Most small business owners pay more in taxes than they need to, not because they're careless, but because they don't know what qualifies as a deduction. Business tax deductions directly reduce your taxable income, which means real money stays in your business instead of going to the IRS. The problem is that the tax code doesn't exactly make it easy to figure out what you can and can't write off.

Whether you're a sole proprietor, an LLC, or running an S-corp, there are deductions available to you right now that you might be overlooking. Some are obvious (yes, office rent counts). Others, like the home office deduction or vehicle expenses, come with specific rules that trip people up during audits. Getting them right matters, and getting them wrong can cost you more than the deduction was worth.

At Tax Experts of OC, our CPAs and Enrolled Agents help small business owners across all 50 states claim every deduction they're entitled to, accurately and defensibly. Below, we break down 13 deductions every small business should know about, with clear explanations of who qualifies and how each one works. Consider this your practical guide to keeping more of what you earn.

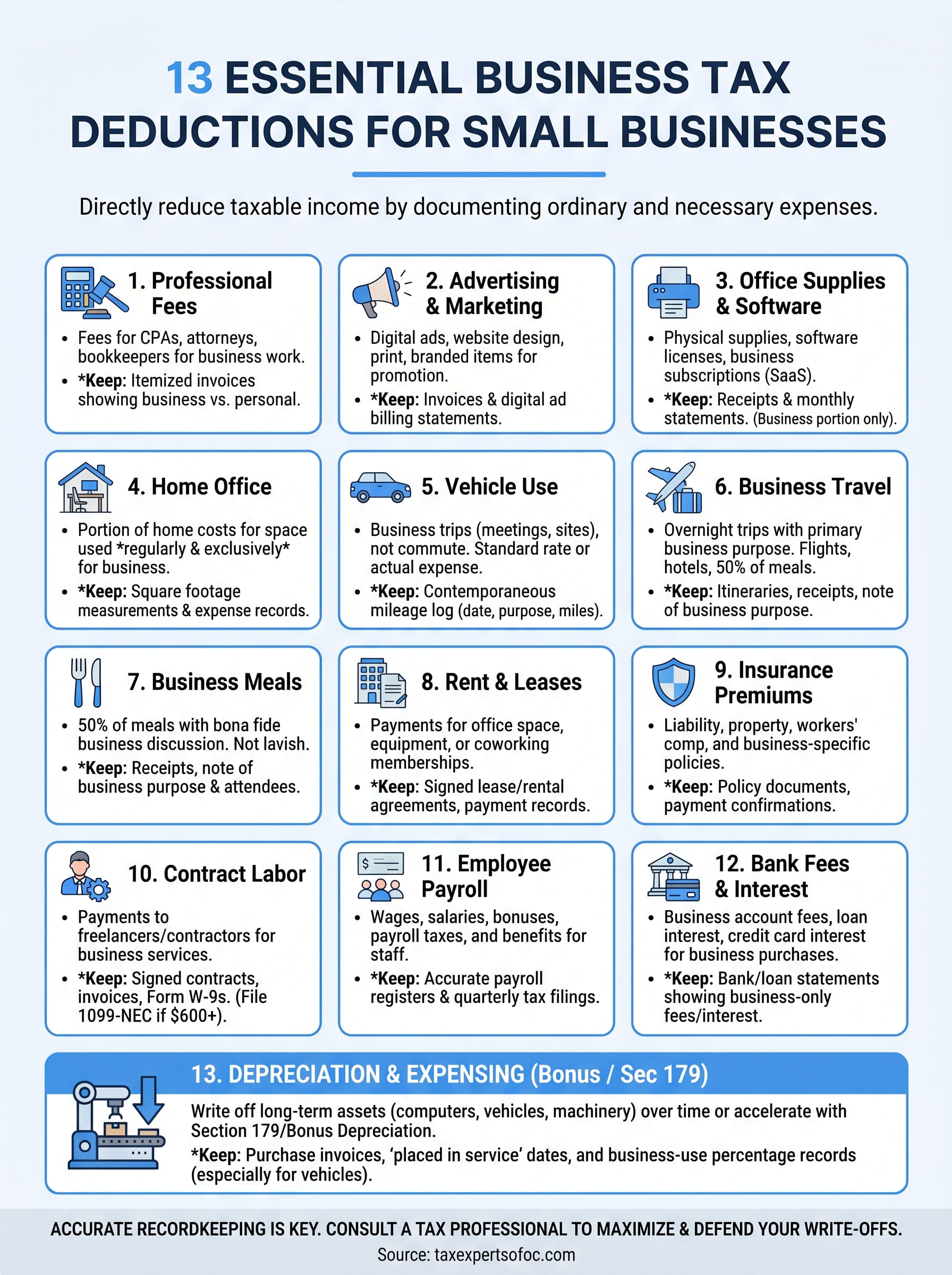

1. Legal, tax, and accounting professional fees

When you pay professionals to help run your business legally and financially, the IRS generally lets you deduct those costs. This is one of the most straightforward business tax deductions available to small business owners, but people still leave money on the table by not tracking every dollar they spend on professional services throughout the year.

What qualifies

Fees you pay to CPAs, tax preparers, bookkeepers, Enrolled Agents, attorneys, and financial consultants for business-related work qualify under IRS Publication 535. This includes tax preparation fees for your business return, the cost of bookkeeping services, legal fees for drafting contracts or resolving business disputes, and fees paid for tax representation before the IRS.

Note that legal fees related to personal matters, even if they tangentially involve your business, are not deductible.

You cannot deduct fees paid to attorneys or accountants for personal tax returns or personal legal matters, even if you use the same professional who handles your business work. The expense must be ordinary and necessary for your business operation to qualify.

How to calculate the deduction

Add up every invoice you paid to qualifying professionals during the tax year. If a professional handles both personal and business work, you can only deduct the portion attributable to your business. Ask your accountant to itemize invoices if they cover mixed work, so you have a clear business-use percentage on record.

