Choosing to structure your business as an S corporation can significantly reduce your overall tax burden, but only if you understand how the rules actually work. With S corporation taxes explained clearly, you can make informed decisions about distributions, salary requirements, and filing obligations that directly affect your bottom line. Too many business owners elect S corp status based on a tip they heard without grasping what it means for their personal income tax returns each year.

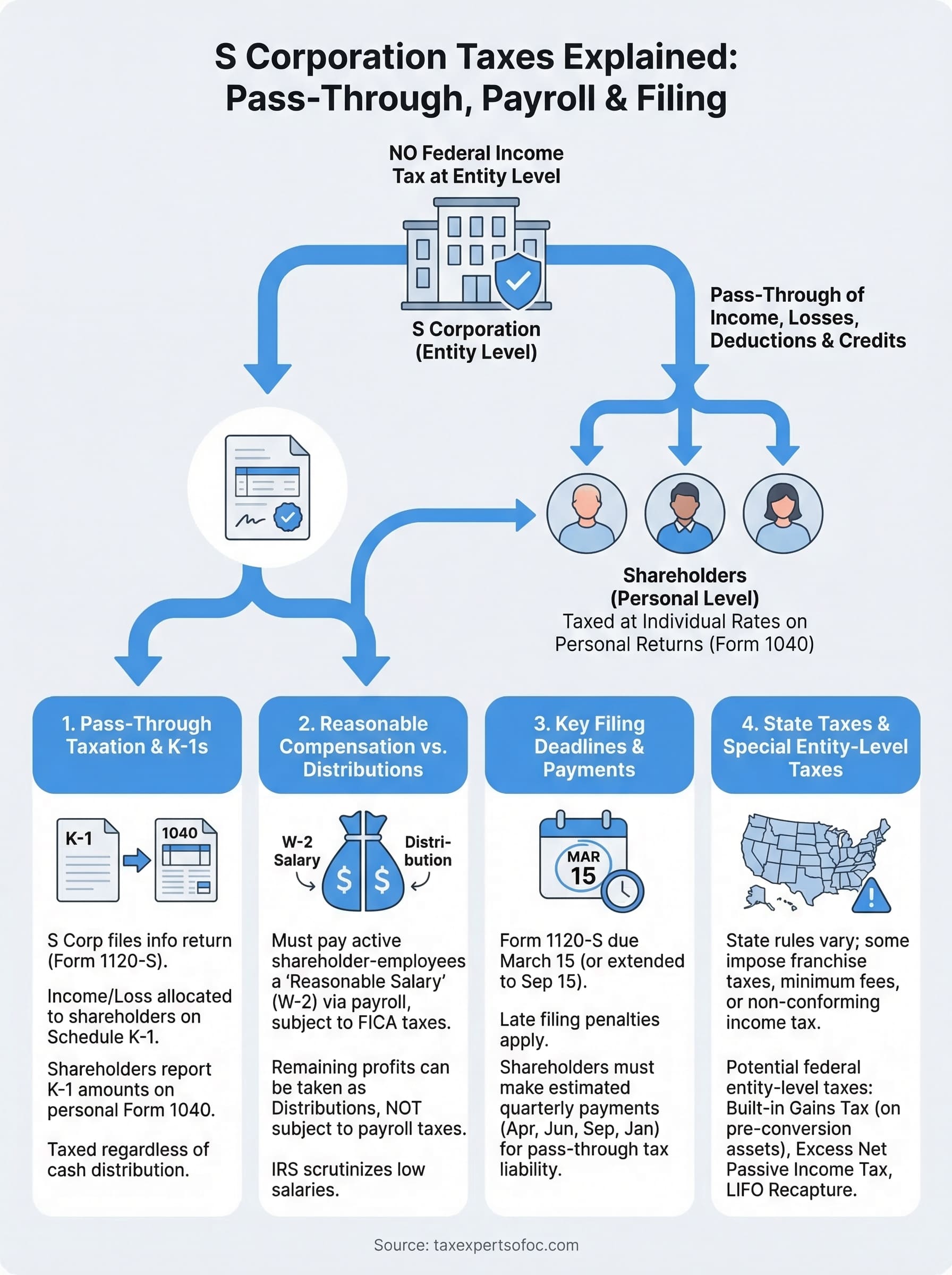

An S corporation doesn't pay federal income tax at the entity level. Instead, profits and losses pass through to shareholders, who report them on their individual returns. That pass-through structure creates real advantages, and real complexity. You're dealing with Form 1120-S, Schedule K-1s, reasonable compensation rules, and state-level requirements that vary depending on where you operate. Getting any of these wrong can trigger IRS scrutiny or cause you to overpay on taxes you could have legally avoided.

