If you've recently started a company, or you're thinking about it, one of the first questions you'll face is what is business tax and how much of it applies to you. The answer isn't as simple as a single payment to the IRS once a year. Depending on your entity type, revenue, and whether you have employees, you could owe several different types of taxes, each with its own rules and deadlines.

Business taxes generally fall into categories like income tax, self-employment tax, employment (payroll) tax, and excise tax. Which ones you're responsible for depends largely on how your business is structured, a sole proprietorship has different obligations than an S corporation or LLC. Getting this wrong, or missing a filing, can lead to penalties that add up fast.

At Tax Experts of OC, we help business owners across all 50 states sort through these obligations with the guidance of a CPA and Enrolled Agent. Whether you're filing your first return or cleaning up years of missed deadlines, understanding the tax basics is the starting point. This guide breaks down each major type of business tax, explains how your entity structure affects what you owe, and gives you a clear picture of what to expect when tax season comes around.

Why business tax matters

Understanding what is business tax isn't just an academic exercise. The IRS and state tax agencies expect you to know which taxes apply to your business, file on time, and pay accurately. When you skip a filing or underestimate what you owe, the consequences hit your business directly: interest, penalties, and sometimes collection actions that can disrupt your operations or put your personal assets at risk.

The cost of getting it wrong

Missing tax deadlines or misclassifying your obligations triggers penalties that compound quickly. The IRS charges a failure-to-file penalty of 5% of the unpaid tax per month, up to 25%. On top of that, a separate failure-to-pay penalty applies at 0.5% per month. If you have employees and fall behind on payroll tax deposits, the Trust Fund Recovery Penalty can make you personally liable for those unpaid amounts, even if your business is a corporation or LLC.

The Trust Fund Recovery Penalty is one of the few situations where the IRS can pierce your business structure and come after you personally.

These costs are avoidable with the right setup and a consistent filing schedule. Waiting until a problem surfaces almost always makes the resolution more expensive than getting ahead of it.

How taxes shape your financial planning

Your tax obligations directly affect your cash flow throughout the year, not just in April. Many business taxes require quarterly estimated payments, and payroll taxes are due on a schedule tied to your payroll size. If you don't plan for these payments in advance, you can find yourself short when the due date arrives.

Building accurate tax projections into your budget gives you a clearer picture of your true profit margins and helps you make better decisions around hiring, spending, and growth.

