If you owe back taxes or just received a threatening IRS notice, you've probably come across the term "tax resolution" while searching for help. It sounds straightforward enough, but the details matter, especially when the IRS is on the other side of the table. Understanding what tax resolution actually involves is the first step toward making informed decisions about your finances and your future.

Tax resolution covers a range of strategies, from installment agreements and offers in compromise to penalty abatement and audit representation, all designed to settle or reduce your tax debt through legitimate IRS channels. But here's the problem: the industry is also full of companies that overpromise, charge steep fees upfront, and deliver little to nothing. Knowing the difference between real help and a scam can save you thousands of dollars and months of frustration.

At Tax Experts of OC, we handle tax resolution cases every day as licensed CPAs and Enrolled Agents, professionals who are authorized to represent you directly before the IRS. This article breaks down what tax resolution is, how the process works, what it typically costs, and how to spot red flags before you hand over your money.

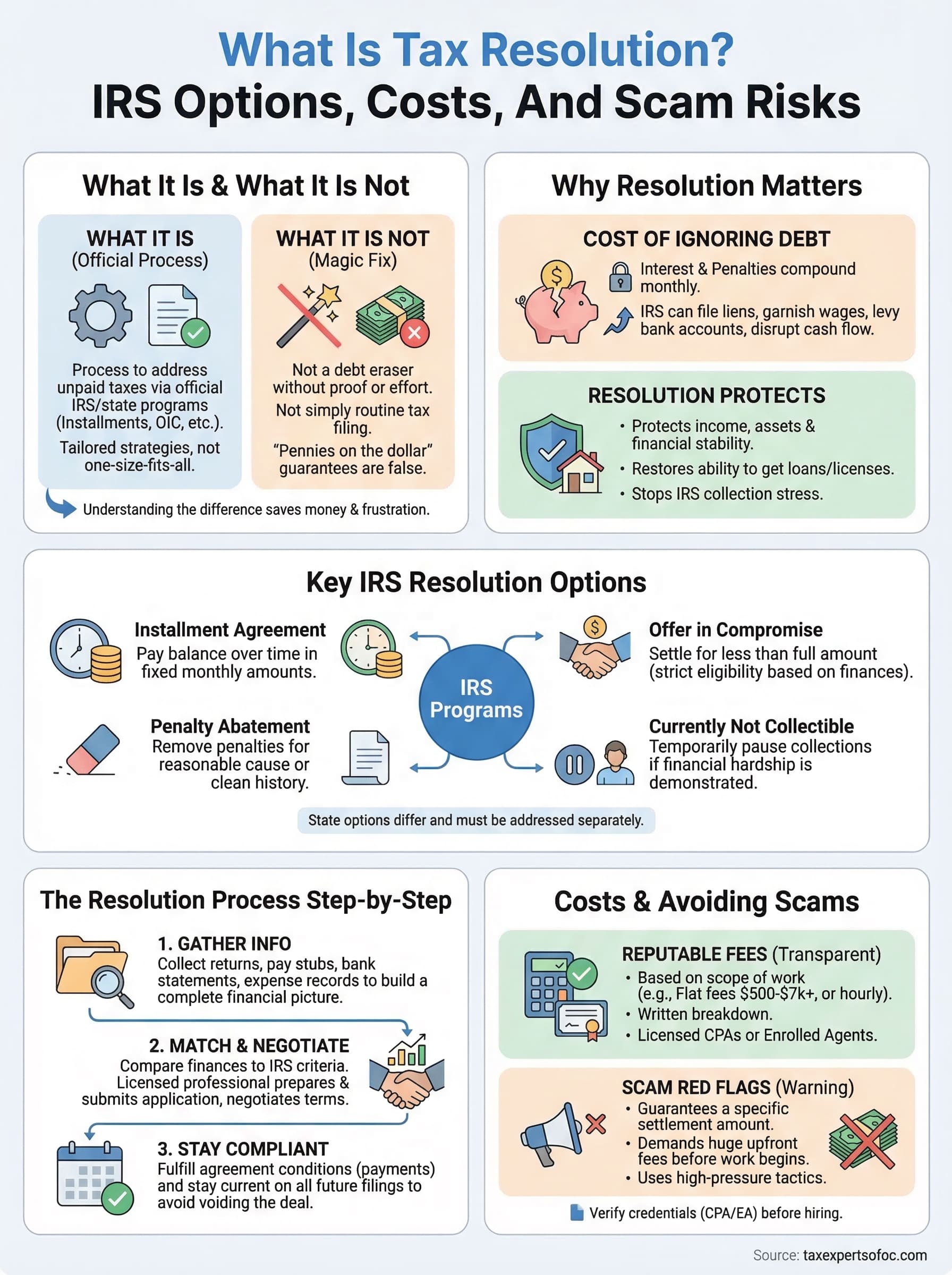

What tax resolution is and what it is not

When people ask what is tax resolution, the simplest answer is this: it is the process of working through official IRS or state tax agency programs to address unpaid taxes, penalties, or disputes that you can no longer manage on your own. It is not a single service or a one-size-fits-all fix. Instead, it is a broad category of strategies, each tailored to a specific financial situation, that a qualified professional uses to bring your tax account into a manageable or fully resolved state.

What tax resolution actually covers

Tax resolution includes several legitimate IRS programs created specifically to help taxpayers who owe more than they can pay in full. These programs include installment agreements, which let you pay your balance over time; offers in compromise, which allow you to settle your debt for less than the full amount owed if you meet strict eligibility criteria; penalty abatement, which can reduce or remove penalties if you have reasonable cause; and currently not collectible status, which temporarily pauses IRS collection activity if you can demonstrate financial hardship. Each of these tools requires accurate documentation, careful negotiation, and in most cases, direct professional representation before the IRS.

Enrolling in the wrong program, or misrepresenting your financial situation, can result in rejected applications, additional penalties, or a return to active IRS collections.

Tax resolution also covers situations that go beyond simple debt repayment. Audit representation places a licensed professional between you and the IRS during examinations, handling all correspondence and hearings on your behalf. Unfiled return assistance helps you prepare and submit years of missing returns before the IRS files substitute returns on its own terms, which almost always result in a higher balance owed than what you would actually owe with proper filing.

What tax resolution is not

Tax resolution is not a process that erases your debt without documentation, effort, or proof of your financial position. Many companies advertise that they can settle your tax debt for pennies on the dollar, but the IRS only accepts offers in compromise from a small percentage of applicants who meet specific income, expense, and asset thresholds. If your financial situation does not qualify, that advertised outcome is simply not available to you regardless of what a company promises.

