Getting a letter from the IRS announcing a business tax audit can stop you mid-stride. Your mind races through years of deductions, receipts you may or may not have saved, and every judgment call you made on a return. But here's what most business owners don't realize: an audit isn't an accusation. It's an examination, and how you respond to it matters far more than the fact that it's happening.

At Tax Experts of OC, our CPAs and Enrolled Agents represent business owners through IRS audits across all 50 states. We've seen what triggers them, what makes them worse, and what separates a smooth resolution from a costly one. The difference almost always comes down to preparation and professional guidance.

This article breaks down how the business tax audit process actually works, the most common reasons the IRS selects a return for review, and concrete steps you can take to prepare if you're facing an examination, or reduce your chances of being selected in the first place.

Why business tax audits happen and what is at stake

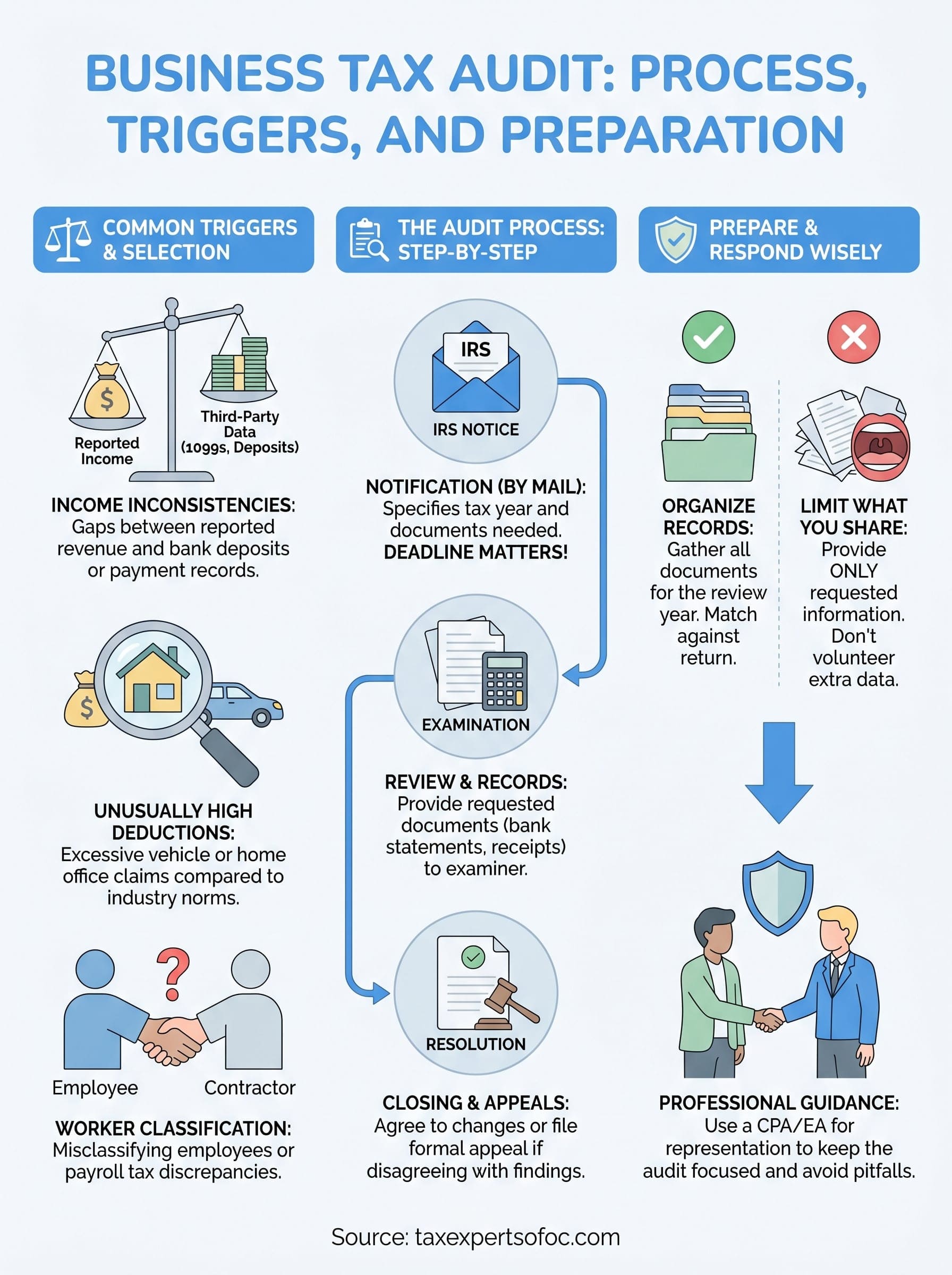

The IRS doesn't audit businesses randomly. Its selection process is systematic and data-driven, built around a combination of automated scoring, statistical benchmarks, and specific signals in your return. Understanding why a business tax audit gets triggered helps you see it for what it is: a process with predictable patterns, not an arbitrary disruption to your operations.

How the IRS selects returns for examination

The IRS uses a scoring system called the Discriminant Information Function (DIF) to evaluate every return it receives. Your return gets scored against statistical norms for businesses in your industry and income range. If your numbers fall outside those norms, your score goes up, and a higher score increases the chance that a human examiner takes a closer look. Third-party data, such as 1099s, W-2s, and financial institution reports, gets cross-referenced against what you report. Any gap between those sources and your return raises a flag.

The IRS also runs targeted audit programs that focus on specific industries, business types, or tax issues it has identified as high-risk in a given year.

Beyond the DIF score, related-party audits can pull you in. If a business partner, investor, or major vendor gets audited, your return may come under review as a result, even if your own filing was accurate and complete.

What you actually risk if an audit goes badly

A poorly handled audit can cost you far more than the original tax difference. Back taxes are only the starting point. The IRS can add accuracy penalties of 20 percent on the underpaid amount, and if it determines fraud was involved, that penalty jumps to 75 percent. Interest accrues daily on any amount owed from the original due date, so delays in resolving an audit make the final bill grow.

