Filing your federal income tax return starts with one document: IRS Form 1040 instructions. Whether you're reporting straightforward W-2 wages or juggling multiple income sources, these instructions tell you exactly what goes on each line, and what you can skip. The problem is, the IRS booklet runs over 100 pages, and most of it doesn't apply to your situation.

That's why we built this guide. At Tax Experts of OC, our CPAs and Enrolled Agents help individuals and business owners across all 50 states file accurate returns and resolve tax issues with the IRS. We've distilled the official Form 1040 instructions into a practical, line-by-line walkthrough so you can complete your 2025 tax year return with confidence. Below, you'll find clear explanations for each section of the form, along with tips on common mistakes that trigger IRS notices, and how to avoid them.

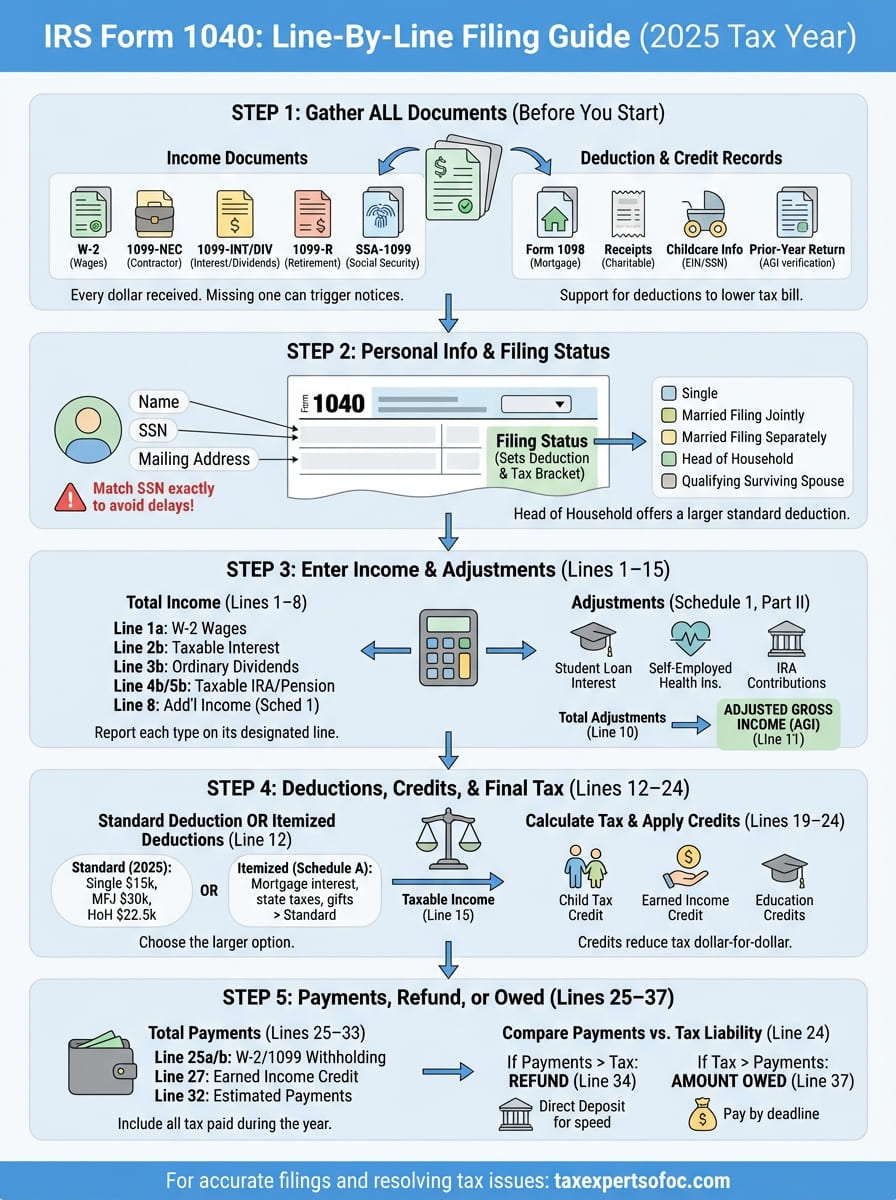

What to gather before you start Form 1040

Before you open the IRS Form 1040 instructions, spend 15 minutes pulling together every document you need. Starting without them means you'll stop mid-form to hunt for numbers, which leads to errors and missed deductions. The IRS matches the figures on your return against the information returns it already has, so every number must line up exactly.

Missing even one income document can trigger an IRS notice months after you file.

Income Documents

Your return requires a record of every dollar you received during the tax year. Gather all of the following before you complete a single line:

- W-2 from each employer showing wages and taxes withheld

- 1099-NEC for freelance or contractor income over $600

- 1099-INT and 1099-DIV for interest and dividend income

- 1099-B for stock or investment sales

- 1099-R for pension, IRA, or annuity distributions

- SSA-1099 if you received Social Security benefits

- Schedule K-1 if you are a partner, shareholder, or trust beneficiary

Deduction and Credit Records

Deductions and credits directly lower what you owe, so the supporting records matter just as much as your income documents. Pull together receipts, statements, and letters that cover each of the following:

- Mortgage interest statement (Form 1098) and property tax bills

- Student loan interest paid, also reported on Form 1098-E

- Charitable contribution receipts for cash and non-cash donations

- Childcare provider information, including the provider's EIN or SSN

- Health insurance premium records if you are self-employed

- Prior-year tax return for your adjusted gross income, which most e-file systems require to verify your identity

Having these documents ready before you start keeps the process moving and lowers the chance you will need to file an amended return later.