This guide breaks down how S corp taxation works from election to filing, including how it compares to C corp taxation, what pass-through means in practice, and where business owners commonly trip up. At Tax Experts of OC, our CPAs and Enrolled Agents help S corporation owners across all 50 states stay compliant and keep more of what they earn. Whether you're considering the S corp election or already filing as one, this article gives you the foundation to understand exactly what's happening with your taxes, and when to get professional help.

Why S corp taxes confuse business owners

S corp taxation sits in a gray zone that trips up even experienced business owners. Unlike a sole proprietorship or partnership, an S corp requires you to file a separate corporate return (Form 1120-S) each year. Unlike a C corporation, it doesn't pay tax at the entity level. That combination creates a structure that feels corporate in form but personal in effect, and understanding exactly where each obligation falls is where most of the confusion starts. Add in state-level rules, payroll tax requirements, and built-in IRS scrutiny, and you can see why so many owners get it wrong.

The gap between entity-level and personal taxes

Most business owners first encounter S corporation taxes explained through conversations about "pass-through" status, but that phrase doesn't tell the whole story. When your S corp earns $200,000 in profit, that income doesn't stay in the business for tax purposes. It flows through to your personal tax return via a Schedule K-1, whether you actually took the money out of the business or not. That distinction surprises many new S corp owners who assume they only owe taxes on cash they withdrew.

You owe tax on your allocated share of S corp income in the year it's earned, not in the year you actually receive the cash.

This creates a real cash flow problem if your S corp retains earnings for reinvestment. You might keep $150,000 inside the business to fund operations or equipment, then receive a K-1 showing that full $150,000 as taxable income on your personal return. Without proper planning around estimated quarterly payments, you face a surprise tax bill with no personal cash to cover it. Several specific issues contribute to this confusion:

- Tax year vs. cash flow misalignment: Income is taxable in the year the S corp earns it, not when you withdraw it.

- K-1 timing: You often receive your K-1 late in tax season, making it hard to plan personal payments in advance.

- Basis tracking: Your ability to deduct S corp losses depends on your stock and debt basis, a calculation many owners have never done.

- Phantom income: Retained earnings that you never touched can still show up as taxable income on your return.

The reasonable compensation requirement

The IRS requires you to pay yourself a reasonable salary if you work actively in your S corp. That salary runs through payroll and is subject to Social Security and Medicare taxes. Many owners try to keep their salary artificially low and pull the rest of their income as distributions, which are not subject to self-employment tax. The IRS actively scrutinizes this strategy, and if your compensation doesn't match what you'd pay a third party to perform your role, you risk having distributions reclassified as wages, with back payroll taxes, interest, and penalties added on top.

Determining what counts as "reasonable" depends on your industry, the hours you work, your specific duties, and comparable pay data for similar positions. There is no fixed formula, which means the judgment call falls on you and your tax professional. Getting this calculation wrong is one of the most audited issues in small business taxation, and the IRS has a long history of winning these cases when owner salaries look obviously structured to avoid payroll taxes rather than reflect real market compensation.

Multistate operations add another layer

If your S corp operates across state lines, your obligations multiply quickly. Each state where you have nexus, which generally means a taxable presence such as employees, inventory, or regular business activity, may require its own state return and potentially a state franchise fee or entity-level tax. Some states do not fully recognize the federal S corp election, which means you could owe corporate-level state income tax even while your income passes through federally.

California imposes a 1.5% franchise tax on S corp net income, with an $800 annual minimum regardless of whether your business turned a profit. If you recently expanded, hired remote workers in new states, or moved your residence while maintaining S corp activity elsewhere, your filing footprint may be larger than you realize. Multistate complexity is one of the clearest signs that managing your S corp taxes without professional guidance is a costly risk.

