Seeing your paycheck shrink because the IRS is taking a cut is more than frustrating, it's financially devastating. If you're wondering how to stop IRS wage garnishment, you're likely already feeling the pressure of reduced income while trying to cover rent, groceries, and other essentials. The good news is that wage levies aren't permanent, and there are concrete steps you can take to release the hold on your earnings.

At Tax Experts of OC, we help clients across the country navigate IRS collections and reclaim control of their finances. Our CPAs and Enrolled Agents handle wage garnishment cases regularly, and we've seen firsthand how taking quick action makes a measurable difference in outcomes. Whether you owe $5,000 or $500,000, real options exist to stop or reduce what the IRS takes from each paycheck.

This guide walks you through the specific methods available to halt an IRS wage levy, from installment agreements to financial hardship claims to offer in compromise negotiations. You'll learn what triggers these garnishments, what rights you have as a taxpayer, and the exact steps to move forward with confidence.

What IRS wage garnishment is and how it starts

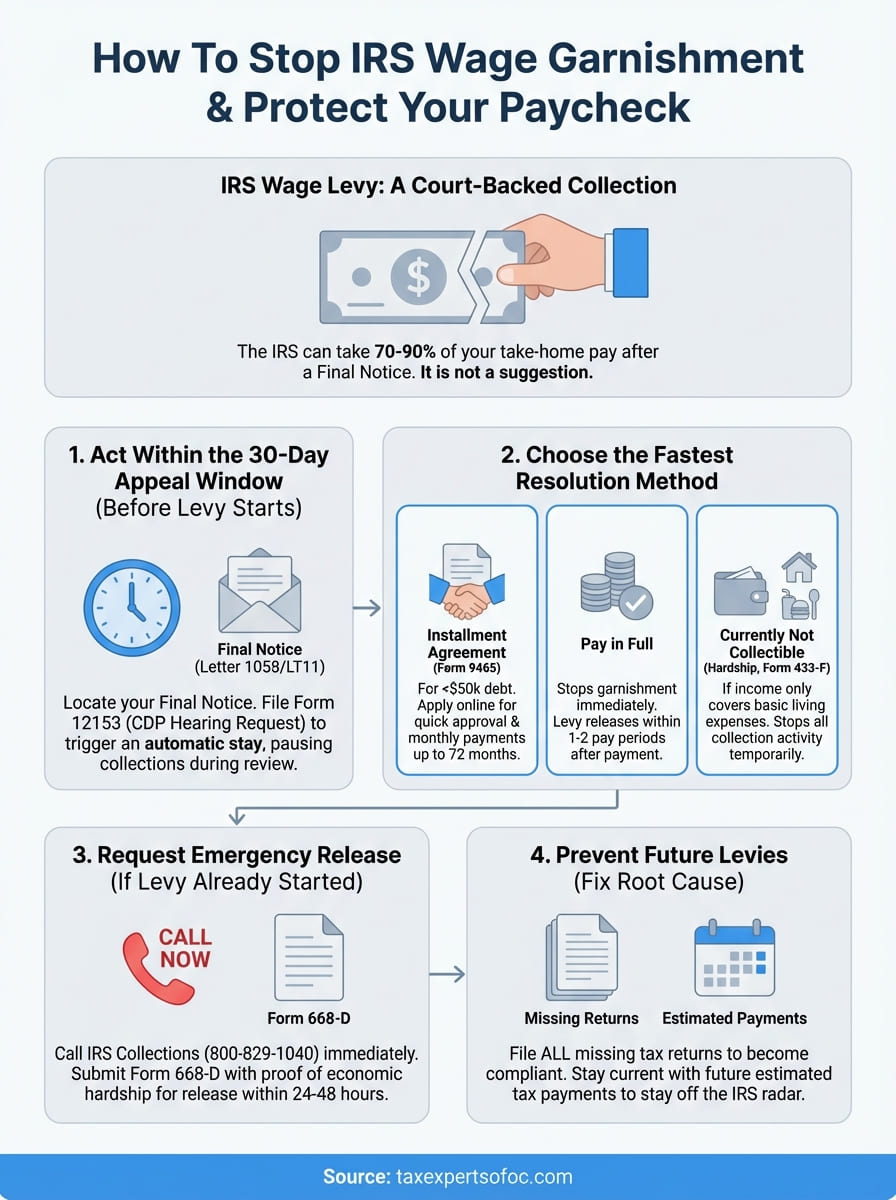

IRS wage garnishment (officially called a wage levy) gives the government legal authority to take money directly from your paycheck before you ever see it. Your employer receives a notice requiring them to withhold a portion of your earnings and send it to the IRS until your tax debt is satisfied or another arrangement is made. This isn't a suggestion or a request; it's a court-backed collection action that your employer must follow or face penalties themselves.

