Every year, millions of Americans sit down to file their taxes and realize they're missing something, a W-2 that never arrived, a 1099 buried in an email inbox, or a deduction receipt they swore they saved. That scramble wastes time, causes errors, and often leaves money on the table. A solid tax preparation checklist for individuals eliminates the guesswork and keeps you organized from the start, whether you're filing through software or handing everything off to a qualified tax professional.

At Tax Experts of OC, our CPAs and Enrolled Agents prepare individual returns for clients across all 50 states. One pattern we see consistently: the taxpayers who show up with their documents organized file faster, claim more deductions, and deal with far fewer IRS headaches down the road. The ones who wing it? They're the ones calling us in July wondering why they got a notice.

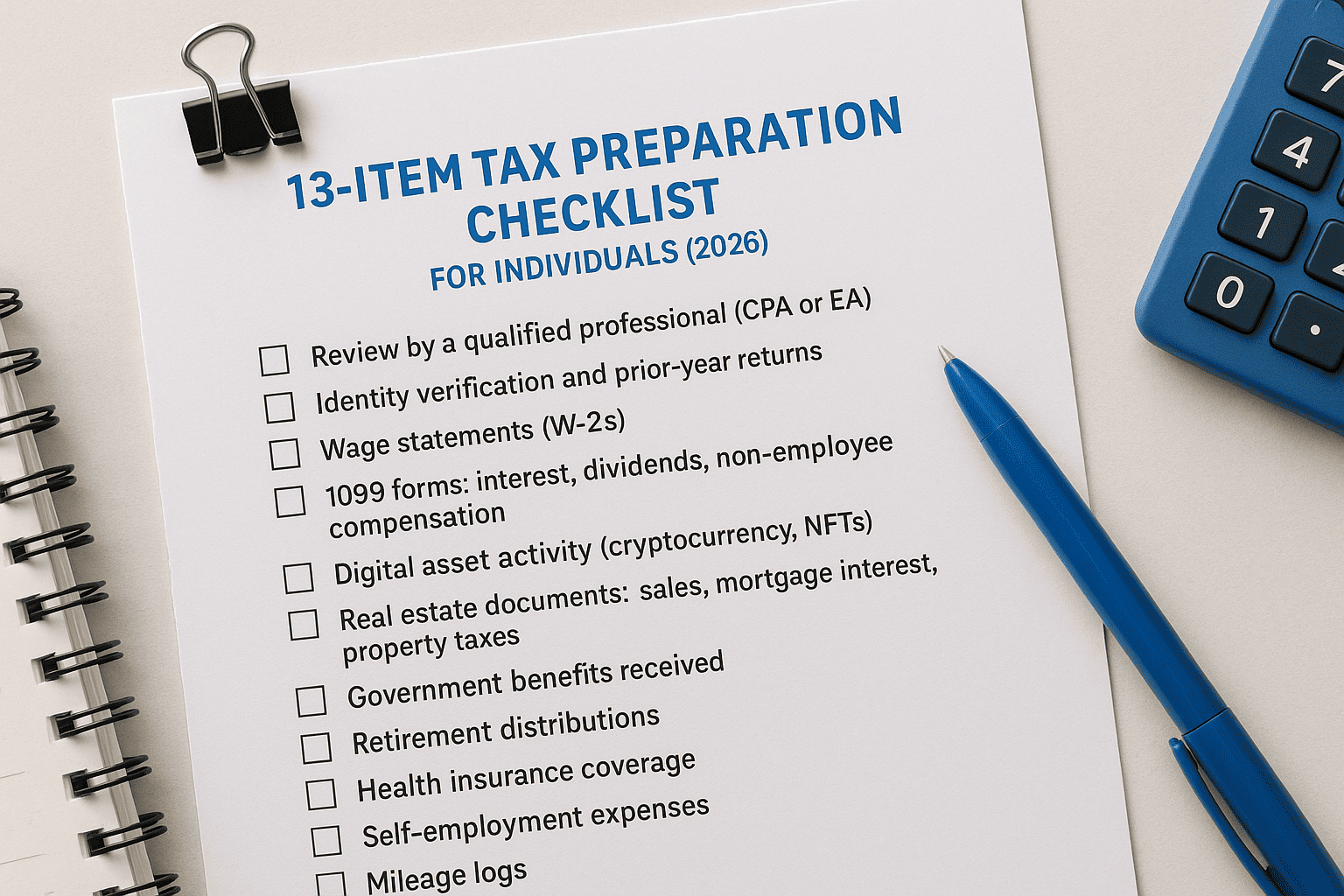

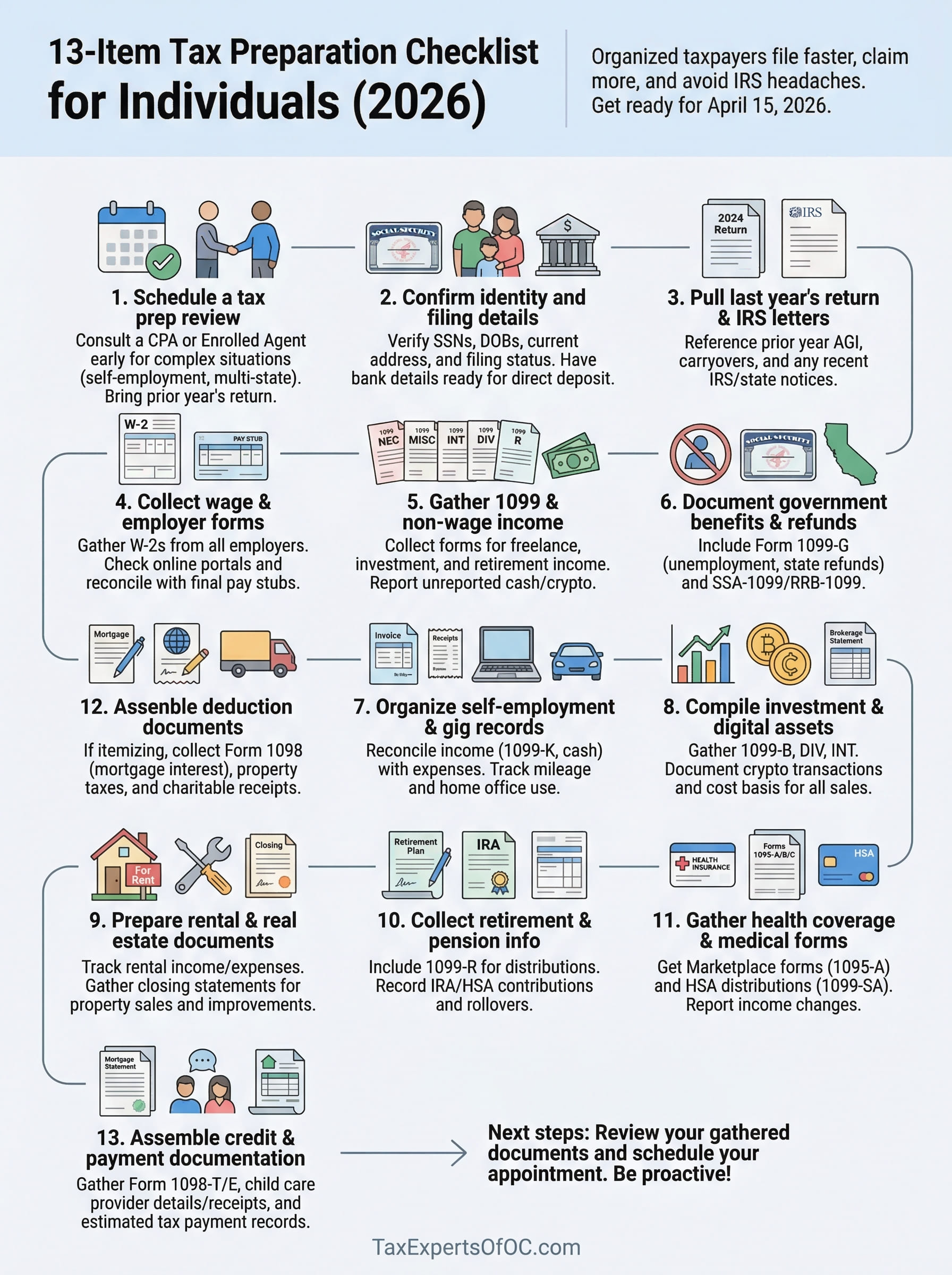

This checklist covers the 13 essential items you need to gather before you file your 2025 return (due April 15, 2026). We organized it in the order most people work through their returns, starting with basic personal information and moving through income documents, deductions, and credits. Print it, bookmark it, or forward it to your spouse. Either way, you'll walk into tax season ready.

1. Schedule a tax prep review with a CPA or enrolled agent

