Owing the IRS more than you can pay is stressful, but it doesn't have to end with drained bank accounts or garnished wages. What most people don't realize is that the IRS itself offers several tax relief programs designed to help taxpayers settle, reduce, or restructure what they owe. These aren't loopholes or gimmicks. They're formal IRS tax relief programs built into the tax code, and qualifying for the right one can make a real difference in your financial future.

The challenge is figuring out which program fits your situation. Each one has specific eligibility requirements, and choosing the wrong path, or missing a deadline, can cost you. That's where working with a qualified professional matters. At Tax Experts of OC, our CPA and Enrolled Agents help clients across all 50 states navigate these programs every day, from negotiating offers in compromise to setting up manageable payment plans with the IRS.

Below, we break down five IRS tax relief programs that could help you take control of your tax debt. You'll learn how each program works, who qualifies, and what to expect during the process, so you can make an informed decision about your next step toward resolution.

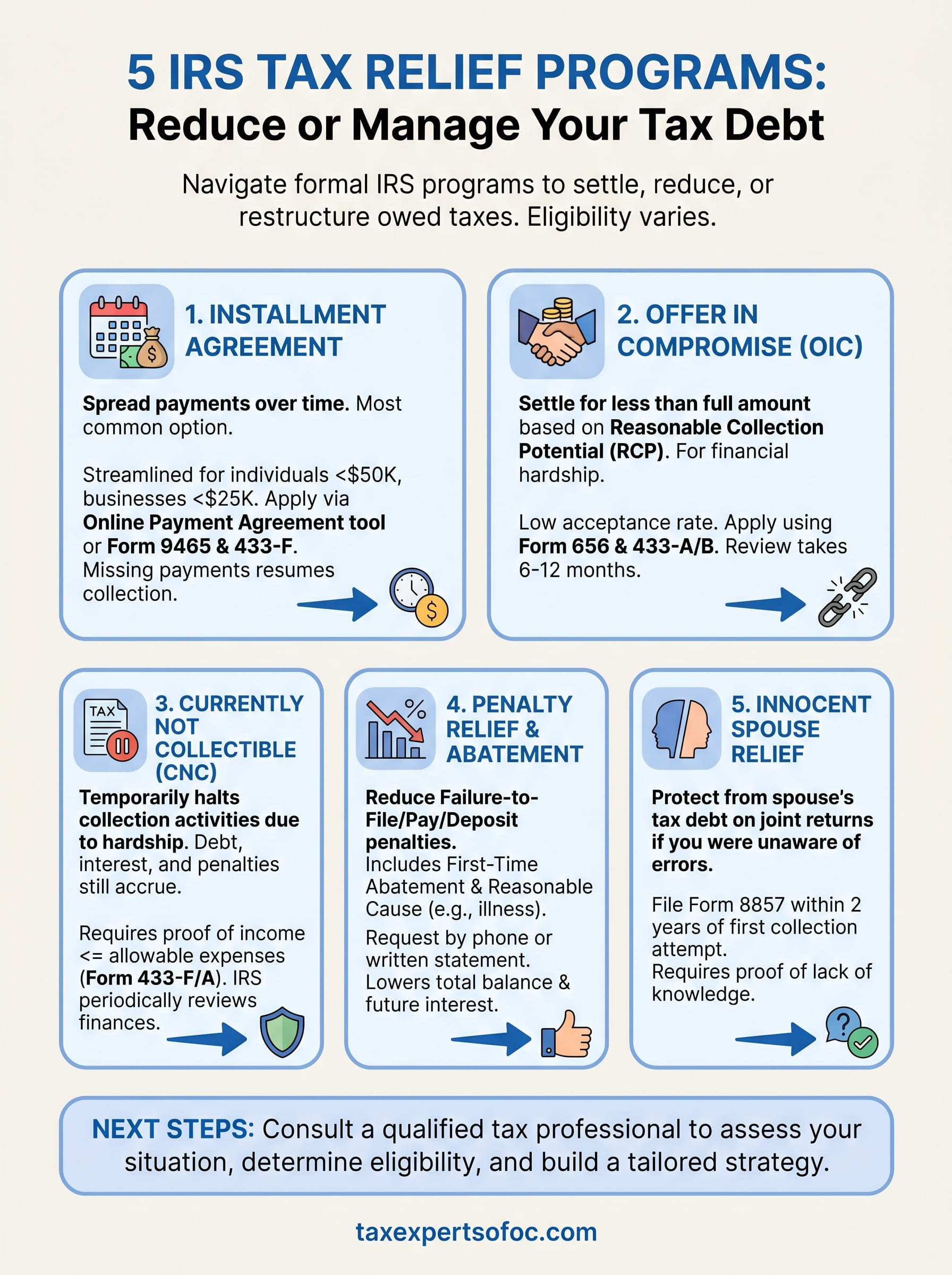

1. IRS installment agreement payment plans

An installment agreement is the most widely used option among the IRS tax relief programs available to taxpayers. It lets you spread your tax debt across monthly payments rather than paying everything at once, making it the most accessible starting point for anyone who can't cover their full balance.

What it is and how it works

This program is a formal arrangement where you commit to paying your outstanding tax balance through fixed monthly amounts set by the IRS. The IRS charges interest and fees throughout the repayment period, but collection actions like bank levies are generally paused while your agreement stays active.

Your monthly payment must cover your balance within the IRS collection statute, which is typically ten years from the date the tax was assessed.

Who qualifies and common IRS thresholds

Most individual taxpayers who owe $50,000 or less in combined tax, penalties, and interest can qualify for a streamlined installment agreement without submitting detailed financial records. Businesses that owe $25,000 or less may also qualify under streamlined terms. If you owe more, the IRS will review your income, expenses, and assets before approving a plan.

Owing more than $50,000 doesn't automatically disqualify you, but it does require you to provide full financial documentation and negotiate terms directly with the IRS.

