Real estate can be one of the most tax-advantaged asset classes available, but only if you know how to use the rules in your favor. Without a clear strategy, investors leave thousands of dollars on the table every year through missed deductions, poorly timed sales, and overlooked deferral opportunities. That's exactly why tax planning for real estate investors isn't optional. It's the difference between building wealth and just breaking even.

Whether you own a single rental property or manage a growing portfolio, the tax code offers powerful tools, depreciation, 1031 exchanges, cost segregation, pass-through deductions, that can dramatically reduce what you owe. But these strategies come with strict rules, tight deadlines, and real consequences if you get them wrong. Knowing what's available in 2026 is only half the equation. You need to know how to apply it to your specific situation.

At Tax Experts of OC, our CPAs and Enrolled Agents work directly with real estate investors across all 50 states to structure their holdings, maximize deductions, and stay ahead of IRS requirements. We built this guide to give you a complete, actionable breakdown of the strategies that matter most right now, from depreciation methods and capital gains deferral to entity structuring and quarterly planning. If you're serious about keeping more of what your properties earn, this is where you start.

Why tax planning matters for real estate investors

Real estate investing creates multiple taxable events at once: rental income, depreciation recapture, and capital gains each require a different approach. Without a deliberate plan, you're likely overpaying on income you don't need to, missing deductions you're entitled to claim, and stumbling into tax bills that could have been deferred or reduced. Tax planning for real estate investors isn't about finding loopholes. It's about understanding how the tax code treats your income and structuring your activity to take full advantage of rules that already exist.

The cost of skipping a tax strategy

When you don't plan proactively, the IRS defaults to the most straightforward interpretation of your income, which is rarely the most favorable one for you. Rental income gets taxed as ordinary income unless you actively classify and manage your activity correctly. Depreciation goes unclaimed when properties aren't properly analyzed at acquisition. Repairs get capitalized instead of expensed because no one documented them correctly at the time. Each mistake compounds year over year, and by the time you realize the gap, you may owe back taxes, penalties, and interest on top of the original liability.

Reactive tax management also puts you in a position where you're always catching up. You sell a property without planning the exit, and suddenly you're facing a large capital gains bill with no offset strategy in place. You form an LLC without understanding how it gets taxed, and you miss the pass-through deduction you qualified for. Real estate rewards investors who plan ahead, not those who sort out the paperwork after the fact.

How timing changes what you owe

Many of the most powerful tax strategies available to you are entirely time-dependent. A 1031 exchange has a 45-day identification window and a 180-day closing deadline from the sale date. Miss those windows and you lose the deferral completely. Cost segregation studies need to be coordinated at or shortly after acquisition to maximize first-year bonus depreciation. Quarterly estimated payments need to reflect your actual income, or you face underpayment penalties regardless of how accurately you file at year end.

The decisions you make at acquisition, mid-year, and at exit each carry real tax consequences, and you rarely get a second chance to apply the right strategy retroactively.

Your property type, holding period, and participation level also affect which rules apply to you. Short-term rentals are taxed differently than long-term ones. Real estate professionals who qualify under IRS rules can offset unlimited passive losses against ordinary income, while everyone else faces strict caps. Getting classification right from the start is what separates investors who build wealth efficiently from those who hand a large portion of their returns back to the IRS.

Why 2026 changes the stakes

Several provisions from the Tax Cuts and Jobs Act were set to expire after 2025, and their status heading into 2026 directly affects real estate investors. While Congress has addressed some extensions, the rules around bonus depreciation rates, pass-through deduction thresholds, and individual income tax brackets have all shifted or remain uncertain. Acting now, while you still have clarity on the current rules, gives you the best position to lock in available benefits. Key items to track include:

- Section 199A pass-through deduction: The 20% deduction for qualified business income affects how rental income flows through LLCs and partnerships

- Bonus depreciation: Phase-out rules continue to reduce the percentage available each year without new legislation

- Individual tax brackets: Potential rate increases for higher earners make income timing strategies more valuable than in prior years

Waiting to see what happens before you act is itself a tax decision, and often not a favorable one.

