Knowing how to calculate business taxable income directly affects how much you owe the IRS, and how much you keep. Whether you run an LLC, partnership, or corporation, understanding this calculation helps you plan smarter and avoid surprises at tax time.

The formula itself isn't complicated: start with gross revenue, subtract allowable business expenses, and you arrive at your taxable income. But knowing which expenses qualify as deductions and how to document them properly makes the difference between accurate filings and potential IRS scrutiny.

At Tax Experts of OC, we help business owners across all 50 states navigate these calculations every day. This guide breaks down each step of the process so you can determine your taxable income with confidence, and know when it's time to bring in a CPA or Enrolled Agent for more complex situations.

What business taxable income means in the US

Business taxable income represents the amount of profit your company reports to the IRS after subtracting allowable expenses from your total revenue. This figure determines your federal tax liability and forms the foundation for your annual tax return, whether you file Form 1120, 1120-S, or Schedule C.

The IRS defines taxable income differently than your total sales or gross receipts. You start with all revenue your business generates, then subtract cost of goods sold (COGS) if applicable, followed by ordinary business expenses like rent, salaries, and utilities. What remains is your taxable income, which the government applies your tax rate against.

Understanding this distinction prevents you from overpaying taxes or missing deductions that lower your bill.

The basic formula all businesses use

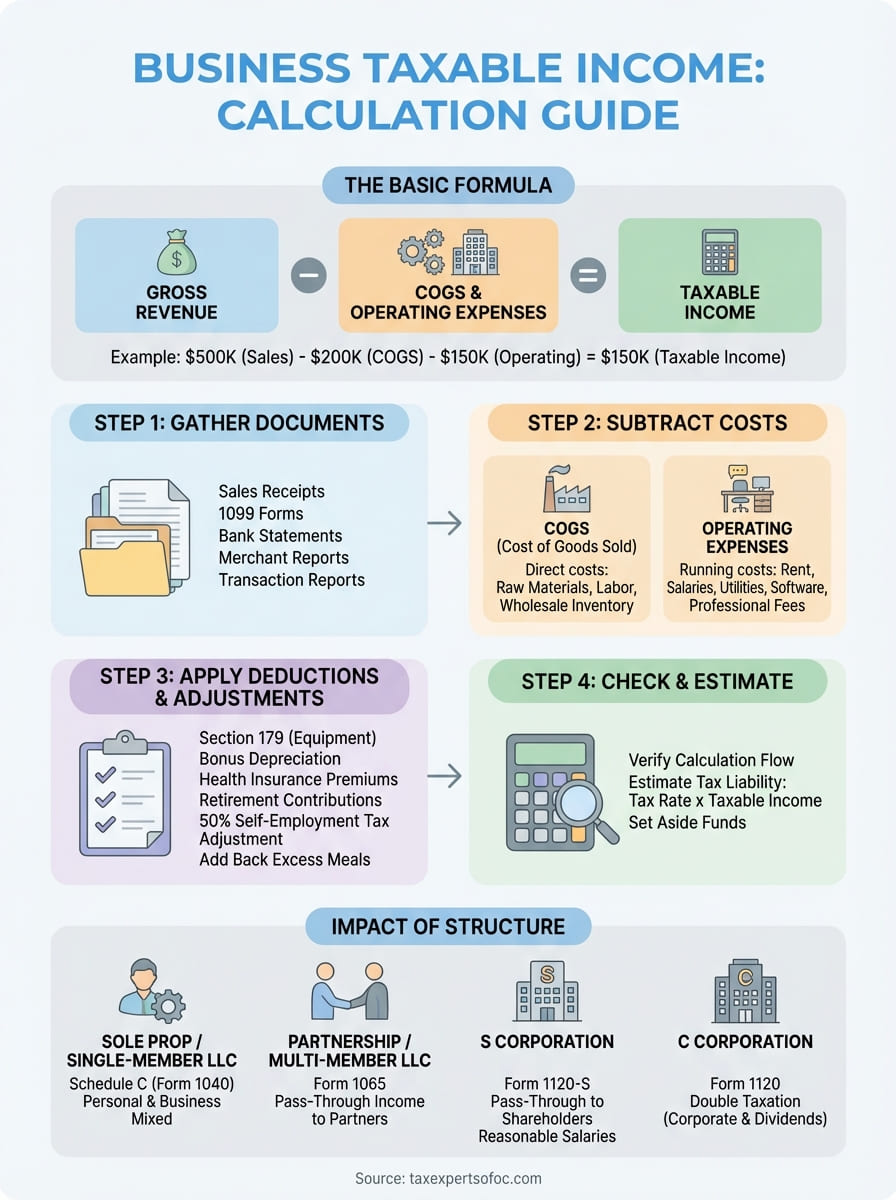

The calculation follows a straightforward pattern: Gross Revenue minus COGS minus Operating Expenses equals Taxable Income. If you run a retail business with $500,000 in sales, $200,000 in COGS, and $150,000 in operating costs, your taxable income equals $150,000.

This formula applies across industries, but the specific line items within each category change based on what you sell and how you operate. A consulting firm won't have COGS, while a manufacturing company tracks raw materials, labor, and factory overhead in that section.

How your business structure affects the calculation

Your entity type determines where you report this income and how the IRS taxes it. Sole proprietors and single-member LLCs report business income on Schedule C attached to Form 1040, mixing personal and business taxation together.

