Every dollar you keep from unnecessary taxes is a dollar working for your financial future. What is tax planning? It's the strategic process of organizing your finances to legally minimize your tax liability while staying fully compliant with IRS regulations.

Whether you're an individual facing a complex return or a business owner juggling multiple entities, understanding tax planning helps you make informed decisions throughout the year, not just at filing time. At Tax Experts of OC, our CPAs and Enrolled Agents work directly with clients across all 50 states to develop personalized tax strategies that protect income and support long-term financial goals.

This guide breaks down the fundamentals of tax planning, the strategies that matter most, and real-world examples of how proactive planning creates measurable results.

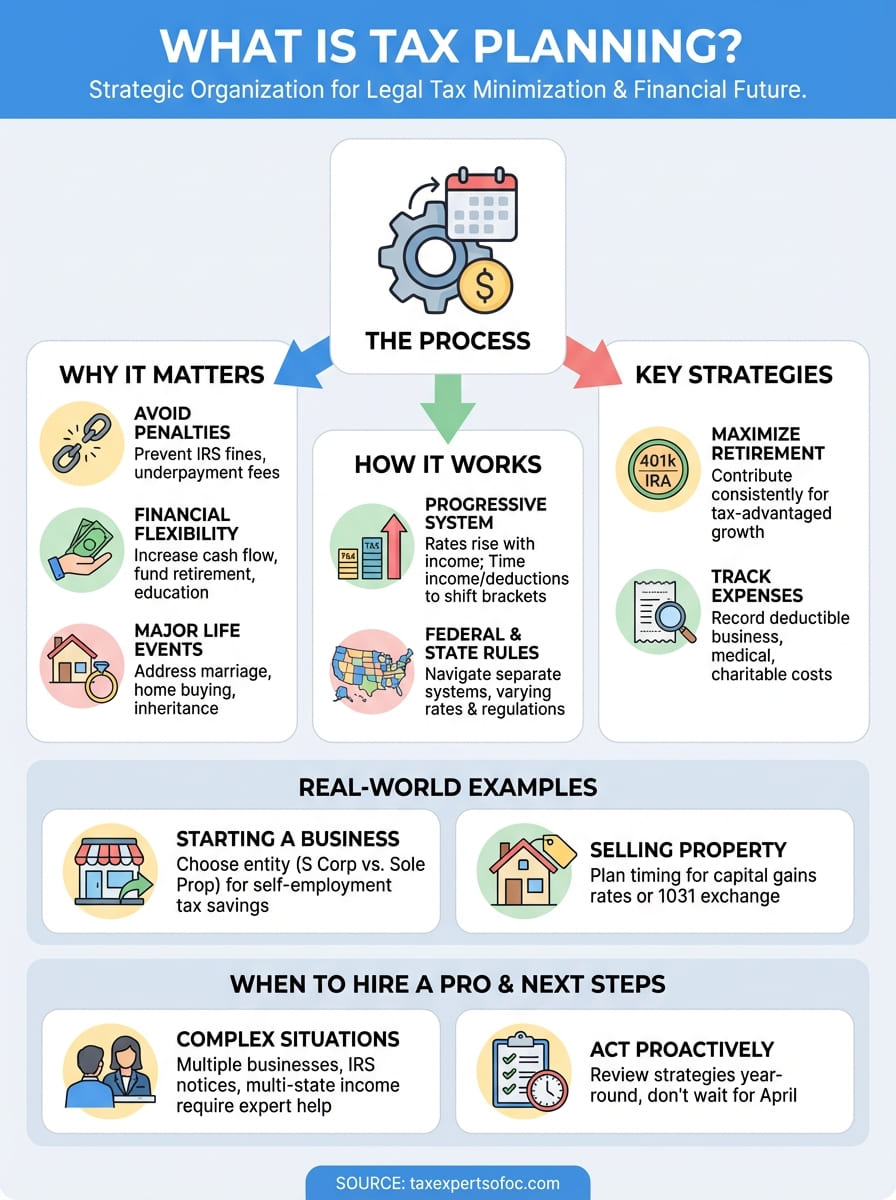

Why tax planning matters

Tax planning directly impacts your financial stability and long-term wealth accumulation in ways that reactive tax filing never can. When you wait until April to think about taxes, you lose the opportunity to structure income, time deductions, and leverage credits that could save you thousands of dollars. Planning ahead transforms taxes from a painful annual surprise into a manageable component of your overall financial strategy.

