Most people only think about taxes when it's time to file. By then, the biggest opportunities to reduce what you owe have already passed. That's exactly the gap that tax planning services for individuals are designed to close, helping you make smarter financial moves before year-end, not after. The difference between reacting to a tax bill and preparing for one ahead of time can be thousands of dollars.

But not all tax planning looks the same, and not every provider offers the same level of expertise. Some firms hand you off to seasonal staff. Others rely on software-driven shortcuts. At Tax Experts of OC, our CPA and Enrolled Agent work directly with clients across all 50 states to build tax strategies grounded in each person's actual financial picture, not generic advice pulled from a template. Whether you're managing investment income, self-employment taxes, or multi-state filings, you deserve a plan that fits your situation, not someone else's.

This article breaks down what individual tax planning services actually include, how to evaluate whether a provider is qualified, and what you should expect from the process from start to finish.

Why tax planning matters for individuals

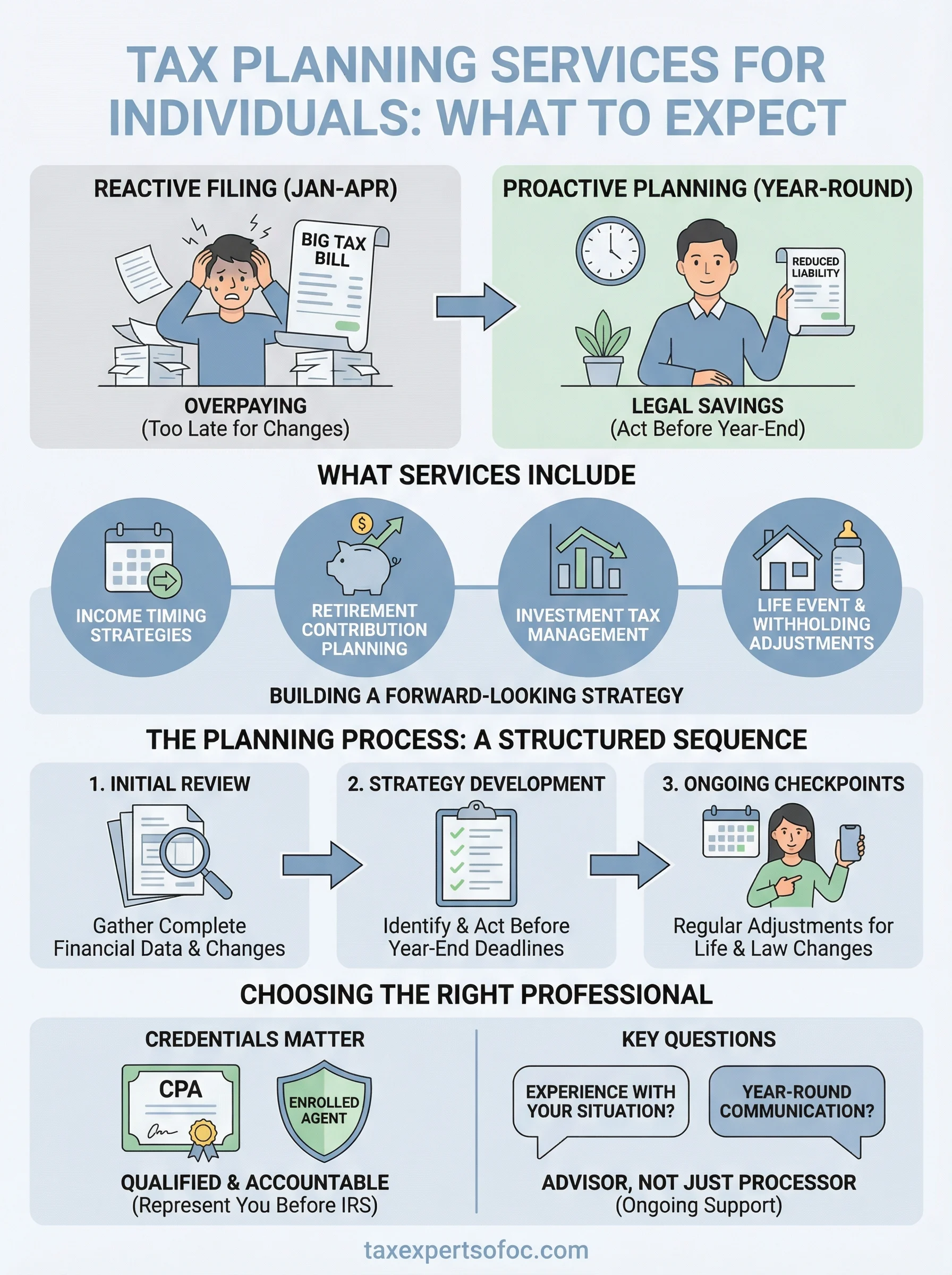

Most people treat taxes as a once-a-year task. You gather documents, hand them to a preparer, and hope the number on the return isn't too painful. That approach leaves real money on the table because preparers working in March and April can only report what already happened. They cannot undo decisions you made the prior year that increased your taxable income. Reactive filing is not a strategy, and for most people, it means consistently overpaying.

The difference between tax preparation and tax planning is direct: one records what happened, the other shapes what will happen.