How the IRS gets authority to take your wages

The IRS doesn't start garnishing wages overnight. You'll receive multiple notices over several months before a levy hits your account. The process begins with a tax bill (Notice CP14 or similar), followed by additional collection letters if you don't respond or pay. After at least two notices, the IRS sends a Final Notice of Intent to Levy (Letter 1058 or LT11), which gives you 30 days to appeal before they can legally garnish your wages.

Most taxpayers miss or ignore these warnings because they don't understand the urgency. Once that 30-day period expires, the IRS contacts your employer directly with Form 668-W, and the garnishment starts with your next pay period. Understanding how to stop IRS wage garnishment requires catching the issue during this notice period or acting immediately after the levy begins.

If you received a Final Notice of Intent to Levy, you have appeal rights that can pause collections while you work out a solution.

What the IRS can take from each paycheck

The IRS doesn't take a fixed percentage like other creditors. Instead, they use a formula based on your filing status and number of dependents, leaving you with only a small exempt amount for basic living expenses. For a single person with no dependents in 2026, that could mean the IRS takes everything above roughly $1,000 per month, regardless of your actual bills or obligations.

Your employer calculates the levy amount using IRS Publication 1494. The exempt amount changes annually and varies by pay frequency (weekly, biweekly, monthly). Unlike other garnishments limited to 25% of disposable income, IRS levies can consume 70% to 90% of your take-home pay, making it nearly impossible to cover rent, transportation, or food.

Step 1. Find the notice and protect your rights

The first move in learning how to stop IRS wage garnishment is tracking down the Final Notice of Intent to Levy (Letter 1058, LT11, or CP90) that the IRS sent you. This document gives you specific appeal rights and a countdown clock that determines whether you can stop the garnishment before it starts or need to take emergency action after the fact. You'll find the notice date, the tax years involved, and the total amount owed, all critical for building your defense.

Locate your Final Notice of Intent to Levy

Check your mailbox, email spam folder, and any mail addressed to previous residences where you might have lived when the IRS sent notices. The IRS mails these documents via certified mail to your last known address on file, which may not be current if you've moved recently. If you can't find the physical notice, call the IRS at 800-829-1040 with your Social Security number and ask for the levy notice date and the specific tax periods included.

Your notice includes a Collection Due Process (CDP) appeal deadline, typically 30 days from the notice date. Missing this window doesn't mean you lose all options, but it eliminates your automatic right to pause collections while the IRS reviews your case.

What to do within the 30-day window

File Form 12153 (Request for a Collection Due Process or Equivalent Hearing) before the deadline expires if you want to challenge the levy or propose an alternative payment arrangement. This form triggers an automatic stay, meaning the IRS cannot start wage garnishment while your appeal is under review. You can request an installment agreement, offer in compromise, or currently not collectible status through this process.

Filing Form 12153 within 30 days of your Final Notice stops the IRS from garnishing wages while your case is reviewed.

Submit the form via certified mail or fax to the address listed on your notice to create a paper trail proving you met the deadline.

Step 2. Choose the fastest way to stop the levy

Once you've found your levy notice and understand your timeline, you need to pick the fastest resolution method that fits your financial situation. The IRS offers several paths to stop wage garnishment, and choosing the right one depends on whether you can pay immediately, need time to pay, or genuinely cannot afford to pay anything right now. Your goal is to halt the levy while keeping the IRS off your back long-term.

Pay the full amount or set up an installment agreement

Paying your total tax debt (including penalties and interest) stops the garnishment immediately. Once the IRS receives full payment, they release the levy within one to two pay periods. If you can't pay in full, filing Form 9465 (Installment Agreement Request) offers the next fastest route to halt collections, especially if you owe less than $50,000 in combined tax, penalties, and interest.

The IRS typically approves streamlined installment agreements within 72 hours if you owe under $50,000 and can pay off the balance within 72 months. You'll make monthly payments based on what you can afford, and the wage levy stops once the agreement is approved and active. Apply online through the IRS website or submit Form 9465 by mail or fax to the address on your levy notice.

