Earning more means paying more, that's how the federal tax system works. But there's a significant difference between paying what you owe and paying more than you should. Tax planning for high income earners isn't about gaming the system; it's about using the strategies Congress built into the tax code to keep more of what you've earned. Without a deliberate plan, six- and seven-figure earners routinely lose tens of thousands of dollars each year to avoidable taxes.

The challenge is that most generic tax advice doesn't apply once your income crosses certain thresholds. Phase-outs kick in, deductions disappear, and surcharges like the 3.8% Net Investment Income Tax start eating into your returns. What works for a $75,000 household often backfires at $500,000. You need strategies built specifically for higher income brackets and complex financial situations.

At Tax Experts of OC, our CPAs and Enrolled Agents work with high-income individuals and business owners across all 50 states to build tax plans that actually move the needle. We've seen firsthand which strategies deliver real, measurable savings, and which ones are just noise. This article pulls from that experience to give you 12 actionable strategies you can start evaluating right now, whether you're a W-2 executive, a business owner, or both.

Let's get into what's actually working in 2026.

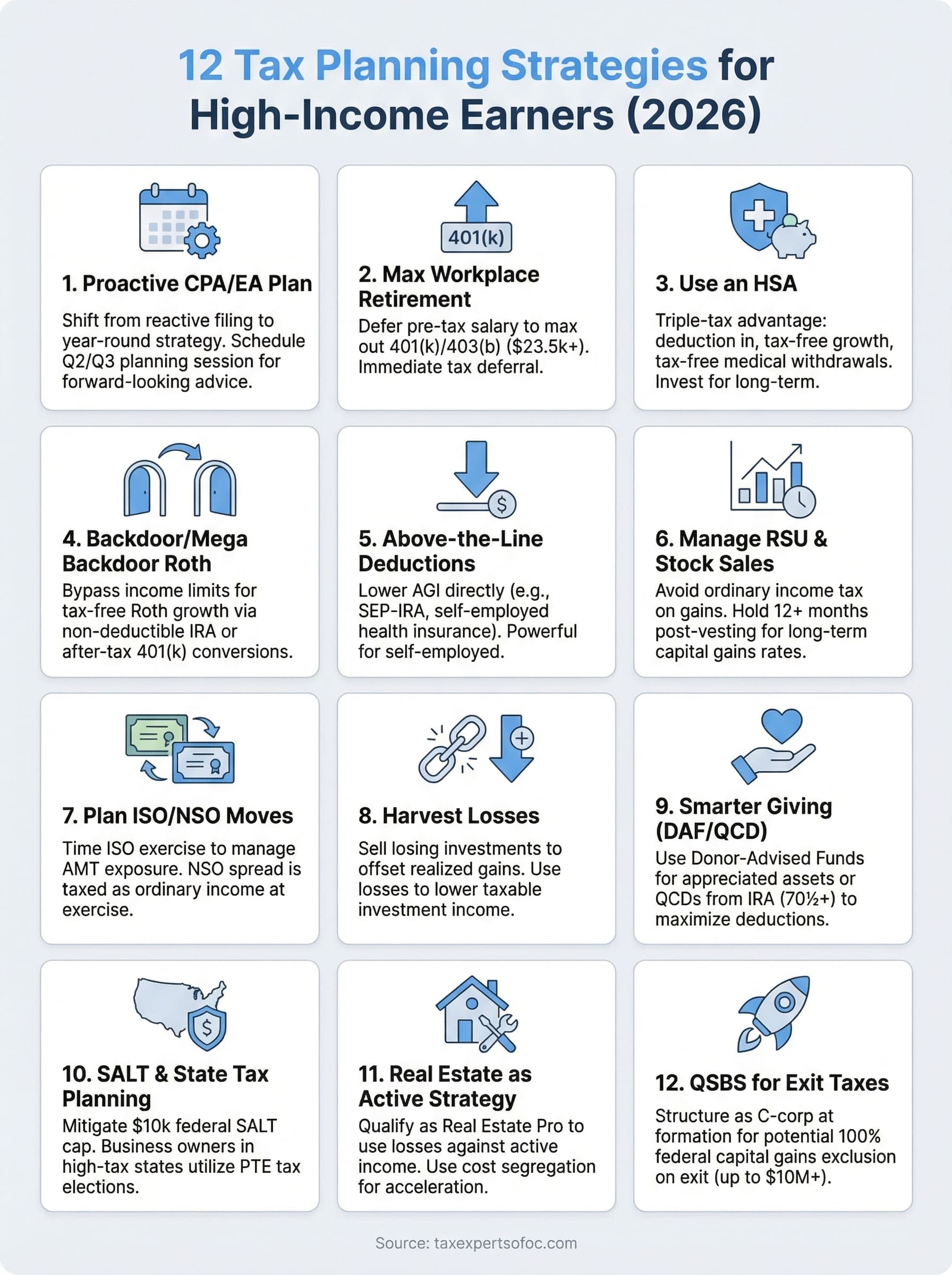

1. Get a proactive plan from a CPA or EA

Most people treat taxes as a once-a-year event: gather documents in March, file by April 15, and move on. That approach works fine when your income is straightforward. But high income earners face a layered tax picture that changes throughout the year, and reacting after December 31 leaves you almost no room to actually save anything. The single biggest leverage point available to you is shifting from reactive filing to deliberate, year-round tax planning.

What it is

A proactive tax plan is a written, forward-looking strategy built around your specific income sources, deductions, and financial goals, developed before the tax year ends rather than after. A Certified Public Accountant (CPA) or Enrolled Agent (EA) reviews your current and projected income, identifies every legal deduction and credit available to you, and creates a roadmap for decisions you need to make throughout the year. This is fundamentally different from tax preparation, which simply records what already happened.

Who it fits