Partnerships and multi-member LLCs file Form 1065 but don't pay taxes at the entity level. Instead, the business passes income through to partners who report their share on individual returns. C corporations file Form 1120 and face double taxation, paying corporate tax first, then shareholders pay tax on dividends.

S corporations file Form 1120-S and pass income to shareholders, but they must pay owners reasonable salaries before distributing profits. This structure affects how to calculate business taxable income because salary expenses reduce taxable income, while pure profit distributions do not.

Step 1. Gather your income and source documents

You can't calculate accurate taxable income without complete financial records from the entire tax year. Start by collecting every document that shows money coming into your business, including sales receipts, 1099 forms, bank statements, and merchant processing reports. This step determines whether you're working with reliable numbers or making dangerous estimates.

Primary revenue documents you need

Your sales records form the foundation of your calculation. Collect all invoices you issued to customers, cash register tapes if you operate retail, and deposit records from your business bank account. If you received 1099-NEC or 1099-K forms from clients or payment processors, gather those as well since the IRS receives copies and will expect you to report matching amounts.

Missing even one revenue source can trigger an audit when IRS systems detect unreported income.

For online businesses, download transaction reports from platforms like Shopify, Stripe, or PayPal that show your gross sales before fees. Service businesses should compile client contracts and payment confirmations that prove when you earned the income, not just when cash arrived.

Supporting records that validate income

Beyond direct sales documents, you need bank statements showing all deposits to verify your revenue totals match actual cash flow. Keep copies of merchant statements that detail processing fees, since these fees reduce your gross receipts when you learn how to calculate business taxable income properly.

Document any refunds or returns you issued during the year, as these decrease your gross revenue before you start subtracting expenses. Store these records electronically with clear file names organized by month or quarter.

Step 2. Subtract COGS and operating expenses

Once you've totaled your gross revenue, you subtract cost of goods sold (COGS) and ordinary operating expenses to arrive at taxable income. This step separates businesses that produce or resell physical products from service-based companies, since COGS only applies when you manufacture, purchase inventory for resale, or transform raw materials into finished goods.