How to apply and what documents you may need

You can apply through the IRS Online Payment Agreement tool if you meet streamlined thresholds. For larger balances, you'll need to submit Form 9465 (Installment Agreement Request) and Form 433-F (Collection Information Statement), which covers your income, monthly expenses, and assets.

What it costs and what happens if you miss payments

The IRS charges a one-time setup fee ranging from $31 to $225 depending on how you apply and whether you qualify for low-income relief. If you miss a scheduled payment, the IRS can terminate your agreement and immediately resume collection activity, including wage garnishments and bank levies.

Keeping your agreement current also means staying current on any new tax obligations, since falling behind on a future year's taxes can void your existing plan.

2. Offer in compromise

An offer in compromise (OIC) lets you settle your tax debt for less than the full amount you owe. This is one of the more well-known IRS tax relief programs, but acceptance rates are lower than most people expect.

What it is and when the IRS accepts less than full pay

The IRS accepts an OIC when it determines your offer reflects the most it can reasonably collect from you, based on your income, assets, and future earning potential. If paying in full would create genuine financial hardship, this program may apply to your situation.

The eligibility basics the IRS looks at

Your reasonable collection potential (RCP) is what the IRS examines, factoring in your assets and projected income minus allowable living expenses. You must also be current on all tax filing requirements before submitting.

The IRS rejected roughly 67% of OIC applications in recent years, which is why submitting a well-documented offer with accurate financials matters so much.

How to apply and what to expect during review

You apply using Form 656 along with Form 433-A or 433-B. The review typically takes 6 to 12 months, and collection activity is paused during that window.

Fees, payment options, and common reasons offers fail

There is a $205 application fee, waived for low-income applicants. You can pay as a lump sum or in short-term installments. Offers most often fail when applicants underreport income or submit incomplete financial documentation.

3. Currently not collectible status

Currently not collectible (CNC) status is one of the IRS tax relief programs that temporarily halts collection activity when you truly cannot afford to pay your tax debt and still cover basic living expenses.

