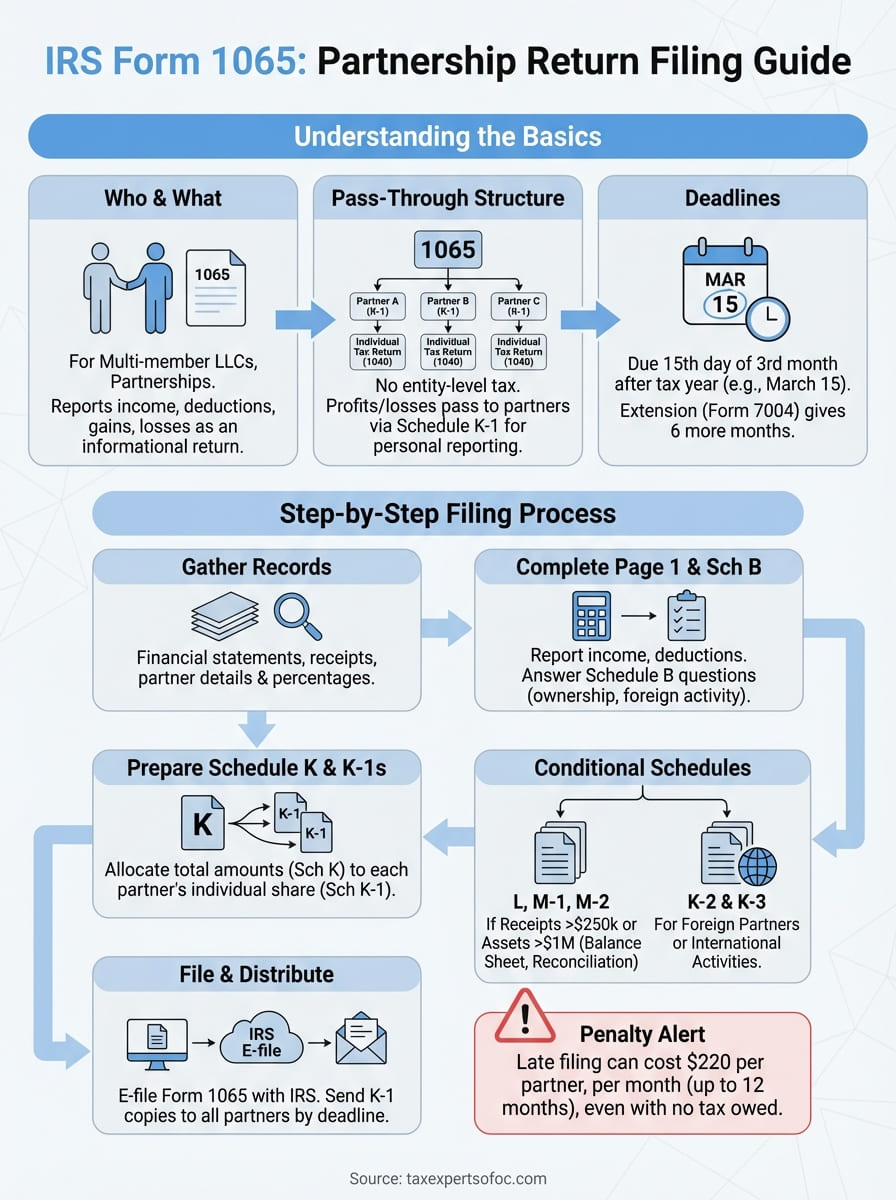

Filing a partnership tax return isn't optional, it's required by federal law, and getting it wrong can trigger penalties, delays, and unwanted IRS attention. The IRS Form 1065 instructions can feel overwhelming at first glance, with multiple schedules, income allocations, and strict deadlines to manage. For multi-member LLCs and partnerships, understanding exactly what the IRS expects is the difference between a smooth filing season and months of back-and-forth corrections.