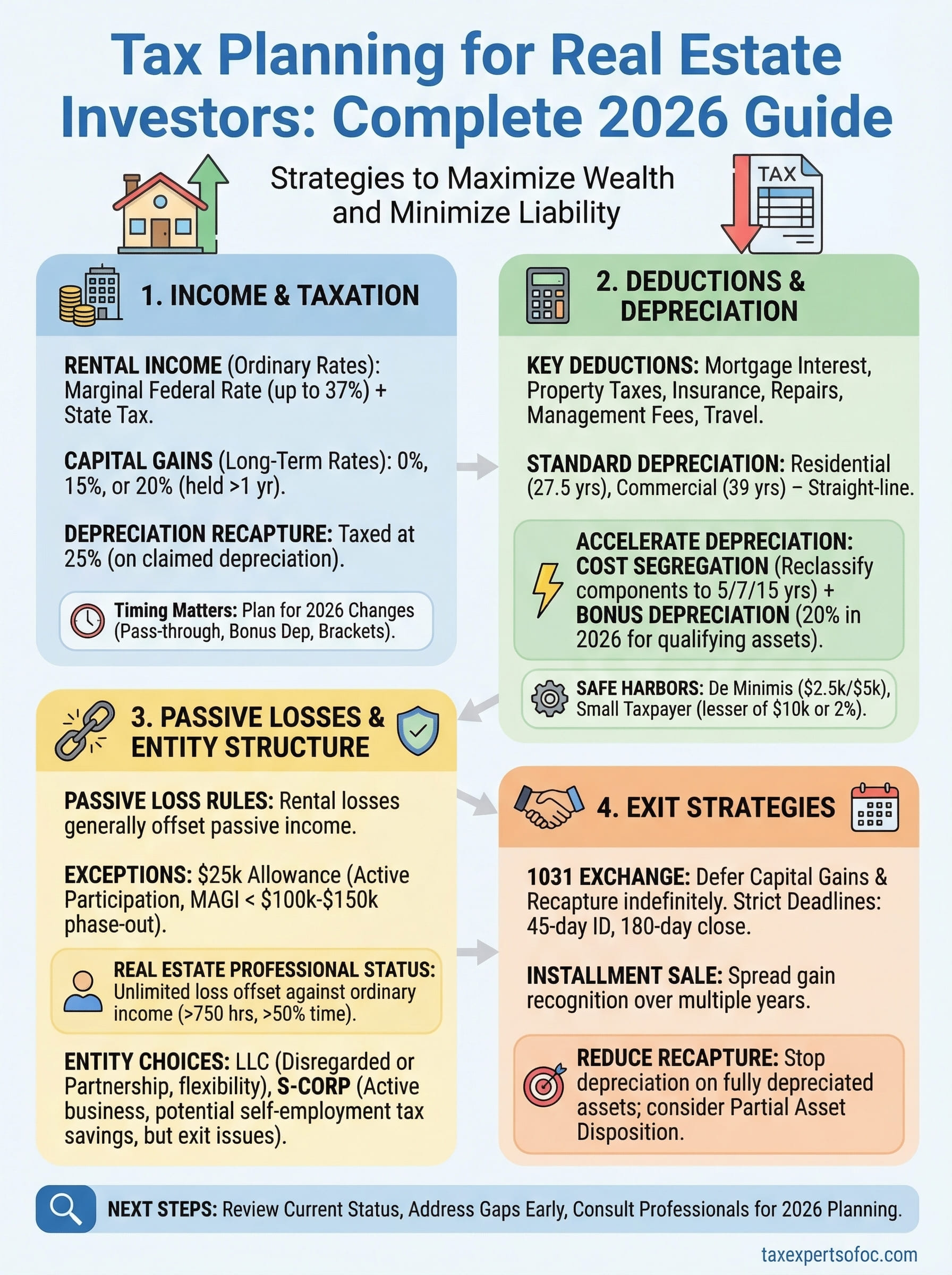

How real estate income gets taxed

Real estate income doesn't fit into a single tax category, and that's exactly why tax planning for real estate investors requires understanding how different income types are treated separately. The IRS distinguishes between rental income, capital gains, and depreciation recapture, and each one carries different rates, rules, and timing implications. Getting these categories straight is the foundation of every strategy covered in this guide.

