Owing money to the IRS isn't something that resolves itself. Interest accrues, penalties stack up, and collection actions can escalate from notices to wage garnishments or bank levies. If you're searching for help with IRS back taxes, the good news is that the IRS itself offers several programs designed to help taxpayers settle or manage their debt, but knowing which option fits your situation makes all the difference.

The relief programs available to you depend on how much you owe, your current financial situation, and your filing history. Payment plans, Offers in Compromise, penalty abatement, and Currently Not Collectible status each serve a different purpose. Some reduce what you owe. Others buy you time. Choosing the wrong one, or applying incorrectly, can cost you months and leave you worse off than where you started.

This guide breaks down each of those options step by step: what qualifies you, how to apply, and what to expect from the process. At Tax Experts of OC, our CPAs and Enrolled Agents work with taxpayers across all 50 states to resolve IRS debt, from straightforward installment agreements to complex settlement negotiations. Whether you're handling this on your own or considering professional representation, this article gives you the information you need to take the right next step.

Before you act, confirm what you owe and why

Many taxpayers jump straight into payment plans or settlement applications without first verifying their actual balance. The figure you remember owing and the amount the IRS has on file can differ significantly, especially after penalties and interest have been compounding for months or years. Before you take any action toward resolving back taxes, you need a clear, documented picture of what the IRS says you owe and why.

Pull your IRS account transcript

The IRS provides free access to your account transcripts through its online portal at IRS.gov. Your Account Transcript shows your tax balance, payment history, penalty assessments, and any collection actions for each tax year. Pull a transcript for every tax year in which you carry a balance, because each year is tracked separately.

If you cannot access the online portal, call the IRS directly at 1-800-829-1040 or submit Form 4506-T to request transcripts by mail.

When reviewing your transcripts, pay close attention to the following:

- Transaction codes: These three-digit codes explain every action on your account, including when penalties were assessed and when collection holds were placed.

- Balance per module: Each tax year is treated as a separate "module," so your total debt is the sum across all open years.

- CP notices referenced: Transcripts often include the notice number tied to a specific action, which helps you match IRS letters to your account history.

Once you have all your transcripts, write out each year's balance, the type of liability, and the date the debt was assessed. This summary becomes your working document throughout the resolution process and keeps you from making decisions based on incomplete or outdated information.

Understand what makes up your balance

Your total IRS balance is rarely just the original unpaid tax. Failure-to-file penalties add 5% of the unpaid tax per month, up to a maximum of 25%, while failure-to-pay penalties add 0.5% per month on top of that. Interest compounds daily based on the federal short-term rate plus 3 percentage points, and it applies to both the unpaid tax and any assessed penalties.

For example, if you owed $10,000 in tax and went three years without filing or paying, your balance could easily reach $15,000 or more once penalties and interest are calculated. Knowing the specific breakdown of each component matters because certain IRS relief programs target penalties directly rather than the underlying tax, and applying to the wrong program wastes time.

Watch for errors before you move forward

IRS records contain errors more often than most people expect. Misapplied payments, duplicate assessments, and data entry mistakes do appear on account transcripts, and identifying them is your responsibility. Compare each transcript entry against your own records: bank statements showing past tax payments, prior-year returns you filed, and every IRS notice you have received.

When you spot a discrepancy, document it in writing immediately. Submitting an amended return or a formal written dispute early in the process protects your position and stops you from entering a payment agreement based on an inflated balance. This verification step is the foundation of any effective help with IRS back taxes.