Form 1065 itself doesn't calculate taxes owed by the partnership. Instead, it's an informational return that reports income, deductions, gains, and losses to the IRS. The actual tax burden passes through to individual partners, who then report their share on personal returns using Schedule K-1. This structure creates layers of complexity, especially when partners have different ownership percentages or the business operates across multiple states.

This guide breaks down every section of Form 1065 with clear, practical steps you can follow from start to finish. At Tax Experts of OC, our CPAs and Enrolled Agents prepare partnership returns for businesses across all 50 states, and we've seen firsthand where filers commonly stumble. Whether you're handling this yourself or want to know what your tax professional should be doing, you'll find the answers here.

What Form 1065 is and who must file it

Form 1065 is the U.S. Return of Partnership Income, which the IRS requires partnerships to file annually. This form reports the partnership's gross income, deductions, gains, losses, and credits for the tax year, but it doesn't calculate tax owed at the partnership level. Instead, the form acts as an information return that shows how the business performed and how profits or losses get distributed among partners.

The partnership itself pays no federal income tax. Instead, you pass through all tax liability to individual partners, who report their share on personal tax returns using the Schedule K-1 they receive from the partnership. This pass-through structure means Form 1065 serves as the foundation document that connects business activity to individual tax obligations, making accuracy critical for everyone involved.

Every domestic partnership operating for any part of the tax year must file Form 1065, regardless of whether it made a profit or loss.

Partnership entities that must file

You must file Form 1065 if your business operates as a general partnership, limited partnership (LP), limited liability partnership (LLP), or multi-member LLC taxed as a partnership. The IRS considers any unincorporated organization with two or more members conducting a trade, business, financial operation, or venture to be a partnership. Even if you haven't formally registered your partnership with your state, the federal tax treatment still applies once you start operating with a partner.

Multi-member LLCs default to partnership taxation unless you elect corporate treatment by filing Form 8832. If you've made this election, you file Form 1120 or 1120-S instead of Form 1065. Single-member LLCs never file Form 1065 because the IRS treats them as disregarded entities, requiring the owner to report business income on Schedule C or Schedule E of their personal return.

Foreign partnerships also file Form 1065 if they have U.S.-source income, gain, or loss, or if they have income effectively connected with a U.S. trade or business. The filing requirements extend beyond just domestic operations, and international partnerships often face additional schedule complexity with Forms 8865 and other international reporting.

Key filing deadlines and extensions

You must file Form 1065 by the 15th day of the third month following the end of your tax year. For calendar-year partnerships, this means a deadline of March 15. If you operate on a fiscal year, count three months from your year-end date. Missing this deadline triggers penalties that start at $220 per partner per month (or partial month) the return is late, up to 12 months maximum.

Extensions give you an automatic six additional months when you file Form 7004 before the original deadline. This pushes a calendar-year partnership's due date to September 15, but remember that an extension to file is not an extension to pay. If your partners owe estimated taxes based on partnership income, those payments still follow the quarterly estimated tax schedule regardless of the filing extension.

The IRS Form 1065 instructions specify that you must furnish Schedule K-1 copies to each partner by the same date your partnership return is due, including extensions. This coordination matters because partners need their K-1 to complete their own tax returns. If you delay your partnership filing, you force every partner to either file their own extension or file without complete information, which often leads to amendments later.

What you need before you start

Gathering the right documents before you open Form 1065 saves hours of backtracking and prevents errors that trigger IRS notices. You need specific financial records, partnership details, and partner information ready before you start filling out any schedules. The IRS Form 1065 instructions assume you have organized records that accurately reflect the partnership's financial activity for the entire tax year, and missing even one key document can derail your filing timeline.

Financial records and accounting documentation

Start with your year-end financial statements, including a complete profit and loss statement and balance sheet. These documents form the backbone of Form 1065 because you'll transfer income and expense totals directly from your accounting records to the tax return. If you use accounting software like QuickBooks or Xero, run reports for the full tax year and verify that all transactions have been categorized correctly.

You also need bank statements, credit card statements, and receipts that support your reported income and deductions. The IRS can request substantiation for any item on your return, so maintain records for at least three years after filing (longer if you have international operations or significant assets). Keep digital copies organized by category, such as office expenses, travel costs, and equipment purchases, to make future audits easier to handle.

