You check your bank account and the balance reads near zero. The IRS has frozen your funds, and now you can't pay rent, cover payroll, or buy groceries. If you're searching for how to stop IRS bank levy actions, you're likely dealing with this exact scenario, and you have a limited window to act before the bank sends your money to the IRS.

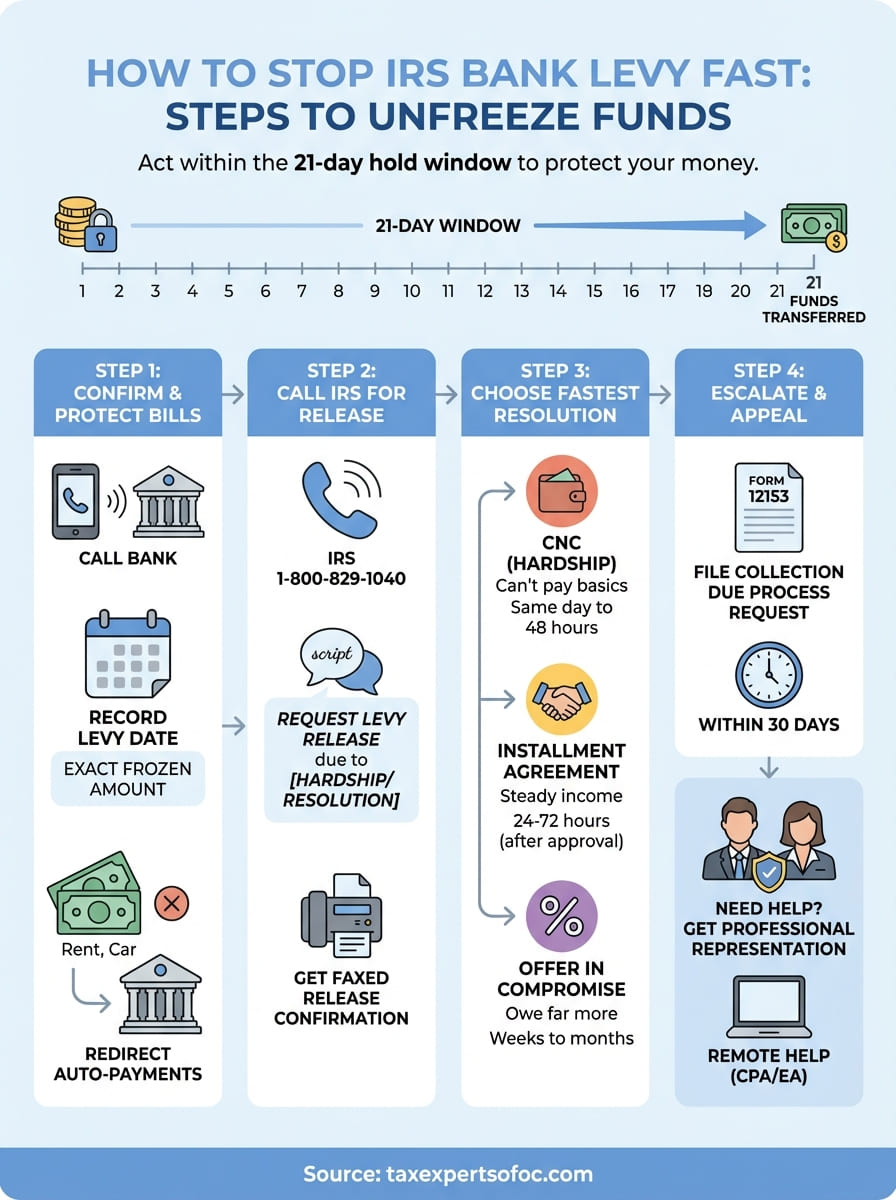

Here's what most people don't realize: once the IRS issues a levy, your bank places a 21-day hold on your funds before turning them over. That 21-day period is your opportunity to negotiate a release, prove financial hardship, or set up an alternative arrangement with the IRS.

At Tax Experts of OC, our CPA and Enrolled Agent work directly with the IRS on behalf of clients facing active levies, remotely, from anywhere in the country. This guide walks you through the specific steps you can take to get your bank account unfrozen, the forms you'll need, and when it makes sense to bring in a professional. We'll cover everything from same-day contact strategies to long-term resolution options that prevent future levies from happening again.

What an IRS bank levy does and the 21-day window

When the IRS issues a bank levy, it sends a legal demand directly to your financial institution, not to you. Your bank is legally required to freeze the exact amount you owe, including penalties and interest, in your account on the day it receives the notice. You don't get advance warning. The funds simply become inaccessible, and any direct deposits that arrive after the freeze point can still flow in and out normally since the levy only captures the balance on that specific date.

How the freeze actually works

Your bank holds the frozen funds for 21 calendar days before transferring them to the IRS. This hold exists to give you time to resolve the issue, but the clock starts the moment your bank receives the levy notice, not when you find out. During those 21 days, the frozen amount stays locked, but you can still use the rest of your account balance if any remains. For example, if the IRS levied $4,200 and you had $5,000 in the account, the remaining $800 is still accessible.

