Every quarter, employers across the United States must report withheld income taxes, Social Security, and Medicare taxes to the IRS. Form 941, the Employer's Quarterly Federal Tax Return, is how you do it. Whether you're filing for the first time or need a refresher, having clear IRS Form 941 instructions makes the difference between a smooth submission and costly penalties that can snowball fast.

The form itself isn't complicated once you understand each line item. But the IRS instructions PDF can feel dense, and missing a calculation or deadline creates problems you don't want, think interest charges, trust fund recovery penalties, or unwanted IRS attention. That's why understanding the step-by-step process matters, especially when your business's payroll tax compliance is on the line.

At Tax Experts of OC, we help employers nationwide handle payroll tax filings, resolve IRS disputes, and stay compliant quarter after quarter. This guide breaks down everything you need to know about completing Form 941 for 2026: what each section requires, how to calculate your tax liability, filing deadlines, and where to submit. By the end, you'll have the clarity to file confidently, or know exactly when to call in a CPA or Enrolled Agent for backup.

What Form 941 covers for 2026 filings

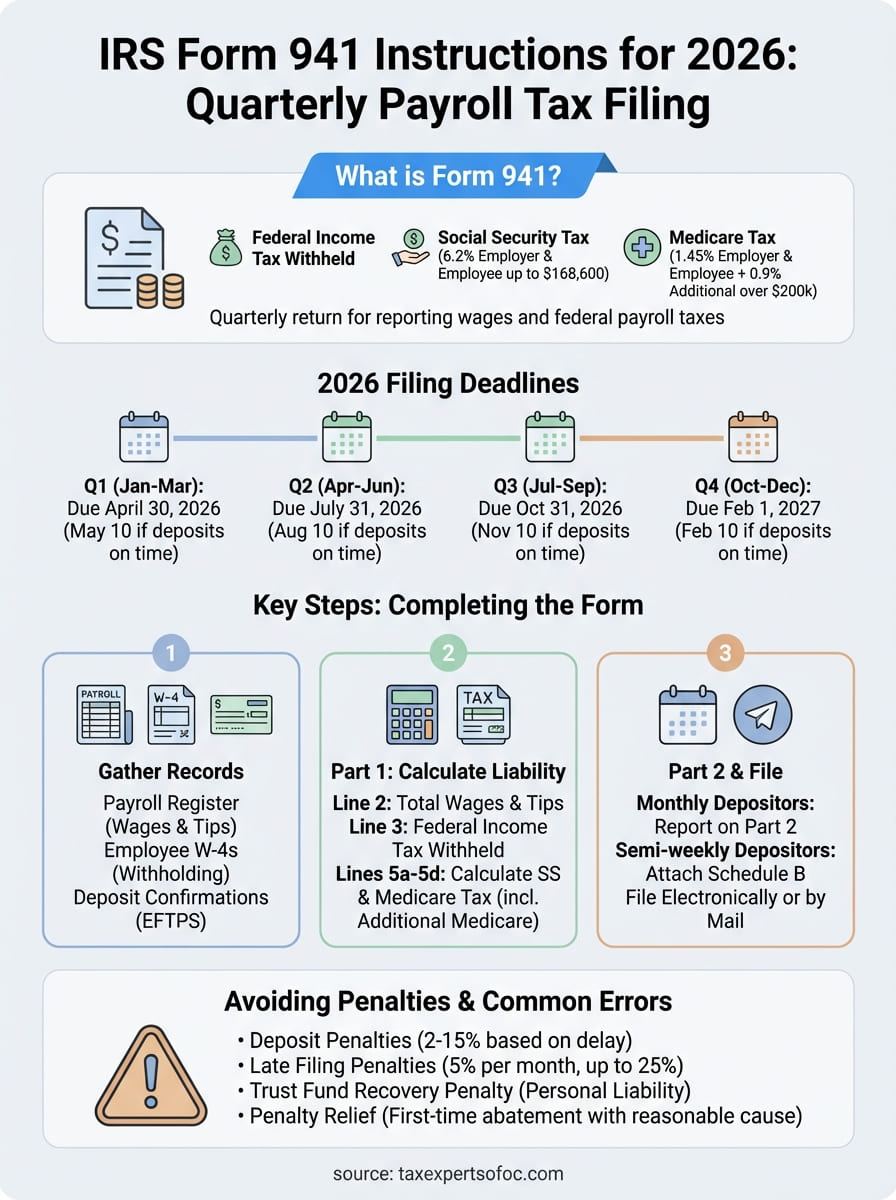

Form 941 captures three main federal payroll taxes: federal income tax withheld from employee wages, Social Security tax (both employer and employee portions), and Medicare tax (both portions as well). You use this form to reconcile your quarterly tax deposits with the actual amounts you owe, and to report total wages paid to all employees during that quarter. The form also tracks any adjustments for sick pay, tips reported by employees working in food service or hospitality, and credits like the qualified small business payroll tax credit for increasing research activities.