Partnerships with gross receipts exceeding $250,000 or total assets over $1 million must complete Schedules L, M-1, and M-2, which require detailed balance sheet and reconciliation information.

Partnership and partner information

You must provide the partnership's Employer Identification Number (EIN) and complete legal name exactly as registered with the IRS. Include the business address where you maintain books and records, along with the principal business activity code from the instructions that best describes your primary income source. If this is your first year filing, confirm that you've already applied for your EIN through IRS Form SS-4.

Collect each partner's full legal name, Social Security Number or EIN, and current address. You need their exact ownership percentages for both profit and loss sharing, as these determine how you allocate income on Schedule K-1. Partners who joined or left during the year require special attention because you must track their ownership period and calculate their share based on the time they held their partnership interest, not the full year.

Document any guaranteed payments made to partners for services or capital use, separate from their distributive share of income. Track capital contributions and distributions for each partner throughout the year because these transactions affect their basis and appear on both Schedule K-1 and the partnership's capital accounts.

Step 1. Set up the return basics on page 1

Page 1 of Form 1065 establishes your partnership's identity with the IRS and sets foundational details that affect how you complete the rest of the return. You'll fill out the top section first, entering your partnership's exact legal name as it appears on your EIN application, then your EIN in the designated box. The IRS Form 1065 instructions emphasize that any mismatch between your legal name and EIN can delay processing or trigger correspondence from the IRS asking you to verify your identity.

Partnership identification and return type

Enter your business address exactly as the IRS has on record, using the address where you maintain your books and records. If you've moved since last year's filing or this is your first return, make sure this matches any address updates you've submitted to the IRS. You must also provide the date your partnership began business operations, which usually corresponds to when you first started generating revenue or incurring expenses in the partnership's name.

Check the appropriate boxes that describe your return. Mark whether this is an initial return, final return, name change, address change, or amended return. If you're dissolving the partnership, check the final return box and complete Schedule K-1 for all partners showing their final distributive shares. These checkboxes tell the IRS how to process your return and what to expect in future years.

Business activity and accounting details

Select your principal business activity code from the list in the IRS Form 1065 instructions that best matches your primary source of income. This six-digit code helps the IRS categorize your business for statistical purposes and determines which audit guidelines apply to your return. You'll also enter a brief description of your principal product or service in plain language that anyone can understand.

Mark your accounting method as cash, accrual, or other. Most small partnerships use cash basis accounting, which records income when received and expenses when paid. Accrual accounting records transactions when they occur regardless of cash movement. If you're required to use accrual accounting based on your gross receipts, you cannot elect cash basis without IRS permission through Form 3115.

Partnerships with average annual gross receipts exceeding $27 million over the prior three years must use accrual accounting and cannot elect the cash method.

Partner count and signature requirements

Count the number of Schedules K-1 you're filing and enter that total in the designated box. This number should match your total partner count, with one K-1 for each partner regardless of their ownership percentage. The general partner or authorized person must sign and date the return, then provide their title and phone number for IRS contact if questions arise during processing.

Step 2. Report income, deductions, and payments

Lines 1 through 22 on page 1 capture your partnership's financial activity for the year, forming the foundation for your Schedule K allocations to partners. You transfer totals from your accounting records into each designated line, following the categories the IRS Form 1065 instructions define. Every dollar of income and every deductible expense flows through these lines before you allocate them to individual partners, so accuracy here prevents K-1 errors that force amended returns later.

Income reporting on lines 1 through 8

Report your gross receipts or sales on line 1a, then subtract returns and allowances on line 1b to arrive at your net income from operations on line 1c. This figure represents your core business revenue before any expenses. If you sold business property or securities, you'll complete Form 4797 or Schedule D separately and enter the gain or loss on lines 4 or 5, depending on whether the assets were ordinary business property or capital assets.