Your business operations can also take a hit. An audit that uncovers unreported income or improper deductions can lead to liens on business assets or levies on your accounts. For small businesses operating on tight margins, that kind of outcome can threaten the business itself, not just its tax bill.

Who audits businesses and what they look at

Not every business tax audit comes from the same part of the IRS. Which division handles your case and what that examiner is trained to look for both shape how the process unfolds. Knowing who you're dealing with helps you and your representative respond in the right way from the start.

The IRS divisions that handle business audits

The IRS routes business examinations through different offices depending on the size and complexity of the return. Small businesses and self-employed filers typically fall under the Small Business/Self-Employed (SB/SE) Division, which handles the majority of business audits. Larger corporations with assets above a certain threshold get assigned to the Large Business and International (LB&I) Division, which uses teams of specialists and tends to run longer, more detailed examinations.

The division assigned to your case affects the scope, timeline, and resources the IRS brings to the table, which is why having professional representation matters early.

What examiners focus on during the review

Examiners are trained to look for inconsistencies between what you reported and what the IRS can verify through third-party sources. On the income side, they check that your reported revenue matches 1099s, bank deposits, and payment processor records. On the deduction side, they scrutinize business expenses that appear unusually high relative to your industry, such as meals, travel, vehicle use, and home office claims. They also look at whether you correctly classified workers as employees versus independent contractors, since misclassification carries its own set of tax consequences.

Common business tax audit triggers to watch for

Several patterns consistently draw IRS attention, and knowing what they are gives you a real advantage. While no single item guarantees a business tax audit, certain combinations of factors raise your DIF score significantly and increase the probability of a closer look.

Income reporting inconsistencies

Underreported income is one of the most reliable triggers. If your bank deposits, payment processor records, or 1099s don't match the revenue on your return, an examiner will notice. Cash-intensive businesses, such as restaurants, contractors, and retail shops, face extra scrutiny because the IRS knows that cash transactions are harder to verify independently.