What an S corporation is for tax purposes

An S corporation is a legal business entity that has elected a special tax status with the IRS under Subchapter S of the Internal Revenue Code. From a legal standpoint, it operates like any other corporation: it issues stock, holds shareholders, follows corporate formalities, and provides liability protection to its owners. The tax treatment, however, is fundamentally different from a standard corporation, which is the entire reason most small business owners pursue the election in the first place.

The IRS requirements to qualify

Not every corporation can elect S corp status. The IRS sets specific eligibility rules that your business must meet before the election is valid, and maintaining compliance with these rules is an ongoing obligation, not a one-time check.

Your corporation must meet all of the following conditions to hold S corp status:

- Domestic corporation: Your business must be incorporated in the United States.

- Allowable shareholders only: Shareholders must be U.S. citizens or resident aliens, certain trusts, or estates. Partnerships, corporations, and non-resident aliens cannot hold shares.

- 100 shareholder maximum: You cannot have more than 100 shareholders at any one time.

- One class of stock: Your corporation can only issue one class of stock, though voting and non-voting shares are permitted.

- Eligible entity type: Certain financial institutions, insurance companies, and international sales corporations are not eligible for the election.

If your S corp violates any of these rules after the election takes effect, the IRS can terminate your S corp status, potentially backdating the termination and creating significant unexpected tax liability.

How S corps differ from C corps

With s corporation taxes explained in contrast to C corp treatment, the distinction becomes clearer. A C corporation pays federal income tax on its profits at the corporate level, currently at a flat 21% rate. When the C corp then distributes remaining profits to shareholders as dividends, those dividends get taxed again on the shareholder's personal return. This double taxation is the core disadvantage of C corp status for most small business owners.

An S corp sidesteps that problem entirely. No federal income tax applies at the entity level. Instead, every dollar of profit or loss allocated to you as a shareholder flows directly to your personal return and gets taxed only once. For a business generating consistent profits, that structural difference often translates into thousands of dollars in annual tax savings, which is why the S corp election remains one of the most widely used tax planning strategies for profitable small businesses in the country.

How pass-through taxation works for S corps

Pass-through taxation means the S corporation itself does not pay federal income tax. Every dollar of profit or loss the business generates in a given year flows through to the shareholders based on their ownership percentages. You then report that allocated income on your personal Form 1040, and the IRS taxes it there at your individual income tax rates. The business acts as a conduit rather than a separate taxable entity, which is the fundamental mechanism that makes the S corp election attractive for most small business owners.

How income flows from the S corp to your return

The S corp calculates its net income or net loss on Form 1120-S at the end of the tax year. The business then allocates that figure to each shareholder in proportion to their stock ownership. If you own 60% of the shares and the S corp earns $300,000, your allocated share is $180,000, regardless of how much cash you actually took out of the business during the year. That $180,000 appears on your Schedule K-1 and gets reported on your personal return.

You owe income tax on your allocated S corp profits even if the money stayed inside the business and you never touched it.

This is where s corporation taxes explained in simple terms becomes essential for new owners. The tax obligation follows the allocation, not the distribution. If the business retains earnings to purchase equipment, cover payroll, or build a cash reserve, those retained profits still appear on your K-1 as taxable income. Planning around this reality requires that you set aside enough personal cash each quarter to cover estimated taxes on income you may never have received in hand.

How losses pass through to your return

Pass-through treatment applies to losses as well as profits, but the IRS limits how much of an S corp loss you can actually deduct. Your deductible loss in any year is capped by your stock and debt basis, which is essentially your adjusted investment in the business. If your basis is $40,000 and your allocated loss is $60,000, you can only deduct $40,000 this year. The remaining $20,000 carries forward until you restore enough basis to absorb it.

Basis increases when you contribute capital or lend money directly to the S corp, and it decreases when you take distributions or receive loss allocations. Tracking basis accurately every single year is not optional. Failing to maintain proper records means you could either miss legitimate deductions or accidentally claim losses that trigger an IRS adjustment.

How owners pay themselves: salary vs distributions

One of the most tax-sensitive decisions you make as an S corp owner is how to split your income between a W-2 salary and shareholder distributions. Salary payments run through payroll and are subject to Social Security and Medicare taxes, which combine to 15.3% up to the Social Security wage base. Distributions, on the other hand, are not subject to payroll taxes. That gap creates a strong incentive to pay yourself less in salary and more in distributions, but the IRS anticipates exactly that move and requires you to pay yourself a reasonable salary before taking any distributions at all.