Rental income and ordinary income rates

Rental income you collect from tenants is treated as ordinary income by default. That means it gets stacked on top of your other earnings and taxed at your marginal federal rate, which can reach 37% for high earners. Rental income doesn't receive any preferential rate treatment on its own, which is exactly why deductions against it carry so much weight in any real estate tax strategy.

Your state also taxes rental income, and rates vary significantly by location. California, for example, taxes ordinary income at rates up to 13.3%, while states like Florida and Texas impose no state income tax at all. If you own properties in multiple states, you may need to file separate returns in each one and carefully track which income is sourced to which jurisdiction to avoid overpaying or filing incorrectly.

Capital gains and depreciation recapture

When you sell a property, the profit splits into two distinct components: capital gain on appreciation and depreciation recapture. The capital gain portion is taxed at long-term rates if you held the property for more than one year, currently 0%, 15%, or 20% depending on your taxable income. That's a meaningful advantage over ordinary income rates and one of the primary reasons long-term holds are more tax-efficient than short-term flips.

Depreciation recapture is the piece most investors underestimate, and it adds a 25% tax on the portion of your gain that corresponds to depreciation you claimed while you held the property.

The recapture amount depends entirely on how much depreciation you took over the holding period, not on how much the property appreciated in value. This is why exit strategies like 1031 exchanges and installment sales become so important when you plan a sale. Understanding what you'll owe before you close is a core part of protecting your returns as an investor.

How to set up clean books and documentation

Clean documentation is the foundation of every successful tax strategy. Without accurate records, depreciation claims fall apart, deductions get disallowed, and you're left relying on memory during an audit. Effective tax planning for real estate investors starts long before you file anything. It starts with the systems you put in place the day you acquire a property.

Separate your finances from day one

The first step is opening a dedicated bank account and credit card for each property or, at minimum, for your real estate activity as a whole. Mixing personal and business transactions is the fastest way to lose deductions. When an expense sits inside a combined account, you have to reconstruct what was business-related and what wasn't, and that reconstruction rarely holds up under IRS scrutiny. A clean separation makes tax preparation faster, reduces errors, and gives you a defensible record from the start.

If you ever face an audit, the IRS will ask for transaction-level records, and "I think I spent that on the rental" is not documentation.

Track every transaction with the right labels

Once your accounts are separate, you need a system that categorizes income and expenses consistently throughout the year. Basic accounting software works well for most investors. The key is labeling transactions correctly at the time they happen, not six months later when you're trying to reconstruct everything for your tax preparer. Tag each expense by property and expense category, such as repairs, insurance, or management fees, so your year-end reports are already organized when you need them.

Rental income should also be logged by property with the tenant's name and payment date. This matters because gross rents, security deposits, and late fees are treated differently under tax rules, and your records need to reflect which type of payment you received and when.

Keep documentation that survives an audit

For each deductible expense, hold onto the receipt, invoice, or bank statement that connects the amount back to a specific property and date. For repairs especially, a written description of what broke, what was done, and why it qualifies as a repair rather than a capital improvement gives you a complete audit trail. Store digital copies in a dedicated folder organized by property and tax year, and retain them for at least seven years from the date you file.

How to claim rental deductions the right way

Rental deductions are one of the most direct ways to reduce what you owe, but claiming them incorrectly triggers audits and disallowed expenses. Tax planning for real estate investors depends on knowing not just which deductions exist, but how to substantiate and apply them correctly based on your property type, ownership structure, and level of activity.

The deductions most investors miss

The obvious deductions, mortgage interest, property taxes, and insurance, get claimed routinely. The ones that get missed are the ones that require more documentation. Property management fees, advertising costs, professional services like accounting and legal fees, and mileage driven to inspect or maintain a property are all deductible and often overlooked. If you use a portion of your home exclusively for managing your rental business, you may also qualify for a home office deduction tied to that activity.