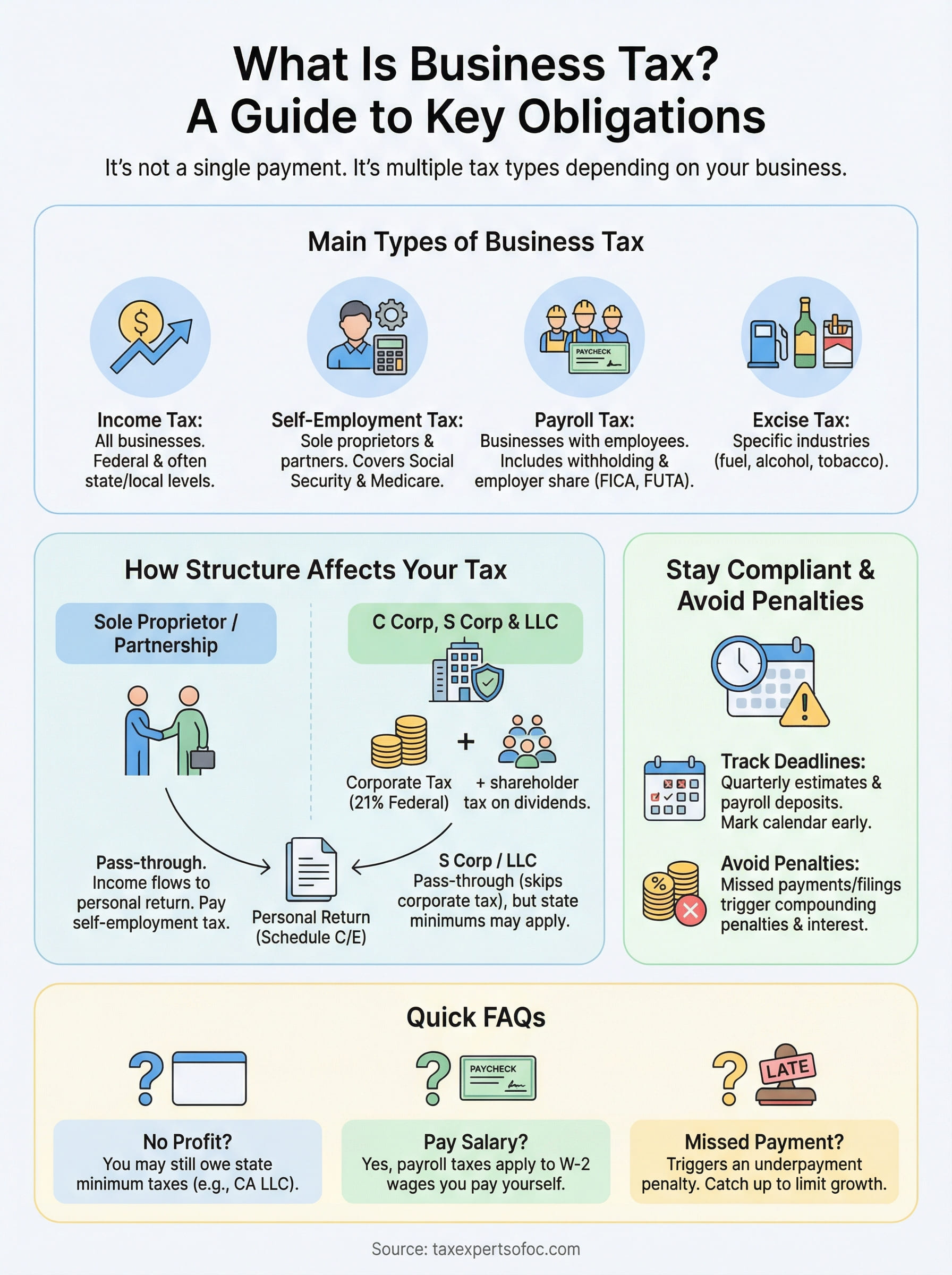

Types of business taxes in the US

When you ask what is business tax, the answer covers several distinct obligations rather than one single annual payment. Federal law requires most businesses to manage at least two or three different tax categories, and state and local requirements add more obligations on top of those.

Federal taxes you'll likely owe

The four main federal business taxes are income tax, self-employment tax, employment (payroll) tax, and excise tax. Which of these apply to you depends on your business structure, whether you have employees, and the specific industry you operate in.

| Tax Type | Who Pays It |

|---|---|

| Income tax | All businesses |

| Self-employment tax | Sole proprietors, partners |

| Payroll tax | Businesses with employees |

| Excise tax | Specific industries (fuel, alcohol, tobacco) |

If you have employees, payroll tax alone involves multiple components: Social Security, Medicare, and federal unemployment (FUTA).

State and local taxes

Beyond federal obligations, most states impose their own income or franchise taxes on businesses operating within their borders. Some cities and counties add local business taxes on top of those. California businesses, for example, owe a state franchise tax minimum each year regardless of profitability, which means your total tax picture includes both federal and state layers.

How business structure affects taxes

One of the most practical answers to what is business tax is this: your entity type shapes your entire filing process. The IRS treats sole proprietors, partnerships, and corporations through different rules, so your structure determines which forms you file, which taxes you owe, and when payments are due.

Sole proprietors and partnerships

If you operate as a sole proprietor or partner, your business income flows directly onto your personal return. You report profits on Schedule C or Schedule E and pay self-employment tax on top of income tax, covering both the employer and employee sides of Social Security and Medicare.

This pass-through treatment means your profits get taxed at your individual rate, not a separate corporate rate.

Corporations and LLCs

C corporations pay income tax at the corporate level at a flat 21% federal rate, and shareholders pay again on dividends. S corporations and LLCs with pass-through elections skip that double layer by pushing income to owners' personal returns. Choosing the wrong structure can cost you more than you expect each year.

Picking the right structure early prevents overpayment down the road. A tax professional can review whether an entity change makes sense for your current income level.

How to stay compliant and avoid penalties

Once you understand what is business tax and which obligations apply to your entity, the next step is building habits that keep you current with the IRS. Missing a deadline or underestimating a payment is rarely a one-time problem; it tends to compound into larger balances with interest and penalties that take time and money to resolve.

Track your filing deadlines

The IRS publishes a tax calendar for businesses that lists every major due date by form type. Quarterly estimated payments are typically due in April, June, September, and January, and payroll tax deposits follow a separate schedule based on your payroll size. Knowing these dates well in advance lets you set aside funds before the bill arrives.

Marking deadlines at least two weeks early and setting calendar reminders gives you time to gather records without rushing at the last minute.

Work with a qualified tax professional

A CPA or Enrolled Agent can review your full obligations at the start of each year and flag any changes in tax law that affect your situation. Proactive planning almost always costs less than resolving an IRS penalty notice after the fact.

FAQs and quick examples

Understanding what is business tax gets clearer with concrete examples. These frequently asked questions cover the situations most business owners run into when they first start filing.

What if my business made no profit this year?

Even with zero profit, you may still owe taxes. If you're a sole proprietor with a net loss, you typically don't owe income tax, but S corporations and California LLCs must still pay the state minimum franchise tax of $800 regardless of profitability.

Owing taxes despite no profit surprises many first-year business owners, especially those operating in California.

Do I owe taxes if I pay myself a salary?

Yes. If your business pays you a W-2 salary, payroll taxes apply to those wages. Your business withholds Social Security and Medicare on your behalf and matches those amounts as the employer.

What happens if I miss a quarterly payment?

Missing a quarterly estimated payment triggers an underpayment penalty from the IRS. The penalty is calculated based on the amount owed and how late the payment was. Catching up quickly limits how much that penalty grows before your annual return is due.

Next Steps

Now that you understand what is business tax and how it applies based on your entity type, the practical move is to confirm which obligations are active for your business right now. Income tax, payroll tax, and quarterly estimated payments all run on different schedules, and getting clarity on each one prevents the kind of missed deadlines that turn into IRS penalty notices.

Building a consistent filing routine starts with knowing your due dates and setting aside funds before each one arrives. If your situation involves back taxes, unfiled returns, or an IRS notice you haven't addressed, the sooner you get professional help, the less it typically costs to resolve.

At Tax Experts of OC, a CPA and Enrolled Agent review your full tax picture and help you stay current going forward. Schedule a free 30-minute consultation with our business tax resolution and accounting team today.