Before you start sorting receipts or logging into tax software, consider whether a CPA or Enrolled Agent is the right move for your situation. This step sits at the top of any complete tax preparation checklist for individuals because it shapes everything that follows. A qualified professional can identify deductions you might miss, flag potential issues before they become IRS problems, and represent you if questions arise after filing. Many firms, including Tax Experts of OC, offer a free 30-minute consultation so you can assess the fit before committing.

What to bring to the first call

Your first call with a tax professional goes much faster when you arrive prepared. Bring or send a copy of your most recent tax return (usually the prior year), a rough summary of any major income changes during the current year, and a list of significant life events such as marriage, divorce, a new dependent, or a home purchase. If you received any IRS or state notices since your last filing, include those as well. The professional uses this information to scope your return and estimate the complexity before the engagement begins.

- Prior-year federal and state returns

- Any IRS notices, audit letters, or balance-due letters

- Notes on major life or income changes

- Business income summary (if applicable)

Who benefits most from professional preparation

Most taxpayers can benefit from professional help, but a few groups have the most to gain. If you own a small business, work as a freelancer, received a large inheritance, or sold property during the year, the complexity of your return rises quickly. Families with multiple dependents, taxpayers navigating a divorce, and anyone with income from multiple states also tend to see the most value from working with a credentialed professional versus filing alone.