Understanding exactly what goes on Form 941 keeps you from mixing up different tax obligations. Unemployment taxes (FUTA) don't appear here; those go on Form 940, filed annually. State unemployment and state income tax withholding also fall outside Form 941's scope, so you'll handle those separately through your state agencies. The IRS Form 941 instructions clarify these boundaries in detail, but the short version is this: if it's federal income tax, Social Security, or Medicare related to employee wages, it belongs on Form 941.

Taxes you report on Form 941

Federal income tax withholding is the first component. You calculate this based on each employee's W-4 form, pay frequency, and taxable wages. The amount varies by employee, so your payroll system should track withholding per pay period, then sum it for the quarter. You report the total withheld amount on line 2 of Part 1.

Social Security and Medicare taxes make up the rest. For 2026, the Social Security tax rate remains 6.2% for both employer and employee on wages up to $168,600 (the 2026 wage base limit). Medicare tax stays at 1.45% for both parties on all wages, with an additional 0.9% Medicare tax on employee wages exceeding $200,000 in a calendar year. You report combined employee and employer portions on lines 5a through 5d, depending on the type of wages and any applicable credits.

Form 941 reconciles what you deposited throughout the quarter with what you actually owe, so accurate payroll records determine whether you get a refund or owe more.

Who must file (and who doesn't)

You must file Form 941 if you paid wages subject to federal income tax withholding or FICA taxes to one or more employees during any part of the quarter. This applies whether you run a corporation, partnership, LLC, nonprofit, or sole proprietorship with employees. Household employers who pay household employees like nannies or housekeepers typically use Schedule H instead of Form 941, unless they operate through a business entity.

Employers who pay agricultural workers generally file Form 943 annually rather than quarterly. Seasonal employers who don't pay wages during a specific quarter can check the seasonal employer box on Form 941 to notify the IRS, which prevents unnecessary penalty notices for quarters with no activity. If you cease operations entirely or stop paying wages permanently, you file a final return and indicate closure on the form.

