You spent decades saving for retirement. But without a solid retirement tax planning strategy, a surprising chunk of that money could end up going straight to the IRS. Social Security benefits, 401(k) withdrawals, pension income, each one carries tax consequences that catch retirees off guard every single year.

The difference between a comfortable retirement and a stressful one often comes down to how and when you pull money from your accounts. A well-timed Roth conversion, a smarter withdrawal sequence, or a simple adjustment to your Medicare-related income thresholds can save you thousands of dollars annually. These aren't loopholes, they're legitimate strategies that most retirees never implement because no one showed them how.

That's where working with a qualified professional makes a real difference. At Tax Experts of OC, our CPA and Enrolled Agent help clients across all 50 states build tax-efficient retirement plans tailored to their specific financial picture. This guide breaks down the core strategies you can use to reduce your retirement tax bill, protect your income, and keep more of what you've earned. Let's get into it.

What retirement tax planning covers

Retirement tax planning is the ongoing process of managing your income sources, account withdrawals, and tax brackets to minimize what you owe the IRS throughout retirement. It's not a one-time event you complete at age 65. Your tax situation in retirement is actually more complex than during your working years because you're juggling multiple income streams, each taxed differently, and small decisions can trigger surprisingly large, preventable tax bills.

The way you pull money from your accounts can matter more than how much you saved in the first place.

The three buckets of retirement money

Most retirees hold assets across three distinct account types, and each one gets taxed at a different time and at a different rate. Understanding these buckets is the foundation of any effective retirement tax strategy. Before you can reduce your tax bill, you need a clear picture of what you're working with.

Here's how each bucket works:

| Account Type | When You Pay Tax | Common Examples |

|---|---|---|

| Tax-deferred | At withdrawal | Traditional 401(k), Traditional IRA, 403(b) |

| Tax-free | Never (if rules are followed) | Roth IRA, Roth 401(k) |

| Taxable | On dividends, interest, and realized gains | Brokerage accounts, savings accounts |

Your goal is to draw from each bucket in a deliberate order so you stay inside lower tax brackets, reduce your exposure to Medicare premium surcharges, and limit the portion of your Social Security benefits that becomes taxable income.

The specific rules that shape your retirement taxes

Several IRS rules and income thresholds directly control how much tax you pay once you stop working. Required Minimum Distributions, or RMDs, force you to withdraw from tax-deferred accounts starting at age 73. Miss one and the IRS charges a 25% excise tax on the amount you should have taken. Beyond RMDs, Social Security benefits can become up to 85% taxable when your combined income crosses specific thresholds. Medicare Part B and Part D premiums can also jump significantly once your income rises above the IRMAA brackets.

Your total taxable income in retirement is rarely just what you spend each month. It includes RMDs you didn't need, investment income from taxable brokerage accounts, pension payments, and part-time earnings, all stacking together before the IRS applies your standard deduction. Thorough retirement tax planning means looking at this full picture across every account you own, not just one at a time, so every withdrawal decision you make actively works in your favor rather than against it.

