Owing the IRS more than you can pay is stressful, but it doesn't always mean you're stuck paying the full amount. The IRS Offer in Compromise application gives qualifying taxpayers a legitimate path to settle their tax debt for less than what they owe. It's one of the most powerful tools available for tax relief, and one of the most misunderstood. The process involves specific forms, fees, and eligibility requirements that trip people up before they even get started.

At Tax Experts of OC, our CPAs and Enrolled Agents help clients across all 50 states navigate the Offer in Compromise process from start to finish. We've seen firsthand how small mistakes on the application can lead to rejection, costing taxpayers months of time and leaving them back at square one. That's why understanding the process matters, whether you're filing on your own or working with a professional to strengthen your case.

This guide walks you through everything you need to file an Offer in Compromise in 2026: who qualifies, which forms to submit, what it costs, and how to avoid common pitfalls. By the end, you'll have a clear picture of whether an OIC is the right move for your situation and exactly how to move forward.

What an IRS offer in compromise is and isn't

The Offer in Compromise is a formal IRS program that allows you to settle your federal tax debt for less than the total amount you legally owe. It's governed by IRC Section 7122 and administered through a specific application process with defined eligibility rules, calculation methods, and deadlines. Before you invest time in preparing an application, you need a clear picture of what this program actually does, and what it doesn't do, so you can make an informed decision about whether to pursue it.

What the OIC actually does

When you submit an IRS offer in compromise application, you're proposing a specific dollar amount that you believe represents the most the IRS can reasonably expect to collect from you given your current financial situation. The IRS evaluates that number against what it calls your Reasonable Collection Potential (RCP), which is a calculation based on your available assets, monthly income, and allowable living expenses. If your proposed amount meets or exceeds your RCP, the IRS will generally accept the offer.

The program recognizes three separate legal grounds for submitting an offer, and your application must identify which one applies. Choosing the wrong basis is one of the most common reasons applications stall or get returned before the IRS even reviews the financials.

| Basis | When it applies |

|---|---|

| Doubt as to Collectibility (DATC) | You can't pay the full balance before the IRS's 10-year collection window closes |

| Doubt as to Liability (DATL) | You dispute whether the tax debt is accurate or legally valid |

| Effective Tax Administration (ETA) | The debt is valid and collectible, but full payment would create serious economic hardship or be fundamentally unfair |

The vast majority of accepted offers fall under Doubt as to Collectibility, where the IRS concludes that your financial picture makes full collection unlikely.

What the OIC is not

The OIC is not a guaranteed settlement program, and it's not available to every taxpayer who owes money. The IRS accepts a relatively small percentage of applications each year. Applicants who submit without verifying eligibility first often lose their $205 application fee, have their collection clock paused during the review period, and end up back where they started months later with no relief secured.

An offer in compromise is also not a replacement for an installment agreement if you can realistically afford to pay your debt over time. The IRS will reject your offer if your RCP shows you have the income and assets to cover the balance through a structured payment plan. Submitting an OIC when a payment plan is the appropriate solution wastes review time and can signal to the IRS that you're attempting to avoid a reasonable payment arrangement.

The OIC does not apply to all tax-related debts automatically. Certain federal tax debts connected to fraud penalties or trust fund recovery penalties require additional scrutiny. Additionally, the program is not a bankruptcy proceeding; discharging tax debt through bankruptcy is an entirely separate legal process with different courts, rules, and timelines that don't intersect with the OIC program.

Finally, submitting an offer does not immediately stop all IRS enforcement action. The IRS will suspend most collection activities while your offer is under review, but it can still file a Notice of Federal Tax Lien during that period. Understanding this distinction matters if you're also managing wage garnishments or bank levies while your application is pending.