Line 6 captures other income not reported elsewhere, including items like cancellation of debt income, recapture of prior deductions, or income from partnerships in which your partnership is a partner. Attach a statement describing each type of other income and its amount. You sum lines 1c through 6 to calculate total income on line 7, which becomes the starting point for your deduction calculations on line 8.

Partnerships cannot deduct charitable contributions, Section 179 deductions, or domestic production activities deductions at the entity level because these items pass through to partners on Schedule K.

Deductions reported on lines 9 through 21

Enter ordinary and necessary business expenses on lines 9 through 20, matching the categories listed on the form. These include salaries and wages (line 9), guaranteed payments to partners (line 10), repairs and maintenance (line 11), bad debts (line 12), rent (line 13), taxes and licenses (line 14), and interest expense (line 15). You report depreciation on line 16a, but only after completing Form 4562 if you placed property in service during the year or claimed Section 179 deductions.

Depletion appears on line 17 for partnerships with natural resource operations. Line 18 covers retirement plans and employee benefits, while line 19 captures other deductions not specifically listed. Attach a detailed statement for line 19 showing each expense type and amount. Your total deductions appear on line 21 after you sum lines 9 through 20.

Calculating ordinary business income

Subtract line 21 (total deductions) from line 7 (total income) to determine your ordinary business income or loss on line 22. This figure flows to Schedule K, line 1, where you allocate it among partners based on their profit-sharing ratios. If line 22 shows a loss, you enter it as a negative number, and partners will report their share as a loss on their personal returns.

Step 3. Answer Schedule B other information

Schedule B requires you to answer 14 yes/no questions that help the IRS understand your partnership's structure, transactions, and compliance with various tax rules. You find this section on pages 2 and 3 of Form 1065, immediately after the income and deduction lines. The IRS Form 1065 instructions provide detailed guidance for each question, and your answers determine whether you need to attach additional forms or statements to support your return.

Questions about ownership and structure

Questions 1 through 4 focus on the types of partners in your business and ownership changes during the year. You answer question 1a by indicating whether your partnership has any partners who are partnerships, corporations, trusts, tax-exempt organizations, or foreign entities. If you check yes, question 1b requires you to attach Schedule B-1 (Form 1065) listing information about each such partner, including their EIN and type.

Question 2 asks if the partnership owns foreign or domestic disregarded entities, while question 3 covers whether you own interests in other partnerships. You must answer question 4 about partnership interest transfers during the year, which includes sales, exchanges, or gifts of partnership interests. Any yes answer to question 4 triggers reporting requirements on Schedule K-1 for affected partners and may require additional forms.

Failing to disclose ownership changes or foreign activities on Schedule B can result in penalties and increased audit scrutiny, even if no tax is owed.

Foreign transactions and specialized situations

Questions 5 through 9 address international and cross-border activities. You indicate whether your partnership has foreign partners, owns foreign assets, receives distributions from foreign trusts, or maintains foreign bank accounts. Question 5b specifically asks about requirements to file Forms 8865 or 8858, which report foreign partnership interests and disregarded entities. Accurate answers here prevent international reporting penalties that start at $10,000 per form.

Questions 10 through 14 cover specialized tax situations including debt cancellation, liability assumptions, partnership terminations, and Section 754 elections. You answer question 13 about whether your partnership has made or plans to make a Section 754 election, which allows basis adjustments when partnership interests transfer or distribute. Question 14 asks about filing requirements for Forms 8918, 1042, 1065-B, or 8804, which apply to publicly traded partnerships, foreign partner withholding, and other specific situations.

Attach explanatory statements for any yes answers that require additional detail. You mark each question clearly with an X in the appropriate box, and you verify your answers against your financial records and transaction history for the year before signing the return.

Step 4. Complete Schedule K and prepare K-1s

Schedule K consolidates all partnership-level income, deductions, and credits that you must allocate to partners on their individual Schedule K-1 forms. You transfer specific amounts from page 1 and other schedules to Schedule K, then divide each line item among partners according to their profit and loss sharing percentages. The IRS Form 1065 instructions provide line-by-line guidance for both Schedule K and K-1, which function as companion forms that must reconcile perfectly before you file.