This strategy fits anyone whose income, complexity, or exposure to multiple income streams makes reactive filing costly. If you earn over $200,000 as a single filer or $250,000 as a married couple filing jointly, you're already in the crosshairs of the Net Investment Income Tax (NIIT) and higher marginal rates. Business owners, executives with equity compensation, real estate investors, and anyone doing tax planning for high income earners across multiple states all benefit from having a licensed professional involved before decisions get made, not after.

How to implement it

Start by scheduling a comprehensive planning session with a CPA or EA, ideally in Q2 or Q3 so you have time to act on the recommendations before year-end. Come prepared with your most recent tax returns, a current-year income projection, and a list of major financial events planned for the year, such as a business sale, property purchase, or stock option exercise. Your advisor will map out your estimated tax liability, flag opportunities, and assign action items with clear deadlines.

The earlier in the year you engage a tax professional, the more moves you can actually make. By November, many of the most effective strategies are already off the table.

Key limits and pitfalls

Not all professionals deliver the same level of service. A general tax preparer who files returns but doesn't offer planning advice won't give you this kind of forward-looking guidance. Look specifically for a CPA or EA with direct experience in your income bracket and financial situation. Beyond that, a plan is only as good as your follow-through: if you don't implement the recommendations on time, you've paid for advice that produces no real savings.

Cost and effort

Expect to pay $500 to $5,000 or more per year for ongoing advisory services, depending on the complexity of your situation. That number looks different when you weigh it against the savings a well-executed plan typically generates. Your side of the work is moderate: gather documents, respond to information requests promptly, and make decisions when your advisor flags a deadline. For most high-income clients, the financial return on this investment runs well into the tens of thousands of dollars per year.

2. Max out workplace retirement plans

Contributing the maximum allowed to your employer-sponsored retirement accounts is one of the most efficient tax moves you can make each year. Every dollar you defer into a traditional 401(k) or 403(b) reduces your taxable income dollar-for-dollar, delivering immediate tax savings before you ever touch the money.

What it is

A workplace retirement plan lets you defer pre-tax salary into a tax-advantaged account. For 2026, the IRS sets the employee contribution limit at $23,500, plus a $7,500 catch-up contribution if you're 50 or older. Some plans also allow after-tax contributions, which opens the door to the mega backdoor Roth strategy covered later in this list.