It protects your income from avoidable penalties

The IRS assesses over $1.5 billion in penalties annually for late filing, underpayment, and accuracy errors. Most taxpayers face these penalties not because they intentionally broke rules, but because they didn't anticipate their tax obligations throughout the year. When you engage in tax planning, you calculate estimated payments correctly, adjust withholding before shortfalls occur, and identify potential issues while you still have time to address them. Business owners who plan quarterly avoid the 0.5% monthly penalty on unpaid taxes that compounds quickly into significant amounts.

Planning prevents the costly cycle of penalties, interest, and IRS collections that derail both personal and business finances.

It creates financial flexibility over time

Strategic tax planning frees up cash flow you can redirect toward investments, retirement accounts, or business growth. You gain control over when you recognize income, how you structure deductions, and which tax-advantaged accounts receive your contributions. A self-employed professional who maximizes retirement contributions through a SEP IRA or Solo 401(k) can defer taxes on up to $69,000 annually while building retirement security. Families who plan for education expenses using 529 plans reduce their taxable estate and fund college costs with tax-free growth.

It positions you for major life events

Life changes like marriage, home purchases, business formation, and inheritance all carry significant tax implications that planning addresses before they become problems. Selling a home without understanding the capital gains exclusion can cost you $75,000 or more in unnecessary taxes. Starting a business without proper entity selection leaves you paying self-employment tax at 15.3% on income that could have been structured differently. Receiving an inheritance without planning for the tax treatment of retirement accounts accelerates your tax burden in ways that reduce the value of what you inherit. Understanding what is tax planning means recognizing these pivotal moments and structuring decisions to minimize tax impact while maximizing financial outcomes.

Each of these situations benefits from professional guidance that connects tax strategy to your specific circumstances, income level, and future goals.

How tax planning works in the US

Tax planning in the United States operates within a progressive tax system where your income determines your tax rate, and strategic timing of income and deductions can shift you between tax brackets. The IRS collects federal taxes through a combination of withholding, estimated payments, and annual reconciliation, while most states add their own income tax requirements on top. Understanding what is tax planning means recognizing that you have legal flexibility in how you structure transactions, when you recognize income, and which deductions you claim within the framework of current tax law.

The progressive tax system drives planning decisions

Your federal tax rate increases as your taxable income rises, creating clear incentives to reduce income in high-earning years or accelerate it in lower-earning years. For 2026, single filers pay 10% on income up to $11,600, then 12% on income between $11,600 and $47,150, and rates climb to 37% on income over $609,350. This structure means that every dollar you move from a 37% bracket to a 24% bracket through deductions or deferrals saves you 13 cents per dollar. Business owners who anticipate a high-income year can defer bonuses or accelerate expenses to stay in lower brackets, while retirees can strategically withdraw from retirement accounts to avoid pushing themselves into higher rates later.

Planning around brackets turns the progressive system from a burden into a tool you control.

Federal and state rules create layered obligations

You navigate two separate tax systems simultaneously because 41 states impose their own income taxes with different rates, brackets, and rules. California residents face a top state rate of 13.3%, while Texas residents pay zero state income tax but higher property taxes. This dual structure means that relocating, establishing residency, or structuring multi-state business operations carries significant tax consequences. Federal deductions don't always transfer to state returns, and some states require different treatment of retirement income, capital gains, or business expenses. Planning accounts for both systems to prevent surprises and optimize your total tax liability across all jurisdictions.

Tax planning strategies to use year-round

Year-round tax planning replaces April panic with consistent actions that compound into significant savings. You don't need to make complex moves monthly, but implementing a few core strategies throughout the year prevents missed opportunities and keeps you in control of your tax situation. Understanding what is tax planning means recognizing that small, regular adjustments create better outcomes than last-minute scrambling at year-end.

Maximize retirement contributions throughout the year

Contributing to retirement accounts consistently gives you more time for tax-advantaged growth while reducing your current taxable income. You can contribute up to $7,000 to an IRA (or $8,000 if you're 50 or older) and up to $23,500 to a 401(k) for 2026, but waiting until December limits your investment growth and creates cash flow strain. Setting up automatic monthly contributions ensures you capture the full deduction while spreading the financial impact across the year. Self-employed individuals benefit even more from SEP IRAs or Solo 401(k) plans that allow contributions based on net business income, but you need to calculate these amounts quarterly to avoid under-contributing.

Regular contributions turn tax savings into long-term wealth accumulation without year-end pressure.

Track deductible expenses as they occur

Recording business expenses, charitable donations, and medical costs as they happen prevents you from losing thousands in deductions you can't document later. Business owners who wait until tax time to gather receipts routinely miss 20 to 30% of legitimate deductions because records vanish or transactions become unclear. Using basic tracking systems throughout the year captures mileage, home office expenses, professional development costs, and client entertainment before you forget the details. Medical expense tracking matters particularly for years when costs exceed 7.5% of your adjusted gross income, allowing you to deduct the excess, but only if you have complete records of all payments, insurance reimbursements, and out-of-pocket costs.