Even small gaps between third-party reports and your filed return can flag your business for review.

Unusually high deductions

Claiming deductions that fall well outside the norms for your industry puts your return on the IRS radar. Vehicle and home office deductions are two of the most over-claimed categories, and examiners know it. If you claim 100 percent business use of a vehicle or a large portion of your home as an office, you need documentation that clearly supports those numbers.

Worker classification and payroll issues

Misclassifying employees as independent contractors reduces your payroll tax obligations, and the IRS actively looks for this pattern. Similarly, payroll tax discrepancies, such as differences between wages reported on W-2s and amounts paid to the IRS, create immediate red flags that can escalate quickly into a broader examination.

How the business tax audit process works step by step

A business tax audit follows a defined sequence from the first notice to the final resolution. Understanding each stage helps you respond with intention rather than reacting out of fear, and it reduces the chance you'll say or submit something that complicates your case.

How the IRS notifies you

The IRS contacts you exclusively by mail for the initial notice. It will not call you out of the blue or email you. The letter identifies which tax year is under review, what type of audit applies, and what documentation the IRS wants you to provide. Read it carefully before doing anything else, and note the response deadline.

Missing the response deadline can escalate a routine examination into a more serious collections situation, so treat the date on that letter as a hard stop.

What happens during the examination

Your examiner will either request documents by mail for a correspondence audit or schedule an in-person meeting for a field or office audit. You'll need to produce records that support the items under review, such as bank statements, receipts, contracts, and payroll records. Professional representation at this stage keeps the scope of the examination focused and prevents you from volunteering information that opens new lines of inquiry.

How the audit closes

Once the examiner finishes reviewing your records, the IRS issues a Revenue Agent Report that outlines any proposed changes. You can agree with the findings, negotiate adjustments, or file a formal appeal through the IRS Independent Office of Appeals if you disagree with the outcome.

How to prepare and respond without creating new issues

Your response to a business tax audit sets the tone for everything that follows. Acting too quickly or submitting more documentation than the IRS specifically requested are two of the most common mistakes business owners make, and both can open new lines of inquiry you weren't expecting.

Organize your records before you respond

Start by pulling together every document that relates to the specific tax year and items under review. Bank statements, receipts, invoices, contracts, and payroll records should all be gathered and matched against what you reported on your return. If you find a gap between your records and your return, note it before the examiner does.

Work with a CPA or Enrolled Agent during this phase so you understand exactly what the IRS is asking for before you send anything.

Avoid submitting records for years the IRS didn't request, and keep originals separate from the copies you plan to provide. Disorganized submissions can signal poor recordkeeping and give the examiner a reason to look more broadly at your finances.

Limit what you share with the examiner

Responding to an audit is not the same as full financial disclosure. Only provide what the IRS specifically asked for in the notice and nothing beyond that scope. Volunteering extra returns, additional financial statements, or explanations that reach outside the reviewed period can give an examiner a reason to expand the audit significantly.

Letting a qualified representative handle all direct communication with the IRS removes that risk entirely and keeps the examination contained to its original scope, which protects you throughout the process.

Next steps after you get audit results

When the IRS sends you a final determination after a business tax audit, you have more options than simply accepting what it says. If you agree with the findings, you sign the agreement form and arrange payment for any balance owed, including any applicable penalties and interest. If you disagree, you can file an appeal with the IRS Independent Office of Appeals, and in some cases pursue the matter in Tax Court.

Your response window is limited, so moving quickly matters. Unpaid balances begin accruing additional interest from the date the IRS issues its determination, and missing appeal deadlines removes options that were otherwise available to you.

Resolving an audit on your own is possible, but having a CPA or Enrolled Agent in your corner significantly improves your outcome. If you're dealing with audit results or want to get ahead of a potential examination, contact Tax Experts of OC for a free 30-minute consultation.