Tax resolution is also not the same as tax preparation, which focuses on filing your returns accurately for a given tax year. Resolution deals with what happens after a filing problem already exists or after the IRS has taken collection action against you. Recognizing this difference helps you identify the right professional for your actual situation, rather than hiring someone who only handles routine filings and lacks the authority or experience to negotiate directly with the IRS on your behalf.

Why tax resolution matters for your finances

Unresolved tax debt does not sit still. The IRS charges both interest and failure-to-pay penalties that compound on your balance every month, meaning a debt you could have managed a year ago may now be significantly larger. Once you understand what is tax resolution and how it applies to your situation, you can act before that growth moves beyond your reach.

The real cost of ignoring IRS debt

When you leave a tax balance unaddressed, the IRS has broad legal authority to collect what it is owed without going to court first. That includes filing a federal tax lien against your property, issuing wage garnishments that take a portion of every paycheck, and levying funds directly from your bank accounts. These collection actions can damage your credit, disrupt your cash flow, and make it harder to secure financing for a home or business.

The IRS can seize your wages, bank accounts, and certain retirement funds if a tax debt goes unresolved long enough.

How resolution protects what you have built

The purpose of working through tax resolution is not just to satisfy a debt on paper. It is to protect your income, your assets, and your financial stability going forward. A qualified professional reviews your full financial picture, matches you to the most appropriate IRS program, and negotiates terms that reflect what you can actually afford rather than the full amount the IRS demands upfront.

Resolving your tax issues also restores your ability to move forward financially. Once your account is in good standing, you can qualify for loans, fulfill licensing requirements that depend on tax compliance, and stop the stress that comes with knowing the IRS is actively pursuing collections against you. That outcome is a practical financial benefit, not just a relief from paperwork.

IRS and state options used in tax resolution

When you ask what is tax resolution, the answer depends heavily on which IRS or state programs apply to your specific financial situation. The IRS offers several structured programs designed for taxpayers who cannot pay their full balance, and knowing which one fits your circumstances makes the difference between a workable solution and a rejected application.

Federal IRS programs

The IRS offers multiple routes depending on how much you owe and what you can realistically afford. An installment agreement lets you pay your balance in fixed monthly amounts over time, and most taxpayers with balances under $50,000 can qualify through a streamlined process without extensive financial disclosure. An offer in compromise lets you settle your debt for less than the full amount, but the IRS approves these only when your income, expenses, and asset equity show you genuinely cannot pay the full balance. Penalty abatement removes penalties if you have a clean compliance history or a documented reasonable cause, such as a medical emergency or a natural disaster.