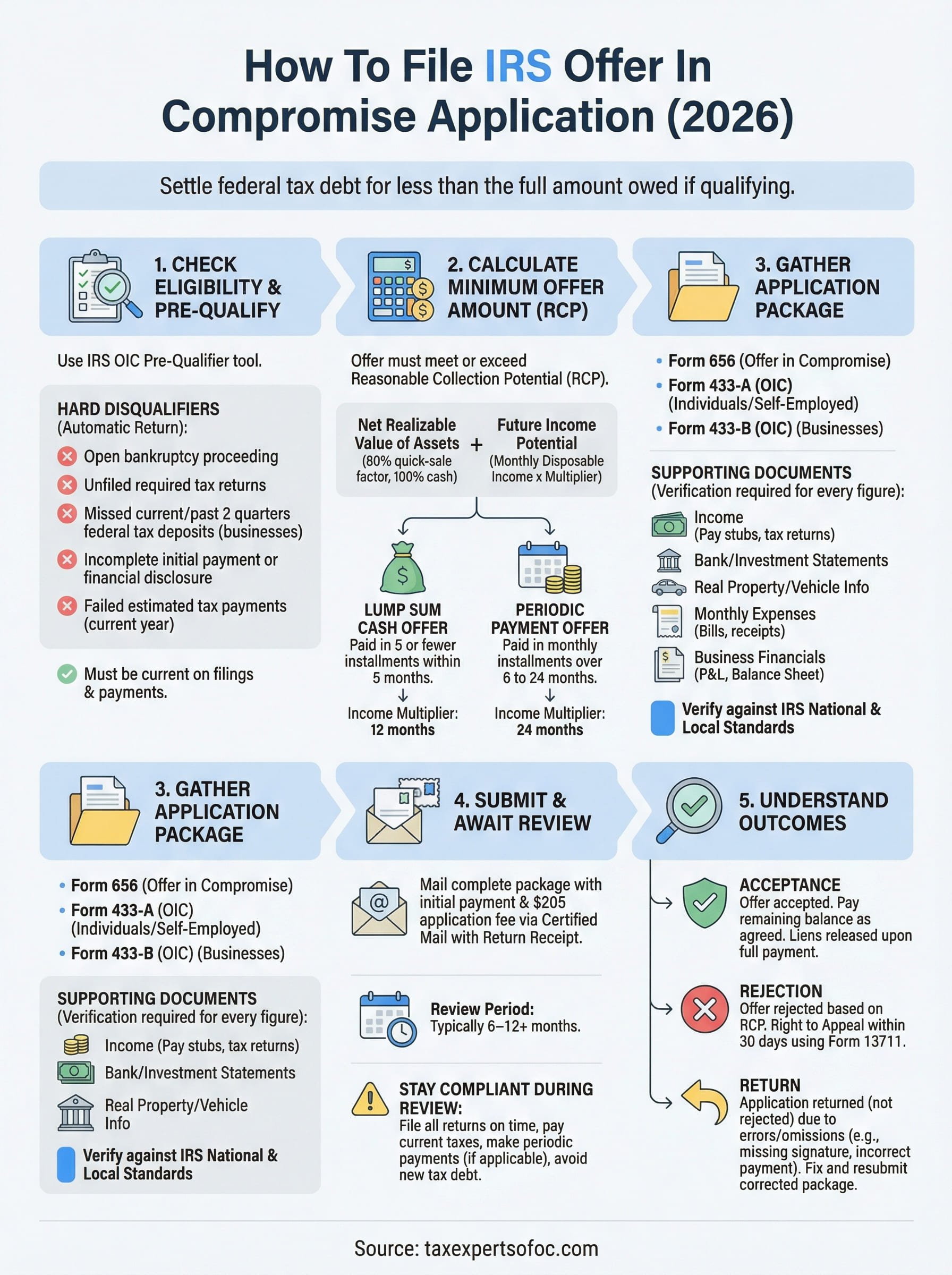

Check eligibility before you apply

The IRS has a strict pre-screening process, and submitting an IRS offer in compromise application without checking eligibility first is a reliable way to lose your $205 application fee and delay resolution by months. Before you touch Form 656, run yourself through the IRS's OIC Pre-Qualifier tool at irs.gov to get an initial read on whether you're likely to qualify based on your income, assets, and expenses.