Allocating items on Schedule K

You report your partnership's ordinary business income from line 22 of page 1 on Schedule K, line 1. Lines 2 through 11 capture various types of income and losses that receive special tax treatment at the partner level, including net rental real estate income, other rental income, guaranteed payments, interest income, dividends, royalties, net short-term capital gain, and net long-term capital gain. Each of these items passes through to partners separately because they face different tax rates or limitations on personal returns.

Lines 12 through 13d break out specific deductions and Section 179 expenses that partners claim individually rather than at the partnership level. You report charitable contributions on line 13a, investment interest expense on line 13b, and Section 179 deduction on line 13c. Credits appear on lines 14 and 15, including the low-income housing credit and other tax credits your partnership qualifies for during the year.

Partners cannot deduct more than their basis in the partnership, so accurate Schedule K-1 reporting determines whether they can use losses immediately or must carry them forward.

Self-employment earnings information goes on line 14a, while foreign transactions and alternative minimum tax items appear on lines 16 through 18. You attach supporting schedules for items reported on line 20, which captures other information partners need for their individual returns.

Preparing individual Schedule K-1 forms

You create a separate Schedule K-1 for each partner using the allocation percentages from your partnership agreement. Enter each partner's name, address, SSN or EIN, and their beginning and ending capital account balances in Part II. Part III contains the actual allocation of income, deductions, and credits that flows from Schedule K, with each partner receiving their proportionate share based on ownership.

Box 1 of each K-1 shows that partner's share of ordinary business income or loss from Schedule K, line 1. You continue through all applicable boxes, entering each partner's allocated amount for rental income, guaranteed payments, dividends, capital gains, and other items. Your Schedule K totals must equal the sum of all amounts reported across every partner's K-1 for each line item, creating a built-in verification method that catches allocation errors.

Track each partner's capital account using the tax basis method unless you've elected to use GAAP or Section 704(b) book method. You report beginning capital, current year increases from income and contributions, decreases from distributions and losses, and ending capital in Part II of their K-1.

Step 5. Handle Schedules K-2 and K-3

Schedules K-2 and K-3 report international tax information that affects partners with foreign activities or foreign partners in the partnership. You file Schedule K-2 at the partnership level to report items like foreign taxes paid, foreign-sourced income, and other international transactions. Schedule K-3 works like Schedule K-1 but specifically addresses foreign tax items that each partner needs for their individual return, including foreign tax credit calculations and income sourcing details.

When you must file these schedules

You must complete both schedules if your partnership has foreign partners, foreign operations, or international transactions during the tax year. This includes partnerships that earn income from foreign sources, pay taxes to foreign governments, or have partners who are nonresident aliens or foreign entities. The IRS Form 1065 instructions specify that you can skip these schedules only if you check the domestic filing exception box on Schedule B and meet specific criteria showing no foreign activity or foreign partners.

Partnerships claiming the domestic exception must verify that no partner is foreign, the partnership has no foreign transactions, and no partner needs international tax information for their individual returns. You check box 5 on Schedule B, question 5a, to claim this exception. Missing these schedules when required can prevent partners from claiming foreign tax credits they're entitled to and may trigger IRS inquiries about incomplete reporting.

Partnerships with any foreign activity must provide Schedule K-3 to affected partners by the same deadline as Schedule K-1, or risk penalties for incomplete partner reporting.

Completing Schedule K-2 partnership-level items

Schedule K-2 contains five parts that capture different types of international information. Part I reports partnership-level foreign tax credits and other items. Part II breaks down income by country and category. Part III covers other international information including controlled foreign corporations and passive foreign investment companies. You complete only the parts that apply to your specific foreign activities, leaving irrelevant sections blank.

Transfer totals from Schedule K-2 to the corresponding lines on Schedule K, then allocate each partner's share to their individual Schedule K-3. You calculate foreign taxes paid by multiplying your total foreign tax by each partner's ownership percentage, adjusted for any special allocations in your partnership agreement.