Records to keep

Keep every invoice and receipt from your professional service providers. Bank statements or credit card records showing payment amounts help, but itemized invoices are what hold up under IRS scrutiny. Store these alongside the contracts or engagement letters that show the scope of work performed.

- Dated invoices with itemized service descriptions

- Proof of payment (bank statement or cancelled check)

- Engagement letters or contracts with the service provider

- Notes on which services relate to business vs. personal matters

Red flags and common mistakes

The most common mistake is deducting the full cost of a combined personal-and-business invoice without allocating correctly. Another issue is claiming fees for work that had no clear business purpose. If an attorney helped you with a personal injury claim unrelated to your business, that fee does not qualify, regardless of who paid the bill.

2. Advertising and marketing

The IRS lets you deduct ordinary and necessary costs to market your products or services. These are among the most accessible business tax deductions for small businesses, covering both digital and traditional promotion.

What qualifies

Almost any expense directly tied to promoting your business qualifies: paid digital ads (Google Ads, Meta, LinkedIn), social media management fees, website design and maintenance, SEO services, print advertising, business cards, branded merchandise, and event sponsorships connected to your business.

Website design and maintenance fees count as advertising expenses as long as you treat them as recurring operational costs rather than capital improvements.

How to calculate the deduction

Add up every qualifying advertising expense you paid during the tax year. If a campaign spans two tax years, deduct only the portion attributable to the current filing year, not the full contract amount.

Records to keep

Keep invoices and receipts from every vendor you paid for promotional work. For digital ad campaigns, download monthly billing statements from each platform and file them with your tax records.

- Ad platform billing statements (Google, Meta, etc.)

- Invoices from agencies, designers, or consultants

- Receipts for print materials or branded merchandise

- Contracts with marketing service providers

Red flags and common mistakes

The most frequent mistake is mixing personal social media costs with business promotion expenses. If you upgrade a personal account or pay for a service that primarily benefits you personally, that cost does not qualify.