Travel costs to visit out-of-state properties are another area where investors leave money on the table. You can deduct airfare, lodging, and transportation expenses tied directly to rental property management, provided you document the business purpose of each trip. Keep a simple log with dates, destinations, and the reason for each visit, and attach it to your receipts at year end.

What you can and cannot deduct in the same year

Not every cost related to your rental property is immediately deductible. Ordinary operating expenses like repairs, supplies, utilities paid by the landlord, and professional fees are deductible in the year you pay them. Capital improvements, however, must be depreciated over time rather than expensed upfront, which is a distinction the IRS takes seriously.

Misclassifying an improvement as a repair is one of the most common audit triggers for rental property owners, so getting this right before you file protects you from costly corrections later.

The IRS also requires that deductions connect directly to a property you hold for rental purposes. Expenses tied to personal use periods of a vacation rental, for example, are not deductible at full value. If a property has both personal and rental use during the year, you need to allocate expenses by the number of days each use type occurred, which requires accurate tracking throughout the year rather than a reconstruction at tax time.

How depreciation works for rental property

Depreciation is one of the most valuable tax tools available to rental property owners. The IRS lets you deduct the cost of a residential rental property over 27.5 years and commercial property over 39 years, even while the property's market value may actually be increasing. This non-cash deduction reduces your taxable rental income each year without requiring you to spend any additional money, which is why it sits at the center of effective tax planning for real estate investors.