Taxpayers with self-employment income, rental properties, or prior-year IRS issues almost always recover the cost of professional preparation through deductions or penalty avoidance they would have missed on their own.

Red flags that signal you need representation

Some situations go beyond preparation and require a professional who can speak directly with the IRS on your behalf. If you have unfiled returns from prior years, received a notice of intent to levy or garnish, or owe back taxes you cannot pay in full, you need more than tax software. An Enrolled Agent or CPA with representation authority can negotiate installment agreements, submit offers in compromise, and stop collection actions while your case gets resolved.

- Unfiled returns from one or more prior years

- IRS levy, garnishment, or federal tax lien notice

- Back taxes you cannot pay in a lump sum

- A notice of audit or examination

2. Confirm your identity and filing details

Before any income document gets sorted, you need to confirm the basic personal information that determines your filing status, tax bracket, and eligibility for credits. Errors here, like a misspelled name or wrong Social Security number, are one of the most common reasons the IRS rejects an electronic return outright.

Personal information to verify

Every return starts with the same foundational data. Confirm your full legal name exactly as it appears on your Social Security card, your Social Security Number (SSN) or Individual Taxpayer Identification Number (ITIN), and your current mailing address. Your filing status (single, married filing jointly, married filing separately, head of household, or qualifying surviving spouse) also belongs in this category and directly affects your standard deduction and tax rate.

Choosing the wrong filing status is one of the most costly mistakes individuals make on an otherwise accurate return, and it often goes unnoticed until the IRS sends a correction notice.

Dependent and custody documents to gather

If you claim any dependents, gather each person's full legal name, date of birth, and SSN. For divorced or separated parents, also include your custody agreement or a signed copy of IRS Form 8332 if the other parent is formally releasing the exemption to you. These records prevent duplicate claims and protect your eligibility for dependent-related credits.

Banking details you need for refund or payment

Whether you expect a refund or owe a balance, having your bank account and routing numbers ready speeds up direct deposit and electronic payment processing. Locate a voided check or log into your bank's website to confirm the exact account and routing numbers before your preparer asks for them.

3. Pull last year's return and IRS letters

Your prior-year tax return is one of the most useful documents in any tax preparation checklist for individuals. It gives your preparer a baseline for income, filing status, and deductions, and it surfaces discrepancies before they become problems with the IRS.

Prior-year return pages to reference

Pull your complete federal and state returns, not just the first page. The key pages include your Form 1040 along with all schedules, your state return, and any worksheets related to credits or deductions. Your preparer also needs your prior-year adjusted gross income (AGI), which the IRS uses to verify your identity when you e-file a new return.

If you filed with a tax professional last year, request a full copy of the return package before your appointment this year.

Carryovers to look for

Some tax items carry forward from one year to the next and directly affect your current return. Check your prior-year return for capital loss carryovers, net operating loss carryovers, and passive activity losses from rental or business activity. Also review it for unused charitable contribution deductions and any credit carryforwards such as the general business credit.

- Capital loss carryovers (Schedule D)

- Passive activity loss carryovers (Form 8582)

- Charitable contribution carryovers

- Business credit carryforwards (Form 3800)

IRS and state notices to include

Any notice you received from the IRS or your state tax agency after your last filing belongs in your tax folder. This includes CP notices about balances due, correspondence about amended returns, and letters confirming a payment plan or resolution. Bring these documents to your preparer so they can confirm that all prior-year issues are fully resolved before your new return is submitted.