Always pay for business advertising from a dedicated business account. Commingling personal and business payments is one of the fastest ways to lose a deduction under IRS examination.

3. Office supplies, software, and subscriptions

Day-to-day operational costs add up fast, and many of them qualify as business tax deductions. The IRS allows you to deduct purchases of supplies and software you use regularly to run your business, as long as the expense is ordinary and necessary for your operations.

What qualifies

Pens, paper, printer ink, and other physical office supplies you use in the course of doing business are fully deductible. Software licenses, monthly SaaS subscriptions (such as accounting platforms, project management tools, or communication apps), cloud storage plans, and website hosting fees also qualify. If a subscription covers both personal and business use, only the business portion is deductible.

The IRS treats annual software subscriptions as deductible expenses in the year you pay them, not spread across future periods, so timing your purchases can directly affect your tax liability.

How to calculate the deduction

Total every qualifying purchase made during the tax year. For subscriptions with mixed personal and business use, calculate the percentage of business use and apply it to the total annual cost. Keep that calculation documented in writing so you can support the number if the IRS asks.

Records to keep

Receipts and invoices are your best protection during an audit. For software and subscriptions, monthly billing statements from each vendor work well. Organize them by vendor and tax year.

- Receipts for physical supply purchases

- Invoices or billing statements from software vendors

- Bank or credit card records confirming payment dates and amounts

Red flags and common mistakes

The biggest mistake is deducting personal subscriptions as business expenses. Streaming services, personal cloud storage, or apps you use exclusively outside work hours do not qualify, even if you open them occasionally during the workday.

4. Home office expenses

If you regularly use part of your home exclusively for business, the IRS allows you to deduct a portion of your housing costs as a legitimate business tax deduction. This applies to homeowners and renters alike, as long as the space meets the IRS requirements.

What qualifies

Your home office must meet two requirements: regular use and exclusive use for your business. The space must be your principal place of business or where you meet clients consistently. A dedicated room works best; a corner of your living room that doubles as personal space generally does not qualify.

How to calculate the deduction

The IRS offers two calculation methods. The simplified method lets you deduct $5 per square foot of your home office, up to 300 square feet, for a maximum of $1,500. The regular method requires calculating your office's share of your home's total square footage and applying that percentage to actual expenses like rent, mortgage interest, utilities, and insurance.

The regular method often produces a larger deduction but demands more documentation, so run both calculations before you decide which to use.

Records to keep

Keep documentation that supports both the size of your workspace and the costs associated with your home. Organized records make it straightforward to defend the deduction if the IRS questions it.

- Square footage measurements for your home office and your total home

- Rent or mortgage statements, utility bills, and insurance invoices

- Photos of the dedicated workspace to support exclusive-use claims

Red flags and common mistakes

The most common mistake is claiming a space that serves dual purposes, like a guest bedroom you also use as an office. If the IRS finds the space is not exclusively used for business, it will disallow the entire deduction, not just a portion of it.

5. Business vehicle use and mileage

If you use a vehicle for business purposes, those costs count as business tax deductions under IRS rules. Whether you own one car or a fleet of trucks, the IRS provides two methods to deduct vehicle-related expenses for any miles driven in service of your business.

What qualifies

Trips you make for client meetings, job sites, supply runs, or business errands qualify as deductible business miles. Your daily commute from home to your regular office does not qualify, even if you think of it as work-related travel.

How to calculate the deduction

You choose between two IRS-approved methods. The standard mileage rate (67 cents per mile for 2024) lets you multiply qualifying miles by the current rate. The actual expense method requires you to track real costs like gas, insurance, repairs, and depreciation, then apply the percentage of total miles driven for business.

You must choose your method in the first year you use a vehicle for business; switching methods later comes with restrictions, so pick carefully.

Records to keep

A mileage log is your most important document. The IRS expects entries showing the date, destination, business purpose, and miles driven for each trip.