Step 1. Complete your personal info and filing status

The top of Form 1040 is where you enter your name, Social Security number (SSN), and mailing address. The IRS matches your SSN to its records first, so a single digit error here can delay your refund or trigger an identity verification letter.

Your Name, SSN, and Address

Enter your name exactly as it appears on your Social Security card, and use your current mailing address even if it differs from last year's return. If you are filing jointly, list both spouses' SSNs in the same order every year. Watch for these common errors:

- Transposed SSN digits

- Nickname instead of legal name

- Old address that no longer receives mail

Choosing the Right Filing Status

Your filing status sets your standard deduction and tax bracket, so picking the wrong one costs you money. The irs form 1040 instructions outline five options:

| Status | Basic requirement |

|---|---|

| Single | Unmarried as of December 31 |

| Married Filing Jointly | Married; both spouses file together |

| Married Filing Separately | Married but filing individual returns |

| Head of Household | Unmarried; paid over half the cost of a home for a qualifying person |

| Qualifying Surviving Spouse | Spouse died in the prior two years; dependent child lives with you |

If you qualify for Head of Household, you receive a larger standard deduction than Single filers, which directly reduces your tax bill.

Step 2. Enter income and adjustments the right way

Lines 1 through 15 of Form 1040 build your total income and then reduce it down to your adjusted gross income (AGI). The AGI figure controls your eligibility for many credits and deductions, so accuracy here affects the rest of your return.

Report every income source on Lines 1 through 8

The irs form 1040 instructions break income into specific line entries. Each income type belongs on a designated line, and mixing them up can trigger an IRS mismatch notice.

- Line 1a: W-2 wages

- Line 2b: Taxable interest

- Line 3b: Ordinary dividends

- Line 4b: IRA distributions (taxable amount)

- Line 5b: Pension and annuity income

- Line 8: Additional income from Schedule 1, Part I

Enter only the taxable portion on lines 4b and 5b, not the gross distribution amount.

Reduce your income with Schedule 1 adjustments

Above-the-line adjustments on Schedule 1, Part II lower your AGI before you reach the deduction section. Common adjustments include student loan interest, self-employed health insurance premiums, and contributions to a traditional IRA. Transfer the total from Schedule 1, Line 26 to Form 1040, Line 10, and subtract it from your total income to get your AGI on Line 11.

Step 3. Take deductions, claim credits, and compute tax

Lines 12 through 24 of Form 1040 convert your AGI into taxable income, then apply credits to reduce what you actually owe. This section is where most of the tax savings happen, so follow the irs form 1040 instructions closely.

Choose between standard and itemized deductions

Your standard deduction is the faster option, and for most filers it produces the bigger result. For the 2025 tax year, the amounts are:

| Filing Status | Standard Deduction |

|---|---|

| Single | $15,000 |

| Married Filing Jointly | $30,000 |

| Head of Household | $22,500 |

If your itemized deductions (mortgage interest, state taxes, charitable gifts) exceed those figures, complete Schedule A and enter that total on Line 12 instead.

You cannot claim both the standard deduction and itemized deductions on the same return.

Apply credits and calculate your final tax

After you subtract your deduction on Line 12, enter your taxable income on Line 15 and use the IRS tax tables to find your gross tax. Then subtract any credits on Lines 19 through 24. Common credits include the Child Tax Credit, Earned Income Credit, and education credits, each of which reduces your tax dollar-for-dollar.

Step 4. Add payments, choose refund or amount owed, and file

Lines 25 through 33 of Form 1040 pull together everything you already paid toward your 2025 tax bill, then compare that total against your computed tax. The result determines whether you get a refund or owe a balance, and filing the wrong numbers here is one of the most common reasons the IRS sends a correction notice.

Enter your tax payments on Lines 25 through 32

The irs form 1040 instructions direct you to report each payment type on a separate line. Entering them correctly avoids mismatches with IRS records:

- Line 25a: Federal income tax withheld from W-2s

- Line 25b: Federal income tax withheld from 1099s

- Line 26: Prior-year refund applied to this year

- Line 27: Earned Income Credit

- Line 32: Amount from Schedule 3, which captures additional credits and estimated tax payments

Claim your refund or pay what you owe

After you total your payments on Line 33, subtract your tax on Line 24. A positive result goes on Line 34 as your refund; enter your bank routing and account numbers to receive it by direct deposit. If your tax exceeds your payments, enter the difference on Line 37.

Direct deposit is the fastest way to receive your refund, typically within 21 days of e-filing.

Wrap up and what to do next

Following the irs form 1040 instructions section by section keeps your return accurate and reduces the chance the IRS will send you a notice. You now know what documents to gather, how to report every income source correctly, which deductions and credits apply to you, and how to submit your payment or claim your refund. Each step builds on the last, so skipping ahead creates errors that compound.

If your tax situation involves back taxes, IRS notices, or unfiled returns, a DIY approach can put you at risk. The stakes are higher when penalties and interest are already accumulating. Our CPAs and Enrolled Agents work with individuals and businesses across all 50 states to resolve those issues and get returns filed correctly.

Book a free 30-minute consultation with Tax Experts of OC today and get clear answers about your specific tax situation.