Who it fits

This applies to W-2 employees at companies with a qualifying plan, including executives, physicians, attorneys, and tech workers in upper income brackets. If you're in the 32%, 35%, or 37% federal bracket, every deferred dollar saves you that percentage in immediate federal taxes. The tax deferral alone justifies maxing out your plan even when your employer offers no match.

How to implement it

Log into your HR or benefits portal and confirm your current contribution rate and annual projection. Adjust your elections to reach the IRS maximum before December 31. If your plan offers a Roth 401(k) option, consult your CPA to determine whether pre-tax or Roth contributions better fit your projected income trajectory.

If your plan permits after-tax contributions beyond the employee limit, rolling those into a Roth account is a move that tax planning for high income earners consistently underutilizes.

Key limits and pitfalls

Exceeding the annual IRS limit creates a taxable excess contribution that carries penalties. Watch your year-to-date total carefully if you change jobs mid-year, because both employers report contributions independently. Common pitfalls include:

- Changing employers mid-year without tracking combined contributions across both plans

- Missing open enrollment windows that lock you into a lower contribution rate for the full year

Cost and effort

No advisory fees apply beyond what your existing benefits administrator charges. The action is a single HR portal update that takes roughly 15 minutes and can save you thousands in taxes for the year.

3. Use an HSA to cut taxes and build wealth

A Health Savings Account (HSA) is the only account in the tax code that delivers three separate tax advantages at once: a deduction going in, tax-free growth inside the account, and tax-free withdrawals for qualified expenses. For high-income earners, this combination makes the HSA one of the most efficient savings vehicles available.

What it is

An HSA is a personal savings account tied to a High Deductible Health Plan (HDHP). Contributions reduce your taxable income in the year you make them, the money grows without being taxed, and qualified medical withdrawals are completely tax-free. Unlike a Flexible Spending Account, an HSA has no use-it-or-lose-it rule, so your balance rolls over every year and can compound for decades.

Who it fits

This strategy works best for high-income earners in the 32% bracket or above who can afford to pay current medical expenses out of pocket and let the HSA balance accumulate. If you're enrolled in an HDHP through your employer or on your own, you qualify. Tax planning for high income earners often overlooks the HSA as an investment account, not just a medical expense fund.

An HSA invested in low-cost index funds and left untouched until retirement functions as a secondary IRA with better tax treatment than either a traditional or Roth account.

How to implement it

Confirm that your health plan qualifies as an HDHP, then open or fund your HSA to the 2026 IRS limit of $4,300 for individuals or $8,550 for families, plus a $1,000 catch-up if you're 55 or older. Move the funds into a diversified investment portfolio inside the HSA rather than leaving them in the default cash position.

Key limits and pitfalls

You cannot contribute to an HSA if you're enrolled in Medicare or covered under a non-HDHP plan. Non-qualified withdrawals before age 65 trigger income tax plus a 20% penalty, so keep records of every medical expense carefully.

Cost and effort

Most HSA providers charge minimal or no annual fees, and the contribution itself is the only recurring action required. The effort is low, and the long-term tax savings are substantial.

4. Use a backdoor Roth or mega backdoor Roth

Once your income crosses the Roth IRA phase-out threshold, you can no longer contribute directly to a Roth IRA. But a legal workaround exists, and it gives high earners access to tax-free retirement growth that most people assume is off the table for them.

What it is

The backdoor Roth involves making a non-deductible contribution to a traditional IRA and then immediately converting it to a Roth IRA. Because you contributed after-tax dollars, you owe no additional tax on the conversion, and all future growth inside the Roth is tax-free. The mega backdoor Roth takes this further by using after-tax 401(k) contributions, up to the total IRS limit of $70,000 in 2026, and rolling those into a Roth account, either inside your plan or through a rollover to a Roth IRA.