Hard disqualifiers

Some circumstances automatically disqualify you from the program regardless of how little you can pay. The IRS will return your application without consideration if any of these apply, and your fee will not be refunded.

- You are currently in an open bankruptcy proceeding

- You have not filed all required tax returns (the IRS requires every return to be filed before it reviews an offer)

- You are a business owner with employees and have not made all required federal tax deposits for the current and past two quarters

- You did not include the $205 application fee or a complete financial disclosure

- You failed to make required estimated tax payments for the current tax year

Clearing these five checkpoints before you apply is the single most effective way to prevent an automatic return of your application.

What the IRS measures to determine financial eligibility

Once you clear the hard disqualifiers, financial eligibility comes down to one core question: can the IRS realistically collect more from you than what you're proposing to pay? The IRS answers that by calculating your Reasonable Collection Potential (RCP), which combines the net realizable value of your assets with your future income potential minus allowable living expenses.

Your monthly disposable income plays a significant role in this calculation. The IRS uses its own National and Local Standards to cap what you're allowed to spend on housing, food, transportation, and healthcare. If your actual expenses exceed those caps, the IRS will still use the cap figure, not your real spending, when it determines what you can pay. This often surprises applicants who assumed their actual budget would serve as the benchmark. Before estimating any offer amount, look up the applicable IRS expense standards for your county and household size directly on irs.gov so you're working from the same numbers the IRS will use.

Gather what you need for the application package

Pulling together a complete application package before you start filling out forms saves you from scrambling mid-process and reduces the risk of submitting an incomplete package that the IRS returns without review. The IRS offer in compromise application consists of two primary components: the financial disclosure collection statement and Form 656. Every document you include should directly support the numbers you report in those forms, because the IRS will request verification for anything it can't confirm from its own records.

The core IRS forms

Your application package always includes Form 656, which is the actual offer document where you identify your basis for applying, propose your settlement amount, and select a payment option. Alongside it, you submit a financial collection statement that gives the IRS a full picture of your assets, income, expenses, and liabilities.

- Form 433-A (OIC) for individual taxpayers and self-employed filers

- Form 433-B (OIC) for businesses, including corporations, partnerships, and LLCs

- Form 656-L only if you're submitting based on Doubt as to Liability, which replaces Form 433-A or 433-B entirely

Download the most current versions of these forms directly from irs.gov to ensure you're using the 2025 revision and not an outdated version.

Supporting financial documents

The IRS requires documentation for every figure you report on your collection statement. Submitting forms without backup evidence invites requests for additional information, which stalls the review and extends your case timeline. Gather these documents before you fill out a single line on Form 433-A or 433-B.

| Document category | What to collect |

|---|---|

| Income verification | Last three months of pay stubs, most recent two years of tax returns, business profit and loss statements |

| Bank and investment accounts | Last three months of statements for all checking, savings, and brokerage accounts |

| Real property | Most recent mortgage statement, property tax bill, and a current market value estimate |

| Vehicle assets | Loan statements and registration showing current year, make, and model |

| Monthly expenses | Utility bills, insurance premiums, childcare invoices, and medical expense receipts |

| Business financials | Payroll records, accounts receivable aging reports, and current balance sheet |

Once your documents are organized by category, cross-reference each figure against the IRS National and Local Standards you identified during eligibility screening. If a reported expense exceeds the IRS cap for your area, note the actual allowable figure so you're entering the correct number on the form, not your real spending.