- Balance due or overpayment notices

- Audit or examination letters

- Amended return correspondence

- Payment plan confirmation letters

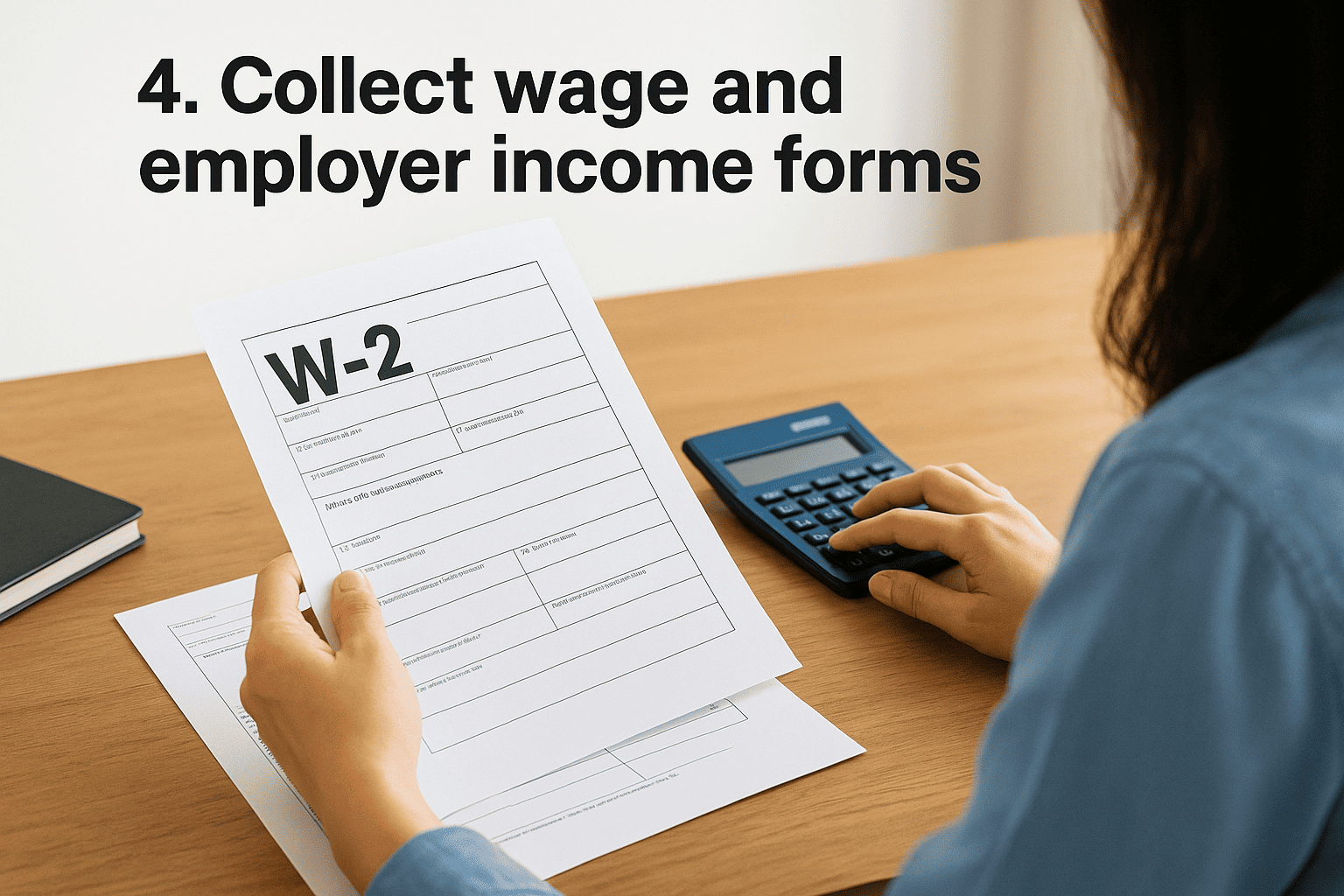

4. Collect wage and employer income forms

Wage income is the starting point for most personal returns, and the W-2 is the core document in this category. Every employer who paid you wages, salary, tips, or other compensation during 2025 must send you a Form W-2 by January 31, 2026. Many employers now deliver W-2s through an online payroll portal, so check your email and any HR platforms you used during the year before assuming a form is missing.

Forms to expect and where they show up

Your primary income document from each employer is Form W-2, which reports your total wages and the federal, state, and local taxes withheld. If you worked multiple jobs in 2025, you receive a separate W-2 from each employer. Check your final pay stub of the year to confirm the numbers match before handing the forms to your preparer.

A mismatch between your W-2 and your final pay stub often signals a payroll error that can delay your refund or trigger an IRS notice.

Items that often go missing

Several income sources fall off even a thorough tax preparation checklist for individuals. Tips reported to your employer appear on your W-2, but unreported cash tips must still be included separately on your return. Also look for W-2s from seasonal or part-time jobs you may have overlooked.

- W-2s from short-term or seasonal employment

- Cash tips not reported to your employer

- W-2s from a job you left early in the year

What to do if a form is wrong or late

If a W-2 contains an error, contact your employer's payroll department first and request a corrected Form W-2c. If January 31 passes and a form still has not arrived, contact the employer directly. If you still cannot get it, reach the IRS at 800-829-1040 and they can contact the employer on your behalf.

5. Gather 1099 income and other non-wage income

Non-wage income is the category where gaps in a tax preparation checklist for individuals become most expensive. Payers are required to mail 1099 forms by January 31, but digital delivery through brokerage accounts and payment platforms is increasingly common. Check every financial account portal you used during 2025 before assuming all your forms have arrived by mail.

Common 1099 forms and what they cover

Several 1099 variations exist, and each covers a different income type. Form 1099-NEC reports nonemployee compensation paid to freelancers and independent contractors. Form 1099-MISC covers rents, royalties, and certain other payments. Form 1099-INT reports bank interest, Form 1099-DIV covers dividends and capital gain distributions, and Form 1099-R reports retirement and pension distributions. Gather every version that applies to your accounts and payment sources.

A single missing 1099 can trigger an IRS CP2000 notice months after you file, so cross-reference your forms against your own income records before submitting your return.

Income you still must report without a 1099

Not every income source comes with a form attached, and the IRS expects you to report it regardless. Cash payments for freelance or contract work, informal rent income, barter income, and prizes or gambling winnings below the reporting threshold are all taxable. Keep your own records for these amounts so you can report them accurately even when no form arrives.