Who it fits

This strategy fits high-income W-2 earners whose modified adjusted gross income exceeds $165,000 as a single filer or $246,000 as a married couple filing jointly, the 2026 Roth IRA phase-out range. Tax planning for high income earners frequently identifies the backdoor Roth as one of the most impactful long-term moves available, particularly for anyone with a long investment horizon and a desire to reduce future required minimum distributions.

The mega backdoor Roth is only available if your employer's 401(k) plan permits after-tax contributions and in-service withdrawals or in-plan Roth conversions, so check your plan documents before counting on it.

How to implement it

Open a traditional IRA, make your non-deductible contribution, then convert it to a Roth IRA before the account earns significant interest. For the mega backdoor, confirm your plan allows after-tax contributions, then contribute beyond the standard employee limit and convert promptly.

Key limits and pitfalls

The pro-rata rule is the most common trap. If you hold pre-tax IRA balances anywhere, the IRS treats your conversion as partly taxable. Work with your CPA before executing to avoid an unexpected tax bill.

Cost and effort

Brokerage accounts typically charge no conversion fees. The primary effort is coordinating the timing with your tax advisor to sidestep the pro-rata rule cleanly.

5. Use above-the-line deductions to lower AGI

Your Adjusted Gross Income (AGI) is one of the most important numbers on your tax return. It determines your eligibility for other deductions, your exposure to the Net Investment Income Tax, and whether phase-outs start eliminating benefits you'd otherwise qualify for. Above-the-line deductions reduce your AGI directly, before you even get to itemizing, which makes them particularly powerful for high earners.

What it is

Above-the-line deductions are subtractions you take directly from gross income to arrive at your AGI. They include contributions to a SEP-IRA or SIMPLE IRA if you're self-employed, the self-employed health insurance deduction, alimony payments under pre-2019 divorce agreements, and the deductible portion of self-employment tax. Unlike itemized deductions, these reductions apply regardless of whether you take the standard deduction.

Who it fits

This strategy is most valuable for self-employed individuals, independent contractors, and small business owners whose income structure gives them access to multiple above-the-line deductions simultaneously. Tax planning for high income earners frequently focuses on these deductions because lowering AGI can unlock additional savings elsewhere, such as restoring eligibility for deductions that phase out at higher income levels.

Reducing your AGI by even $10,000 can have a compounding effect across your entire return, affecting your Medicare surtax exposure, itemized deduction limits, and eligibility for credits all at once.

How to implement it

Work with your CPA to identify every deduction you qualify for before year-end. If you're self-employed, confirm your SEP-IRA contribution limit, which can reach 25% of net self-employment income up to $70,000 in 2026, and fund it before the filing deadline including extensions.

Key limits and pitfalls

Contribution limits on retirement accounts change annually, so verify the current figures before contributing. The self-employed health insurance deduction cannot exceed your net profit from self-employment, which creates a ceiling some business owners hit in low-revenue years.

Cost and effort

Most of these deductions require minimal paperwork beyond accurate recordkeeping. The main effort is ensuring your CPA has complete income figures early enough to calculate the optimal contribution amounts before deadlines close.

6. Avoid overpaying on RSUs and stock sales

Restricted Stock Units are a common form of compensation for executives, tech employees, and business professionals, but they carry a tax trap that catches many people off guard. Without deliberate planning, you can easily pay ordinary income tax rates on gains that could have qualified for the lower long-term capital gains rate, simply because of timing.

What it is

When your RSUs vest, the IRS treats the fair market value on the vesting date as ordinary income, and your employer withholds taxes accordingly. If you hold those shares past the vesting date and they appreciate further, you can qualify for long-term capital gains treatment on that additional gain by holding at least 12 months from vesting. The difference between the 37% ordinary income rate and the 20% long-term capital gains rate represents real money at high income levels.

Who it fits

This strategy applies directly to W-2 employees who receive equity compensation, particularly those in the technology, finance, and healthcare sectors where RSU grants are standard. Tax planning for high income earners with significant equity positions often finds this to be one of the largest overlooked opportunities on the return.