- Date and starting location of each trip

- Business destination and purpose

- Total miles driven per trip

- Odometer readings at the start and end of the year

Red flags and common mistakes

The most common mistake is failing to keep a contemporaneous mileage log. Reconstructing your driving history at tax time from memory will not hold up under IRS scrutiny. A simple app or spreadsheet updated in real time is all you need to protect this deduction.

6. Business travel

When your work takes you away from home overnight, the IRS allows you to deduct qualifying travel costs as business tax deductions. These expenses can add up to a significant reduction in taxable income, but the rules around what qualifies are specific enough that many small business owners either under-claim or get flagged for claiming too much.

What qualifies

Travel must be temporary and require you to stay away from your tax home (your regular place of business) overnight to qualify. Deductible costs include flights, trains, rental cars, taxis, rideshares, hotels, and 50% of meals you purchase while traveling. The trip must have a clear primary business purpose, such as attending a conference, meeting a client, or visiting a job site.

Personal side trips taken during a business trip are not deductible, even if the overall trip otherwise qualifies.

How to calculate the deduction

Add up all qualifying transportation, lodging, and meal costs for each trip during the tax year. Apply the 50% meal limitation to any food and beverage expenses incurred while away. If a trip combines business and personal time, allocate costs proportionally based on the number of business days versus personal days.

Records to keep

- Itineraries and receipts for every flight, hotel, and transportation expense

- A written note documenting the business purpose of each trip

- Calendar entries or meeting confirmations that show business activity on travel days

Red flags and common mistakes

The most common mistake is deducting travel for trips that were primarily personal with minor business activity attached. The IRS looks at whether the primary driver of the trip was business, not whether any business happened during it. Keep your documentation specific about what business you conducted and on which days.

7. Business meals

The IRS allows you to deduct 50% of qualifying meal costs when those meals have a clear business purpose. This is one of the more frequently misapplied business tax deductions, largely because the rules changed with the Tax Cuts and Jobs Act and many owners are still operating on outdated assumptions.

What qualifies

A meal qualifies when you have a bona fide business discussion with a client, prospective client, employee, or business partner during or directly before or after the meal. The meal must not be lavish or extravagant, and you or one of your employees must be present. Office snacks and meals you provide to employees on your business premises for your convenience also qualify.

Entertainment expenses like sporting events or concerts, even when combined with a meal, no longer qualify for any deduction under current tax law.

How to calculate the deduction

Add up all qualifying meal costs for the year and multiply by 50%. That 50% limitation applies to both the food and any applicable taxes and tips included in the bill.

Records to keep

- Receipts for every meal showing the amount, date, and restaurant name

- A written note of the business purpose and the names of everyone present

- The business relationship of each person at the meal

Red flags and common mistakes

The most common mistake is failing to document the business purpose at the time of the meal. A credit card statement alone is not enough. Without a written record of who you met with and why, the IRS will disallow the deduction entirely.

8. Rent, coworking, and equipment leases

Payments you make to use space or equipment in your business are fully deductible, and this category covers more ground than most owners realize. From a traditional office lease to a monthly coworking membership or a rental agreement on specialized machinery, these costs qualify as business tax deductions as long as the space or equipment serves a business purpose.

What qualifies

Rent you pay for office space, retail locations, storage units, warehouses, or coworking memberships is deductible. Equipment leases also qualify, including rentals of computers, vehicles, tools, or machinery used in your operations. The space or equipment must be used for business, not personal purposes.

- Office and retail space leases

- Coworking and shared workspace memberships

- Equipment rentals for business operations

How to calculate the deduction

Add up all rent and lease payments you made during the tax year. If a space has mixed personal and business use, calculate the business-use percentage and deduct only that portion.

If your lease includes an option to buy, the IRS may classify the arrangement as a purchase rather than a rental, which changes how you deduct the cost entirely.

Records to keep

Keep every signed lease agreement and payment record for rented spaces and equipment. Bank statements showing the payment dates and amounts support your deduction if the IRS asks.