Records to match against the forms

Once your 1099s are in hand, compare each form against your bank statements or payment app records to confirm the amounts match. For freelancers, reconcile your 1099-NEC totals against invoices you issued. For investors, match your 1099-DIV and 1099-INT figures against your year-end account statements to catch any discrepancies before they reach your return.

6. Document government benefits and refunds

Government benefits and state tax refunds generate taxable income more often than people expect, and missing these forms is a common gap in any tax preparation checklist for individuals. Gather every form related to government payments before your filing appointment so nothing gets left off your return.

Unemployment and state refund forms

If you received unemployment compensation in 2025, the state agency that paid you will send Form 1099-G reporting the total amount. This income is fully taxable at the federal level. Your state tax refund from the prior year may also appear on a 1099-G, and whether it is taxable depends on whether you itemized deductions on your federal return in the year you received the refund.

- Form 1099-G for unemployment compensation

- Form 1099-G for state and local tax refunds

Social Security and railroad retirement forms

The Social Security Administration sends Form SSA-1099 to everyone who received Social Security benefits during the year. If you received railroad retirement benefits, look for Form RRB-1099 from the Railroad Retirement Board instead. Both forms report the gross benefit amount and any federal income tax withheld.

Up to 85 percent of your Social Security benefits can be taxable depending on your combined income, so bring your SSA-1099 even if you believe your income is too low to owe tax.

Common tax traps with benefit income

Many recipients assume government benefits arrive tax-free, but that assumption leads to surprise balances due at filing. If you did not elect voluntary withholding on your unemployment or Social Security payments throughout the year, you may owe taxes when you file. Review your Form W-4V elections and confirm whether withholding was applied to any benefit payments you received.