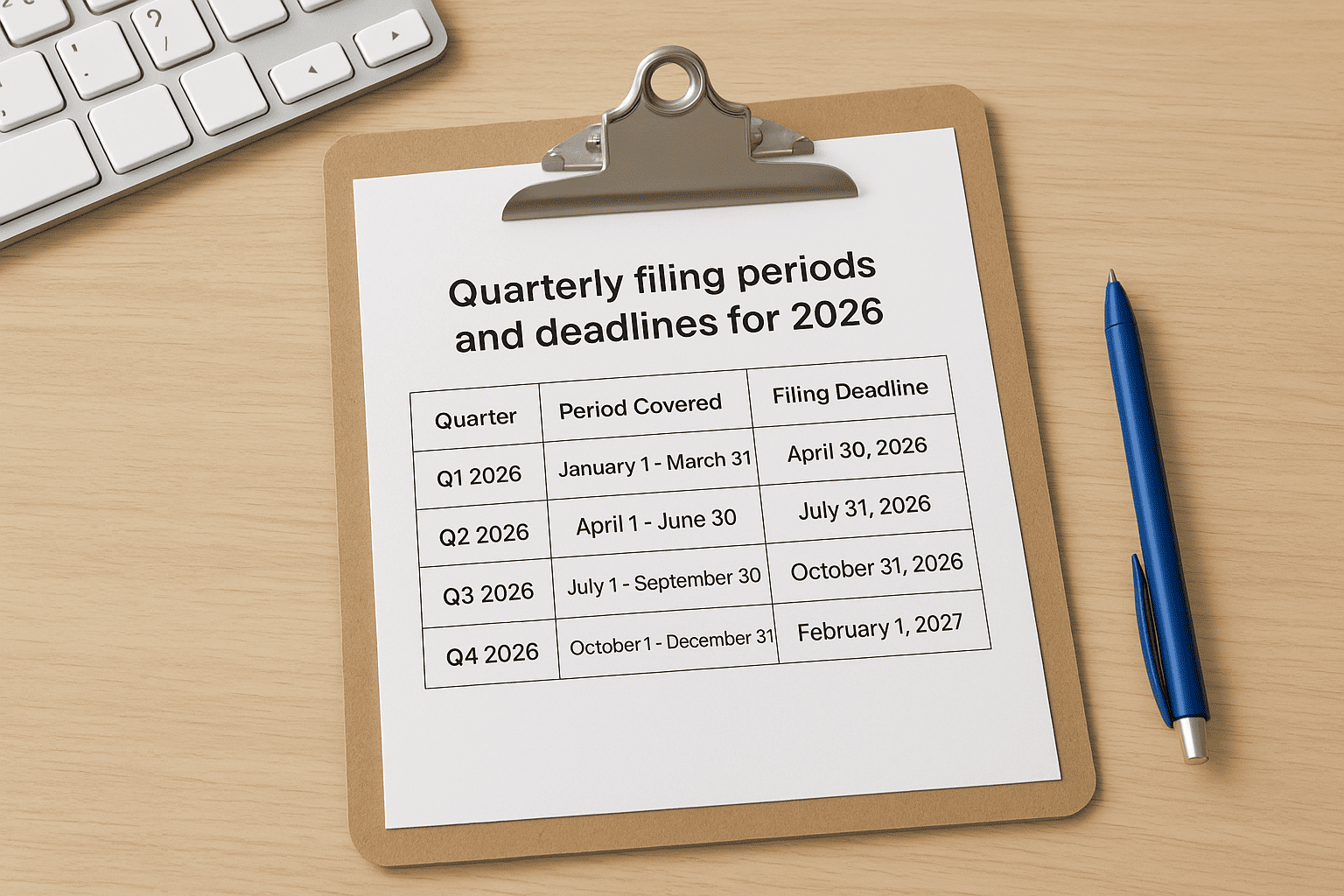

Quarterly filing periods and deadlines for 2026

Form 941 divides the calendar year into four quarters, each with its own filing deadline. You file by the last day of the month following the quarter's end, unless that day falls on a weekend or federal holiday, in which case the deadline shifts to the next business day.

| Quarter | Period Covered | Filing Deadline |

|---|---|---|

| Q1 2026 | January 1 - March 31 | April 30, 2026 |

| Q2 2026 | April 1 - June 30 | July 31, 2026 |

| Q3 2026 | July 1 - September 30 | October 31, 2026 |

| Q4 2026 | October 1 - December 31 | February 1, 2027 |

If you deposited all taxes on time and in full during the quarter, you get an automatic 10-day extension to file. That pushes the Q1 2026 deadline to May 10, Q2 to August 10, Q3 to November 10, and Q4 to February 10, 2027. This extension only applies to filing the form itself, not to paying taxes owed.

Before you start: info and records to gather

You can't fill out Form 941 accurately without the right documentation in front of you. The IRS Form 941 instructions require precise figures for employee wages, tax deposits, and withholding calculations, so you need complete payroll records for the entire quarter. Missing or incomplete data leads to errors that trigger IRS notices, penalties, or audits you'd rather avoid.

Before you open the form, pull together your payroll register, tax deposit confirmations, and business identification details. Having everything organized saves time and reduces mistakes. You'll reference these documents line by line as you work through each section of Form 941.

Employee wage data and tax withholding records

Your payroll register should show total wages paid to all employees during the quarter, broken down by pay period. You need the gross wages before any deductions, plus any taxable fringe benefits like bonuses, commissions, or employer-provided life insurance over $50,000. This total becomes the basis for calculating Social Security and Medicare taxes.