- Signed lease or rental agreements

- Monthly payment records or bank statements

- Documentation of the business purpose for each rental

Red flags and common mistakes

The most common mistake is deducting the full rent on a space you also use personally without reducing the deduction to reflect actual business use. Failing to identify lease-to-own arrangements correctly is another issue that leads to incorrect deduction amounts that the IRS will challenge.

9. Business insurance premiums

Insurance is a real cost of doing business, and the IRS treats most business insurance premiums as fully deductible. If you carry coverage specifically to protect your operations, those premiums count as business tax deductions you can claim each year.

What qualifies

Premiums you pay for general liability, professional liability (errors and omissions), commercial property, business interruption, workers' compensation, and malpractice insurance all qualify. Cyber liability coverage and commercial auto insurance also count, provided the policy covers a vehicle or asset used for business.

Health insurance premiums for yourself as a self-employed individual are deductible separately on Schedule 1, not as a business expense on Schedule C.

How to calculate the deduction

Add up every qualifying premium payment you made during the tax year. If you pay annually, deduct the full amount in the year you paid it. If a single policy covers both personal and business assets, calculate the business-use percentage and apply it to the total premium cost.

Records to keep

Keep your insurance policy documents alongside payment receipts or bank statements. Insurers typically issue annual billing summaries that work well as supporting documentation.

- Policy declarations pages showing coverage type and effective dates

- Payment confirmations or bank records for each premium paid

- Insurer invoices or annual billing statements

Red flags and common mistakes

The most common mistake is deducting life insurance premiums where your business is the named beneficiary. The IRS specifically disallows that deduction. Claiming personal health or life insurance costs as business expenses without meeting the self-employed qualifying rules is another error that draws direct IRS scrutiny.

10. Independent contractors and contract labor

When you pay freelancers, consultants, or other independent contractors to perform work for your business, those payments are fully deductible. This is one of the more straightforward business tax deductions available, but it comes with a reporting obligation that many small business owners overlook until it causes problems at tax time.

What qualifies

Payments to independent contractors for services rendered in connection with your business are deductible under IRS rules. This includes graphic designers, web developers, copywriters, bookkeepers, IT consultants, and any other specialist you bring on without adding them to your payroll. The work must serve a legitimate business purpose, and the person must genuinely meet the IRS definition of an independent contractor rather than an employee.

If the IRS determines that a worker you classified as a contractor was actually an employee, you become liable for back payroll taxes, penalties, and interest on every payment you made.

How to calculate the deduction

Add up every payment you made to qualifying contractors during the tax year. If a single contractor received $600 or more from your business, you are required to issue them a Form 1099-NEC by January 31 of the following year.

Records to keep

- Signed contracts or agreements outlining the scope of work and deliverables

- Invoices from each contractor showing payment amounts and dates

- Completed Form W-9 collected from each contractor before the first payment

Red flags and common mistakes

The most common mistake is misclassifying employees as independent contractors to avoid payroll taxes. The IRS uses a behavioral, financial, and relationship-based test to determine worker status, and getting it wrong carries significant financial penalties.

11. Employee wages, benefits, and payroll costs

What you pay your employees is one of the most significant business tax deductions available to any small business with staff. The IRS allows you to deduct wages, salaries, bonuses, commissions, and most employee benefits as ordinary and necessary business expenses, provided the compensation is reasonable and the work is actually performed.

What qualifies

Deductible employee costs include regular wages and salaries, overtime pay, bonuses, and vacation pay. You can also deduct your employer share of payroll taxes, health insurance premiums paid on behalf of employees, contributions to retirement plans, and fringe benefits like education assistance or dependent care programs.

Sole proprietors and single-member LLC owners cannot deduct their own draws as wages, but owner-employees of S-corps can deduct a reasonable salary paid to themselves.

How to calculate the deduction

Add up all qualifying compensation and benefit costs you paid during the tax year. Include your employer share of FICA taxes, unemployment tax contributions, and premiums for employer-sponsored benefits. Each cost is tracked separately across your payroll records and quarterly filings, so pulling the totals is straightforward if your records are current.

