Most people overpay on taxes, not because they earn too much, but because they don't plan ahead. The difference between someone who owes $12,000 and someone who owes $7,000 often comes down to tax planning strategies for individuals applied consistently throughout the year. It's not about loopholes or aggressive schemes. It's about making informed moves at the right time with the money you're already earning and investing.

At Tax Experts of OC, our CPAs and Enrolled Agents work with clients across all 50 states to build tax plans that actually reduce what they owe, legally and strategically. We see firsthand how a few targeted adjustments to retirement contributions, investment timing, or charitable giving can save thousands of dollars each filing season. That hands-on experience with real client situations is exactly what shaped this list.

Below, you'll find nine specific strategies you can start using now to lower your tax bill, keep more of your income, and stop leaving money on the table every April.

1. Build a year-round plan with a CPA or EA

Most tax planning strategies for individuals fall apart because they only happen in March or April, when the filing deadline is already visible in the rearview mirror. A Certified Public Accountant (CPA) or Enrolled Agent (EA) works with you throughout the year to make proactive decisions, not reactive ones, which is where the real savings come from.

Why it works

Waiting until tax season to think about taxes is like trying to plant a garden after the frost. The decisions that affect your tax bill happen throughout the year: when you sell an investment, whether you contribute to a retirement account, how you structure a side income. A CPA or EA tracks those decisions in real time and helps you redirect money before it becomes taxable income.

The earlier in the year you engage a tax professional, the more options you have to act on.

How to do it

Start by scheduling a planning meeting in January or February, not just a filing appointment. You want to walk through your projected income and major life events (job change, marriage, home purchase), and any investments you plan to move. From there, your advisor sets up checkpoints, often quarterly, to make sure the plan stays current.

Bring documentation to those meetings: prior-year returns and pay stubs, along with any notices from the IRS or state tax agency. The more context your CPA or EA has, the more specific the guidance they can offer.

Watch-outs

Not every tax preparer offers year-round planning. Many firms are staffed up only during filing season, which means you may not get real strategic input outside of a narrow window. Make sure you confirm upfront whether your advisor is available for mid-year consultations and whether that service is included in your fee or billed separately.

Also watch out for advisors who focus only on last year's return rather than helping you plan for the current one. You want someone who is looking forward, not just filing paperwork.

2. Control the timing of income and deductions

When income lands on your return matters almost as much as how much you earn. Shifting a deduction or payment across December 31 by even a few weeks can change your bracket outcome in a meaningful way.

Timing decisions made before year-end consistently carry more impact than anything you do at filing time.

Why it works

Progressive taxation means higher marginal rates apply once you cross a bracket threshold. Pulling deductions into a high-income year saves money at your highest rate, while pushing income into a lower-income year keeps more of it taxed at a lower rate. These shifts are among the most practical tax planning strategies for individuals that tax professionals apply regularly.

Knowing your projected income for both this year and next is what makes timing precise. Without that forward-looking estimate, moves that seem smart can backfire.

How to do it

Self-employed individuals and small business owners can accelerate deductible expenses before December 31 or delay invoicing until January. Employees can ask their employer to defer a year-end bonus into the next calendar year if their current income already pushes against a higher bracket.

Check with your CPA whether your income next year will be higher or lower before deciding which direction to shift. The direction of the move matters as much as the timing itself.

Watch-outs

Deferring income only works if your tax rate stays flat or drops next year. A raise or large capital gain could push you into a higher bracket, wiping out the benefit entirely.

Also, passive income and investment distributions often carry limited timing flexibility. Always verify your approach with a tax professional before acting on any calendar-year strategy.

3. Fix withholding and estimated taxes now

Getting withholding wrong in either direction costs you money. Underwithholding triggers IRS penalties and a surprise bill in April, while overwithholding means you handed the government an interest-free loan for the entire year. Correcting this is one of the most actionable tax planning strategies for individuals to execute right now, with no waiting required.

Why it works

Your W-4 form directly controls how much your employer pulls from each paycheck. When you update it to reflect your current situation, your take-home pay aligns with what you actually owe, rather than a rough estimate you submitted years ago during onboarding. Self-employed individuals benefit equally by recalculating quarterly estimated payments whenever income shifts, keeping them current without overpaying or underpaying.