What counts as reasonable compensation

The IRS does not define a specific dollar amount for reasonable compensation. Instead, it expects your salary to reflect what you would pay a third party to perform the same services in your role. If you skip the salary analysis and just pick a number that minimizes payroll taxes, you are taking on significant audit risk. The IRS has successfully reclassified distributions as wages in court cases where owner salaries were clearly structured to avoid payroll taxes rather than reflect real market rates.

Several factors determine what the IRS considers reasonable for your situation:

- Industry and role: What comparable professionals in your field earn for performing similar duties

- Hours worked: The time you actively spend in the business each week

- Business revenue: Larger, more profitable businesses typically support higher salaries

- Training and experience: Your qualifications and the specialized value you bring to the role

- Geographic market: Compensation rates vary significantly by region

Setting your salary too low is one of the most scrutinized issues in S corp taxation, and the IRS wins these cases more often than business owners expect.

How distributions work and why they save you money

Once you pay yourself a reasonable and documented salary, any remaining profits you pull out of the S corp come as shareholder distributions. These distributions are not subject to payroll taxes, which is where the core tax advantage of the S corp structure actually lives. With s corporation taxes explained this way, you can see why a profitable business generating income well above the owner's market-rate salary can produce real annual savings compared to operating as a sole proprietor, where all net earnings face self-employment tax.

Distributions require your shareholder basis to support them. If your basis drops below zero, the IRS treats excess distributions as capital gains, which creates a separate taxable event you need to track and plan around every year to avoid surprises at filing time.

What Form 1120-S and K-1s report

Every S corporation files Form 1120-S with the IRS each year, and that return is the foundation of how S corp income gets reported and distributed to shareholders. With s corporation taxes explained at the entity level, Form 1120-S acts as an informational return: it tells the IRS what the business earned, what it spent, and how those results break down across shareholders. The IRS does not assess tax on the S corp itself based on this return, but the document drives what every shareholder ultimately reports on their personal return.

What Form 1120-S covers

Form 1120-S reports the S corporation's total income, deductions, credits, and other tax items for the year. The return includes the company's gross receipts, cost of goods sold, officer compensation, rent, depreciation, and any other business deductions. It also contains Schedules B, K, K-1, L, M-1, and M-2, which together document shareholder information, balance sheet data, and reconciliation between book income and taxable income.

The IRS uses Form 1120-S primarily to verify that shareholders are reporting their allocated shares of income correctly on their individual returns.

One section business owners frequently overlook is Schedule K on the main return, which aggregates the total pass-through items before the S corp splits them among shareholders. Schedule K shows income, deductions, credits, and separately stated items such as capital gains, rental activity, and charitable contributions, each of which flows to shareholders as a distinct line item rather than a single lump-sum profit figure.

How Schedule K-1 works for shareholders

Each shareholder receives a separate Schedule K-1 that breaks out their individual share of every item from Schedule K. If the S corp has three shareholders owning 50%, 30%, and 20% respectively, each receives a K-1 reflecting their exact proportional slice of every income or deduction category the business reported. You take those K-1 figures and enter them directly on your personal Form 1040, typically through Schedule E.

Your K-1 will report the following categories separately, because the IRS treats each differently at the individual level:

- Ordinary business income or loss: Your share of regular operating profits or losses

- Net rental real estate income or loss: If the S corp holds rental property

- Interest, dividends, and capital gains: Investment-type income allocated to you

- Section 179 deductions: Immediate expensing of qualifying assets

- Credits: Business credits passed through to reduce your personal tax liability

Receiving your K-1 late in the filing season is common, since the S corp return is due March 15, and many businesses file on extension. If you file your personal return before receiving your K-1, you risk filing an inaccurate return that requires an amendment later.

Key deadlines and penalty traps

S corporation filing deadlines differ from personal return deadlines in ways that catch many owners off guard. With s corporation taxes explained fully, you need to understand that the IRS holds S corps to a separate calendar from individual filers, and the penalties for missing key dates compound quickly if you are not prepared going into each tax year.

The March 15 filing deadline

Form 1120-S is due on March 15, which is one month earlier than the April 15 deadline for individual returns. This earlier date exists specifically so that shareholders can receive their K-1s in time to complete their personal returns. If you miss the March 15 deadline without filing for an extension, the IRS charges a late-filing penalty of $235 per shareholder per month, up to a maximum of 12 months. For a multi-shareholder S corp, those penalties stack fast.