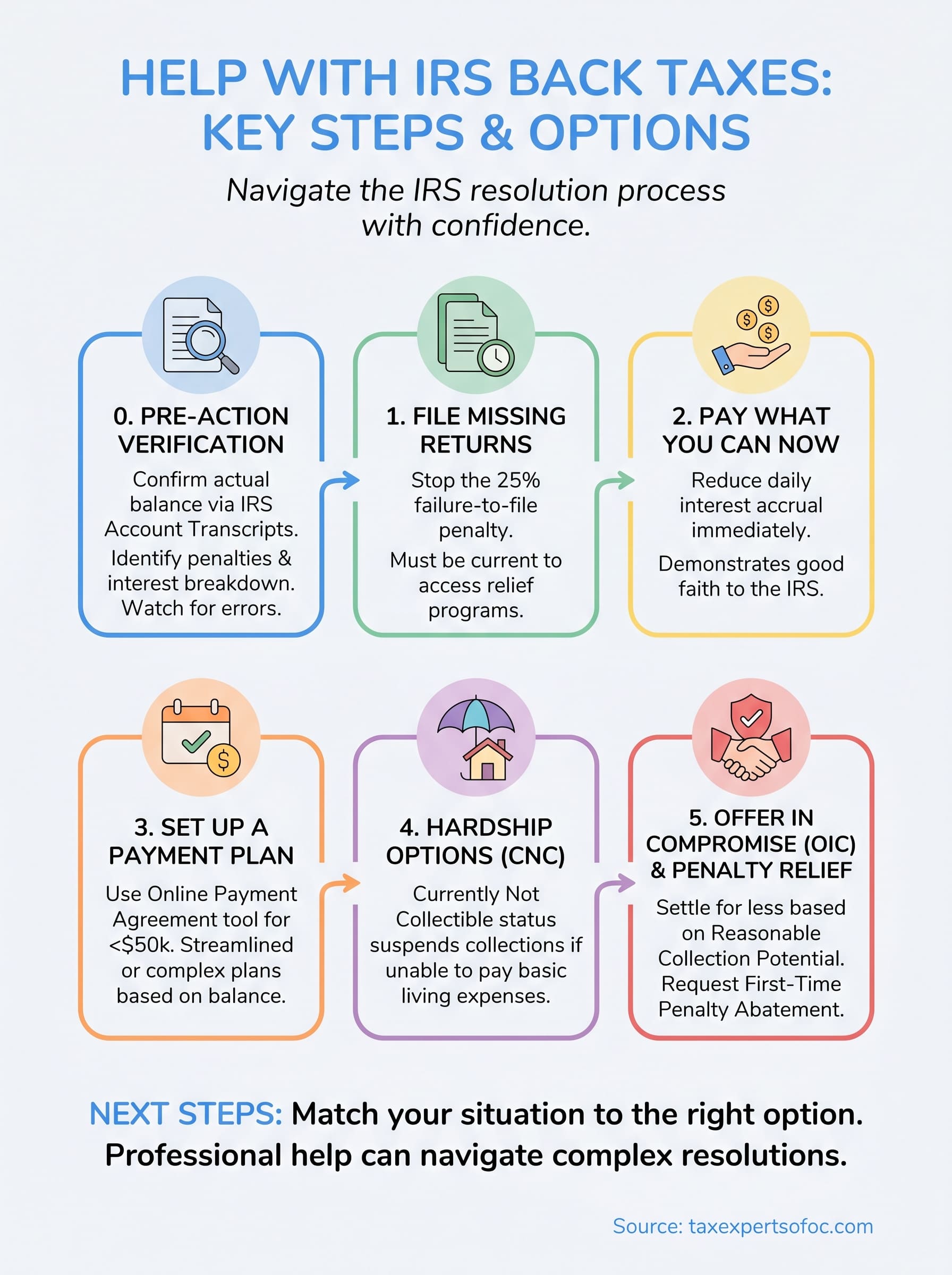

Step 1. File missing returns and stop the worst penalties

If you have unfiled tax returns, filing them is the single most important action you can take before exploring any payment or settlement option. The IRS cannot set up an installment agreement, process an Offer in Compromise, or grant most hardship relief if you have outstanding returns. Getting current on your filings gives you access to every resolution program available and stops the most damaging penalty from growing any further.

Why the failure-to-file penalty hits hardest

The failure-to-file penalty runs at 5% of your unpaid tax balance per month, capped at 25% of the total tax owed. Compare that to the failure-to-pay penalty, which runs at only 0.5% per month. Filing your return, even if you cannot pay a single dollar, eliminates the larger of those two penalties immediately.

Filing late is always better than not filing at all, because the failure-to-file penalty alone can add 25% to your balance within five months.

If you owe $8,000 in tax and go five months without filing, the failure-to-file penalty alone adds $2,000 to your balance. Filing on time but paying nothing would have added only $200 in failure-to-pay penalties over that same period. The math strongly favors filing first, regardless of your ability to pay.

How to file late returns correctly

Gather your W-2s, 1099s, and any other income documentation for each unfiled year. If you are missing records, request wage and income transcripts from IRS.gov to reconstruct your income figures accurately. File the correct form for each tax year, such as the Form 1040 for individuals, and mail each return to the address listed in that year's instructions, since IRS mailing addresses change periodically.

For those seeking help with IRS back taxes involving multiple unfiled years, prioritize the most recent years first. The IRS is more likely to initiate enforcement on recent balances, so clearing the newest returns quickly reduces your immediate collection risk while you work through the older years in order.