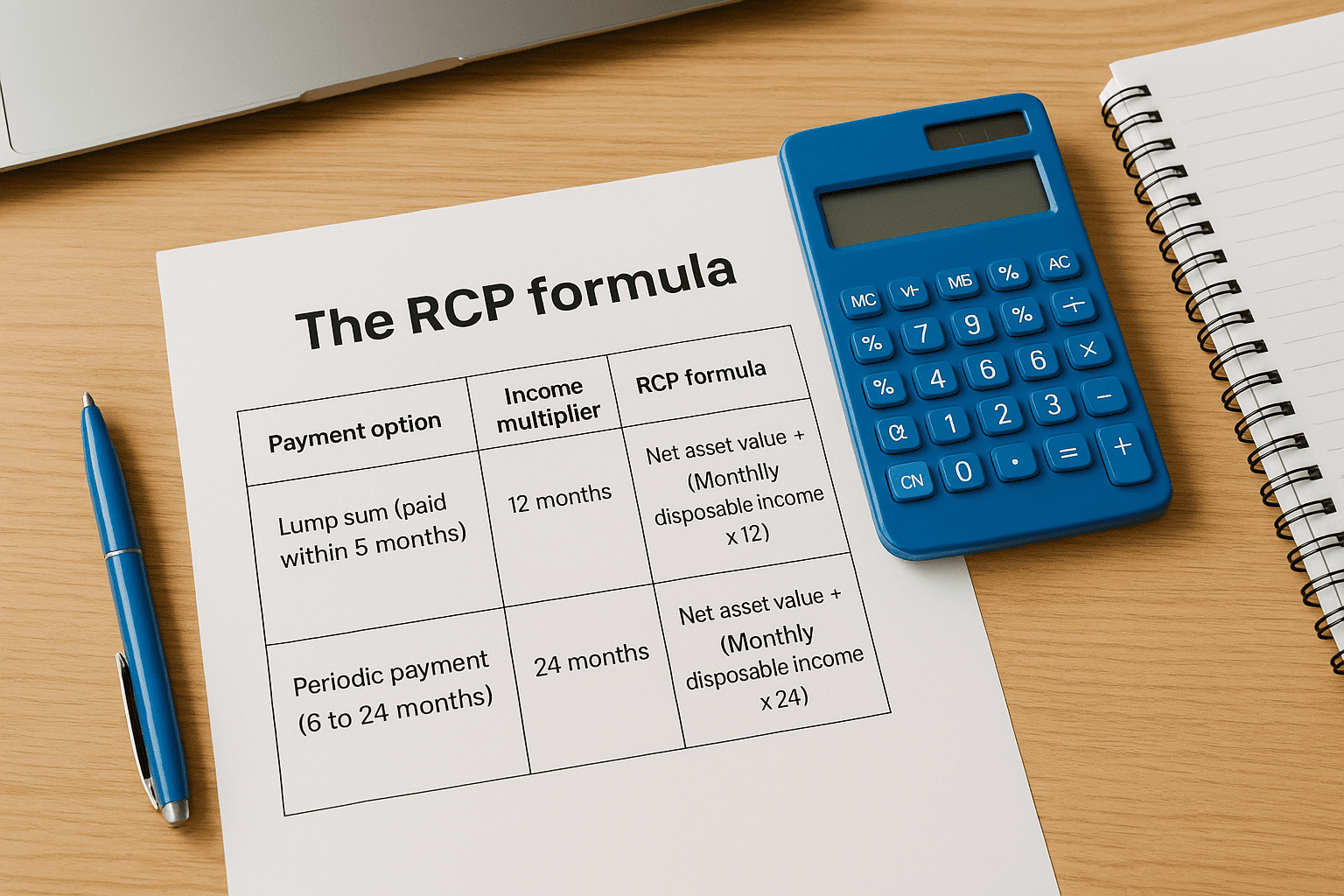

Calculate your minimum offer amount

The number you write on your IRS offer in compromise application has to reflect a specific calculation, not a figure you choose because it feels affordable. The IRS measures every submitted offer against your Reasonable Collection Potential (RCP), which is the maximum amount the IRS believes it can realistically collect from you before the 10-year collection statute expires. Your proposed offer must meet or exceed that figure to have a genuine chance of acceptance, so running this calculation before you fill out Form 656 is one of the most important steps in the process.