Missing the March 15 deadline by even one day triggers per-shareholder penalties that can easily exceed what you would have paid a professional to file on time.

The late-filing penalty for Form 1120-S applies even though the S corp owes no federal income tax at the entity level. Many owners assume no tax owed means no penalty exposure, but the IRS treats failure to file as its own separate violation, independent of any underlying tax liability.

Filing for an extension

You can request a six-month extension using Form 7004, which moves your deadline to September 15. Filing the extension is straightforward and gives your tax professional more time to prepare an accurate return. However, an extension to file is not an extension to pay. If your S corp owes any entity-level taxes, such as the built-in gains tax or excess net passive income tax, those amounts are still due on March 15.

Estimated tax payments for shareholders

Your S corp does not make estimated tax payments on your behalf for pass-through income. You are responsible for covering your personal tax liability on allocated S corp earnings through quarterly estimated payments due in April, June, September, and January. Skipping or underpaying those estimates leads to underpayment penalties on your personal return, even if you file and pay the balance in full by April 15. The penalty calculation uses the IRS underpayment rate and applies to each quarter individually, so waiting until year-end to catch up does not eliminate the exposure for earlier quarters.

Building a system to track your allocated income throughout the year and set aside funds quarterly is one of the most practical steps you can take to avoid penalties that have nothing to do with filing late.

Deductions and credits S corps commonly use

Your S corp can claim the same business deductions that any corporation can take, and those deductions directly reduce the net income that flows through to your personal return. With s corporation taxes explained at the deduction level, understanding what your business can legitimately write off is as important as understanding pass-through mechanics. Every dollar of deductible business expense lowers the taxable income your shareholders report, which makes capturing every available deduction a direct tax savings strategy.

Business deductions that reduce ordinary income

The most impactful deductions in most S corps fall into a few consistent categories. Your S corp can deduct officer compensation, which is the salary you pay yourself as a shareholder-employee, along with the employer's share of payroll taxes on that salary. Rent, utilities, insurance premiums, professional fees, advertising costs, and technology expenses are all deductible in the year incurred if they meet the ordinary and necessary standard the IRS applies to business expenses.

Depreciation and Section 179 expensing can let your S corp deduct the full cost of qualifying equipment in the year of purchase rather than spreading the deduction over several years.

Vehicles used for business purposes also generate deductions, though you must track actual business mileage and maintain documentation. The IRS requires a contemporaneous log showing the date, destination, business purpose, and miles driven. Claiming a vehicle deduction without that documentation is one of the most commonly disallowed expenses in small business audits.

Tax credits available to S corps

Credits reduce your tax bill dollar for dollar rather than simply reducing taxable income, which makes them more valuable per dollar than standard deductions. S corps can pass credits through to shareholders just like other tax items, and each credit type flows on its own line through Schedule K-1 so you apply it correctly on your personal return.

Some credits your S corp may qualify for include the following:

- Work Opportunity Tax Credit (WOTC): Available when you hire employees from specific targeted groups, including veterans and long-term unemployed individuals

- Research and Development Credit: Applies if your business conducts qualified research activities, even at a small scale

- Employer Credit for Paid Family and Medical Leave: Covers a percentage of wages paid to qualifying employees during leave

- Small Employer Health Insurance Credit: Available to S corps with fewer than 25 full-time employees that pay at least 50% of employee premium costs

Tracking which credits your business qualifies for requires ongoing attention throughout the year, not just a review at tax time. Decisions made in January, such as which employees you hire or what equipment you purchase, often determine credit eligibility that your tax professional calculates in March.

Special S corp taxes you might owe

S corporation taxes explained at the entity level would be incomplete without covering the situations where your S corp actually does owe federal tax directly. Most S corp owners know the business avoids corporate income tax, but three specific scenarios can trigger entity-level tax liability that catches unprepared owners off guard. Knowing these rules in advance lets you plan around them rather than absorbing a surprise bill at filing time.

The built-in gains tax

If your business converted from a C corporation to an S corp, the IRS imposes a built-in gains (BIG) tax on any appreciated assets your company held at the time of conversion. The recognition period for this tax is five years following the S corp election date. If you sell or otherwise dispose of a converted asset within that window and it carried appreciated value on the conversion date, the S corp owes corporate-level tax on that gain at the highest corporate rate, currently 21%.