You also need the federal income tax withheld from each employee's paycheck throughout the quarter. Your payroll system should track this automatically based on W-4 forms, but verify the totals match your actual deposits. For employees who received tips, gather tip reports they submitted to you, since you report tips separately on Form 941. If you paid any sick pay or had third-party sick pay providers involved, you'll need those amounts documented as well.

Accurate wage records prevent reconciliation issues later, when the IRS matches your Form 941 against W-2 forms and deposit records.

Business identification information

You'll enter your Employer Identification Number (EIN) at the top of Form 941, along with your business name and address exactly as they appear on your IRS records. If you moved or changed your business name during the quarter, note the old address or name so you can update it properly on the form. You also need to know your business type (sole proprietor, partnership, corporation, etc.) and whether you qualify as a seasonal employer.

Prior quarter deposits and payments

Gather confirmation numbers or receipts for every federal tax deposit you made during the quarter using EFTPS (Electronic Federal Tax Payment System) or through your payroll provider. You'll report these deposits on Schedule B (Form 941) if you're a semi-weekly depositor, or summarize them in Part 2 if you're a monthly depositor. If you made any estimated tax payments, adjustments for prior quarters, or received credits, have those records ready too.

Step 1. Complete the top section and Part 1

The top section of Form 941 establishes your identity with the IRS and sets the reporting period. You start by entering your Employer Identification Number (EIN), business name, and trade name if different from your legal name. Match these exactly to your IRS records to avoid processing delays. Fill in your complete address including suite or apartment numbers, then check the box for the quarter you're reporting (January-March, April-June, July-September, or October-December).

Fill in the header information

Enter your EIN in the nine-digit format (XX-XXXXXXX) at the very top. If you're a seasonal employer who doesn't pay wages every quarter, check the seasonal employer box. This prevents the IRS from sending unnecessary notices during inactive quarters. You also indicate if this is an amended return (correcting a previously filed Form 941) or a final return (you've closed your business or stopped paying wages permanently).

The IRS Form 941 instructions specify that you must check the address change box if you moved since your last filing. Write your phone number and business contact person's name in case the IRS needs clarification on anything you reported.