Accurate withholding keeps your money in your hands throughout the year, where it can actually work for you.

How to do it

Use the IRS Tax Withholding Estimator at irs.gov to calculate the right withholding amount. Then submit a revised W-4 to your payroll department promptly. Strong trigger points for recalculating include:

- A raise, job change, or new freelance contract

- Marriage, divorce, or a new dependent

- Selling a significant asset during the year

Watch-outs

Updating your W-4 once and leaving it alone is a frequent mistake. If your income fluctuates throughout the year, a single adjustment rarely stays accurate. Review your withholding again any time something material changes rather than waiting until April to discover an unexpected shortfall.

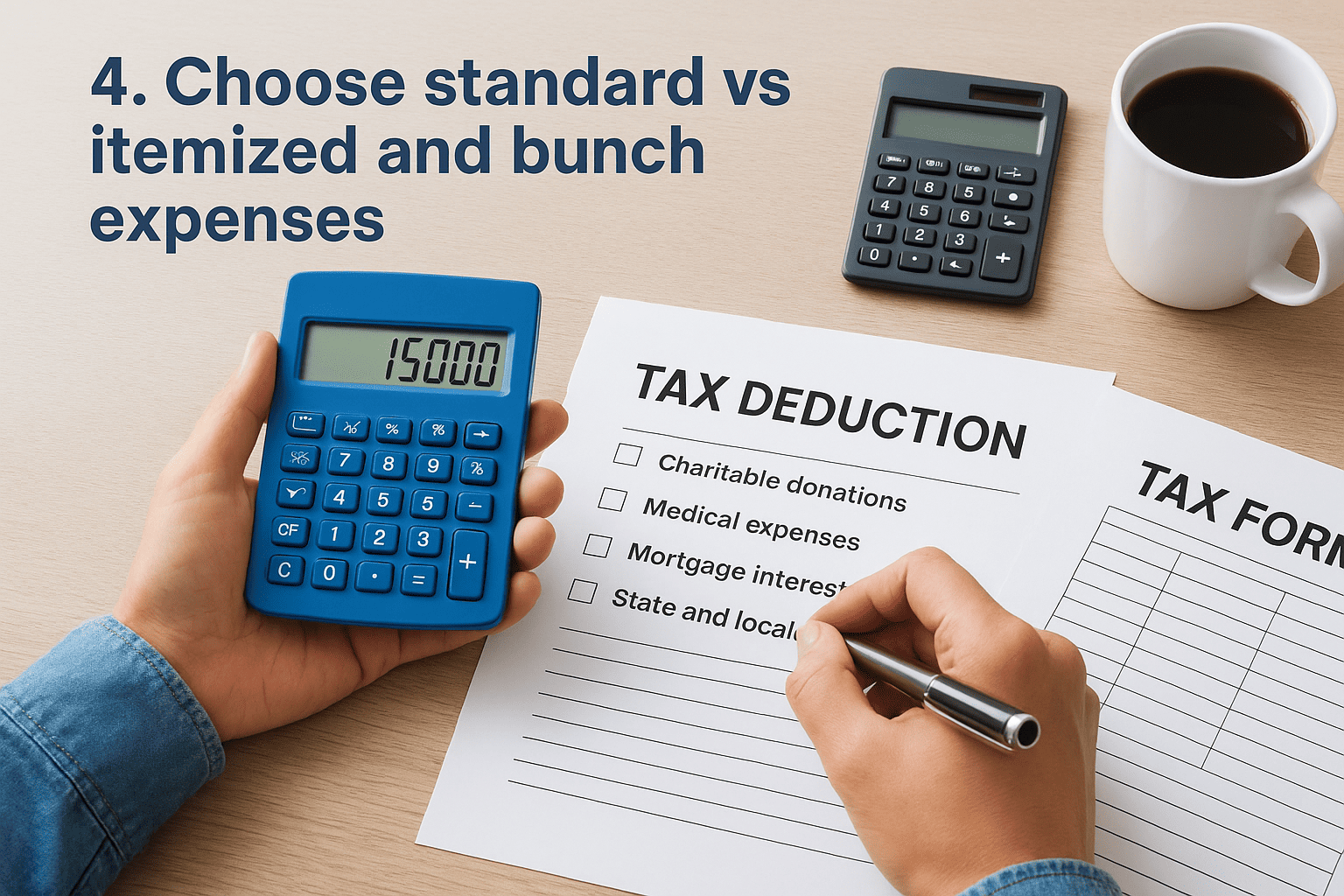

4. Choose standard vs itemized and bunch expenses

The standard deduction for 2025 sits at $15,000 for single filers and $30,000 for married couples filing jointly. If your qualifying expenses don't cross that threshold, itemizing wastes your time and gains you nothing. But with a deliberate approach, you can concentrate deductions strategically to beat that number in targeted years.

