Most taxpayers know that tax credits vs tax deductions both lower what you owe the IRS, but few understand that one puts significantly more money back in your pocket than the other. That distinction can mean hundreds or even thousands of dollars on your return, and missing it is one of the most common (and costly) mistakes we see at Tax Experts of OC.

A tax credit directly reduces your tax bill, dollar for dollar. A deduction reduces the income the IRS uses to calculate that bill. Same goal, very different impact on your bottom line. Knowing which applies to your situation, and how to claim each one correctly, is essential for anyone trying to keep more of what they earn.

This article breaks down exactly how credits and deductions work, walks through real examples of each, and explains which one delivers a bigger financial benefit so you can approach your next filing with confidence.

Why credits and deductions matter

The difference between a tax credit and a tax deduction is not just a technical detail. It directly changes how much money stays in your account after you file. Many taxpayers assume that a larger deduction always means a bigger refund, but that assumption leads to real, preventable losses. Understanding how each tool works gives you a clear picture of your actual savings before you sign your return, and it puts you in a position to make smarter decisions throughout the year.

The real cost of your tax bracket

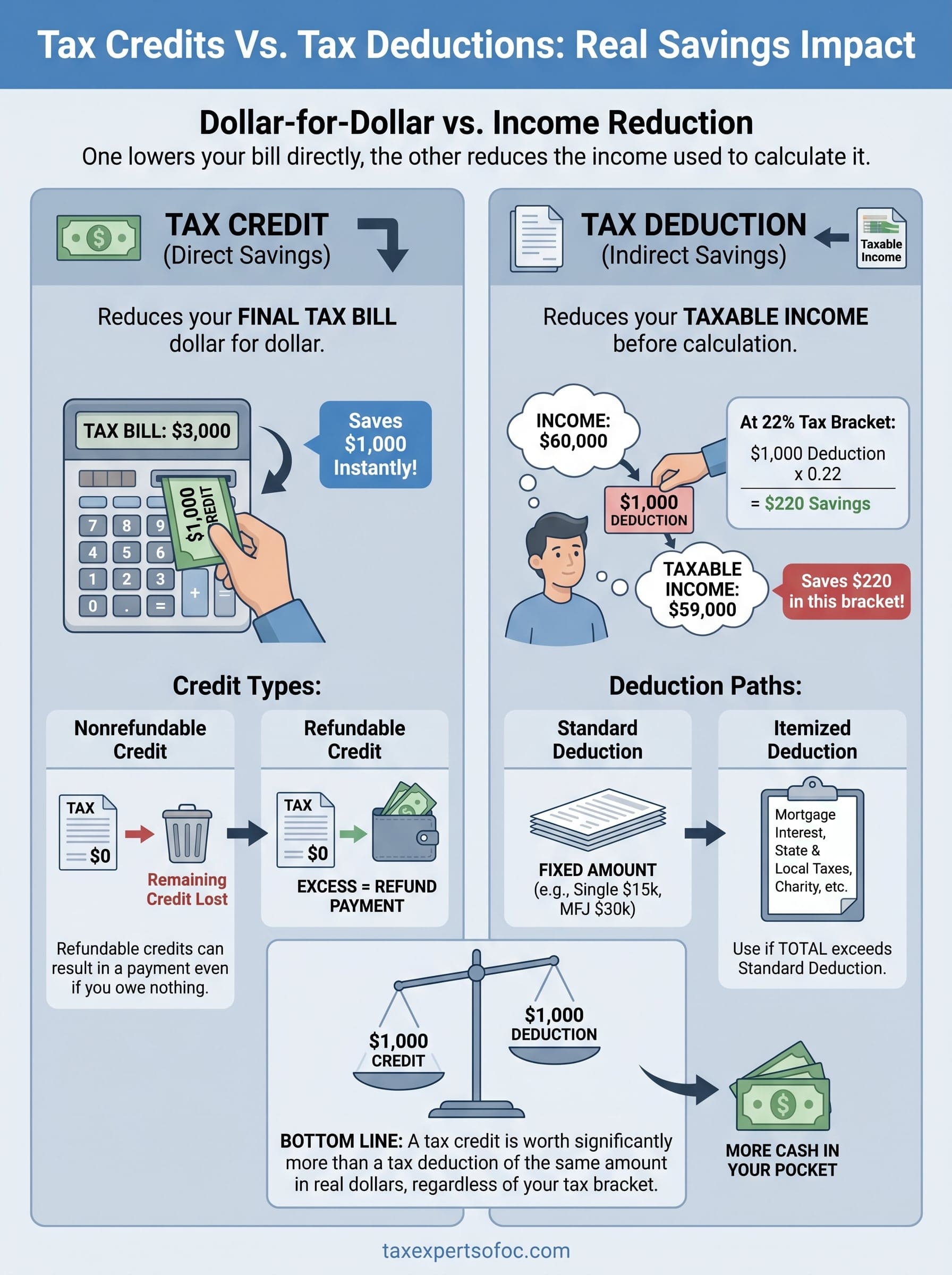

Your marginal tax bracket is what determines how much value a deduction actually delivers. If you're in the 22% bracket, a $1,000 deduction reduces your tax bill by $220. That same $1,000 as a tax credit reduces your bill by the full $1,000, regardless of your bracket or income level. The gap in real dollars is significant, and it compounds quickly when multiple credits or deductions are in play at the same time.