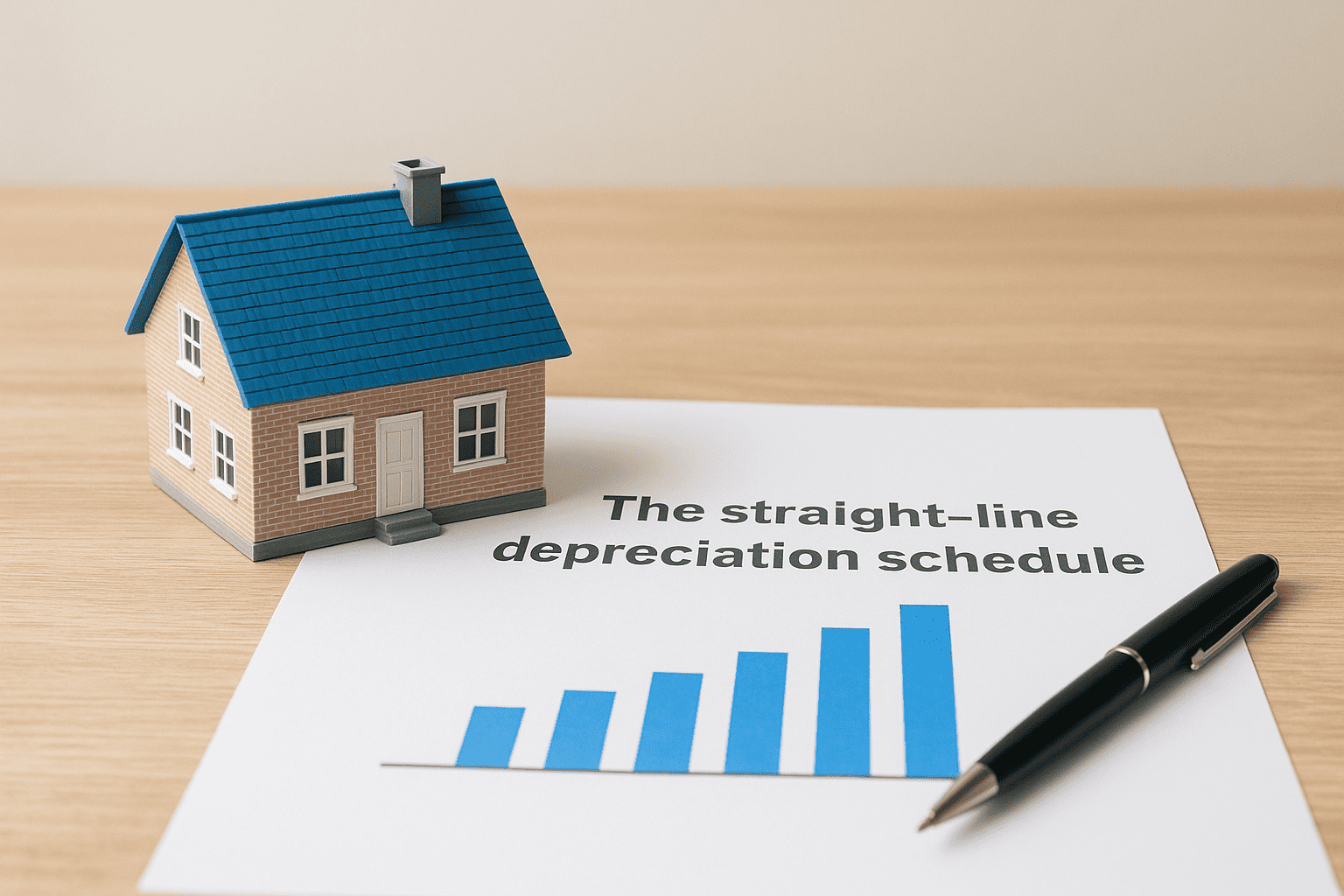

The straight-line depreciation schedule

The standard depreciation method for rental property is straight-line depreciation, which spreads the cost evenly across the recovery period. For a residential rental, you divide the depreciable basis by 27.5 to get your annual deduction. If your depreciable basis is $275,000, for example, you claim $10,000 per year in depreciation regardless of how much rent the property generates or what you paid in expenses.

Land is never depreciable, so you must allocate your purchase price between the land and the building before you calculate your annual deduction.

Your depreciation starts the month you place the property in service, meaning it's available for tenants to occupy, not necessarily the month a tenant moves in. If you placed the property in service in October, you claim depreciation for only three months in that first tax year rather than the full twelve.

How your depreciation basis gets calculated

The depreciable basis starts with the purchase price of the property, but it doesn't stop there. You also add in closing costs, legal fees, and capitalized improvements made before the property was placed in service. Items like title insurance, recording fees, and transfer taxes paid at closing are includable in your basis and increase the annual deduction you're entitled to claim.

Improvements made after the property is already in service get added to your basis and depreciated separately over their own recovery periods. A new roof, for example, is depreciated over 27.5 years starting from the month you complete the work. Tracking each improvement separately from the original purchase basis is essential because it affects both your annual deduction and your gain calculation when you eventually sell.

How cost segregation and bonus depreciation work in 2026

Standard depreciation spreads your deduction across 27.5 or 39 years, which is slow. Cost segregation and bonus depreciation are two strategies you can use together to accelerate that timeline significantly, pulling forward deductions that would otherwise trickle in over decades. Understanding how they interact in 2026 is a core part of practical tax planning for real estate investors who want to maximize first-year deductions.