Step 2. Pay what you can now and avoid new problems

Once your returns are filed, paying any amount you can toward your balance reduces daily interest immediately. Even if the full amount is out of reach, a partial payment signals good faith to the IRS and shrinks the principal on which interest and penalties continue to compound. Sitting on a balance without any action tends to escalate your collection risk faster than most people expect.

Why partial payment reduces your total cost

Interest on IRS back taxes accrues daily, calculated on both the unpaid tax and any outstanding penalties. The faster you reduce the principal balance, the less total interest you accumulate over the entire resolution period. For example, if you owe $12,000 and pay $3,000 immediately, the IRS calculates future interest only on the remaining $9,000, which can save you hundreds of dollars before you reach a final resolution.

Paying even a small amount now costs you less in total than waiting until you have the full balance available.

Your payment also demonstrates active compliance, which matters when you later apply for an installment agreement, penalty relief, or an Offer in Compromise. Reviewers look at your payment history, and even modest contributions made consistently work in your favor during any negotiation.

How to send a payment to the IRS

The IRS offers several direct payment options through its website at IRS.gov. Direct Pay is the fastest and simplest method, letting you authorize a payment directly from your checking or savings account at no cost. When submitting your payment, always apply it to the oldest tax year first, since that is where interest has been running the longest.

When you send a payment by check or money order, write the following on the memo line to ensure proper application:

- Your Social Security Number or EIN

- The tax year the payment applies to (for example, "2023 Form 1040")

- Your daytime phone number

Keeping records of every payment is essential, especially if you are seeking help with IRS back taxes through a formal resolution program later. Payment documentation demonstrates compliance and strengthens your position in any installment agreement or settlement negotiation.

Step 3. Set up an IRS payment plan that fits your budget

If you cannot pay your full balance right now, an IRS installment agreement spreads your payments over time without triggering aggressive collection actions like levies or garnishments. Setting up a plan keeps your account in good standing while you work toward full resolution. This is one of the most commonly used tools when seeking help with IRS back taxes, and the IRS approves most applications automatically when your balance falls within certain thresholds.