A $1,000 tax credit is worth more than a $1,000 deduction at every tax bracket, no exceptions.

Why timing and eligibility change everything

Comparing tax credits vs tax deductions also reveals that not every benefit applies to every taxpayer. Some credits phase out once your income crosses a certain threshold, and some deductions only apply if your qualifying expenses exceed a set floor. Knowing exactly what you qualify for before December 31 gives you time to make decisions that actually affect your return, not just document what already happened.

Eligibility rules also shift based on annual tax law changes, so reviewing your situation each year prevents missed savings and unexpected tax bills at filing time. Your income, filing status, and family situation all feed into which benefits you can legitimately claim.

How tax credits work and when you get a refund

A tax credit applies directly against your final tax liability, not your income. If the IRS calculates that you owe $3,000 and you qualify for a $2,000 credit, your bill drops to $1,000 on the spot. That one-to-one reduction is the core mechanic that makes credits so powerful in any comparison of tax credits vs tax deductions, and why they're often worth more than an equivalent deduction.

Nonrefundable vs. refundable credits

Nonrefundable credits can bring your tax bill down to zero, but they stop there. If the credit amount exceeds what you owe, you forfeit the remaining balance. Refundable credits work differently: when the credit exceeds your total liability, the IRS sends you the difference as an actual refund, even if you never paid that amount in withholding.

A refundable credit can result in a payment from the IRS even if you owe nothing at all.

Partially refundable credits, such as the Child Tax Credit, allow a portion of the unused amount to convert into a refund rather than disappearing entirely. Knowing which category applies to each credit you qualify for before you file tells you whether you're leaving money behind or earning a check back from the IRS.

How tax deductions work, standard vs itemized

A tax deduction reduces your taxable income before the IRS applies your rate to calculate what you owe. If you earn $60,000 and claim $10,000 in deductions, the IRS taxes you on $50,000 instead. The savings you see depend entirely on your tax bracket, which is exactly what separates deductions from credits in any honest comparison of tax credits vs tax deductions.

Standard deduction vs. itemizing

The IRS gives you two paths for claiming deductions. You can take the standard deduction, a flat amount set by your filing status, or you can itemize, listing individual qualifying expenses and claiming the combined total. For 2025, the standard deduction is $15,000 for single filers and $30,000 for married filing jointly.

Itemizing only makes financial sense when your total qualifying expenses exceed your standard deduction amount.

You benefit from itemizing when you carry significant mortgage interest, large state and local tax payments, or substantial charitable contributions that together exceed your standard amount. Most taxpayers find the standard deduction simpler and just as effective, but running both calculations before you file ensures you claim the larger number and keep more of your money.

Key differences that change your real savings

When you put tax credits vs tax deductions side by side, the most important distinction is where each one enters your tax calculation. A deduction reduces your income before the IRS runs the numbers, while a credit steps in after the calculation is done and cuts the final bill directly.

One reduces the starting number; the other cuts the final bill

Your tax bracket determines how much a deduction is actually worth to you. At the 22% bracket, a $1,000 deduction saves you $220. A $1,000 tax credit saves you exactly $1,000, full stop. That gap widens as deductions grow, which means a smaller credit can outperform a much larger deduction in real dollar terms.

At any tax bracket, a dollar-for-dollar credit will always deliver more savings than an equal deduction.

What happens when you owe less than the credit amount

Nonrefundable credits stop at zero. Once they erase your tax liability, any remaining credit value disappears. Refundable credits pay out the excess as a refund, putting actual cash back in your account. That distinction alone can shift your decision about which benefits to prioritize when you file.

Common credits and deductions to check each year

Knowing the distinction in tax credits vs tax deductions only helps if you apply it to items actually on your return. Several benefits come up year after year, and many taxpayers miss them simply because they didn't know to look. Running through this list with a qualified professional before you file prevents that loss.

Credits worth reviewing each year

The Child Tax Credit and the Earned Income Tax Credit are two of the most widely available credits, and both phase out at higher income levels, so your eligibility can shift from year to year. Other credits worth checking include:

- American Opportunity Credit: up to $2,500 for qualifying college tuition expenses

- Child and Dependent Care Credit: applies when you pay for childcare to work or look for work

- Saver's Credit: available if you contribute to a retirement account and meet income limits

Deductions worth reviewing each year

Mortgage interest and state and local taxes, capped at $10,000, are the deductions most likely to push you past the standard deduction threshold and make itemizing worthwhile. Student loan interest is deductible above the line, meaning you claim it whether or not you itemize.

Reviewing these items before December 31 gives you time to make contributions or payments that actually change what you owe.

Your next steps

Understanding tax credits vs tax deductions gives you a real advantage at filing time, but knowing the rules and applying them correctly to your specific situation are two different things. Credits and deductions each carry eligibility requirements, income limits, and phase-out thresholds that shift based on your income, family size, and filing status. Missing even one qualification detail can cost you hundreds of dollars or trigger an IRS notice down the road.

Before you file, take stock of every credit and deduction covered in this article and compare your situation against the current requirements. If your return involves multiple credits, itemized deductions, or business income, working with a qualified professional removes the guesswork and protects you from errors that compound over time. The team at Tax Experts of OC works directly with individuals and business owners to identify every benefit you qualify for and file your return accurately. Schedule your free 30-minute consultation to get started.