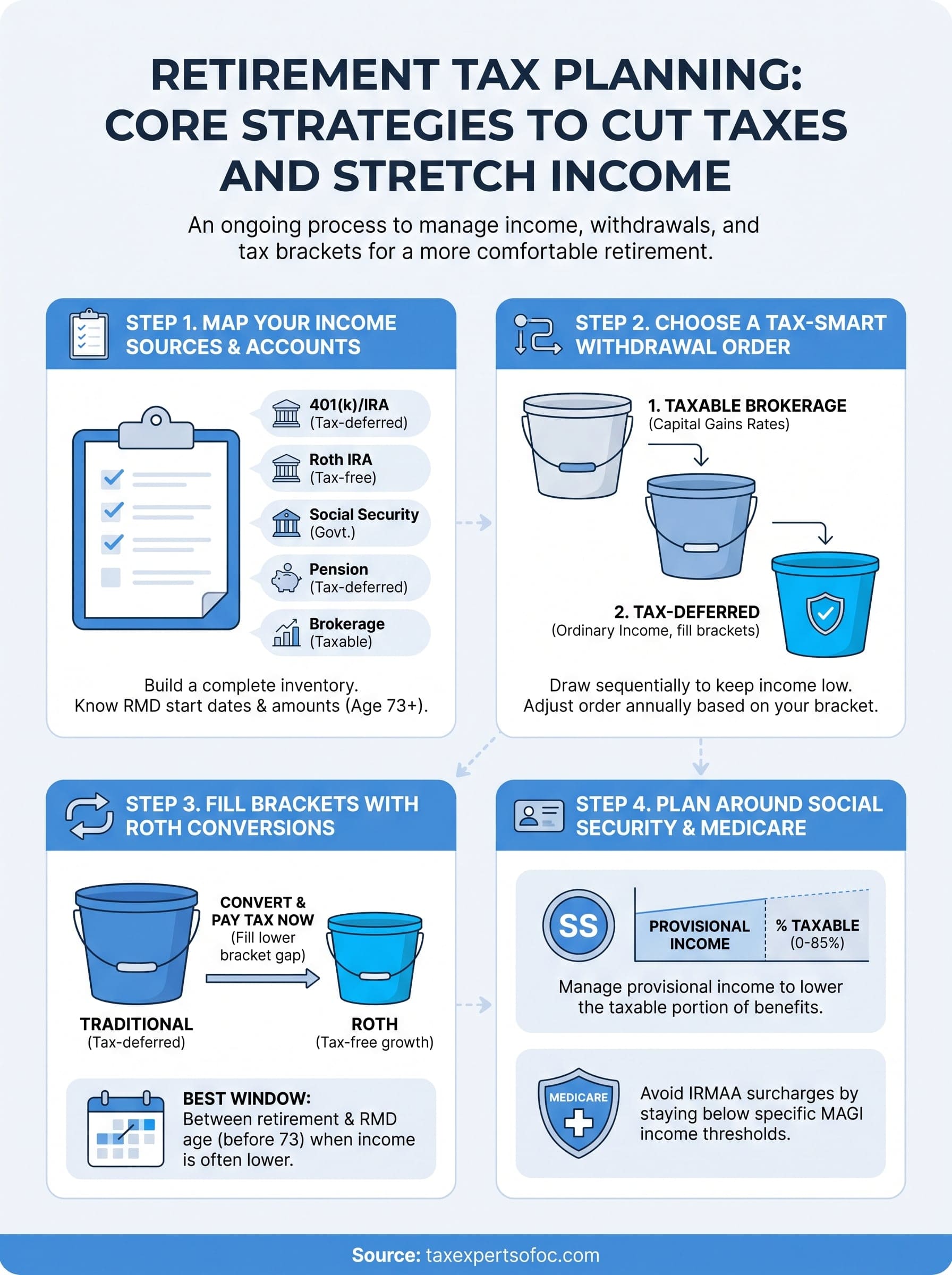

Step 1. Map your income sources and accounts

Before you can reduce any tax bill, you need a complete picture of where your retirement income comes from and how each source gets taxed. Most retirees underestimate how many income streams they're actually managing, and that gap is where unnecessary taxes quietly accumulate. Skipping this step means you're guessing at your tax bracket instead of controlling it.

Build your complete income inventory

Start by listing every source of income you expect in retirement. This doesn't have to be a perfect forecast, but it needs to cover every category. A clear inventory is the starting point for any honest retirement tax planning conversation, whether you're working with a professional or doing your own initial assessment.

Use this template to organize your income sources:

| Income Source | Account Type | Estimated Annual Amount | Taxable? |

|---|---|---|---|

| Traditional 401(k) / IRA withdrawals | Tax-deferred | $_______ | Yes, ordinary income |

| Roth IRA withdrawals | Tax-free | $_______ | No (if qualified) |

| Social Security benefits | Government | $_______ | Partially (0-85%) |

| Pension payments | Tax-deferred | $_______ | Yes, ordinary income |

| Brokerage account distributions | Taxable | $_______ | Yes, cap gains/dividends |

| Part-time or rental income | Earned/passive | $_______ | Yes |

| Required Minimum Distributions | Tax-deferred | $_______ | Yes, ordinary income |

The moment you see all your income sources side by side, the tax inefficiencies become obvious and fixable.

Verify your RMD start date and amounts

Once you have your inventory, flag every tax-deferred account because those accounts carry RMDs starting at age 73 under current IRS rules. The IRS publishes an official RMD worksheet you can use to estimate your required amounts based on your account balances and your age. Knowing your RMD amounts before the year begins lets you plan Roth conversions and other income-shifting moves around them so the distribution doesn't push you into a higher bracket by surprise.

Step 2. Choose a tax-smart withdrawal order

The order you pull money from your accounts directly determines your tax bracket each year. Most retirees default to whatever feels convenient, drawing from the same account repeatedly without a strategy. That approach tends to create large, taxable income spikes that push you into higher brackets, increase the taxable portion of your Social Security, and trigger IRMAA surcharges on Medicare premiums.