Preparing Schedule K-3 for each partner

You generate a separate Schedule K-3 for every partner, similar to how you handle Schedule K-1. Each K-3 shows that partner's allocated share of foreign-sourced income, foreign taxes paid, and other international items from Schedule K-2. Partners use this information to complete Form 1116 on their personal returns to claim foreign tax credits or to properly source their income for other international tax purposes.

Input each partner's share of foreign taxes on Part I, their foreign-sourced income by category on Part II, and any applicable Part III information. Your Schedule K-2 totals must equal the sum of all amounts across every partner's Schedule K-3, providing a built-in reconciliation check before you file the return.

Step 6. Finish Schedule L, M-1, and M-2

Schedules L, M-1, and M-2 complete your partnership's financial picture by showing balance sheet details, book-to-tax reconciliation, and changes in partner capital accounts. You must file these schedules if your partnership has total receipts of $250,000 or more, or total assets of $1 million or more at the end of the tax year. The IRS Form 1065 instructions let smaller partnerships skip these schedules by checking the appropriate box on page 1, but completing them provides valuable documentation that prevents questions during IRS examinations and helps you maintain accurate capital accounts for Schedule K-1 reporting.

Balance sheet preparation on Schedule L

You report your partnership's assets, liabilities, and capital accounts using Schedule L, which shows beginning-of-year and end-of-year balances side by side. Start with assets on lines 1 through 14, listing cash, receivables, inventory, investments, and fixed assets. You report accumulated depreciation as a negative number on line 10b, which reduces your depreciable assets to their net book value on line 10c.

Liabilities appear on lines 15 through 18, including accounts payable, mortgages, and other debts. You calculate total liabilities and capital by adding lines 15 through 17 on line 18, then report each partner's capital account on line 19. Lines 20 through 22 must balance so that total assets equal total liabilities plus capital, creating a standard double-entry bookkeeping verification that catches errors before filing.

Your Schedule L balances must match your accounting records exactly, or you'll face questions about unrecorded transactions or missing adjustments during an IRS review.

Reconciliation on Schedule M-1

Schedule M-1 bridges the gap between your book income and taxable income by adjusting for items treated differently under GAAP and tax rules. You start with net income from your books on line 1, then add back expenses recorded on your books but not deductible for tax purposes on lines 2 through 5. Common additions include charitable contributions, meals and entertainment limitations, and depreciation differences between book and tax methods.

Lines 6 and 7 capture income reported for tax purposes but not included in book income, while line 8 deducts items recorded in book income but not taxable. You calculate the taxable income that should match Schedule K on line 9, providing a reconciliation that verifies your return's internal consistency.

Analysis of changes on Schedule M-2

Schedule M-2 tracks movement in partner capital accounts throughout the year by category. You report beginning balances in column (a), then show capital contributions in column (b), net income components in column (c), and distributions in column (d). Column (e) displays your ending capital balance that must match line 19 of Schedule L and reconcile to the total of all partner capital accounts shown on their Schedule K-1 forms.

Step 7. File on time and choose e-file or mail

You submit Form 1065 either electronically through the IRS e-file system or by mailing a paper copy to the designated service center. Electronic filing processes your return faster, reduces errors through built-in validation checks, and provides immediate confirmation that the IRS received your submission. The IRS Form 1065 instructions include specific mailing addresses by location if you choose paper filing, and these addresses change based on whether you include a payment with your return.

Electronic filing through authorized providers

You e-file Form 1065 through an IRS-authorized e-file provider or tax software that supports partnership returns. The software validates your entries against IRS rules before transmission, catching math errors and missing information that would otherwise delay processing. You receive an acknowledgment within 48 hours confirming the IRS accepted your return, giving you proof of timely filing if you submit near the deadline.

Most partnerships use commercial tax software like Intuit ProConnect, Drake Tax, or Thomson Reuters UltraTax to prepare and transmit returns electronically. These platforms handle Schedule K-1 generation automatically and submit all required schedules together as a single transmission. You can also e-file through a tax professional who has Authorized IRS e-file Provider status, allowing them to submit returns on your behalf after you review and approve the completed forms.