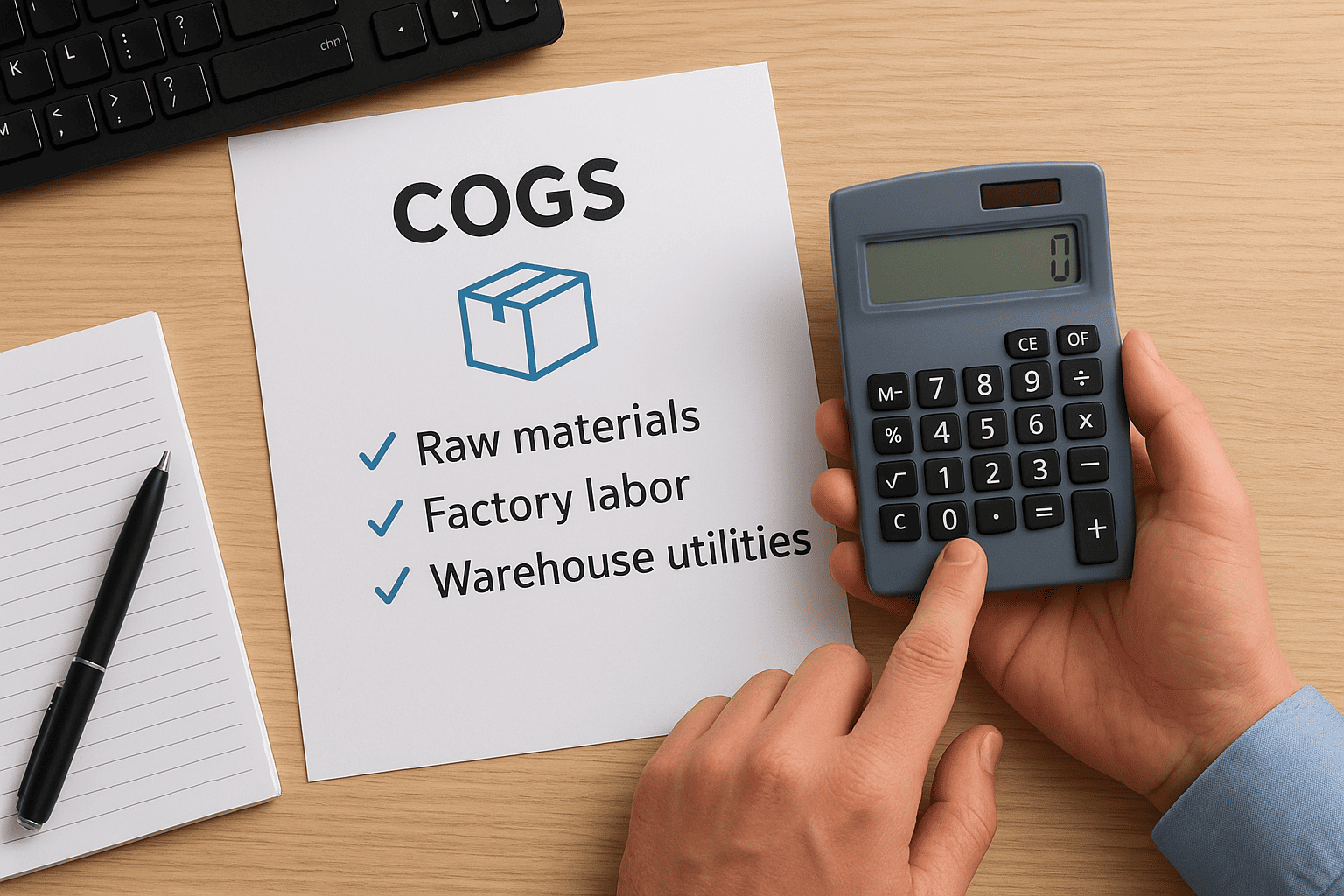

What qualifies as COGS for your business

COGS includes direct costs tied to creating the products you sold during the tax year. If you run a manufacturing operation, this covers raw materials, factory labor, and warehouse utilities. Retailers subtract the wholesale cost of inventory they purchased and sold, including freight charges to receive that merchandise.

Service businesses typically skip this section entirely when they learn how to calculate business taxable income, since you can't claim COGS for time-based services like consulting, legal work, or software development. Your labor becomes an operating expense instead.