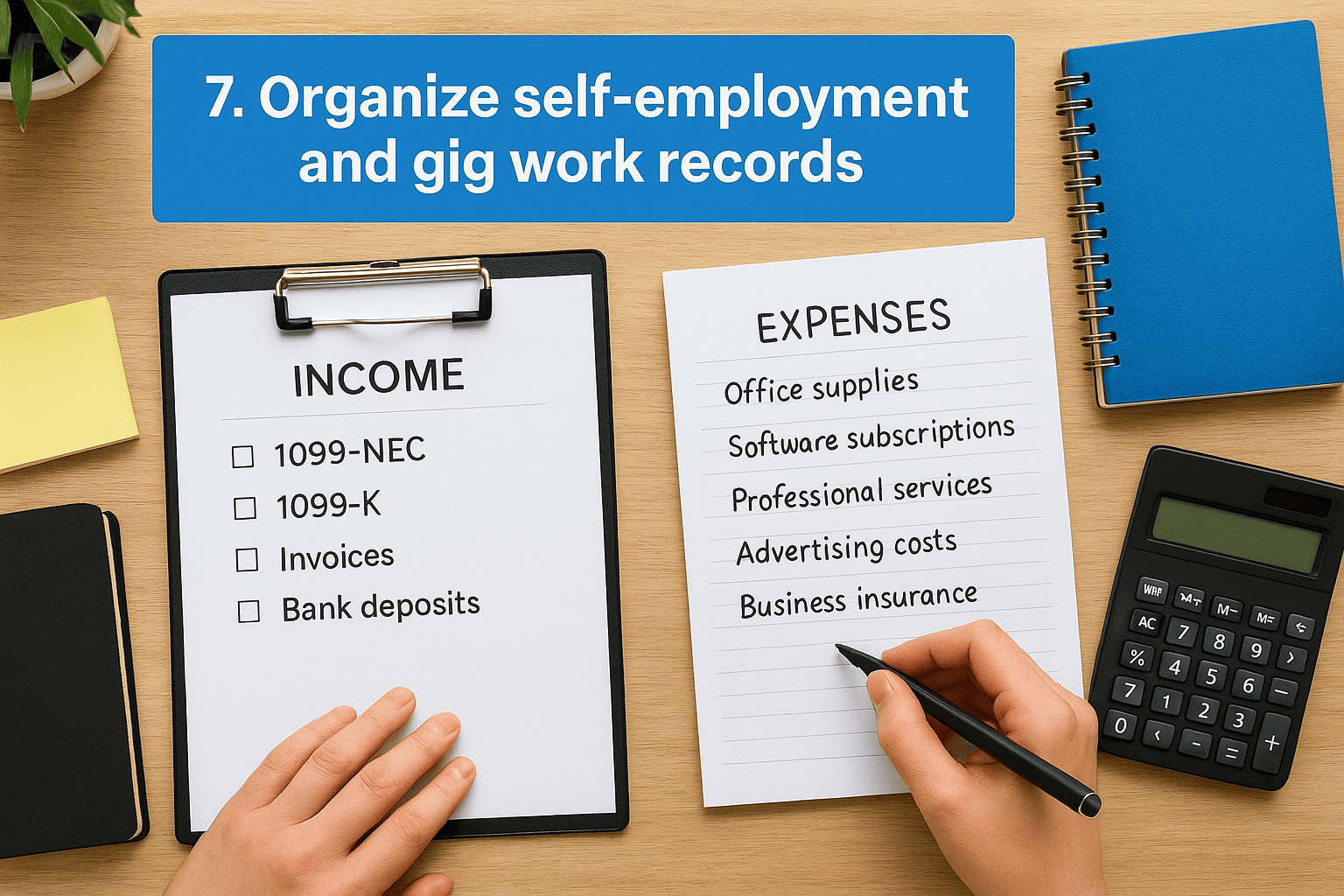

7. Organize self-employment and gig work records

Self-employment and gig income introduces the most document-intensive category on any tax preparation checklist for individuals. Unlike W-2 employees, self-employed taxpayers must reconstruct their total income and expenses from their own records rather than relying on a single employer form. Start pulling these documents together well before your filing appointment.

Income records you need to reconcile

Your goal is to confirm that every dollar you earned is accounted for. Collect all 1099-NEC and 1099-K forms from clients and payment platforms such as PayPal, Venmo, and Stripe. Then compare those totals against your own invoices, bank deposits, and payment app transaction histories. If you received cash payments that generated no form at all, include those amounts in your reconciliation.

The IRS cross-references 1099 totals against your Schedule C, so reporting less than what your forms show is a reliable way to receive a notice.

Expense categories to track and substantiate

Legitimate business expenses reduce your taxable self-employment income directly, so thorough documentation matters. Gather receipts and records for supplies, software subscriptions, professional services, advertising costs, business insurance, and tools specific to your work. Organize these by category so your preparer can apply them to the correct lines on Schedule C without guessing.

- Office supplies and equipment

- Professional fees and contractor payments

- Business-related travel and meals (50 percent deductible)

- Marketing and advertising costs

Home office and vehicle documentation

If you use part of your home exclusively for business, gather your total home square footage and the square footage of your dedicated workspace. For business vehicle use, your mileage log covering the full year is the most important document to have ready, along with records of total miles driven and any parking or toll receipts.