E-filed returns typically process in two to three weeks compared to six to eight weeks for paper returns, giving partners their Schedule K-1 forms faster for their personal tax filings.

Mailing paper returns to IRS service centers

You mail paper Form 1065 to the address listed in the instructions based on your principal business location. If you owe no payment and maintain your principal office in California, for example, you send your return to the Department of the Treasury, Internal Revenue Service Center, Ogden, UT 84201-0011. Different addresses apply to other states and situations where you include payment with your return.

Attach all required schedules in the order listed in the instructions, with Schedule K-1 copies for each partner included behind Schedule K. Use certified mail with return receipt requested to prove you mailed your return by the deadline. Keep your mailing receipt and tracking information because the IRS considers your filing date to be the postmark date, not when they receive or process your return.

Fix mistakes, avoid penalties, and resolve issues

Errors on Form 1065 happen more often than you might expect, and catching them early prevents complications that multiply across every partner's personal return. You file Form 1065-X (Amended Return) to correct mistakes after you've submitted your original return, but you must identify what went wrong and understand the specific correction procedures outlined in the IRS Form 1065 instructions before you start making changes. Acting quickly when you discover errors keeps penalty exposure minimal and shows good faith to the IRS.

Amending returns with Form 1065-X

You complete Form 1065-X when you need to change income amounts, correct deductions, fix partner allocations, or update any information reported on your original return. The form uses a three-column format showing your original amounts, net changes, and corrected totals. You explain each correction in Part III, providing specific details about what changed and why the original return contained incorrect information.

File Form 1065-X within three years from your original filing date or two years from when you paid the tax, whichever is later. Attach corrected Schedule K-1 forms for all affected partners, and mark them clearly as amended. Partners must then file Form 1040-X on their personal returns if the changes affect their individual tax liability, creating a cascade effect that makes accuracy critical at the partnership level.

The IRS assesses penalties starting at $220 per partner per month for late returns, making timely filing and corrections essential to avoid thousands in unnecessary charges.

Common penalties you can prevent

Late filing penalties accumulate fast because the IRS multiplies the base penalty by your partner count. A partnership with five partners filing three months late faces $3,300 in penalties ($220 × 5 partners × 3 months), even if no tax is owed. You avoid this entirely by filing Form 7004 before your deadline to secure an automatic extension, or by filing your return on time with whatever information you have available.

Missing or incorrect Schedule K-1 information triggers separate penalties when partners cannot accurately report their distributive shares. You prevent these issues by maintaining detailed capital account records throughout the year and reconciling partner basis before you prepare K-1 forms.

Responding to IRS notices and audits

Open and read any IRS correspondence immediately when it arrives. Most notices request clarification or additional documentation rather than alleging fraud, so you can resolve many issues with a simple response letter and supporting records. You have 30 days to respond to most notices, and missing this deadline converts manageable problems into formal collection actions.

Partnership audits follow centralized audit procedures under CPAR rules, where the partnership handles the examination rather than individual partners. You designate a partnership representative who has authority to bind all partners to settlement agreements.

Wrap up and next steps

You now have a complete roadmap for preparing and filing Form 1065, from gathering financial records through submitting your return and handling corrections. Following the IRS Form 1065 instructions systematically reduces errors that affect both your partnership and every individual partner's tax situation. Your next priority should be verifying all partner information matches your records before you generate Schedule K-1 forms, since these documents drive each partner's personal tax filing.

Start your preparation at least 30 days before your deadline to allow time for questions, missing information, and unexpected schedule complexity. If you discover international transactions, multiple business activities, or specialized allocations that make the return complicated, professional guidance prevents costly mistakes that take years to unwind.

Partnership taxation involves layers of rules that affect both entity-level reporting and individual partner obligations. Tax Experts of OC provides nationwide partnership return preparation with direct access to CPAs and Enrolled Agents who handle complex multi-state filings daily. Schedule your free consultation today to ensure your Form 1065 meets all IRS requirements without triggering penalties or audit flags.