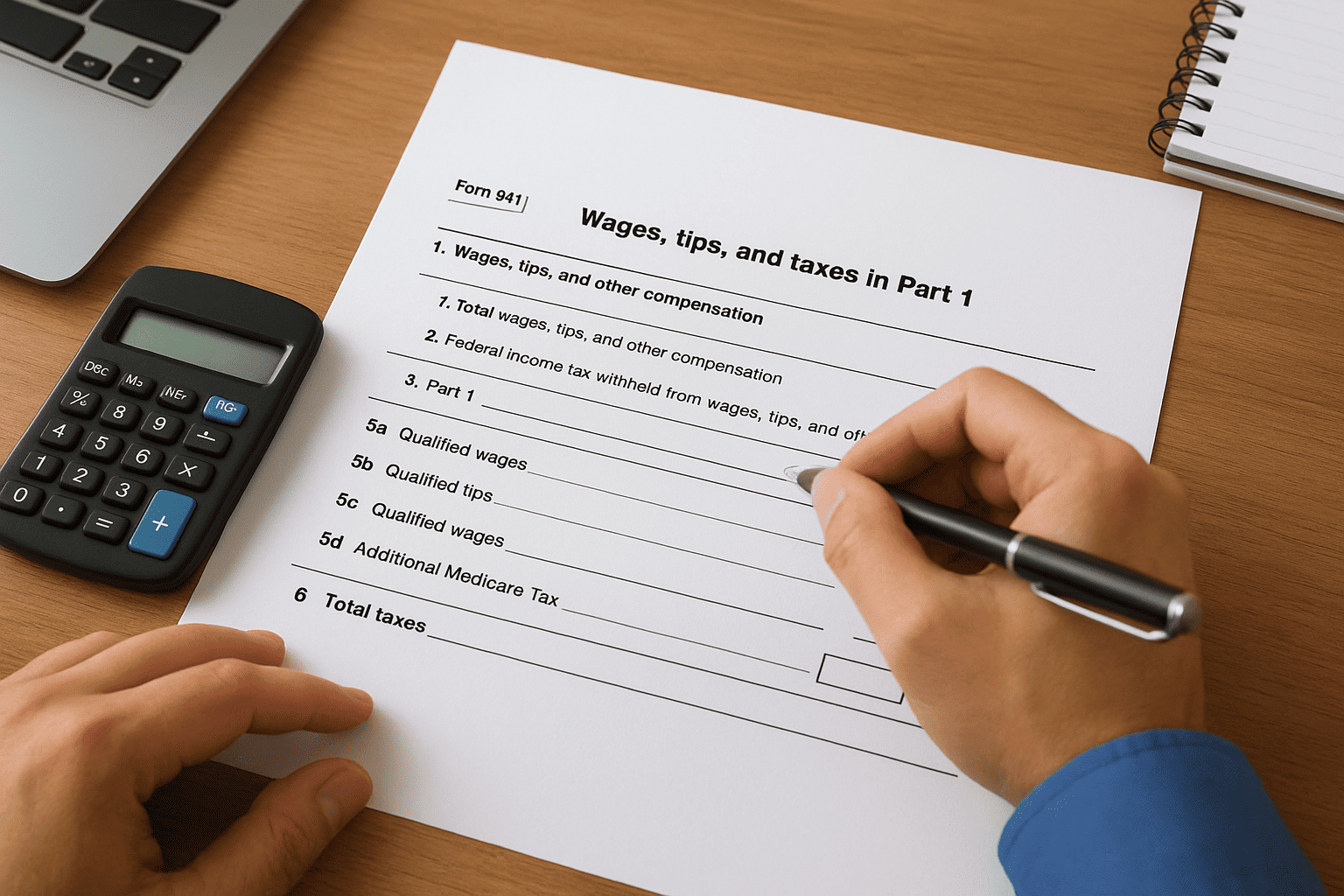

Calculate wages and taxes in Part 1

Part 1 requires you to report employee counts and calculate tax liabilities. On line 1, enter the number of employees who received wages during the pay period that includes March 12 for Q1, June 12 for Q2, September 12 for Q3, or December 12 for Q4. This snapshot date matters for IRS tracking purposes.

Line 2 asks for total wages, tips, and other compensation paid during the quarter. Include gross wages before any deductions, taxable fringe benefits, and employee tips. On line 3, report only the federal income tax you withheld from those wages based on employee W-4 forms. If you had no withholding, enter zero.

Lines 5a through 5d handle Social Security and Medicare taxes. For line 5a, multiply qualified Social Security wages (capped at $168,600 per employee for 2026) by 12.4% to get combined employer and employee tax. Column 1 shows taxable wages, column 2 shows the total tax. On line 5c, multiply all Medicare wages by 2.9% for the combined rate. Add the 0.9% Additional Medicare Tax on line 5d for any employee whose wages exceeded $200,000 during the quarter.

Report tips separately on line 5b if you operate a restaurant or other tipped-wage business, since tip income affects Social Security tax calculations.

Add lines 3, 5a, 5b, 5c, and 5d together to get your total taxes on line 6. This amount represents your full quarterly liability before any adjustments or credits in later sections.

Step 2. Finish Parts 2 to 5 and file

After calculating your tax liability in Part 1, you move to Parts 2 through 5 to report your actual deposits, claim any credits or adjustments, and prepare the form for submission. These sections reconcile what you owe against what you already paid during the quarter. The IRS Form 941 instructions require different approaches depending on whether you're a monthly or semi-weekly depositor, so you'll need to know your deposit schedule before proceeding.

Complete Part 2: deposit schedule and liability

Part 2 asks you to report your total tax liability for each month of the quarter if you're a monthly depositor. You break down line 12 (total taxes after adjustments) into three monthly amounts that match your actual deposit schedule. For example, if you deposited $3,000 in January, $3,200 in February, and $3,100 in March, you enter those exact figures on lines 16a through 16c for Q1 2026.

If you're a semi-weekly depositor, you must attach Schedule B (Form 941) instead of completing Part 2. Schedule B requires you to report the tax liability for each pay date during the quarter, which gives the IRS a detailed deposit history. You determine your depositor status based on your total taxes reported in the lookback period (the 12 months ending the previous June 30). If your total taxes exceeded $50,000 during that period, you're a semi-weekly depositor.

