Most people use the terms tax planning vs tax preparation interchangeably, as if they mean the same thing. They don't. One looks backward at what already happened. The other looks forward to shape what happens next. Confusing the two can cost you thousands of dollars every year, not because you did anything wrong, but because you missed opportunities you didn't know existed.

Tax preparation is the process of filing your return after the year ends. It's necessary, it's compliance-driven, and it's reactive. Tax planning, on the other hand, is a proactive strategy, a set of decisions made throughout the year to reduce what you'll owe before the filing deadline arrives. Both matter, but they serve fundamentally different purposes.

At Tax Experts of OC, our CPAs and Enrolled Agents work with individuals and business owners across all 50 states on both sides of this equation. We file accurate returns, yes, but we also help clients build year-round strategies that minimize tax liability before a single form gets filled out. This article breaks down exactly how tax planning and tax preparation differ, when each one applies, and why you likely need both to keep more of what you earn.

What tax preparation is

Tax preparation is the process of gathering your financial records from the previous year and organizing them into a return that satisfies your legal filing obligations. A tax preparer, whether that's a CPA, an Enrolled Agent, or a tax software program, takes the information you provide and translates it into the appropriate IRS forms. The entire process is backward-looking by design: you're reporting on what already happened between January 1 and December 31 of the prior year, with no ability to revise those underlying facts once the calendar flips.

What actually happens during tax prep

When you sit down to file, you compile documents like W-2s, 1099s, mortgage interest statements, and records of any deductions you plan to claim. Your preparer verifies the accuracy of those numbers, applies the correct tax rules for your filing status and situation, and submits the return before the deadline. The primary goal is compliance, which means the return needs to be complete, accurate, and submitted on time to avoid penalties and interest.

For most individual taxpayers, April 15 is the main deadline. Businesses face different schedules depending on their entity type. S-corporations and partnerships file by March 15, while C-corporations share the same April 15 deadline as individuals. IRS.gov publishes the full calendar of filing deadlines and extension procedures so you can confirm exactly what applies to your situation before anything is late.

What tax prep cannot do for you

Here is where understanding tax planning vs tax preparation becomes genuinely important for your bottom line. Tax preparation works with the facts as they exist on the first day of the filing year. By that point, most of your financial decisions are already locked in. Your income is what it is, and your deductions are either present or they are not. A skilled preparer will find every credit and deduction you are legally entitled to claim, but they are working with a fixed set of variables they have no power to alter.

Tax preparation reports the outcome. It does not change it.

No adjustment to your withholding, no retirement contribution, and no income-shifting strategy can happen after December 31 for that tax year. Those windows close permanently. Filing an accurate return is absolutely necessary, but accuracy alone will not lower your bill by a single dollar that was not already reducible before the year ended. That reality is precisely why preparation on its own is rarely enough for anyone managing a growing income, a business, or a complex financial picture.

What tax planning is

Tax planning is the proactive process of making financial decisions throughout the year with the specific goal of reducing your tax liability before the year closes. Unlike preparation, which records what happened, planning shapes what happens. It puts you in control of variables like income timing, retirement contributions, deduction stacking, and entity structure, and that control translates directly into lower tax bills.

When tax planning happens

Planning is not a once-a-year event. The most effective strategies require decisions made in real time, often months before your filing deadline arrives. For example, if you know your income will push you into a higher bracket, you can accelerate deductible expenses or increase contributions to a tax-advantaged account like a 401(k) or HSA before December 31 to bring that number down.

The best time to reduce your tax bill is before the year ends, not after.

Your advisor monitors your numbers as the year progresses and adjusts the strategy based on changes in income, life events, or new tax law. That ongoing attention is what separates planning from a one-time transaction.

What tax planning actually covers

When you compare tax planning vs tax preparation, the scope of planning is significantly broader. A qualified CPA or Enrolled Agent looks at your full financial picture, including your business structure, investment activity, real estate holdings, retirement accounts, and projected income. From there, they build strategies tailored to your situation rather than applying a standard formula.

Some moves, like a Roth conversion or a business restructure, deliver benefits over several years rather than immediately. Your advisor looks ahead at how current decisions will affect your tax position in future filing years, which is something no standard preparation service is designed to do.