An approved installment agreement releases your wage garnishment and gives you up to six years to pay off your tax debt.

Request Currently Not Collectible status for immediate hardship

If your income barely covers basic living expenses like rent, food, and utilities, you can request Currently Not Collectible (CNC) status by proving financial hardship. Submit Form 433-F (Collection Information Statement) with documentation showing your monthly income and necessary expenses. The IRS evaluates whether collecting would create an undue burden, and if approved, they stop all collection activity, including wage garnishment.

CNC status isn't permanent. The IRS reviews your financial situation periodically and can resume collections if your income increases. Interest and penalties continue accruing during this time, but you get breathing room to stabilize your finances without losing your paycheck.

Step 3. If the levy already started, act today

If the IRS already started taking money from your paycheck, you need to act within the next business day to minimize further losses. Each pay period that passes means more money withheld before you can reverse the garnishment. Understanding how to stop IRS wage garnishment after it starts requires contacting the IRS immediately and filing the right forms to request an emergency release based on your financial situation.

Contact the IRS immediately to request release

Call the IRS Collections Division at 800-829-1040 as soon as you discover the garnishment. Have your Social Security number, the tax years involved, and recent pay stubs ready before you dial. Explain your financial hardship and ask the agent to review your case for an immediate levy release. The agent can process a release on the spot if you demonstrate that the garnishment prevents you from covering basic living expenses like rent, utilities, food, or medical care.

Document everything during the call, including the agent's name, ID number, and any case notes they create. Request a reference number for your conversation in case you need to follow up or escalate the issue.

Submit Form 668-D for emergency levy release

File Form 668-D (Release of Levy) if the phone call doesn't resolve the issue or if the agent requires written documentation. Attach proof of your monthly income and expenses, including rent receipts, utility bills, and grocery costs. The form requests that the IRS release the levy because continuing it creates an immediate economic hardship that prevents you from meeting necessary living expenses.

Filing Form 668-D with documented proof of financial hardship can stop wage garnishment within 24 to 48 hours if approved.

Fax the completed form to the number on your levy notice to create a time-stamped record, then follow up with a phone call to confirm receipt.

Step 4. Prevent another levy and fix the root issue

Knowing how to stop IRS wage garnishment solves your immediate crisis, but preventing future levies requires addressing the underlying tax compliance problem. The IRS won't hesitate to levy your wages again if you fall behind on new tax obligations or leave old returns unfiled. Fixing the root cause means catching up on all filing requirements and staying current with tax payments going forward, which keeps you off the IRS collections radar permanently.

File all missing tax returns to stop future collection action

The IRS considers you non-compliant if you have unfiled returns, even if you've set up a payment plan for existing debt. Pull your IRS Account Transcript online or by calling 800-908-9946 to identify which years remain unfiled. Gather W-2s, 1099s, and expense records for each missing year, then file those returns immediately, even if you can't pay what you owe.

Filing late returns stops the IRS from filing Substitute for Returns (SFR) on your behalf, which almost always results in higher tax bills because the IRS claims zero deductions and uses the least favorable filing status. Submit your returns electronically or by certified mail to create proof of filing.

Filing all missing returns removes the IRS's justification to impose additional penalties and keeps your payment agreement active.

Stay current with estimated tax payments

If you're self-employed or have income without withholding, make quarterly estimated tax payments using Form 1040-ES to avoid accumulating new debt. Calculate your payment by taking your expected annual tax liability, subtracting any withholding, and dividing by four. Pay by the deadlines: April 15, June 15, September 15, and January 15 of the following year.

Set up automatic payments through IRS Direct Pay or EFTPS (Electronic Federal Tax Payment System) so you never miss a deadline. Missing even one quarterly payment while on an installment agreement can trigger default and restart collection activity.

Next steps to get your paycheck back

You now have a clear roadmap for how to stop IRS wage garnishment and protect your income from ongoing levies. The key is taking immediate action whether that means filing Form 12153 within your 30-day window, requesting Currently Not Collectible status, or calling the IRS today to negotiate a payment plan. Every day you wait means another paycheck reduced or seized entirely.

If you're dealing with multiple tax years, unfiled returns, or complex financial hardship, handling this alone increases your risk of mistakes that delay relief. Our team at Tax Experts of OC has successfully stopped wage garnishments for clients in all 50 states by negotiating directly with IRS agents and filing the correct forms the first time. Schedule a free 30-minute consultation to discuss your specific situation and get professional help stopping your wage levy before your next pay period.