Tax planning examples for common situations

Real scenarios demonstrate how understanding what is tax planning translates into measurable tax savings and better financial outcomes. Each situation requires specific strategies that address timing, entity structure, and deduction optimization within your unique circumstances.

Starting a business or side income

You face immediate decisions about entity structure that permanently affect your tax treatment when launching a business. Operating as a sole proprietor means paying 15.3% self-employment tax on all net income, while forming an S corporation allows you to split income between salary and distributions, reducing self-employment tax on the distribution portion. A consultant earning $100,000 annually saves approximately $7,650 in self-employment taxes by electing S corp status and taking a $60,000 reasonable salary with $40,000 in distributions. Planning also involves setting up a SEP IRA or Solo 401(k) before year-end to reduce taxable income by up to $69,000, but you need to calculate contribution limits based on your net earnings.

Entity selection in year one sets your tax structure for years to come, making early planning essential.

Selling a home or investment property

Capital gains from property sales trigger different tax rates depending on how long you owned the asset and how you used it. You exclude up to $250,000 in gains ($500,000 if married filing jointly) when selling your primary residence, provided you lived there for two of the last five years, but rental properties don't qualify for this exclusion. Selling investment property held over one year qualifies for long-term capital gains rates of 0%, 15%, or 20% instead of ordinary income rates up to 37%. Planning the timing of a sale can defer gains into a lower-income year or allow for a 1031 exchange that postpones taxation entirely when you reinvest proceeds into similar property.

When to hire a tax pro for planning

You reach a point where professional tax guidance stops being optional and becomes financially necessary when your situation involves complexity that software can't handle or mistakes that cost more than professional fees. Most taxpayers benefit from expert help when facing significant life changes, running businesses, or dealing with IRS problems that require representation by a CPA or Enrolled Agent. Understanding what is tax planning includes recognizing when your circumstances demand professional expertise rather than self-service solutions.

Your situation has grown beyond basic returns

Complex income sources trigger the need for professional help because they create interdependent tax calculations that generic software mishandles. You should hire a tax professional when you operate multiple businesses, have rental properties, receive investment income from partnerships or trusts, or work across state lines. Self-employment income combined with retirement distributions and capital gains creates planning opportunities that require calculation of estimated taxes, optimal timing of income recognition, and coordination between federal and state obligations. Medical practices, real estate investors, and freelancers with six-figure incomes routinely leave $10,000 to $30,000 on the table annually by attempting to self-file without understanding available deductions and entity optimization strategies.

Professional guidance prevents expensive mistakes that compound over years of incorrect filing.

You're facing IRS notices or multi-state obligations

Contact a tax professional immediately when you receive IRS correspondence about audits, unpaid taxes, or unfiled returns because these situations require representation by credentialed practitioners. CPAs and Enrolled Agents possess Power of Attorney authority to negotiate directly with the IRS on your behalf, structure payment plans, and resolve collections before they escalate to wage garnishments or bank levies. Multi-state tax obligations from working remotely, owning property in different states, or operating businesses across jurisdictions create overlapping filing requirements that professionals navigate to prevent double taxation and ensure compliance in all relevant jurisdictions.

You want proactive strategy, not just compliance

Hiring a tax professional for year-round planning rather than annual filing creates value that exceeds the cost when you have significant assets or complex financial goals. Strategic planning addresses retirement account optimization, business succession, estate planning coordination, and timing of major transactions like property sales or business exits. Professionals who work with you quarterly provide guidance before you make decisions, not after when options have disappeared.

Your next step

Understanding what is tax planning gives you the foundation, but applying it to your specific situation requires action before tax season arrives. You've seen how strategic planning reduces liability, prevents penalties, and creates financial flexibility that extends far beyond April 15.

Start by reviewing your current tax situation against the strategies outlined here. Calculate whether you're maximizing retirement contributions, tracking deductible expenses throughout the year, and structuring income to minimize your bracket exposure. If you're facing IRS notices, managing business income, or navigating multi-state obligations, professional guidance prevents costly mistakes that compound over years.

Tax Experts of OC provides direct access to CPAs and Enrolled Agents who develop personalized strategies for individuals and businesses nationwide. Schedule your free 30-minute consultation to discuss your specific circumstances and identify opportunities you're currently missing. Proactive planning starts with one conversation that transforms how you approach taxes for years to come.