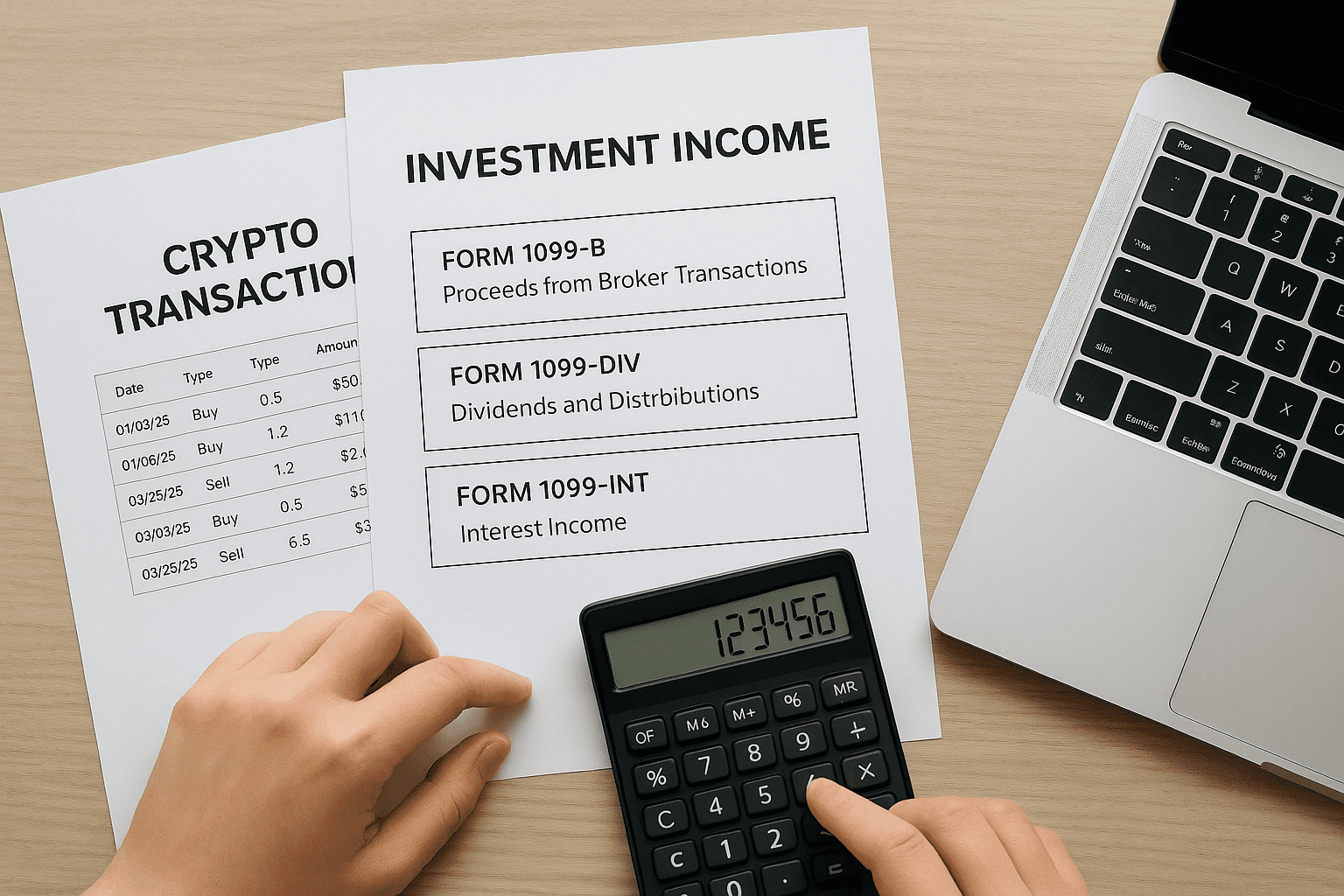

8. Compile investment and digital asset activity

Investment income adds several layers to any tax preparation checklist for individuals, and the records you need arrive from multiple sources across different timelines. Brokerage firms often send corrected statements in February and March, so confirm you have the final version of each form before your preparer files your return.

Brokerage forms and statements to gather

Your primary document for investment activity is Form 1099-B, which your brokerage issues to report proceeds from the sale of stocks, bonds, mutual funds, and other securities. You will also need Form 1099-DIV for dividend income and capital gain distributions, plus Form 1099-INT for any interest earned inside taxable accounts. Pull the year-end consolidated statement from each brokerage account you hold, since it typically combines all three forms in one document.

Brokerage firms frequently issue corrected 1099s through mid-March, so waiting until you have the final statement prevents you from filing an amended return later.

Cost basis and holding period records

Your cost basis is what you originally paid for an investment, and your holding period determines whether your gain or loss is taxed at short-term or long-term rates. For securities purchased before your current brokerage relationship began, gather original purchase confirmations or account transfer statements to establish an accurate basis. Without these records, your preparer may have to report your full sale proceeds as a gain.

Crypto, NFTs, and wallet exchange history

Every taxable cryptocurrency transaction, including sales, trades, and payments made with digital assets, generates a reportable gain or loss. Download your complete transaction history from each exchange you used in 2025, including records of wallet-to-wallet transfers, staking rewards, and any NFT sales, so your preparer can calculate the correct gain or loss on each event.

9. Prepare rental property and real estate sale documents

Rental properties and real estate transactions create some of the most complex entries on any tax preparation checklist for individuals. Gather your records before your filing appointment, because missing documents in this category frequently delay returns and increase the risk of an IRS inquiry.

Rental income and expense support

Every dollar of rent you collected in 2025 is taxable income, so pull your bank statements or property management reports to confirm your total rental receipts for the year. Alongside the income, compile receipts and records for every deductible expense, including repairs, property management fees, insurance premiums, utilities you paid, and advertising costs for finding tenants.

Repairs are immediately deductible, but improvements must be capitalized and depreciated, so keeping those two categories clearly separated saves your preparer significant time.

Depreciation and asset purchase details

Your rental property generates a depreciation deduction each year based on the original purchase price of the structure and any improvements you have made. Bring your prior-year depreciation schedule (typically attached to Schedule E) so your preparer can continue from the correct accumulated depreciation figure rather than recalculating it from scratch. If you purchased new appliances or made capital improvements during 2025, include the purchase receipts and dates for each item.

Home sale and closing documents

If you sold a primary residence or investment property in 2025, gather your closing disclosure from the sale along with the original purchase closing documents. Your preparer needs the original purchase price, the sale price, and any closing costs from both transactions to calculate your gain or loss accurately. Also locate records of major improvements made during your ownership period, since those additions increase your cost basis and reduce your taxable gain.

10. Collect retirement and pension information

Retirement income is a critical category on any tax preparation checklist for individuals, and it arrives through multiple forms that are easy to misplace. Whether you took a pension distribution, withdrew from an IRA, or converted funds between accounts, each transaction creates a tax event your preparer needs to document accurately.

Distribution forms and withholding details

Form 1099-R is the primary document for retirement and pension income, and you receive one from every plan that distributed funds to you during 2025. This covers traditional IRA withdrawals, 401(k) distributions, pension payments, and annuity income. The form also reports any federal and state income tax withheld from those distributions, so confirm the withholding amounts match your own records before your appointment.

If you took an early distribution before age 59½, your Form 1099-R will carry a distribution code that triggers the 10 percent penalty unless a specific exception applies.

IRA and HSA contribution records

Your IRA contributions made for the 2025 tax year are deductible only up to the annual limit, and you have until April 15, 2026 to make them. Gather your contribution statements from your IRA custodian to confirm the exact amount deposited. If you also contributed to a Health Savings Account in 2025, your HSA trustee will send Form 5498-SA, but your own contribution records are the most reliable source to bring to your preparer.

Basis and rollover documentation

If you ever made nondeductible contributions to a traditional IRA, part of each withdrawal is tax-free. Your Form 8606 from prior years tracks this basis, so locate it before your appointment. For any rollovers completed in 2025, pull the rollover confirmation from your financial institution to verify the transaction was completed correctly and within the required 60-day window.