The RCP formula

Your RCP combines two separate components: the net realizable value of your assets and your future income potential multiplied over a defined period. The multiplier the IRS applies to your monthly disposable income depends directly on the payment option you select, so the two calculations are linked. A shorter payment window produces a lower multiplier, which often results in a lower minimum offer amount.

| Payment option | Income multiplier | RCP formula |

|---|---|---|

| Lump sum (paid within 5 months) | 12 months | Net asset value + (Monthly disposable income x 12) |

| Periodic payment (6 to 24 months) | 24 months | Net asset value + (Monthly disposable income x 24) |

The lump sum path typically generates a lower floor amount, which is why applicants who can access funds through retirement accounts, family loans, or personal assets often choose it to reduce the size of the required offer.

Net realizable value of your assets

The IRS does not use full fair market value when it counts your assets. Instead, it applies a quick-sale factor of 80% to most asset categories, reflecting what those assets would realistically bring in a forced or expedited sale. Cash and bank balances are counted at 100% with no discount applied. For example, if you own a vehicle with a fair market value of $18,000 and an outstanding loan of $9,000, the IRS calculates the net realizable value as: ($18,000 x 0.80) - $9,000 = $5,400. Run this calculation separately for each asset you disclose on your collection statement.

Future income calculation

Your monthly disposable income equals your gross monthly income minus your IRS-allowable living expenses based on the National and Local Standards. If your gross income is $5,500 per month and your IRS-allowed expenses total $4,600, your disposable income is $900. For a lump sum offer, the future income component is $900 x 12 = $10,800. Add that figure to your net asset total to determine your minimum offer floor before you write any number on Form 656.

Choose a payment option and prep your payment

The IRS gives you two payment options on Form 656, and the one you select directly affects the size of your minimum offer and the upfront payment you must submit with your application. Choose your payment option before you finalize your offer amount, because the income multiplier tied to each option changes your RCP floor. Failing to include the correct upfront payment is one of the most common reasons the IRS returns an application without review, and that payment is nonrefundable either way.

Lump Sum Cash Offer

A lump sum offer requires you to pay your full proposed settlement in five or fewer installments within five calendar months of IRS acceptance. When you submit your IRS offer in compromise application under this option, you must include a nonrefundable payment equal to 20% of your total proposed offer amount at the time of filing. For example, if you propose a $12,000 settlement, you submit a $2,400 payment with your package. That amount gets applied to your tax balance whether the IRS accepts or rejects the offer, so confirm your proposed figure is accurate before you write that check.

Because the lump sum option uses a 12-month income multiplier instead of 24 months, it typically generates a lower minimum offer floor and is often the more cost-effective path when you can access funds upfront through savings, retirement accounts, or a personal loan.

Periodic Payment Offer

A periodic payment offer lets you pay your proposed settlement in monthly installments spread over six to 24 months. This option does not require a 20% deposit. Instead, you submit your first proposed monthly payment with your application and continue making those payments each month while the IRS reviews your case. Reviews often take six months to a year or longer, so the dollars add up fast.

One practical calculation to run before you commit: multiply your monthly payment by the estimated review period. If your payment is $600 and the review takes nine months, you will have sent $5,400 toward your balance before the IRS issues any decision, all of it nonrefundable. That figure should fit within your actual monthly cash flow without strain, because missing a single payment during the review period can cause the IRS to return your offer as noncompliant and force you to restart the entire process from scratch.

Fill out Form 656 the right way

Form 656 is a four-page document, and each section requires specific information in a specific sequence. Before you write a single word on the form, have your completed Form 433-A (OIC) or 433-B (OIC) in front of you, because you'll pull numbers directly from those financial statements. Filling out Form 656 in isolation without your supporting documents already finalized almost always produces inconsistent figures that trigger IRS requests for clarification or cause an outright return of your application.