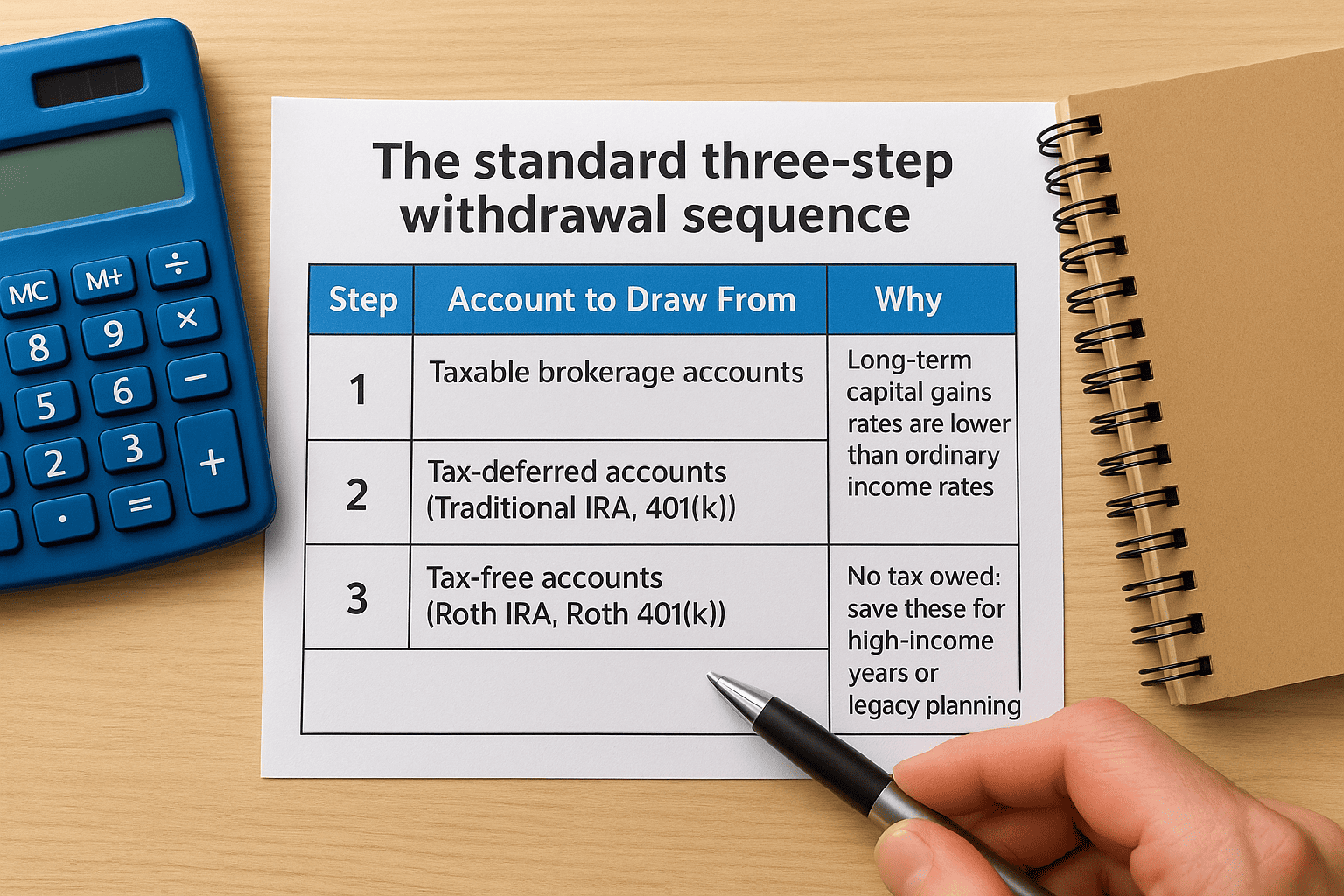

The standard three-step withdrawal sequence

Effective retirement tax planning relies on a withdrawal sequence that keeps your taxable income low in the early years of retirement, giving your tax-deferred accounts more time to grow and your Roth accounts time to compound tax-free. Here is the conventional starting framework:

| Step | Account to Draw From | Why |

|---|---|---|

| 1 | Taxable brokerage accounts | Long-term capital gains rates are lower than ordinary income rates |

| 2 | Tax-deferred accounts (Traditional IRA, 401(k)) | Ordinary income tax applies; draw strategically to fill lower brackets |

| 3 | Tax-free accounts (Roth IRA, Roth 401(k)) | No tax owed; save these for high-income years or legacy planning |

Start by spending down your taxable brokerage accounts first because qualified dividends and long-term capital gains are taxed at 0%, 15%, or 20% depending on your income, not at ordinary income rates. This keeps your taxable income lower while those rates remain favorable.