Why it works

One of the most underused tax planning strategies for individuals is deduction bunching. Instead of spreading deductible expenses like charitable donations or medical costs evenly across years, you pile them into a single tax year to push your itemized total above the standard deduction.

Alternating between itemized and standard deductions across two years often beats claiming the standard deduction both years.

How to do it

Review your projected expenses before December 31 each year to see how close you are to the threshold. If you're near it, consider accelerating these items before year-end:

- Planned charitable contributions (or use a donor-advised fund)

- Prepaid mortgage interest within IRS limits

- Qualifying medical expenses that already exceed 7.5% of your adjusted gross income

Watch-outs

The SALT deduction cap limits state and local tax deductions to $10,000 per household, which cuts the leverage many higher-income filers previously relied on. This single cap can make itemizing harder to justify even with legitimate expenses.

Also, medical costs only count above the 7.5% AGI floor, so run the actual numbers before factoring them into your bunching plan.

5. Max out retirement accounts to lower taxable income

Contributing to tax-advantaged retirement accounts is one of the most direct tax planning strategies for individuals to reduce what you owe in the current year. Every dollar you put into a traditional 401(k) or IRA comes directly off your gross income before the IRS calculates your liability, making this a reliable move with a predictable outcome.

Why it works

Pre-tax contributions directly reduce your adjusted gross income (AGI), which lowers your bracket exposure for the year. A smaller AGI also expands eligibility for credits and deductions that phase out at higher income levels, so the benefit compounds beyond just the contribution itself.

Maxing out retirement accounts is one of the few moves that builds long-term wealth and cuts your current-year tax bill at the same time.

How to do it

Push contributions to their annual maximums across every eligible account you hold. For 2025, the IRS has set the following limits:

- 401(k): $23,500, plus a $7,500 catch-up contribution if you're 50 or older

- Traditional IRA: $7,000, with an $8,000 catch-up option available

- SEP-IRA (self-employed): up to 25% of net self-employment income, capped at $70,000

Confirm exact figures with your CPA each year, since the IRS adjusts these numbers periodically for inflation.

Watch-outs

Traditional IRA deductibility phases out if you or your spouse have access to a workplace retirement plan and your income crosses specific thresholds. Contributing to a non-deductible IRA without knowing it produces no current-year tax reduction.

Always verify deductibility with your advisor before treating that contribution as a write-off against this year's income.

6. Use Roth conversions strategically

A Roth conversion moves money from a traditional IRA into a Roth IRA, paying tax on the converted amount now in exchange for tax-free growth and withdrawals later. Among tax planning strategies for individuals with flexible income, this one rewards forward-thinking timing more than almost any other move.

Why it works

Converting in a year when your taxable income runs lower locks in taxes at a reduced rate. Every dollar you convert and pay tax on today at 22% avoids being taxed at a higher rate during retirement, when required minimum distributions (RMDs) from traditional accounts can push your bracket up unexpectedly.

Converting during low-income years is one of the most durable ways to cut your lifetime tax bill.

How to do it

Work with your CPA to identify the right conversion window, then convert in controlled annual amounts to stay within your current bracket without spilling into the next one. Common timing opportunities include:

- A year with reduced employment income or a planned early retirement

- A gap year between jobs or business transitions

- Years before RMDs begin at age 73

Watch-outs

The converted amount adds directly to your ordinary income for the year, so an oversized conversion can push you into a higher bracket and reduce eligibility for income-sensitive credits. Always confirm the exact dollar amount with your advisor before you execute.

Medicare premium surcharges (IRMAA) are a separate risk worth checking. A large conversion can raise your income enough to trigger higher Part B and Part D premiums two years later.

