of completed work and delivers finalized financial statements, including a profit and loss report and a balance sheet for each period covered. At Tax Experts of OC, this final step connects directly to tax preparation or IRS resolution, so your updated records immediately serve a practical purpose beyond the cleanup itself rather than sitting in a folder collecting dust.

Catch up bookkeeping pricing in the US

Catch up bookkeeping services pricing in the US is project-based rather than fixed, because the scope varies significantly from one client to the next. The two main factors that drive cost are how many months of records need attention and how complex your accounts are.

Providers who offer flat-rate pricing per month of backlog are generally easier to budget for than those who quote hourly without a project cap.

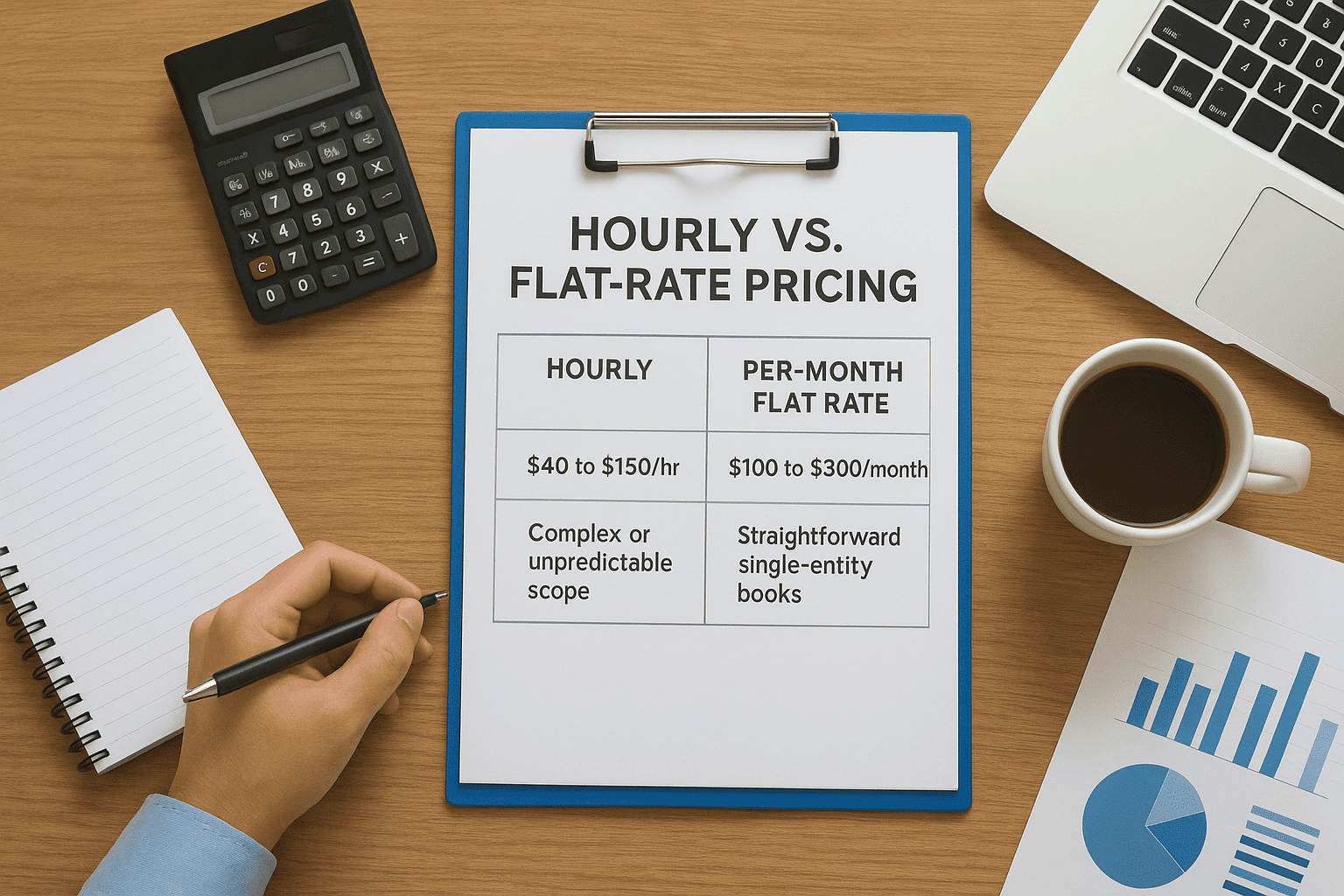

Hourly vs. flat-rate pricing

Most providers use one of two structures. Hourly rates typically range from $40 to $150 per hour depending on credentials and location. Flat-rate pricing charges a set fee per month of cleanup, usually between $100 and $300 for straightforward books with one or two accounts.

Here's a quick comparison of both models:

| Pricing Model | Typical Range | Best For |

|---|---|---|

| Hourly | $40 to $150/hr | Complex or unpredictable scope |

| Per-month flat rate | $100 to $300/month | Straightforward single-entity books |

What drives costs up

Several variables push your total cost higher regardless of the pricing model your provider uses. Missing statements, multiple bank accounts, and payroll records each add meaningful time to the project. Businesses with more than one entity, or those whose cleanup connects to an IRS notice, should expect a larger engagement than a simple reconciliation.

Your best move is to get a written scope estimate before work begins so you know exactly what the quoted price covers and what would trigger additional charges further into the project.

Typical timelines and what slows projects down

How long your catch up bookkeeping services project takes depends primarily on how many months of records need attention and how quickly you can provide the necessary documents. A simple three-month cleanup for a single-entity business with one bank account typically wraps up in one to two weeks. A full-year reconstruction involving multiple accounts, payroll records, and missing statements can take four to eight weeks or longer.

What a typical project looks like by size

Short projects covering one to three months of backlog move quickly because the transaction volume is manageable and most source documents are readily available. Mid-range projects spanning four to twelve months generally take two to four weeks, assuming you can provide complete bank statements without gaps. Multi-year reconstructions sit in a different category entirely and often overlap with tax preparation or IRS resolution work, which extends the timeline further.

The single biggest factor in your project timeline is how fast you respond to document requests and clarifying questions from your provider.

What slows projects down

Missing bank statements are the most common delay. If your provider has to request records directly from your financial institution, that process alone can add one to two weeks. Multiple entities or commingled personal and business accounts also slow the work significantly because every transaction requires more judgment before it can be categorized correctly.

Incomplete payroll records and undocumented transfers between accounts create similar friction. You can reduce delays by gathering your statements, prior tax returns, and any existing accounting files before your first meeting with your bookkeeper.

Getting your books back on track

Falling behind on your books is a problem with a clear solution, and the sooner you start, the lower your total cost and tax exposure will be. Catch up bookkeeping services give you a complete, accurate financial record that supports every decision you make going forward, from filing accurate returns to negotiating with the IRS from a position of documented fact rather than guesswork. The longer you wait, the more months pile onto the project scope and the fewer options you have.

Your books don't need to be perfect before you reach out to a professional. You just need to start the process. At Tax Experts of OC, our CPAs and Enrolled Agents handle the cleanup and connect it directly to your tax preparation or resolution work, so nothing falls through the gaps. Schedule your free 30-minute consultation and get a clear picture of what it takes to bring your records current.