Key differences that affect your bottom line

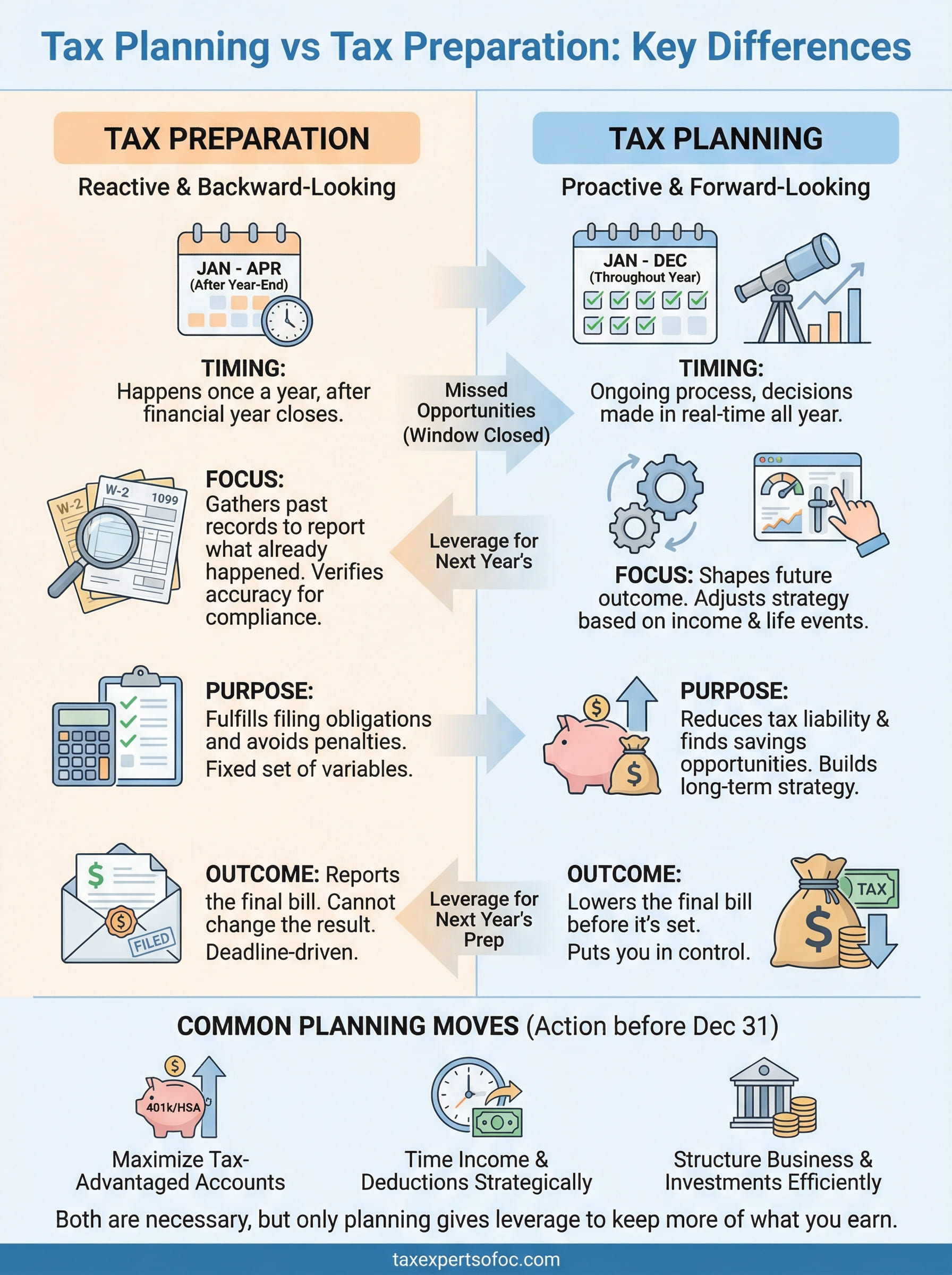

When you look at tax planning vs tax preparation side by side, the most important difference is not paperwork or complexity. It is timing. Preparation is a deadline-driven task you complete once a year. Planning is an ongoing discipline that runs parallel to every financial decision you make throughout the year. That timing gap is where money is either saved or permanently lost.