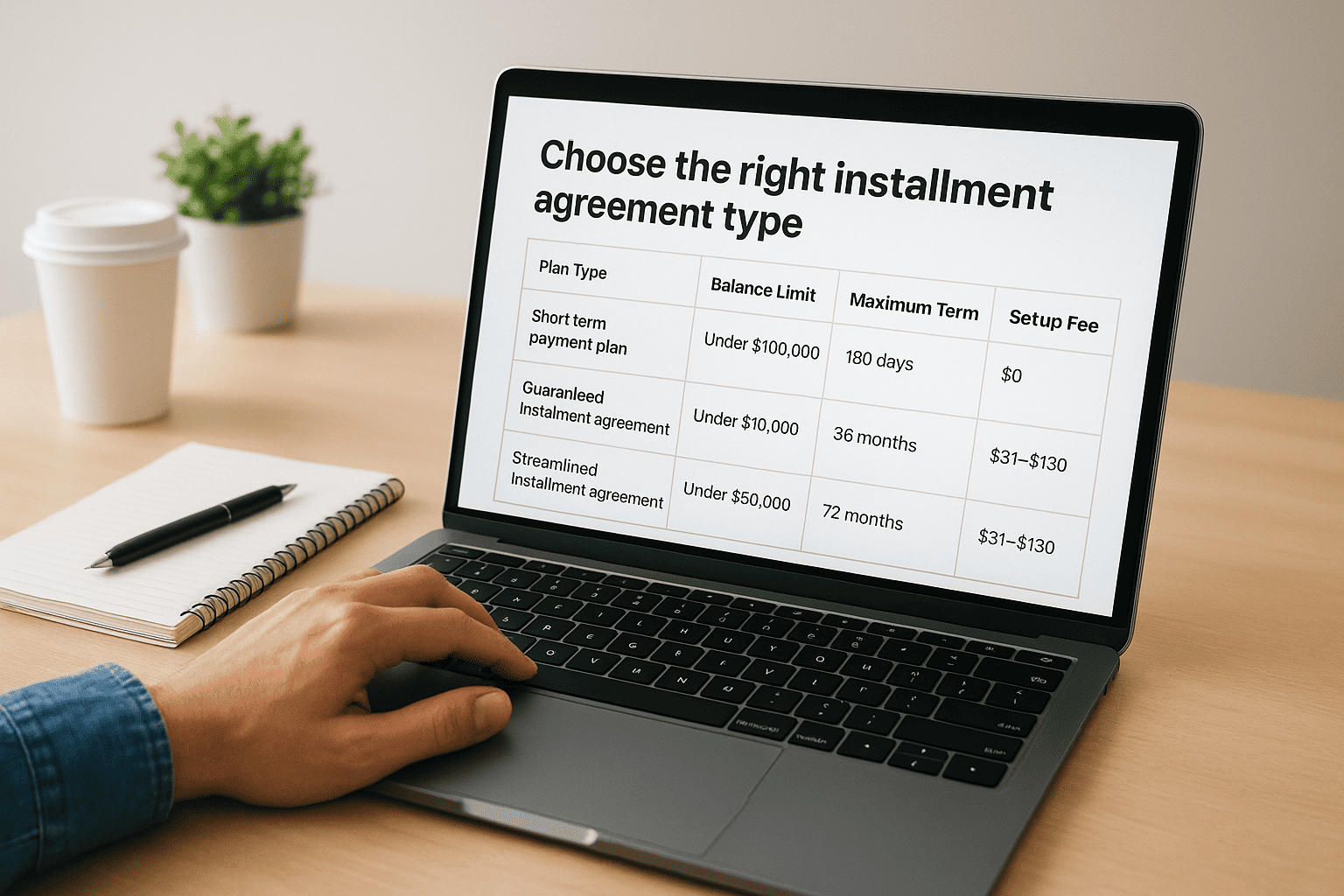

Choose the right installment agreement type

The IRS offers several plan types depending on your total balance and how long you need to pay it off. Selecting the correct category before you apply saves you from submitting more financial documentation than your situation actually requires.

| Plan Type | Balance Limit | Maximum Term | Setup Fee |

|---|---|---|---|

| Short-term payment plan | Under $100,000 | 180 days | $0 |

| Guaranteed installment agreement | Under $10,000 | 36 months | $31–$130 |

| Streamlined installment agreement | Under $50,000 | 72 months | $31–$130 |

| Non-streamlined installment agreement | $50,000 or more | Negotiated | $31–$130 |

If your balance is under $50,000, the streamlined option requires no financial disclosure, which makes approval faster and simpler.

For balances over $50,000, you must submit Form 433-F (Collection Information Statement), which details your income, monthly expenses, and assets. The IRS uses this form to set a monthly payment you can realistically afford based on your actual financial situation.

How to apply online in minutes

The fastest way to apply is through the IRS Online Payment Agreement tool at IRS.gov. You will need your Social Security Number or EIN, your most recent tax return, and a valid email address to complete the application. Most streamlined agreements are approved instantly without speaking to an agent.

Follow these steps to apply:

- Log in or create an account at IRS.gov.

- Select "Apply for a payment plan" and choose your plan type.

- Enter your proposed monthly payment amount and preferred start date.

- Review the agreement terms and submit electronically.

Once approved, make every payment on time. Missing a single payment can default your entire agreement and return your account to active collections immediately.

Step 4. Use hardship options when you truly cannot pay

When your monthly income barely covers basic living expenses, a standard installment agreement is not always a realistic option. The IRS recognizes this and maintains a formal hardship classification called Currently Not Collectible (CNC) status, which temporarily suspends collection activity on your account. While CNC status does not reduce or erase your debt, it stops wage garnishments, bank levies, and other enforcement actions while you stabilize your finances.

CNC status gives you breathing room, but interest and penalties continue to accrue on your balance throughout the period the hold is in place.

What qualifies you for Currently Not Collectible status

To qualify for CNC status, you must demonstrate to the IRS that paying your tax debt would prevent you from covering necessary living expenses such as housing, utilities, food, and basic transportation. The IRS compares your monthly income against its Collection Financial Standards, which are published allowances for essential expense categories. If your allowable expenses equal or exceed your income, you likely qualify.

The IRS evaluates the following when determining CNC eligibility:

- Gross monthly income from all sources, including wages, self-employment, and benefits

- Allowable housing and utility expenses based on your county and household size

- Transportation costs within IRS-published national and local standards

- Out-of-pocket health care expenses supported by documentation

- Other necessary expenses such as court-ordered payments or childcare

How to request CNC status

To request CNC status, call the IRS at 1-800-829-1040 and explain that you are unable to pay due to financial hardship. You will likely need to submit Form 433-A for individuals or Form 433-F, which documents your income, assets, and monthly expenses in detail. Gather recent bank statements, pay stubs, and utility bills before you call so you can provide accurate figures immediately.

Getting help with IRS back taxes through a CNC request is more straightforward when your documentation is organized in advance. Once approved, the IRS will review your status periodically, typically every one to two years, and may reinstate collection if your financial situation improves significantly.