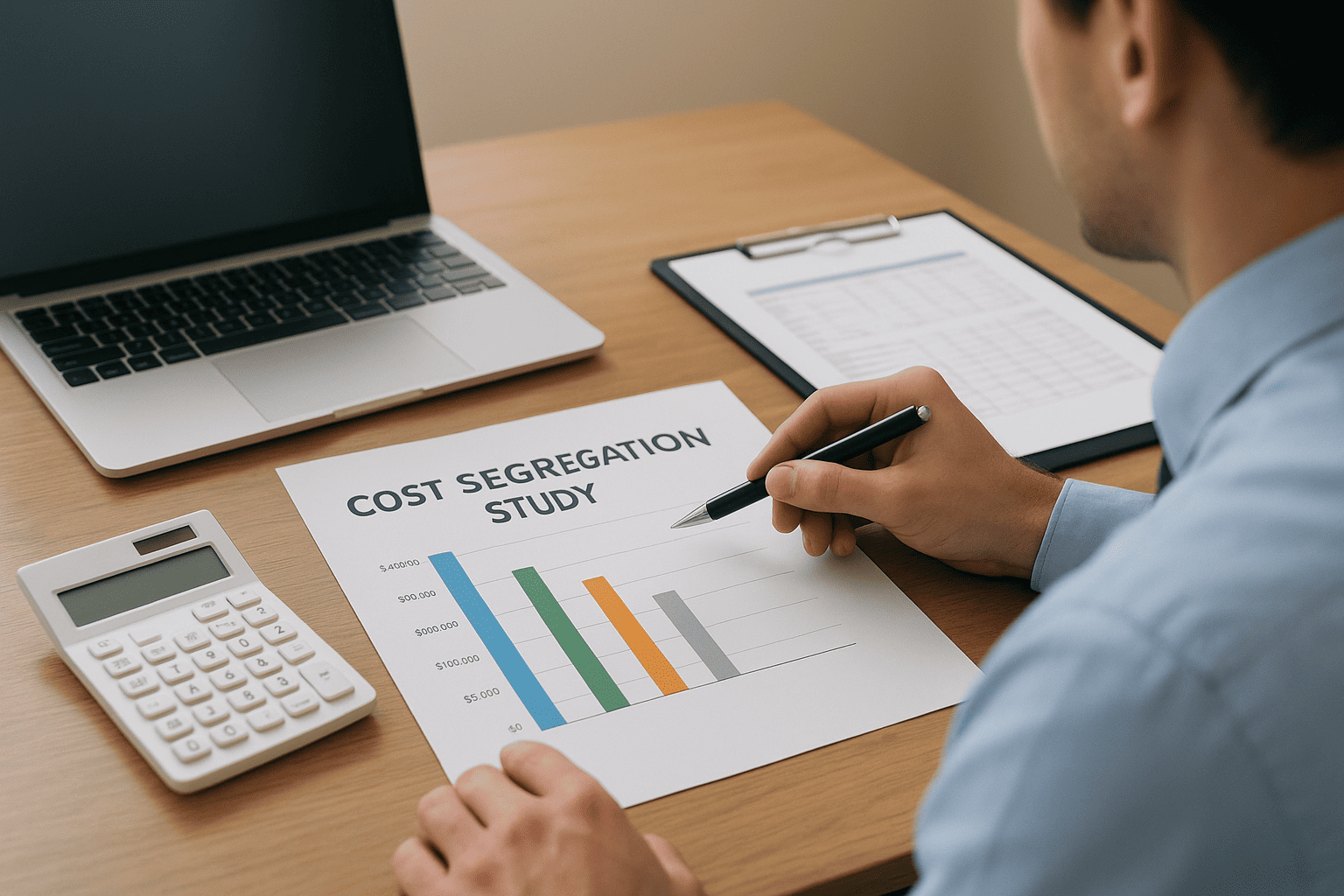

What cost segregation does for your depreciation schedule

A cost segregation study is an engineering-based analysis that breaks a property into its individual components and assigns each one the correct depreciation period under IRS guidelines. Instead of depreciating everything at the 27.5-year or 39-year rate, components like flooring, lighting, land improvements, and certain fixtures get reclassified into 5-year, 7-year, or 15-year categories. That reclassification alone accelerates a meaningful portion of your total depreciation into the early years of ownership.

A cost segregation study on a $1 million commercial property can realistically reclassify 20% to 40% of the building's cost into shorter-life categories, generating substantial deductions in the first few years rather than spreading them over nearly four decades.

The study is performed by a qualified engineer or tax professional, typically at acquisition or shortly after. Retroactive studies are also available if you've owned a property for years without one, and you can catch up on missed deductions without amending prior returns by using a catch-up provision under IRS rules.

How bonus depreciation applies in 2026

Bonus depreciation lets you deduct a percentage of qualifying assets immediately in the year they're placed in service rather than over their standard recovery period. When you combine a cost segregation study with bonus depreciation, the components reclassified into 5-year and 15-year categories become eligible for that accelerated write-off.

For property placed in service in 2026, the bonus depreciation rate sits at 20% under the phase-down schedule established by the Tax Cuts and Jobs Act. That's down significantly from the 100% rate that applied through 2022, but it still produces a real first-year benefit on the qualifying portion of a large acquisition. Without new legislation extending or restoring higher rates, the 20% rate is what you have to work with right now, which makes timing new acquisitions carefully an important part of your planning.