The 21-day window is the most critical period for anyone researching how to stop IRS bank levy actions. Once the bank wires those funds, recovering them becomes significantly harder.

What happens after day 21

If you take no action before day 21, the bank transfers the frozen amount to the IRS and the levy is satisfied to that extent. If you owe more than the account held, the IRS can issue additional levies against the same or other accounts. The IRS does not need a court order to repeat this process, which means the problem does not resolve itself without direct intervention on your part.

Step 1. Confirm the levy and protect essential bills

Before you can figure out how to stop IRS bank levy actions effectively, you need to verify exactly what was frozen and how much time remains in the 21-day window. Call your bank and ask a representative for the exact date the levy notice was received and the total amount currently frozen. Write this down immediately. That date determines your hard deadline for taking action.

Move critical payments right away

Once you know the frozen amount, redirect any automatic bill payments such as rent, utilities, and car payments to a different account or an alternative payment method. The IRS levy only captures the balance on the specific date it was issued, so funds held in a separate account are not at risk under that same levy notice.

Do not wait even one day to move essential payments. A bounced automatic payment adds late fees and credit damage on top of an already difficult situation.

Run through this checklist on day one:

- Record the levy date and the exact frozen amount

- Request written confirmation from your bank

- Redirect all automatic payments to a separate account

- Identify any direct deposits scheduled to land in the affected account and reroute them if possible

Step 2. Call the IRS and request a levy release

Call the IRS directly at 1-800-829-1040 as soon as you confirm the levy date. Explain that you received a levy notice, provide your Social Security Number or Employer Identification Number, and ask to speak with a Collections representative. Have your levy amount and bank contact information ready before you dial.

What to say when you call

Your goal on this call is to request a levy release and establish a resolution path before day 21. The agent will ask why the levy should be released. Provide a concrete reason, such as financial hardship, a pending installment agreement, or a filed appeal. Use this script when asking how to stop IRS bank levy actions over the phone:

"My name is [your name], SSN [number]. I'm calling about a bank levy issued on [date]. I am requesting a levy release due to [hardship/pending agreement] and would like to discuss resolution options before funds are transferred."

If the agent agrees, request a fax confirmation number sent directly to your bank. Your bank needs that written release document in hand before it can legally unfreeze the account.

Step 3. Choose the fastest fix for your situation

After you contact the IRS, the agent will want to know how you plan to resolve the underlying debt before releasing the levy. The resolution path you choose directly determines how quickly the freeze lifts and whether you're protected from future levies hitting the same account. Pick the option that best matches your current financial situation before that call ends.

Match your option to your finances

The IRS offers several resolution programs, and each one carries a different timeline for releasing a levy. Use this table to identify which route fits your circumstances:

| Resolution | Best if... | Typical release time |

|---|---|---|

| Currently Not Collectible (CNC) | You cannot cover basic living expenses | Same day to 48 hours |

| Installment Agreement | You have steady income with back taxes owed | 24 to 72 hours after approval |

| Offer in Compromise | You owe far more than you can realistically pay | Weeks to months |

Knowing how to stop IRS bank levy actions fast comes down to picking the right resolution on the first call, since switching approaches mid-process burns critical days in your 21-day window.

Claim hardship if funds cover essentials

If the levied funds cover rent, utilities, or payroll, tell the IRS representative you are experiencing financial hardship under IRC Section 6343. This can qualify you for same-day Currently Not Collectible status and a written levy release sent directly to your bank.

Step 4. If the IRS says no, escalate and appeal

Sometimes the IRS collections agent refuses to release the levy on the first call. That refusal is not the end of the road for anyone trying to figure out how to stop IRS bank levy actions through official channels. You have a formal right to appeal the levy through the IRS Office of Appeals, and filing that appeal can pause collection activity while your case is under review.

File a Collection Due Process Request

Your primary escalation tool is Form 12153, the Request for a Collection Due Process or Equivalent Hearing. Submit this form within 30 days of the original levy notice date to trigger a formal CDP hearing, where an independent IRS appeals officer reviews whether the levy was legally issued and whether alternative resolution options exist.

Filing Form 12153 does not automatically unfreeze your funds, but it signals to the IRS that you are formally contesting the action, which often opens the door to direct negotiation with an appeals officer rather than a collections agent.

Use this checklist when filing your CDP appeal:

- Download Form 12153 from IRS.gov

- Attach a copy of your original levy notice

- State your preferred resolution: installment agreement, CNC status, or Offer in Compromise

- Send via certified mail to the address listed on your levy notice

Next steps if you need help fast

The 21-day window moves fast, and every day you spend researching how to stop IRS bank levy actions without acting costs you time you cannot recover. If the IRS agent refused your release request, if you missed the CDP deadline, or if your financial situation is too complex to navigate alone, professional representation gives you the best shot at recovering your funds before the transfer date.

A licensed CPA or Enrolled Agent can contact the IRS directly on your behalf, negotiate a levy release, and set up the right resolution agreement in a single call. At Tax Experts of OC, our team handles active levies remotely for clients across all 50 states, with no requirement to visit an office in person.

Schedule your free 30-minute consultation with our tax resolution specialists today. Reach out to Tax Experts of OC and get a clear action plan before your 21-day window closes.