Only count costs for products you actually sold, not items still sitting in inventory at year end.

Operating expenses that reduce taxable income

Operating expenses cover everything you spend to run the business outside of COGS. Subtract rent or mortgage interest on your commercial space, employee salaries and benefits, advertising costs, insurance premiums, and professional fees paid to accountants or lawyers.

Include utilities, office supplies, vehicle expenses for business use, software subscriptions, and equipment repairs. Document each expense with receipts and bank statements so you can prove the deduction if the IRS requests verification during an audit.

Step 3. Apply tax deductions and required adjustments

After subtracting COGS and operating expenses, you apply additional deductions and required adjustments that further reduce your taxable income. These items don't fit neatly into standard expense categories, but the IRS allows them as separate line items when you learn how to calculate business taxable income correctly.

Standard deductions every business can take

Claim the Section 179 deduction to write off equipment and machinery purchases in the year you buy them, rather than depreciating the cost over multiple years. For 2026, you can deduct up to $1,220,000 in qualifying property if your total equipment purchases stay below $3,050,000.

Apply bonus depreciation on eligible assets if Section 179 doesn't cover the full amount. You can also deduct health insurance premiums you pay for employees, plus contributions to retirement plans like SEP-IRAs or 401(k)s that reduce your current tax burden while building future savings.

Track these deductions separately from operating expenses to avoid double-counting costs.

Adjustments that modify your taxable income

Subtract 50% of self-employment tax if you operate as a sole proprietor or partnership, since this adjustment compensates for the employer portion of payroll taxes. Add back any meals and entertainment expenses that exceed the 50% limitation, as the IRS only allows you to deduct half of business meal costs.

Remove personal expenses that accidentally landed in business accounts, and add nondeductible items like federal income tax payments or personal penalties. These adjustments ensure your final taxable income figure matches IRS requirements exactly.

Step 4. Check your numbers and estimate what you owe

After applying all deductions and adjustments, you need to verify your calculation and estimate your tax bill before you file. This final review catches math errors, missing expenses, and helps you prepare for payment or request an extension if you can't cover the full amount immediately.

Run the calculation from start to finish

Take your gross revenue total and subtract COGS, then subtract all operating expenses, then apply your additional deductions and adjustments. Write down each step so you can trace the numbers back if something looks wrong when you learn how to calculate business taxable income accurately.

For example, if you started with $800,000 in revenue, subtracted $300,000 in COGS, $250,000 in operating expenses, and $50,000 in additional deductions, your taxable income equals $200,000. Compare this figure against your bank account balances and profit margins to confirm it makes sense for your industry and sales volume.

A taxable income that seems too high or too low signals missing transactions or classification errors.

Calculate your estimated tax liability

Multiply your taxable income by your applicable tax rate to estimate what you owe. C corporations pay a flat 21% federal rate, so $200,000 in taxable income generates a $42,000 tax bill before credits. Pass-through entities like S corporations and partnerships distribute income to owners who pay at individual tax rates ranging from 10% to 37%.

Add self-employment tax of 15.3% on the first $168,600 of net earnings if you operate as a sole proprietor or partnership. Set aside these funds in a separate account so you can pay when you file or make quarterly estimated payments throughout the year.

Wrap-up and what to do next

You now understand how to calculate business taxable income using the four-step process: gathering income documents, subtracting COGS and operating expenses, applying deductions and adjustments, then verifying your final number. This calculation gives you the foundation for accurate tax filings and helps you avoid overpaying or underpaying the IRS.

Complete this calculation well before your filing deadline so you have time to address any discrepancies or gather missing documentation. If your business involves multiple entities, complex inventory tracking, or significant capital investments, running these numbers yourself can lead to costly mistakes that trigger audits or penalties.

Tax Experts of OC provides direct access to CPAs and Enrolled Agents who calculate taxable income for businesses nationwide. We offer a 30-minute free consultation to review your specific situation, handle multi-state filings, and ensure you claim every deduction you qualify for without crossing into audit territory.