If your employer withholds only the default 22% on RSU vesting but your marginal rate is 37%, you may owe a substantial balance at filing unless you adjust your withholding or make estimated tax payments.

How to implement it

Work with your CPA to track each vest lot separately, noting the date and price. Decide promptly after each vest whether to hold or sell, and coordinate sales with your overall capital gains picture for the year to avoid stacking gains into a higher rate bracket.

Key limits and pitfalls

Selling shares immediately at vest avoids price risk but forfeits potential long-term gains treatment. Holding shares concentrates risk in a single stock, which carries its own financial exposure beyond taxes.

Cost and effort

Your brokerage should provide cost basis reporting for each lot. The main effort is reviewing that data with your CPA before executing any sale.

7. Plan stock option moves to manage AMT and rates

Stock options come in two distinct forms, and the tax treatment couldn't be more different depending on which type you hold. Incentive Stock Options (ISOs) and Non-Qualified Stock Options (NSOs) follow separate rules, and the timing of when you exercise each type can either protect your income or trigger a significant and avoidable tax bill.

What it is

When you exercise an ISO, you don't immediately owe regular income tax. However, the spread between the exercise price and the fair market value at the time of exercise counts as a preference item for the Alternative Minimum Tax (AMT), which runs at a 26% or 28% rate on amounts exceeding the exemption threshold. NSOs work differently: the spread at exercise is taxed immediately as ordinary income at your marginal rate, with no AMT exposure. The long-term capital gains clock on either type only starts after exercise.

Who it fits

This strategy is most relevant for startup employees, executives, and early-stage company stakeholders who hold ISOs or NSOs as part of their compensation package. Tax planning for high income earners with equity in pre-IPO or recently public companies often surfaces the ISO-versus-AMT calculation as one of the most high-stakes decisions on the table.

Exercising ISOs early in the year gives you the rest of the year to monitor the stock price and potentially qualify for the ISO tax treatment without a large AMT surprise at filing.

How to implement it

Work with your CPA to model your AMT exposure before exercising any ISOs, using your projected income for the year. If your AMT liability would be manageable, exercising earlier in the year gives you more time to plan. For NSOs, coordinate the exercise date with lower-income years when your marginal rate is reduced by other deductions.

Key limits and pitfalls

Exercising ISOs in a year when your stock price is high can generate a substantial AMT bill even if you never sell the shares. If the stock subsequently drops in value, you can be left paying taxes on gains you never actually realized.

Cost and effort

Your CPA will need your option grant documents and the current 409A valuation of the company to model this accurately. The effort is moderate, but the savings from proper timing can easily reach five or six figures.