Timing, purpose, and scope

The two services operate on completely different tracks. Preparation confirms what you owe based on decisions that are already final. Planning reduces what you owe by shaping those decisions before they become permanent. The table below makes the contrast concrete:

| Tax Preparation | Tax Planning | |

|---|---|---|

| When it happens | After the year ends | Throughout the year |

| Primary goal | Compliance and accuracy | Reducing tax liability |

| Who drives it | Deadline requirements | Proactive strategy |

| Impact on your bill | Reports the outcome | Changes the outcome |

You cannot go back and restructure last year's income, but you can absolutely restructure this year's before it ends.

The financial stakes of waiting

Relying only on preparation means you arrive at the filing deadline with a fixed tax bill and no leverage to bring it down. Every deductible expense you did not make, every contribution you did not maximize, and every income-timing opportunity you passed on is gone for that year. These are not hypothetical losses for high earners only. Small business owners, freelancers, and salaried employees all pay more than necessary when planning never enters the conversation.

Your income typically grows over time, and so does the cost of skipping a forward-looking strategy. The gap between what you owe and what you could have owed widens each year that proactive decisions are absent from your financial routine.

Common tax planning moves to consider

Understanding tax planning vs tax preparation clarifies one thing immediately: the decisions that lower your tax bill need to happen before the year ends. The good news is that most of the moves available to you are straightforward and accessible, even if you are not running a large business. Knowing which levers exist is the first step toward using them.

Maximize tax-advantaged accounts

Contributions to retirement and health savings accounts reduce your taxable income dollar for dollar, which makes them one of the most direct planning tools available. If you have access to a 401(k) through your employer, pushing your contributions higher before December 31 lowers the income your return reports. Self-employed individuals can open a SEP-IRA or Solo 401(k) and contribute significantly more than a standard employee plan allows. A Health Savings Account, or HSA, works similarly if you carry a high-deductible health plan. Contributions are tax-deductible, the growth is tax-free, and qualified withdrawals face no tax at all.

Few moves deliver as consistent a return as maximizing contributions to accounts the IRS has already set aside for favorable treatment.

Time your income and deductions strategically

If you have control over when income arrives or when expenses are paid, you can shift both to your advantage. A freelancer expecting a high-income year might defer a client invoice into January so that income lands in a lower-earning year. On the deduction side, bunching charitable contributions or prepaying a state tax bill before year-end can push you over the standard deduction threshold in one year while you take the standard deduction in the next. These moves require some advance coordination, but they are legal, well-established, and consistently effective.

How to know what you need this year

Most people default to preparation because it has a hard deadline attached to it. Filing is required, so it gets done. Tax planning, by contrast, has no external forcing function, which means it often gets skipped until someone sees a larger-than-expected bill and starts asking questions. The right question is not which service costs less, but which one your situation actually requires right now.

Signs you need proactive planning

If your income changed significantly this year, you bought or sold a property, you started a business, or you received a large bonus or investment gain, a preparation-only approach will almost certainly leave money on the table. These are situations where income timing, entity structure, and retirement contributions have a direct and measurable impact on what you owe. The more complex your financial picture, the more the tax planning vs tax preparation distinction matters to your actual bottom line.

If any major financial event happened this year, planning is no longer optional.

You should also consider planning if you are self-employed, run payroll, or hold real estate. Each of these areas carries specific deductions and elections that require decisions made before year-end to be effective at all.

When preparation alone is enough

If your income is straightforward, you earn a single W-2, carry no business activity, and your financial situation stayed largely the same, standard preparation likely covers your current needs. A qualified preparer will confirm you claimed every deduction and credit you are entitled to and file an accurate return on time.

That said, even simple tax situations benefit from at least one planning conversation every few years. Life changes like marriage, a new child, or a home purchase can shift your tax position more than you expect, and catching those shifts early costs far less than correcting them later.

Final takeaways

Tax preparation and tax planning serve fundamentally different purposes, and treating them as the same service costs you real money every year. Preparation handles compliance and reports what already happened. Planning changes what happens by putting decisions in your hands before the year closes. Both are necessary, but only planning gives you leverage over the outcome before the year ends.

The core distinction in tax planning vs tax preparation comes down to timing. Every dollar you save through proactive strategy requires action before December 31, not after. Waiting until filing season starts means those savings windows are permanently closed for that year.

If your income grew, your situation changed, or you simply want to stop overpaying, speaking with a qualified CPA or Enrolled Agent is the right move. Schedule a free consultation with Tax Experts of OC to find out exactly where your tax strategy stands and what you can still do this year.