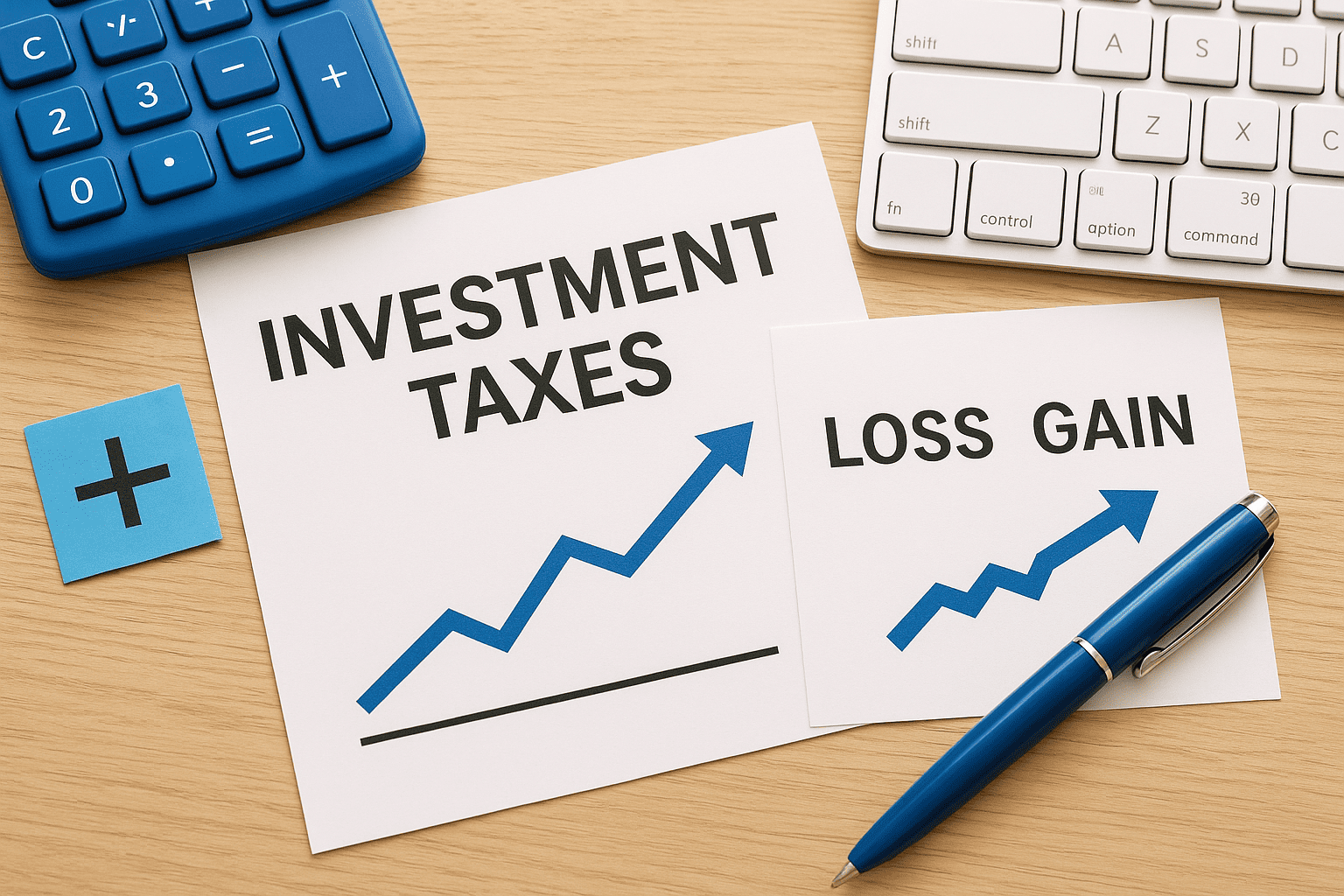

7. Cut investment taxes with gains and loss planning

How long you hold an investment before selling it determines which tax rate applies. Short-term capital gains on assets held under one year are taxed as ordinary income, while long-term capital gains on assets held over a year qualify for preferential rates of 0%, 15%, or 20% depending on your income. This gap creates real leverage within tax planning strategies for individuals who manage taxable brokerage accounts.