When the tax code works in your favor

The U.S. tax code includes dozens of provisions specifically designed to reduce what individual taxpayers owe, including deductions, credits, retirement contribution limits, and capital gains treatment rules. But these provisions come with strict deadlines. If you miss them, no amount of skilled filing can recover the benefit. Some of the most commonly missed opportunities include:

- Maxing out retirement accounts before year-end contribution cutoffs

- Harvesting capital losses before December 31 to offset gains

- Timing deductible expenses across tax years to maximize itemization

- Adjusting withholding mid-year to avoid underpayment penalties

What proactive planning actually changes

Tax planning services for individuals shift the work earlier in the year, giving you and your advisor time to act on strategies while they are still available. If your income is trending higher, a planner can identify whether adjusting withholding, accelerating deductions, or restructuring payments makes financial sense for your specific situation.

Small adjustments made in June or September can lower your effective tax rate in ways that are simply not possible at filing time. Over several years, those incremental changes compound into savings that a standard return cannot generate on its own.

What tax planning services include

Tax planning services for individuals cover far more than reviewing last year's return. A qualified advisor looks at your full financial picture, including income sources, deductions, investments, and major life changes, to build a forward-looking strategy that reduces your tax liability over time.

The goal is not just to file accurately; it is to structure your finances so that you legally owe less before you ever reach filing day.

Core areas your advisor addresses

A tax planning engagement typically touches several interconnected areas, depending on your situation:

- Income timing strategies: shifting income or deductions between tax years to stay in a lower bracket

- Retirement contribution planning: identifying which accounts to fund and how much based on your current income

- Investment tax management: coordinating capital gains, losses, and dividend income to reduce your overall tax burden

- Withholding and estimated tax adjustments: correcting over- or underpayment before penalties accumulate

- Life event planning: accounting for major changes like marriage, a home purchase, or a new business

Your advisor should revisit each of these areas regularly, not just once at year-end, since your income and circumstances shift throughout the year.

How the tax planning process works

Tax planning services for individuals follow a structured sequence rather than a single meeting. Understanding that sequence helps you know what to prepare and what to expect from your advisor at each stage.

Initial financial review

Your advisor starts by gathering a complete picture of your finances, including income sources, existing deductions, investment activity, and any significant changes from the prior year. This review is the foundation everything else builds on. Without accurate data at this stage, the strategies that follow will not reflect your actual situation.

The quality of your tax plan depends directly on the completeness of the information you bring to that first conversation.

Strategy development and ongoing checkpoints

Once your advisor understands your financial position, they identify specific actions you can take to reduce your tax liability before year-end. These typically include contribution adjustments, income timing decisions, and withholding corrections. Your advisor then schedules follow-up checkpoints throughout the year to account for income changes, life events, or new tax law developments. Tax planning is not a one-time exercise. It is an active process that requires revisiting your situation as circumstances shift, ensuring the strategy stays aligned with your goals.

How much tax planning costs and what affects price

Tax planning services for individuals typically range from $300 to $2,500 or more per year, depending on the complexity of your finances and the credentials of the professional you hire. A straightforward engagement with a single income source and no investments costs far less than one involving rental properties, stock portfolios, and multi-state income. Knowing what drives pricing helps you budget accurately and avoid surprises.

What you pay for tax planning is almost always less than what you lose by skipping it.

What drives the cost up or down

Your financial complexity is the single largest factor in what you pay. A self-employed individual with business income, depreciation schedules, and estimated tax payments requires significantly more time than a salaried employee with one W-2. The professional's credentials also matter. A CPA or Enrolled Agent charges more than a seasonal preparer, but that difference reflects the depth of knowledge and legal standing they bring to your situation.

Other factors that affect your final cost include:

- Number of income sources and investment accounts

- Multi-state filing requirements

- Frequency of check-ins throughout the year

- Whether bookkeeping or payroll services are bundled in

How to choose the right tax professional

Choosing the right professional for tax planning services for individuals comes down to two things: credentials and communication. A CPA or Enrolled Agent has passed rigorous licensing requirements and can legally represent you before the IRS, which a general preparer cannot. Before you commit, verify their credentials through official channels and confirm they have direct experience with your specific financial situation.

A credential tells you what a professional is qualified to do; their communication style tells you whether they will actually do it for you.

Questions to ask before hiring

Not every qualified professional is the right fit for your goals. Ask directly how many individual clients they work with year-round and whether they offer mid-year check-ins or only engage at filing time. You want someone who functions as an ongoing advisor, not just a document processor.

Before hiring anyone, get clear answers to these questions:

- Do they specialize in situations like yours, such as self-employment, multi-state income, or investment portfolios?

- How do they structure their planning process beyond the filing deadline?

- What does client communication look like throughout the year?

Firms that offer a free initial consultation give you a low-risk way to assess fit before you commit financially.

Your next step

Tax planning is not a task you complete once and forget. Every year your income, expenses, and financial goals shift, and your strategy needs to keep pace with those changes. Waiting until April to think about taxes means accepting a bill that proactive planning could have reduced significantly.

If you are ready to take control of your tax situation, Tax Experts of OC works directly with individuals across all 50 states to build personalized strategies that go well beyond standard filing. Our CPA and Enrolled Agent handle everything from income timing and retirement contributions to multi-state filings and IRS representation. Tax planning services for individuals work best when the process starts early, giving your advisor enough time to identify every opportunity before deadlines close them off. The best time to act is now, not in April. Schedule your free 30-minute consultation and find out exactly what a proactive tax plan can do for your bottom line.