What it is and what CNC does and does not stop

CNC status directs the IRS to pause active collections, including wage garnishments and bank levies. It does not erase your debt or stop interest and penalties from building, and the IRS can still file a federal tax lien against your property.

Who qualifies based on financial hardship

You qualify when your monthly income falls at or below your allowable living expenses under IRS national and local standards. The IRS considers costs like housing, utilities, food, and transportation when making this determination.

CNC status is a pause, not a resolution. Your balance remains, and the IRS will eventually recheck your finances.

How to request CNC and how the IRS verifies hardship

You request CNC by submitting Form 433-F or 433-A, which documents your income, monthly expenses, and assets. The IRS reviews this information to verify that your hardship is genuine and current.

What happens next, including liens, refunds, and rechecks

While in CNC status, the IRS will apply any future tax refunds toward your outstanding balance. Your case gets reviewed periodically, and if your financial situation improves, the IRS can reactivate collections.

4. Penalty relief and abatement

Penalty relief is one of the IRS tax relief programs that gets overlooked, but it can cut your total balance significantly if you qualify.

Which IRS penalties you may be able to reduce

The IRS charges several penalties that stack on top of your original tax debt. The most common ones eligible for relief include:

- Failure-to-file penalty: 5% of unpaid tax per month, up to 25%

- Failure-to-pay penalty: 0.5% of unpaid tax per month, up to 25%

- Failure-to-deposit penalty: applies to businesses that miss payroll tax deposits

First-time abatement and reasonable cause relief

First-time abatement (FTA) applies if you have a clean compliance history for the prior three years. Reasonable cause relief covers situations where events outside your control, such as a serious illness or natural disaster, caused the failure to file or pay on time.

FTA is often the fastest path to penalty relief, and many taxpayers don't know to ask for it.

How to request penalty relief and support your request

You request relief by calling the IRS directly or submitting a written request. The IRS does not apply this relief automatically, so you must ask. Supporting documents like medical records strengthen a reasonable cause argument considerably.

How penalty relief affects interest and your total balance

Removing penalties reduces your principal balance, which directly lowers the interest the IRS charges going forward. Your total amount owed can drop considerably once abatement is applied.

5. Innocent spouse relief

Innocent spouse relief is one of the IRS tax relief programs that protects you from being held responsible for tax debt your spouse created without your knowledge. If you filed a joint return and your partner understated income or claimed improper deductions, you may not have to share the liability.

What it is and the three types of relief

The IRS offers three separate paths under this program: innocent spouse relief, separation of liability relief, and equitable relief. Each one addresses a different set of circumstances, and only one may apply to your situation depending on how the error occurred and when you learned about it.

Who qualifies and key deadlines to know

You must show you did not know and had no reason to know about the understatement at the time you signed the return. Most requests must be filed within two years of the IRS first attempting to collect from you.

Missing the two-year deadline is one of the most common reasons these requests get denied.

How to file and what evidence matters most

You file using Form 8857 (Request for Innocent Spouse Relief). Evidence that supports your case includes financial records showing separate accounts, limited involvement in household finances, or documentation of abuse or control.

What to expect after filing, including appeals and outcomes

The IRS notifies your spouse or former spouse and gives them a chance to respond. Reviews typically take several months, and if denied, you have the right to appeal through the IRS Office of Appeals.

Next Steps

Each of these five IRS tax relief programs works differently, and the right one depends on your specific financial situation, filing history, and how much you owe. Choosing the wrong program, or missing a key deadline, can delay your resolution and cost you more in penalties and interest over time.

Your best move right now is to talk to a qualified tax professional who can review your IRS account, assess your eligibility across multiple programs, and build a clear strategy tailored to your case. The program that works for someone else may not be the right fit for you, and submitting the wrong application can set your resolution back significantly.

At Tax Experts of OC, our CPA and Enrolled Agents work with clients in all 50 states to resolve tax debt through the right channels. We offer a free 30-minute consultation and transparent upfront pricing so you know exactly where you stand before committing to anything.