Report your deposits exactly as you made them through EFTPS or your payroll provider, since the IRS matches these figures against their payment records.

Report adjustments and credits in Part 3

Part 3 lets you claim refundable credits that reduce your tax liability below what you calculated in Part 1. The most common adjustment involves sick pay paid by third-party insurers, which you subtract on line 8. You also report credits like the qualified small business payroll tax credit for increasing research activities on line 11, if you qualify.

Handle Parts 4 and 5 before submission

Part 4 asks if you want to authorize a third-party designee (like your CPA or Enrolled Agent) to discuss the return with the IRS. Check "Yes" and provide their name, phone number, and a five-digit PIN they choose. Part 5 requires your signature, printed name, and title, along with the date you sign. You can sign electronically if filing through authorized e-file software, or physically sign if mailing a paper return.

Mail paper returns to the IRS address listed in the instructions for your state, or file electronically through IRS-approved software or your payroll service provider. Electronic filing confirms receipt immediately and processes faster than paper submissions.

Fix mistakes, deadlines, and penalties

Errors happen even with careful preparation, and the IRS provides a clear process to correct them before they turn into bigger problems. You file Form 941-X (Adjusted Employer's Quarterly Federal Tax Return) to fix mathematical mistakes, incorrect wage amounts, or wrong tax calculations on a previously submitted Form 941. The IRS Form 941 instructions explain when to use 941-X versus filing a new 941, but generally you use 941-X for corrections after the original return's due date passes. You have three years from the original filing date or two years from when you paid the tax (whichever is later) to claim a refund for overpaid taxes.

How to file an amended Form 941

You complete Form 941-X by first entering the information from your original Form 941 in column 1, then showing the correct amounts in column 2. The form automatically calculates the difference in column 3, which becomes your adjustment. Check the box indicating whether you're claiming a refund, paying additional tax, or making a correction with no money owed.

Process 1 on Form 941-X requires you to adjust both your tax liability and deposit amounts, while Process 2 adjusts only the tax liability without changing deposits. Most corrections use Process 1. You must explain the reason for each correction in Part 3, and the IRS may contact you if your explanation lacks detail or supporting documentation.

File 941-X separately for each quarter you need to correct, since you cannot combine multiple quarters on one adjustment form.

Understanding deposit and filing penalties

Missing a deposit deadline triggers a penalty between 2% and 15% of the unpaid amount, depending on how late you pay. Deposits made 1 to 5 days late incur a 2% penalty, while deposits more than 15 days late face a 10% penalty. If you receive an IRS notice demanding payment and still don't deposit within 10 days, the penalty jumps to 15%.

Late filing penalties equal 5% of the unpaid tax per month, capping at 25% of the total tax due. You also pay interest on unpaid balances calculated from the original due date. The IRS can assess a Trust Fund Recovery Penalty equal to 100% of the unpaid trust fund taxes (employee withholding portions) against business owners and responsible parties personally if they willfully fail to pay.

Requesting penalty relief

You can request first-time penalty abatement if you have a clean compliance history for the past three years and filed all required returns. Submit your request in writing or call the IRS, explaining your reasonable cause for missing the deadline. Documentation like medical records, natural disaster declarations, or death certificates strengthens penalty relief requests.

Keep your payroll taxes on track

Filing Form 941 correctly each quarter protects your business from penalties and keeps you compliant with federal payroll tax requirements. Following the IRS Form 941 instructions step by step ensures you report wages, calculate taxes, and submit deposits accurately. You now have the framework to gather records, complete each section, meet deadlines, and correct errors when they occur.

Consistent quarterly filings build a clean compliance history that prevents IRS scrutiny down the road. Missing a deadline or miscalculating your liability creates avoidable problems that compound over time. Payroll tax compliance demands attention to detail across employee counts, wage calculations, and deposit schedules every three months.

If you're juggling multiple business responsibilities, outsourcing your payroll tax management eliminates the risk of costly mistakes while freeing you to focus on operations. Tax Experts of OC handles Form 941 preparation and filing for employers nationwide, with direct access to CPAs and Enrolled Agents who ensure accuracy and timely submission. Schedule a free 30-minute consultation to review your payroll tax situation.