Records to keep

Accurate payroll documentation is your primary defense if the IRS questions your wage deductions. Keep these records for at least four years after the filing date.

- Payroll registers showing gross wages, deductions, and net pay per employee

- Quarterly Form 941 filings and annual W-2 and W-3 forms

- Benefit plan contribution statements and insurance premium invoices

Red flags and common mistakes

The most common mistake is paying unreasonable compensation to family members employed in the business. The IRS allows deductions only for wages that reflect actual work performed at a rate comparable to what you would pay an unrelated employee doing the same job.

12. Bank fees and business interest

The costs of financing and managing your business accounts are legitimate business tax deductions that many small business owners forget to track. If you carry a business credit card, took out a loan, or pay monthly fees on a business checking account, those costs are fully deductible under IRS rules.

What qualifies

Business bank account fees, wire transfer fees, merchant processing fees, and service charges all qualify as deductible expenses. Interest paid on business loans, business credit cards, and lines of credit also qualifies, as long as the borrowed funds were used strictly for business purposes.

If you use a personal loan or credit card to fund business expenses, you can still deduct the interest, but only on the portion of the balance that financed business costs.

How to calculate the deduction

Add up all qualifying fees and interest charges you paid during the tax year. Your lender will issue a Form 1098 for significant interest payments, but smaller fees from bank statements need to be totaled manually.

Records to keep

Organized records make this deduction easy to defend.

- Monthly bank statements showing all fees charged to your account

- Loan statements detailing interest paid versus principal for each payment

- Credit card statements for any business-use accounts

Red flags and common mistakes

The most common mistake is deducting interest on funds used for personal expenses. If you drew from a business line of credit to cover a personal purchase, that portion of the interest does not qualify. Keep your business and personal borrowing completely separate to protect this deduction.

13. Depreciation, section 179, and bonus depreciation

When your business buys equipment, machinery, or other long-term assets, the IRS normally requires you to deduct the cost gradually over several years through depreciation. Two exceptions, Section 179 and bonus depreciation, let you accelerate that deduction and take a larger write-off in the year you place the asset in service.

What qualifies

Tangible business property you buy and actively use qualifies for depreciation deductions. This includes computers, machinery, vehicles, furniture, and certain building improvements. Section 179 lets you deduct up to $1,220,000 in qualifying asset costs in 2024. Bonus depreciation currently allows you to deduct 60% of eligible asset costs in the first year, with the percentage scheduled to phase down further in coming years.

Section 179 cannot create a net loss for your business, but bonus depreciation can, which makes the two tools useful in different situations depending on your income level.

How to calculate the deduction

Determine the full purchase price of each qualifying asset placed in service during the tax year. Apply Section 179 first up to its annual limit, then apply bonus depreciation to any remaining eligible cost. Use IRS Form 4562 to report all depreciation and amortization claims on your return.

Records to keep

- Purchase invoices and receipts for every asset you depreciate

- Documentation showing the date you placed the asset in service

- Records confirming the asset's business-use percentage

Red flags and common mistakes

The most common mistake is claiming 100% business use on a vehicle that you also drive personally. The IRS scrutinizes vehicle depreciation claims closely and requires you to reduce the deduction to match actual business-use percentage, supported by a mileage log.

Next steps if you want to maximize write-offs

Knowing the 13 deductions above is a solid start, but claiming them correctly and documenting them completely is what actually protects you if the IRS comes calling. Most small business owners leave money on the table not because they are unaware of write-offs, but because their records are incomplete or they miscalculate the business-use portion of mixed expenses.

Your next move is to get your recordkeeping in order before year-end, not after. Business tax deductions only hold up when you can support them with organized, itemized documentation that matches what you reported on your return. A qualified tax professional reviews your full situation, identifies every deduction you qualify for, and makes sure your filings are accurate and defensible under IRS scrutiny.

If you want to stop guessing and start keeping more of what you earn, schedule a free consultation with Tax Experts of OC to review your deductions with a CPA or Enrolled Agent who knows the rules inside out.