Walk through each section of Form 656 in order

Form 656 is divided into numbered sections, and the IRS reviews them in sequence. Working through each one methodically reduces the chance of leaving a required field blank, which is one of the fastest ways to get your IRS offer in compromise application returned without review.

| Section | What it asks for | Common mistake |

|---|---|---|

| Section 1 | Taxpayer name, SSN or EIN, address, and contact information | Using a name that doesn't match IRS records exactly |

| Section 2 | Tax type and the specific tax periods covered by the offer | Omitting a tax year with an outstanding balance |

| Section 3 | Legal basis for the offer (DATC, DATL, or ETA) | Selecting ETA without a written explanation attached |

| Section 4 | Offer amount and payment option (lump sum or periodic) | Entering an amount below your calculated RCP floor |

| Section 5 | Source of funds for your payment | Leaving this blank or writing "savings" without specifics |

| Section 6 | Taxpayer signature and date | Forgetting a co-obligated spouse's signature on a joint liability |

If your offer covers a joint tax liability, both spouses must sign Form 656, even if only one spouse is submitting the financial collection statement.

Write a clear source of funds statement

Section 5 asks where your payment money is coming from, and the IRS takes this seriously. Vague answers like "personal funds" give the IRS no way to verify that your proposed payment is realistic or accessible. Instead, write a specific statement: "Funds will come from $8,000 in a Chase checking account (account ending in XXXX) and a $4,000 personal loan from a family member." If you're using retirement funds or selling an asset, name the account type and the estimated proceeds. A clear, specific source of funds statement tells the IRS your offer is grounded in an actual financial plan and reduces back-and-forth during the review period.

Submit your offer and avoid common errors

Once your Form 656, financial collection statement, supporting documents, and upfront payment are all prepared and verified, you're ready to submit. The IRS processes your irs offer in compromise application through a centralized submission system, and where you mail your package depends on your state of residence. Sending to the wrong processing center is an administrative error that delays your case by weeks before the IRS even opens your envelope.

Where and how to submit your package

The IRS directs applicants to one of two Offer in Compromise processing centers based on geography. You mail the complete package, not fax it, and you do not submit it through irs.gov. Use the mailing addresses published in the Form 656 Booklet, available at irs.gov, and verify the current address before you mail. These addresses have changed in previous years, and using an outdated booklet will route your package to the wrong center.

When you mail your package, send it via certified mail with return receipt requested through the USPS. This gives you a trackable record of the date the IRS received your application, which matters because the IRS collection statute is paused from the date of receipt, and you'll want proof of that date if a dispute arises later.

Errors that trigger automatic returns

The IRS returns incomplete applications without any review of the financials, and the fees you submitted are nonrefundable. Running through this checklist before you seal the envelope prevents the most common causes of automatic returns.

- Missing signature: Every required signer must have signed Form 656. Joint liabilities require both spouses.

- Incorrect or missing payment: Lump sum offers require 20% upfront. Periodic payment offers require the first installment.

- Unfiled tax returns: The IRS will not process your application if any required return remains unfiled.

- Missing collection statement: Form 656 without Form 433-A (OIC) or 433-B (OIC) is an incomplete package.

- Wrong form version: Using an outdated revision of Form 656 can trigger a return. Confirm you downloaded the current version from irs.gov.

- No application fee: The $205 fee must be included unless you qualify for the low-income exception.

Completing a final review against this list before mailing is the single fastest way to protect your application fee and keep your case moving forward without unnecessary delays.

What happens after you file

Once the IRS receives your irs offer in compromise application, the process moves through several distinct stages before you get a decision. The total review period typically runs six to twelve months, and sometimes longer for complex cases. Knowing what to expect at each stage helps you stay compliant, avoid mistakes that could derail your case, and respond quickly when the IRS contacts you.

The IRS acknowledgment period

After the IRS receives your package, it will send you a written acknowledgment letter that confirms receipt and assigns your case a unique offer number. This letter usually arrives within four to six weeks. Keep it in a safe place, because the offer number is required any time you contact the IRS about your case status during the review.

The IRS collection statute of limitations is paused from the date the IRS receives your application through 30 days after a final determination is made, so document your certified mail receipt date immediately.