Why it works

Pairing gains with losses in the same tax year reduces your net taxable gain. Tax-loss harvesting involves selling underperforming positions to generate a realized loss that offsets gains elsewhere in your portfolio. If your losses exceed your gains, you can deduct up to $3,000 against ordinary income per year, with any remaining losses carried forward to future years.

Consistent loss harvesting across multiple years can compound into significant tax savings over time.

How to do it

Review your taxable brokerage accounts before year-end to identify positions sitting at a loss. Sell those positions to lock in the loss, then wait at least 31 days before repurchasing the same or a substantially identical security to avoid triggering the wash-sale rule.

Watch-outs

The wash-sale rule is the primary trap here. Buying the same security within 30 days before or after the sale disqualifies the loss entirely. Also confirm that harvested losses do not disrupt your target asset allocation in ways that hurt your broader long-term financial plan.

8. Give to charity in a tax-smart way

Charitable giving can do more than support causes you care about. With the right structure, it also cuts your tax bill in a meaningful way. Among tax planning strategies for individuals with consistent giving habits, coordinating donations with your overall deduction strategy is one of the most straightforward methods to generate a deduction that actually shows up on your return.

Why it works

When you donate to a qualified 501(c)(3) organization, the contribution counts as an itemized deduction. That deduction only saves you money if your total itemized expenses clear the standard deduction threshold, which is why pairing charitable giving with the bunching strategy from Section 4 amplifies the benefit in high-income years.

Donating appreciated securities directly to a charity instead of selling them first eliminates capital gains tax on the appreciation entirely, while you still claim a deduction at full market value rather than your original cost basis.

How to do it

Instead of writing small checks throughout the year, consolidate your giving into a single large contribution during a high-income year. A donor-advised fund (DAF) lets you claim the full deduction immediately while distributing grants to your chosen organizations over several years at your own pace.

A donor-advised fund separates the timing of your tax deduction from the timing of your actual charitable distributions.

Watch-outs

Non-cash donations like appreciated stock require a qualified appraisal for contributions above $5,000. Always confirm the receiving organization holds active 501(c)(3) status before filing, since contributions to ineligible entities produce no deduction.

9. Use HSAs, 529s, and flexible spending

Three account types sit outside most people's tax planning strategies for individuals, yet each delivers a deduction upfront, tax-free growth, and penalty-free withdrawals when used for qualifying expenses. Health Savings Accounts (HSAs), 529 education savings plans, and Flexible Spending Accounts (FSAs) work together to reduce taxable income across healthcare, education, and dependent care.

Why it works

Each of these accounts reduces your adjusted gross income before the IRS calculates what you owe. An HSA contribution lowers your taxable income, grows without tax, and withdraws tax-free for qualified medical costs. A 529 plan generates no federal deduction, but many states allow a deduction against state income tax, and growth stays untaxed as long as distributions cover qualifying education costs.

Used together, these accounts can cover major life expenses while keeping more money outside the reach of federal taxation.

How to do it

For 2025, check the IRS-set contribution limits and push every eligible account to the maximum:

- HSA: $4,300 for self-only coverage and $8,550 for family HDHP coverage

- FSA: up to $3,300 for healthcare FSAs

- 529: no federal annual limit, but check your state plan for deduction maximums

Fund your FSA early in the year since most employers let you access the full annual election from January 1 forward. Confirm whether your state offers a deduction on 529 contributions, since that benefit varies by state.

Watch-outs

FSAs carry a use-it-or-lose-it rule, meaning unspent balances typically expire at year-end unless your employer offers a grace period or limited rollover. Confirm your plan's exact terms before December to avoid forfeiting unused funds.

Next steps

The nine tax planning strategies for individuals covered here each deliver real savings, but they work best when applied together as part of a coordinated, year-round plan. Retirement contributions, Roth conversions, charitable bunching, and loss harvesting all interact with each other in ways that require someone to look at the complete picture, not just one move at a time.

Taking action before the next filing deadline is what separates the people who reduce their tax bills from those who just file and pay. Tax Experts of OC works with individuals and business owners across all 50 states to build proactive tax plans that cut what you owe legally and consistently. Whether you are dealing with IRS notices or simply want to stop overpaying each April, our CPAs and Enrolled Agents are ready to work through your specific situation.

Schedule your free 30-minute consultation and start putting these strategies to work for your finances today.