The IRS also offers Currently Not Collectible status, which pauses all collection activity when your monthly expenses equal or exceed your income.

State-level resolution options

State tax agencies operate separately from the IRS, and if you owe both federal and state taxes, you need to address them independently. Most states offer their own versions of installment agreements and hardship programs, but the eligibility rules and timelines differ significantly from federal programs. California's Franchise Tax Board, for example, has its own offer in compromise program with distinct criteria that do not mirror IRS standards.

Working with a professional who understands both federal and state programs ensures you do not accidentally miss a state collection deadline while focusing entirely on your IRS case. Handling both tracks at the same time protects you from collection action on either front.

How the tax resolution process works step by step

Understanding what is tax resolution at a conceptual level is useful, but knowing what actually happens during the process helps you prepare realistically. Most cases move through the same core phases, regardless of which IRS program ends up being the right fit.

Gathering your financial information

Before any negotiation starts, your representative needs a complete and accurate picture of your finances. This includes recent tax returns, pay stubs, bank statements, monthly expenses, and any correspondence you have already received from the IRS. That documentation is not a formality; it directly determines which programs you qualify for and what terms the IRS will consider acceptable.

The core documents you will typically need include:

- Last two to three years of filed tax returns

- Recent pay stubs or profit and loss statements

- Bank statements from the last three to six months

- IRS notices or letters you have received

- Monthly expense records, including rent, utilities, and insurance

Matching your situation to the right program

Once your representative reviews your financial documents, they compare your income, assets, and expenses against the eligibility criteria for each available IRS program. This analysis determines whether an installment agreement, an offer in compromise, or another option gives you the best outcome given your actual numbers.

Choosing the wrong program wastes time and fees, and a rejected application can trigger renewed collection activity from the IRS.

Your representative then prepares and submits the application on your behalf, responds to any IRS requests for additional information, and negotiates the final terms. Once the IRS accepts the resolution, you fulfill the agreed conditions, which typically means making payments on time and staying current on future tax filings. Falling out of compliance after reaching a resolution voids the agreement and returns you to active collections status.

Tax resolution costs and how to avoid scams

Understanding what is tax resolution also means knowing what it realistically costs. Fees vary based on the complexity of your case and which IRS programs your situation qualifies for. A simple installment agreement may cost a few hundred dollars in professional fees, while a full offer in compromise case, which requires detailed financial analysis and extended IRS negotiation, typically runs between $3,000 and $6,000 or more.

What you can expect to pay

Most reputable tax resolution professionals charge based on the scope of work involved, not as a percentage of your debt. Common fee structures include flat fees for specific services like penalty abatement requests or audit representation, and hourly rates for ongoing case management. Before you sign anything, ask for a written breakdown of what the fees cover and what additional charges might apply if your case becomes more complex.

A realistic estimate for common resolution services generally falls in this range:

- Installment agreement: $500 to $1,500

- Offer in compromise: $3,000 to $7,000

- Penalty abatement: $500 to $1,500

- Audit representation: $1,500 to $5,000+

Red flags that signal a scam

Several warning signs consistently separate legitimate tax professionals from companies looking to take your money. Any firm that guarantees a specific settlement amount before reviewing your financial documents is making a promise the IRS, not them, controls. Upfront fees in the thousands of dollars paid before any work begins, combined with high-pressure sales tactics urging you to act immediately, are among the clearest indicators that a company is not working in your interest.

The IRS does not endorse any private tax resolution company, and no firm can guarantee a specific outcome on your behalf.

Verifying credentials before hiring anyone protects you from these situations. Licensed CPAs and Enrolled Agents are federally authorized to represent you directly before the IRS and are held to professional and ethical standards that unlicensed tax relief companies simply are not.

Next steps if you need help

Now that you understand what is tax resolution and how the process works, the next step is figuring out where your specific situation fits. Every case is different, and the right program depends on your income, assets, and debt amount, as well as how far the IRS has already moved in its collection process. Waiting longer does not improve any of those conditions.

Taking action early gives you more options. If the IRS has already filed a lien or issued a garnishment, your choices narrow and the cost of resolution typically increases. A licensed professional reviews your full financial picture first, matches you to the right IRS program, and handles all negotiations on your behalf.

Schedule your free 30-minute consultation with a licensed CPA or Enrolled Agent at Tax Experts of OC today. You get clear answers about your options and honest guidance on what your case realistically qualifies for, with no pressure to commit before you are ready.