What the IRS examiner reviews

An IRS offer examiner is assigned to your case and will verify the financial information you reported on your collection statement against IRS records and third-party data sources. The examiner may call you or your authorized representative to request additional documentation, clarify a reported figure, or ask about a specific asset.

Respond to every examiner request within the deadline stated in the letter, typically 10 to 30 days. Missing a response deadline gives the examiner grounds to reject your offer based on insufficient information, and you'll have limited options to appeal that outcome. If you used a tax professional to prepare your application, make sure they are listed on a Form 2848 Power of Attorney so the examiner contacts them directly on your behalf.

Your obligations while the IRS reviews your case

Your responsibilities don't stop the moment you mail your package. The IRS requires you to stay fully compliant throughout the entire review period, and any lapse in compliance is grounds for rejection.

- File all required tax returns on time, including any returns due after you submit your offer

- Pay all current taxes as they come due, including estimated tax payments if you're self-employed

- Make every installment payment on schedule if you selected the periodic payment option

- Avoid incurring new tax debt, which signals to the examiner that your financial situation may be worse than reported

Missing any of these obligations signals to the IRS that you cannot manage an ongoing payment commitment, which directly undermines the credibility of your proposed settlement amount.

If the IRS rejects or returns your offer

Getting a rejection or return on your irs offer in compromise application is not the end of the road, but how you respond depends entirely on which outcome you received. The IRS treats a returned application differently from a formal rejection, and the steps available to you are different in each case. Understanding that distinction upfront saves you from filing the wrong response and losing time you don't have.

The difference between a rejection and a return

A returned application means the IRS never reviewed your financials. The IRS returns offers when a required element is missing, such as an unfiled tax return, an incomplete Form 433-A, or a missing application fee. A return is not a decision on the merits of your offer, so you can fix the identified issue and resubmit a corrected package without filing an appeal. Review the return letter carefully, because the IRS will specify exactly what was missing or incorrect.

A formal rejection means the IRS reviewed your financials and determined your offer does not meet or exceed your Reasonable Collection Potential. This triggers your right to appeal, and you have a defined window to use it.

How to appeal a rejection

You have 30 days from the date on your rejection letter to file an appeal with the IRS Office of Appeals. Miss that window and you lose the right to appeal that specific offer. To file, submit Form 13711 (Request for Appeal of Offer in Compromise) directly to the address listed on your rejection letter, along with a written statement explaining why you believe the examiner's determination was incorrect.

A strong appeal focuses on specific numbers, not general hardship. If the examiner overvalued an asset or disallowed a legitimate expense, state the correct figure and attach supporting documentation.

Your appeal statement should follow this structure:

- State the issue clearly: Identify the specific item in dispute, such as a vehicle valuation or a disallowed expense category

- Provide the corrected figure: Give the number you believe is accurate based on your documentation

- Attach evidence: Include bank statements, appraisals, medical bills, or any record that supports your position

- Request a conference: Ask for an in-person or phone conference with an Appeals Officer to present your case directly

If your appeal is denied, you can revise your offer amount and submit a new application based on updated financials, or explore alternative resolution options such as an installment agreement or Currently Not Collectible status.

Next steps

Filing an irs offer in compromise application is a structured process with real consequences for mistakes, but you now have the full picture: eligibility requirements, form preparation, offer calculation, submission steps, and what to do if the IRS pushes back. The process rewards preparation and penalizes shortcuts, so treat every step in this guide as a checkpoint, not a suggestion.

Your most important action right now is to check your eligibility before touching any forms. Pull your IRS transcripts, verify that all required returns are filed, and run your numbers against the Reasonable Collection Potential formula using the current IRS expense standards for your county. If the math is close or your financial situation is complicated, working with a qualified professional protects your fee and your timeline.

Tax Experts of OC offers a free 30-minute consultation with a CPA or Enrolled Agent who can review your case and tell you exactly where you stand.