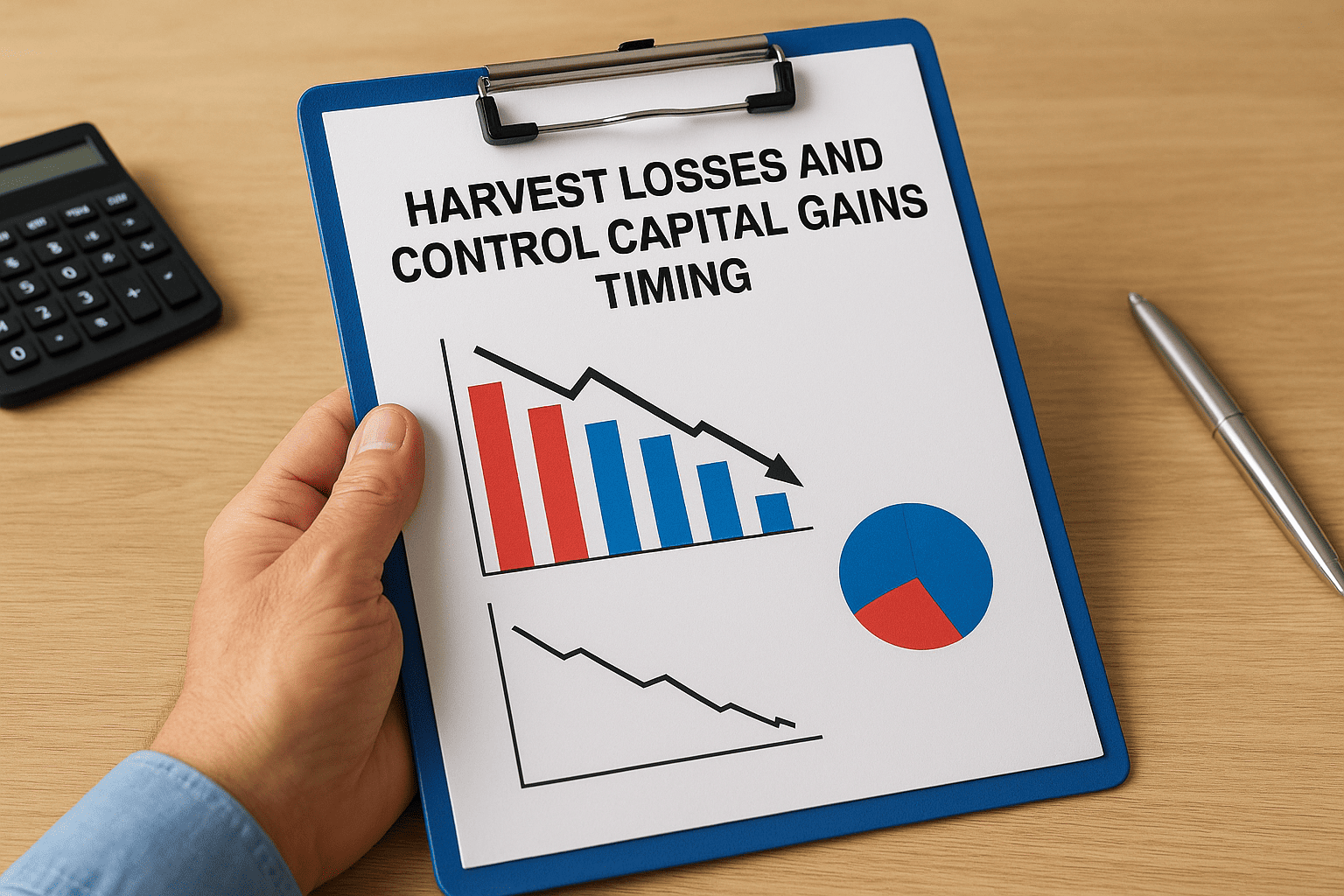

8. Harvest losses and control capital gains timing

Your investment portfolio generates gains and losses throughout the year, and the order in which you recognize them matters as much as the amounts themselves. Tax-loss harvesting lets you sell positions that have declined in value to offset gains you've already realized, reducing the total capital gains tax you owe by the end of the year.

What it is

Tax-loss harvesting is the practice of selling investments at a loss to offset realized capital gains, which directly lowers your taxable income from investment activity. If your losses exceed your gains, you can deduct up to $3,000 of the excess against ordinary income per year, with any remaining losses carried forward to future years.

Who it fits

This strategy applies to anyone holding a taxable brokerage account with unrealized losses alongside realized gains. Tax planning for high income earners benefits most here because the 20% long-term capital gains rate plus the 3.8% NIIT means every dollar of offset saves you nearly 24 cents.

Harvesting losses works best when you execute it continuously throughout the year rather than scrambling in December when your options may be limited.

How to implement it

Review your portfolio regularly and identify positions trading below your cost basis. Sell those positions to lock in the loss, then reinvest the proceeds in a similar but not identical asset to maintain your market exposure. Coordinate each sale with your CPA to confirm the loss fits into your overall capital gains picture for the year and doesn't trigger wash-sale issues.

Key limits and pitfalls

The wash-sale rule prohibits you from claiming a loss if you buy the same or substantially identical security within 30 days before or after the sale. Common pitfalls include:

- Repurchasing the same ETF or fund too quickly and invalidating the loss

- Failing to track adjusted cost basis on replacement shares, which shifts the disallowed loss forward rather than eliminating it

Cost and effort

Most brokerage platforms provide gain/loss reports at no additional cost. The effort is moderate: you'll need to review your positions periodically and coordinate timing decisions with your tax advisor before year-end.