Step 5. Settle for less with an offer in compromise

An Offer in Compromise (OIC) lets you settle your IRS back taxes for less than the full amount owed when paying the full balance would create genuine financial hardship. The IRS accepts OICs when the offered amount represents the most it can reasonably expect to collect from you given your income, assets, and expenses. This is one of the most powerful tools available when seeking help with IRS back taxes, but the IRS rejects poorly prepared applications regularly, so understanding the qualification criteria before you apply is essential.

The IRS accepted roughly 13,000 OIC applications in a recent reporting year, approving about one in three submitted, which means preparation directly determines your outcome.

What the IRS evaluates in your OIC application

The IRS calculates your Reasonable Collection Potential (RCP) to determine whether your offer is acceptable. RCP combines your net realizable asset value with your future income minus allowable living expenses, projected over either 12 or 24 months depending on your chosen payment structure. If your offer equals or exceeds your RCP, the IRS will generally accept it.

The IRS reviews the following components when calculating your RCP:

- Net asset value: the quick-sale value of your home equity, bank accounts, vehicles, and retirement funds

- Monthly disposable income: your gross income minus IRS-approved living expense allowances

- Payment multiplier: 12 months of disposable income for a lump-sum offer or 24 months for a periodic payment offer

How to apply for an offer in compromise

You submit an OIC using Form 656 (Offer in Compromise) along with Form 433-A (OIC) for individuals, which documents your financial position in detail. Both forms are available directly at IRS.gov. A non-refundable $205 application fee applies unless you qualify for a low-income waiver based on your household income falling at or below 250% of the federal poverty level.

Submit your completed package to the IRS Offer in Compromise unit and confirm receipt in writing. Track every document you send, because the IRS has 24 months to accept or reject your offer, and incomplete submissions reset that timeline.

Step 6. Ask for penalty relief and handle IRS notices fast

Penalties can make up a significant portion of what you owe, and the IRS offers two formal programs that remove them entirely under the right circumstances: First-Time Penalty Abatement (FTA) and Reasonable Cause relief. Requesting abatement costs nothing, takes relatively little time to prepare, and can reduce your total balance by hundreds or thousands of dollars if you qualify. Tackling this step alongside any payment or settlement strategy gives you the best chance of paying the smallest possible amount.

Request first-time penalty abatement

First-Time Penalty Abatement is the faster of the two options because it does not require you to explain your circumstances in detail. You qualify if you have no penalties assessed in the three tax years prior to the year you are requesting relief for, you have filed all currently required returns, and you have paid or arranged to pay any tax currently due. Call the IRS at 1-800-829-1040 and request FTA verbally, or submit a written request using the template below.

Your Name

Your Address

Your SSN / EIN

Date

Internal Revenue Service

[Campus Address from your notice]

Re: Request for First-Time Penalty Abatement

Tax Year: [XXXX]

Form: [e.g., 1040]

Notice Number: [if applicable]

Dear IRS Collections:

I am requesting first-time penalty abatement for the [failure-to-file /

failure-to-pay] penalty assessed for tax year [XXXX]. I have filed all

required returns, have no penalties in the prior three tax years, and

have resolved or arranged to resolve my outstanding balance.

Please remove the assessed penalty and confirm the adjustment in writing.

Sincerely,

[Your Signature]

[Your Printed Name]

Respond to IRS notices on time

Every IRS notice carries a response deadline, and missing it limits your appeal rights and can trigger immediate collection escalation. When a notice arrives, read the entire document, identify the specific action required, and mark the response date on your calendar before doing anything else.

Ignoring an IRS notice does not stop the clock. The deadline passes whether you respond or not, and your options narrow with each missed date.

Seeking help with IRS back taxes through a professional becomes especially valuable at this stage, because an Enrolled Agent or CPA can respond on your behalf, communicate directly with the IRS using a Power of Attorney, and prevent procedural mistakes that could cost you relief you were otherwise eligible to receive.

Next steps if you need help

You now have a complete picture of every major program available for resolving IRS back taxes, from filing missing returns to submitting an Offer in Compromise. The right path forward depends on your specific balance, filing history, and monthly cash flow, so the next step is matching your situation to the option that fits best before the IRS escalates collection.

Handling this on your own is possible, but mistakes in documentation or missed deadlines can cost you programs you were eligible for. At Tax Experts of OC, our CPAs and Enrolled Agents provide direct, hands-on help with IRS back taxes for clients across all 50 states. We review your transcripts, identify every relief program you qualify for, and represent you directly with the IRS. Schedule your free 30-minute consultation today and get a clear plan built around your actual numbers.