If you converted from a C corp and are considering selling assets or the entire business, confirming whether you are still inside the five-year recognition period is a critical step before closing any deal.

This tax applies to assets like real estate, equipment, and intellectual property that had a fair market value exceeding their tax basis on the day the S corp election took effect. Your tax professional should document the built-in gain exposure at the time of conversion so you know exactly what liability sits on your books going forward.

Excess net passive income tax

Your S corp owes an excess net passive income (ENPI) tax if two conditions are both true: the corporation carries accumulated earnings and profits from prior C corp years, and more than 25% of your gross receipts consist of passive income such as rent, royalties, interest, or dividends. When both thresholds are met, the IRS taxes the excess passive income at the corporate rate directly at the S corp level, separate from your personal tax obligation on the same income flowing through your K-1.

LIFO recapture tax

The third entity-level tax applies specifically to former C corporations that used the LIFO inventory method before converting to S corp status. The IRS requires the company to recognize the difference between LIFO and FIFO inventory values as taxable income in the final C corp year. That LIFO recapture amount is taxed at the corporate rate and paid in installments over four years following the conversion. This rule prevents businesses from benefiting from the C corp LIFO deduction and then escaping corporate tax on that benefit by switching to S corp status.

State and local taxes: S corp rules vary

Federal pass-through treatment applies nationwide, but state tax treatment of S corporations is not uniform. Each state sets its own rules about whether it recognizes the federal S corp election, what filing requirements apply, and whether it imposes any entity-level taxes on the business itself. With s corporation taxes explained at the federal level, you still need to account for the state layer separately, because ignoring it can produce unexpected tax bills that wipe out the savings you planned for.

States that don't conform to federal S corp treatment

Some states require you to file a separate conformity election to receive pass-through treatment at the state level, even after the IRS has accepted your federal S corp status. New Hampshire and Tennessee historically taxed business income at the entity level under their own rules, and several other states impose their own conditions for recognizing the election. If your state does not conform and you never filed a state-level election, your business may owe corporate-level state income tax on the same profits that already passed through to your personal state return, effectively taxing the same income twice.

If you moved to a new state, expanded operations into another state, or hired remote employees in states where you don't currently file, your S corp's state tax footprint may already be larger than you realize.

You should review the following situations to determine whether you have unresolved state filing obligations:

- New nexus triggers: Hiring employees, storing inventory, or regularly performing services in a state typically creates a taxable presence requiring a state return

- Partial-year residency: If you relocated during the year, you may owe income tax in both your prior and current states on your K-1 income

- Non-resident shareholders: Shareholders living in different states from where the S corp operates often face filing requirements in the state where the business is located

Franchise taxes, minimum fees, and composite returns

Even states that fully recognize the federal S corp election often impose entity-level fees or franchise taxes that the business itself pays. California charges a 1.5% franchise tax on net income with an $800 annual minimum, which applies regardless of whether your S corp turned a profit for the year. New York City imposes a separate corporate tax on S corps operating within city limits. These fees are not eliminated by the pass-through structure, and they apply in addition to the income tax you pay on your K-1 income personally.

Many states also allow or require composite returns for non-resident shareholders. A composite return lets the S corp file and pay state income tax on behalf of out-of-state shareholders who would otherwise need to file individual non-resident returns in every state where the business operates. Understanding whether your state offers this option can simplify compliance significantly if your S corp has shareholders spread across multiple states.

Next steps if you run an S corp

With s corporation taxes explained from election through entity-level exceptions, you now have a complete picture of what running an S corp actually costs and requires each year. The rules around pass-through income, reasonable compensation, basis tracking, and state filings are not areas where guesswork serves you well. One missed deadline, an underdocumented salary decision, or an overlooked state filing can create penalties and back taxes that far exceed what professional help would have cost upfront.

Your next step is a direct conversation with a CPA or Enrolled Agent who works with S corps regularly. Reviewing your current salary structure, verifying your basis calculations, and confirming your state filing obligations are practical tasks that produce measurable results. If you want professional help from a firm that handles S corp clients across all 50 states, schedule a free consultation with Tax Experts of OC to get started.