How to handle repairs vs improvements and safe harbors

The difference between a repair and a capital improvement determines whether you deduct the cost this year or spread it across decades. Getting this classification wrong is one of the most common and costly mistakes in tax planning for real estate investors. The IRS uses a specific set of rules called the tangible property regulations to draw this line, and understanding them before you spend money on your property protects your deductions and keeps you out of trouble.

The distinction that determines when you can deduct

A repair restores a property to its existing working condition without adding significant value or extending its useful life. Patching a broken window, fixing a leaking faucet, or repainting a unit after a tenant moves out all qualify as repairs. You deduct these costs in full in the year you pay them. An improvement, by contrast, betters, restores, or adapts the property to a new or different use, and the IRS requires you to capitalize it and depreciate it over its recovery period.

The key test the IRS applies is whether the work restored the property to a like-new condition or simply kept it functioning as it was before the problem occurred.

The distinction isn't always obvious. Replacing a broken water heater is typically a repair. Replacing the entire HVAC system across all units upgrades the property and must be capitalized. When you're unsure, document what failed, what you did, and why the work was necessary, and consult your tax professional before you file.

The safe harbor rules that protect your deductions

The IRS provides safe harbors that give you a defined threshold below which you can expense items without a detailed analysis. The de minimis safe harbor lets you deduct amounts up to $2,500 per item or invoice if you have no applicable financial statement, provided you have a written accounting policy in place at the start of the tax year. For taxpayers with audited financial statements, that limit rises to $5,000 per item.

The small taxpayer safe harbor covers landlords with gross receipts under $10 million who own buildings with an unadjusted basis under $1 million. Under this rule, you can expense annual repairs and improvements up to the lesser of $10,000 or 2% of the building's unadjusted basis without capitalizing anything. Set up your written accounting policies before January 1 each year to make sure these safe harbors apply to every qualifying expense you pay throughout the year.

How passive loss rules work and how to use losses

Rental activity is classified as passive income by default under IRS rules, which means losses from your rental properties can only offset other passive income, not your wages, business income, or investment returns. If your deductions and depreciation exceed your rental income in a given year, that excess loss doesn't disappear. It gets suspended and carried forward to future years, where it can offset passive income or be released entirely when you sell the property. Understanding where you fall within these rules is one of the most important parts of tax planning for real estate investors because it determines how much your losses are actually worth to you right now.

The $25,000 allowance for active participants

The IRS provides a limited exception for taxpayers who actively participate in managing their rental properties. If your modified adjusted gross income falls below $100,000, you can deduct up to $25,000 in rental losses against non-passive income each year. That allowance phases out dollar for dollar between $100,000 and $150,000 in income, and it disappears entirely above that threshold.

Active participation is a lower bar than most investors realize. You don't need to manage the property yourself. You simply need to make management decisions, such as approving tenants and setting rents, even if you use a property manager to handle day-to-day tasks.

If your income puts you above the phase-out range, the $25,000 allowance won't help you. Your losses will suspend and accumulate until you either generate passive income to absorb them or sell the property and release them all at once.

How real estate professionals unlock unlimited losses

The real estate professional status under IRS rules is the most powerful tool available for high-income investors who want to use rental losses without restriction. To qualify, you must spend more than 750 hours per year on real estate activities, and those hours must represent more than half of your total working time across all occupations.

If you meet both tests, your rental activity is no longer treated as passive, and your losses offset ordinary income with no cap. Married couples filing jointly can use one spouse's qualification to unlock this benefit for the entire household's rental portfolio. You must keep detailed time logs throughout the year to support the hour count if the IRS ever questions your status.

How to reduce capital gains and recapture on exit

Every sale triggers a tax bill, but how large that bill is depends almost entirely on the planning you do before you close. Tax planning for real estate investors treats the exit as a separate discipline, not an afterthought. The strategies below let you defer, reduce, or spread what you owe, but each one requires action well before the sale date.