11. Gather health coverage and medical-related tax forms

Health coverage generates specific tax forms that directly affect your return, and missing any of them is a recurring gap on any tax preparation checklist for individuals. Whether you received coverage through an employer, a government marketplace, or Medicare, each source comes with its own documentation requirements.

Marketplace and employer coverage forms

If you purchased health insurance through the Health Insurance Marketplace in 2025, you will receive Form 1095-A from your exchange. This form reports the months you were covered and the premiums you paid, and your preparer needs it to complete Form 8962 for the premium tax credit calculation. Employers who provide coverage send Form 1095-C (for large employers) or Form 1095-B (for smaller plans and insurers), but these are primarily records of coverage rather than active entries on your return.

HSA and medical account forms

Your HSA trustee sends Form 1099-SA to report any distributions you took from your Health Savings Account during 2025. Keep a record of what each distribution paid for, since only qualified medical expenses make those withdrawals tax-free. If you contributed to a Flexible Spending Account through your employer, review your year-end FSA statement to confirm you used the funds correctly.

Documents that affect premium tax credits

Reconciling your advance premium tax credit requires records of your actual household income versus what you estimated when you enrolled. Gather documentation of any income changes you reported (or failed to report) to the marketplace during the year, since a gap between your estimate and your actual income directly affects your Form 8962 calculation.

If your actual income exceeded your marketplace estimate, you may owe back part or all of the advance credit you already received.

12. Assemble deduction documents for homeowners and itemizers

Itemizing deductions instead of taking the standard deduction only makes sense when your qualifying expenses exceed the standard deduction threshold for your filing status. For 2025, that threshold is $15,000 for single filers and $30,000 for married filing jointly. Before your appointment, pull your potential deduction totals so your preparer can run a quick comparison and confirm which approach saves you more. This is one of the most impactful decisions in any tax preparation checklist for individuals, and it requires the right documents to make accurately.

Mortgage interest and property tax records

Your mortgage servicer sends Form 1098 each January reporting the interest you paid during the year, along with any mortgage insurance premiums and points. Locate this form and compare the interest total against your own mortgage statements to confirm the figure is accurate. Your property tax records, typically a county tax bill or payment confirmation, belong here as well.

Homeowners who refinanced during 2025 need a Form 1098 from each lender they paid interest to during the year, not just the current servicer.

Charitable donation substantiation

Cash donations of $250 or more require a written acknowledgment from the organization to be deductible. For noncash donations such as clothing or furniture dropped at a charity, gather your receipts and a list of donated items with estimated values. Donations of property valued above $500 also require Form 8283.

State and local tax payment support

Your deduction for state and local taxes (SALT) is capped at $10,000 per return. Gather your state income tax return from 2024, any estimated state tax payments made in 2025, and your property tax payment confirmations to document the full SALT amount available to your preparer.

13. Assemble credit and payment documentation

Credits and payments reduce your tax liability dollar for dollar, which makes them the highest-value entries on any tax preparation checklist for individuals. Gathering all supporting documents before your appointment lets your preparer apply every credit you qualify for without leaving money unclaimed.

Education credits and student loan interest forms

Your school sends Form 1098-T to report tuition and fees paid during 2025, and your lender sends Form 1098-E to report student loan interest. Both forms support claims for the American Opportunity Credit, Lifetime Learning Credit, and the student loan interest deduction.

Keep your own payment receipts alongside these forms because the amounts on Form 1098-T sometimes differ from what you actually paid out of pocket.

Child and dependent care credit records

To claim the child and dependent care credit, gather the name, address, and Taxpayer Identification Number (TIN) of every care provider you paid during 2025. Also pull statements confirming the total amount you paid to each provider throughout the year. If your employer offered a dependent care FSA, confirm your W-2 Box 10 figure before your appointment, since it directly reduces the credit amount available to you.

- Provider name, address, and TIN

- Receipts or statements showing total payments made

- W-2 Box 10 amount if a dependent care FSA was used

Estimated payments, extensions, and prior-year credits applied

If you made quarterly estimated tax payments during 2025, pull your bank records or your IRS online account to confirm each payment date and exact amount. Gather any extension payment submitted with Form 4868 as well. Check your prior-year return to see whether you directed an overpayment toward 2025 rather than requesting a refund, since your preparer needs all three figures to calculate your final balance accurately.

Next steps

Working through this tax preparation checklist for individuals before your filing appointment saves time, reduces errors, and puts every deduction you qualify for directly in front of your preparer. The 13 categories above cover the full range of documents most individual filers need, from basic identity records and W-2s to investment activity, retirement income, and credits. Once you have everything gathered, review each item one more time to confirm nothing is missing or outdated.

Your next move is straightforward: schedule a review with a qualified tax professional before April 15, 2026. Waiting until the last week of the season compresses your options and increases the chance of errors. If your return involves self-employment, rental income, prior-year IRS issues, or multi-state filing, professional representation pays for itself. The team at Tax Experts of OC is ready to help. Book your free 30-minute consultation and walk into filing season fully prepared.