9. Give to charity with smarter structures

Writing a check to your favorite nonprofit is generous, but it's not the most efficient way to give when you're in a high tax bracket. Structuring charitable contributions through the right vehicles lets you maximize the deduction you receive while also delivering more to the causes you care about.

What it is

Two structures stand out for high earners: the Donor-Advised Fund (DAF) and the Qualified Charitable Distribution (QCD). A DAF lets you contribute cash, stock, or other appreciated assets to a sponsored account, take an immediate deduction in the year of contribution, and then direct grants to charities over time. A QCD allows taxpayers aged 70½ or older to transfer up to $108,000 directly from an IRA to a qualified charity in 2026, counting toward your required minimum distribution without the amount hitting your taxable income.

Who it fits

This strategy works especially well for high-income earners who hold appreciated securities and want to give without triggering a capital gains tax event. Tax planning for high income earners frequently identifies the DAF as an underutilized tool, particularly in years when your income spikes from a bonus, business sale, or large stock vesting event. The QCD fits anyone past age 70½ who faces a growing RMD obligation and wants to satisfy it charitably.

Donating appreciated stock directly to a DAF instead of selling it first lets you avoid capital gains tax entirely while still deducting the full fair market value on the date of contribution.

How to implement it

Open a DAF through a financial institution, contribute appreciated assets rather than cash when possible, and take the deduction in the current tax year. For QCDs, instruct your IRA custodian to transfer funds directly to the charity before December 31.

Key limits and pitfalls

DAF deductions for appreciated assets are capped at 30% of your AGI, with a five-year carryforward for any excess. QCDs cannot go into DAFs; they must flow directly to a qualifying public charity.

Cost and effort

Most DAF sponsors charge low annual administrative fees, typically under 0.60% of assets. Setup takes a few hours, and your CPA can help you time contributions for maximum impact.

10. Use SALT and state tax planning to your advantage

The $10,000 federal cap on state and local tax (SALT) deductions has been in place since 2018, and it hits high earners in high-tax states the hardest. If you live in California, New York, New Jersey, or Illinois, you're likely paying far more in state income tax than the federal deduction allows you to recover.

What it is

The SALT deduction cap limits your combined federal deduction for state income taxes, property taxes, and local taxes to $10,000 per year. For someone paying $40,000 in California state income tax alone, that cap leaves $30,000 or more completely non-deductible at the federal level, which is a significant hit at higher income brackets.

Who it fits

This strategy matters most for high-income earners in high-tax states who own pass-through businesses such as S corporations, partnerships, or LLCs. Tax planning for high income earners in these states frequently centers on the Pass-Through Entity (PTE) tax election, now available in most high-tax states, which lets your business pay state income tax at the entity level and bypass the individual SALT cap entirely.

The PTE election can effectively restore the full state tax deduction the $10,000 cap eliminated, making it one of the most impactful moves available to business owners in high-tax states.

How to implement it

Work with your CPA to determine whether your state offers a PTE tax election and whether your business structure qualifies. If it does, your entity pays state tax directly, and the deduction flows through your federal return as a business expense rather than an itemized deduction, sidestepping the SALT cap cleanly.

Key limits and pitfalls

Each state administers its PTE election differently, so watch for these common issues:

- Missing the election deadline, which forfeits the deduction for the entire year

- Underpaying estimated PTE taxes, which can trigger state penalties independent of any federal savings

Cost and effort

Your CPA handles the election filing, and the incremental advisory cost is typically small relative to the state tax deductions you recover. Your primary responsibility is confirming the deadline and approving the payment before it closes.

11. Turn real estate into an active tax strategy

Real estate offers some of the most powerful tax benefits in the code, but most investors only access the passive side of the equation. If you qualify as a Real Estate Professional under IRS rules, you can use rental losses to offset ordinary income directly, turning property ownership into an active tax reduction tool rather than a passive one.