How a 1031 exchange defers your tax bill

A 1031 exchange lets you sell a property and roll the entire proceeds into a like-kind replacement without recognizing gain at the time of sale. You defer both the capital gains tax and the depreciation recapture until you eventually sell the replacement property, and if you repeat the exchange at each subsequent sale, you can defer those taxes indefinitely.

The deadlines are strict: you have 45 days from closing to identify a replacement property and 180 days to complete the purchase, with no extensions for most situations.

You must use a qualified intermediary to hold the proceeds between transactions. You cannot touch the funds yourself without triggering immediate recognition of the entire gain. Start identifying your replacement property before you list your current one so you're not scrambling against the 45-day clock after you close.

How installment sales spread the tax over time

If a 1031 exchange doesn't fit your situation, an installment sale lets you collect the purchase price in payments over multiple years rather than all at once. You recognize gain only as you receive each payment, which spreads your tax liability across several tax years instead of concentrating it in one.

This strategy works best when spreading the gain across years keeps you out of a higher capital gains bracket or reduces the Medicare surtax exposure that hits at certain income thresholds. Structure the payment schedule carefully with your tax professional, because the allocation between principal, interest, and gain affects your tax in each year you receive a payment.

How to reduce depreciation recapture before you sell

Depreciation recapture is taxed at 25% regardless of your capital gains rate, so reducing the recaptured amount directly reduces your bill. One approach is to stop claiming depreciation on components that have been fully depreciated, which happens naturally over time with cost-segregated assets. Another approach is a partial asset disposition election, which lets you write off the remaining basis of a replaced component rather than carrying it alongside the new improvement.

How to choose the right entity and ownership structure

The way you hold your real estate investments directly affects how your income gets taxed, how your losses flow through, and how much self-employment tax you owe. Effective tax planning for real estate investors includes evaluating your entity structure at acquisition, not after you've already built equity inside the wrong one. Restructuring later triggers its own tax consequences, so starting with the right setup protects both your current returns and your future exit options.

How LLCs are taxed by default

A single-member LLC is treated as a disregarded entity by the IRS, meaning the income and expenses flow directly onto your personal return as if the LLC didn't exist. A multi-member LLC is taxed as a partnership by default, filing Form 1065 and issuing K-1s to each member. Neither classification adds complexity at the federal level on its own, and both preserve your access to the Section 199A pass-through deduction on qualified rental income, subject to income thresholds and property type.

The LLC structure gives you flexibility in how income gets allocated among members, which matters significantly when multiple investors hold a single property together.

One tax consequence that catches investors off guard inside a partnership is guaranteed payments and special allocations, which must be handled correctly to avoid mismatches between what a partner receives and what they owe at tax time. Review the operating agreement with a CPA before you sign it, not after your first year of distributions.

When an S-corp or other structure changes your tax bill

An S-corp election generally makes more sense for active real estate businesses like property management companies or flipping operations than for passive rental portfolios. If you operate a short-term rental that qualifies as a business rather than a passive activity, the S-corp can reduce self-employment tax by splitting income between a reasonable salary and a distribution, where only the salary portion carries payroll tax obligations.

Holding long-term rentals inside an S-corp creates problems on exit. S-corps don't qualify for Section 1231 treatment the same way an individual or partnership does in all scenarios, and they add payroll requirements that increase your compliance burden without providing proportional benefit for passive activity. Match your entity type to your actual activity level and exit timeline, and revisit the structure whenever your portfolio changes significantly.

Next steps

Tax planning for real estate investors covers a lot of ground: depreciation schedules, passive loss rules, exit strategies, entity structure, and documentation systems that hold up under scrutiny. No single strategy works in isolation. The investors who keep the most of what their properties earn are the ones who connect these pieces into a coordinated, year-round plan rather than a once-a-year filing exercise.

Your first move is to assess where you stand right now. Review your current entity structure, check whether you've claimed depreciation correctly since acquisition, and identify any upcoming sales that need an exit strategy before you close. The earlier you address gaps, the more options you have to fix them without triggering unnecessary tax bills.

If you want a qualified CPA or Enrolled Agent to review your situation directly, schedule a free consultation with Tax Experts of OC and get clear, specific guidance built around your actual portfolio.