When to break the standard order

The standard sequence is a starting point, not a rigid rule. Some years, drawing more from your traditional IRA intentionally makes sense if doing so keeps you inside the 12% or 22% bracket before RMDs force larger withdrawals at 73. For example, if your RMDs are projected to push you into the 24% bracket in five years, pulling forward some traditional IRA income now at a lower rate saves real money later. Review your bracket position every year and adjust accordingly.

Step 3. Fill brackets with Roth conversions

Roth conversions are one of the most powerful tools in retirement tax planning, and most people wait too long to use them. The core idea is straightforward: you convert a portion of your traditional IRA or 401(k) balance into a Roth account, pay ordinary income tax on the converted amount now, and then let that money grow and be withdrawn tax-free later. Done strategically, this move reduces your future RMDs, lowers your taxable income in high-income years, and gives you a tax-free bucket to draw from when Social Security and Medicare costs are at their peak.

Bracket-filling means deliberately converting just enough to reach the top of your current tax bracket without crossing into the next one.

How to calculate your conversion amount

Your goal is to identify the gap between your current taxable income and the top of your target bracket, then convert exactly that amount. Here is a practical template for running the calculation:

| Item | Amount |

|---|---|

| Top of your target tax bracket (e.g., 22% bracket ceiling for MFJ) | $105,050 |

| Your estimated taxable income before any conversion | $62,000 |

| Available room for conversion | $43,050 |

In this example, you could convert up to $43,050 from a traditional IRA to a Roth and stay entirely inside the 22% bracket. You pay tax on that amount now at 22% rather than risk paying it later at 24% or higher once RMDs kick in and push your income up. Use the IRS tax brackets to confirm the current income thresholds before you calculate.

When Roth conversions make the most sense

The best window for Roth conversions is typically the years between retirement and age 73, when your income is lower and your RMDs have not yet begun. During this gap, your tax bracket may be unusually low, making conversions cheaper than they will ever be again.

Retirees with significant traditional IRA balances also benefit from conversions because shrinking the tax-deferred balance early reduces the size of future RMDs, which in turn keeps Social Security income less taxable and helps you stay below IRMAA thresholds for Medicare premiums. Even converting a modest amount each year compounds into meaningful tax savings over a decade.

Step 4. Plan around Social Security and Medicare

Two of the most overlooked factors in retirement tax planning are Social Security taxation and Medicare premium surcharges. Both are triggered by your income level, which means the withdrawal decisions you make in Steps 2 and 3 directly affect what you pay here. Managing your income to stay below specific thresholds is the most practical way to reduce these costs.

Control your provisional income to reduce Social Security taxes

The IRS determines how much of your Social Security benefit gets taxed based on your provisional income, which equals your adjusted gross income plus any nontaxable interest plus half of your annual Social Security benefit. Use this breakdown to see where you land:

| Filing Status | Provisional Income | % of SS Benefit Taxable |

|---|---|---|

| Single | Below $25,000 | 0% |

| Single | $25,000 to $34,000 | Up to 50% |

| Single | Above $34,000 | Up to 85% |

| Married Filing Jointly | Below $32,000 | 0% |

| Married Filing Jointly | $32,000 to $44,000 | Up to 50% |

| Married Filing Jointly | Above $44,000 | Up to 85% |

If your provisional income sits close to one of these thresholds, trimming a traditional IRA withdrawal by a few thousand dollars can drop the taxable portion of your Social Security benefit and produce measurable savings with minimal effort.

Avoid IRMAA surcharges on Medicare premiums

Medicare charges higher Part B and Part D premiums once your modified adjusted gross income (MAGI) exceeds $106,000 for a single filer or $212,000 for married filing jointly in 2026. These surcharges, known as IRMAA, stack on top of standard premiums and can add hundreds of dollars per month to your costs. Timing large Roth conversions or asset sales carefully so your MAGI stays below the first IRMAA bracket protects you from a premium increase that runs for the entire following calendar year.

A single year of income above an IRMAA threshold triggers the surcharge for the full year that follows, not just the months you were over.

Next steps

Retirement tax planning works best when you treat it as an annual process, not a single decision. Mapping your income sources, sequencing your withdrawals, running Roth conversions, and managing your provisional income are four moves that compound in value the earlier you start applying them. Even implementing one of these strategies this year can shift thousands of dollars from your tax bill back into your pocket.

Your next step is to pull together your account balances, estimate your income for the year, and identify which bracket you currently sit in. From there, you can calculate your Roth conversion room and check whether your provisional income puts any Social Security benefits at risk. If your situation involves multiple account types, significant RMDs, or IRMAA exposure, working through the numbers with a qualified professional pays for itself quickly. The team at Tax Experts of OC offers a free 30-minute consultation to help you build a strategy that fits your actual numbers.