What it is

The IRS normally treats rental activity as passive, which means losses can only offset other passive income. However, if you qualify as a Real Estate Professional, those losses become non-passive and can offset your W-2 income, business income, or any other taxable earnings. Even without that designation, cost segregation studies accelerate depreciation on commercial or residential rental properties by reclassifying components into shorter depreciation schedules, generating large deductions in the early years of ownership.

Who it fits

Real estate professional status fits high-income earners who spend more than 750 hours per year in real estate activities and meet the material participation tests. Tax planning for high income earners with significant rental portfolios often identifies this designation as the single most impactful shift available. Cost segregation works for anyone who owns rental or commercial property and wants to pull forward deductions rather than spread them over 27.5 or 39 years.

Combining real estate professional status with a cost segregation study in the same year you purchase a large property can generate deductions large enough to eliminate a significant portion of your taxable income.

How to implement it

Document your real estate hours meticulously throughout the year using a contemporaneous log, since the IRS scrutinizes these claims closely. For cost segregation, hire a qualified engineering firm to conduct the study and provide a report your CPA can attach to your return.

Key limits and pitfalls

The 750-hour threshold must be met annually, and hours from a W-2 job in an unrelated field do not count. At-risk and basis limitations can also restrict how much of a loss you can actually deduct in a given year.

Cost and effort

A cost segregation study typically runs $5,000 to $15,000 depending on property size, but the accelerated deductions it generates routinely exceed that cost many times over.

12. Use business structure and QSBS to cut exit taxes

If you own or plan to start a business, the legal structure you choose at formation carries tax consequences that compound significantly over time. Qualified Small Business Stock (QSBS) under Section 1202 of the tax code offers one of the most powerful exit tax exclusions available, allowing eligible shareholders to exclude up to 100% of federal capital gains on the sale of qualifying stock, subject to per-issuer limits.

What it is

QSBS lets shareholders of qualifying C corporations exclude up to $10 million in capital gains per issuer, or 10 times their adjusted basis in the stock, whichever is greater, when they sell their shares. The corporation must be a domestic C corp with gross assets under $50 million at the time the stock was issued, and you must hold the shares for more than five years to claim the exclusion.

Who it fits

This strategy fits founders, early employees, and angel investors who hold or plan to acquire equity in eligible early-stage businesses. Tax planning for high income earners with a business exit on the horizon makes QSBS one of the highest-value structural decisions available, particularly when the planning happens at or before the time of stock issuance.

If your exit generates $10 million or more in gains and your stock qualifies under Section 1202, the federal tax savings can exceed $2.38 million at the top capital gains rate plus NIIT.

How to implement it

Work with your attorney and CPA at company formation to confirm that the entity qualifies and that your stock certificates are properly documented. Retain records of your original purchase date, price, and any QSBS certification the company provides, since you will need this documentation to claim the exclusion at sale.

Key limits and pitfalls

Several industries do not qualify, including professional services, finance, hospitality, and health. Converting from an LLC or S corp to a C corp after the fact can reset your holding period entirely, which delays your eligibility clock by five full years.

Cost and effort

The legal and accounting work at formation typically runs $2,000 to $5,000. Structuring correctly from day one costs far less than trying to requalify after the fact.

Your next step

The 12 strategies above cover the core of what tax planning for high income earners looks like in practice. But knowing the strategies and executing them correctly are two different things. Missing a deadline, triggering a wash-sale rule, or ignoring the pro-rata calculation can turn a well-intentioned move into an expensive mistake.

Your income mix, business structure, and state of residence all determine which moves make sense for your return. Working with a qualified CPA or Enrolled Agent gives you a plan built around your actual numbers, not general guidance that may not apply to your situation.

If you're ready to stop overpaying and build a real plan, reach out to Tax Experts of OC for a free 30-minute consultation. Our team works with high-income individuals and business owners across all 50 states to create tax strategies that produce measurable, year-over-year savings.