The difference between a high-net-worth individual who pays what they owe and one who overpays often comes down to one thing: tax planning for high net worth individuals that's proactive rather than reactive. With shifting tax brackets, evolving IRS enforcement priorities, and potential legislative changes on the horizon for 2026, the cost of winging it has never been higher. A single overlooked strategy can mean six or seven figures left on the table.

Yet most high-net-worth taxpayers don't have a tax plan, they have a tax preparer. There's a significant gap between filing a return and building a strategy that protects wealth across income types, entities, and generations. Closing that gap requires working with professionals who understand the full picture, not just the forms. At Tax Experts of OC, our CPAs and Enrolled Agents work directly with clients, nationwide, to identify and execute these kinds of strategies before December 31st, not after.

This article breaks down seven specific tax planning moves that high-net-worth individuals should evaluate in 2026. Some are foundational, others are aggressive, but each one is grounded in current tax law and designed to reduce what you owe legally. Whether you're managing a portfolio, running a business, or doing both, these are the moves worth discussing with your tax advisor before your next filing deadline.

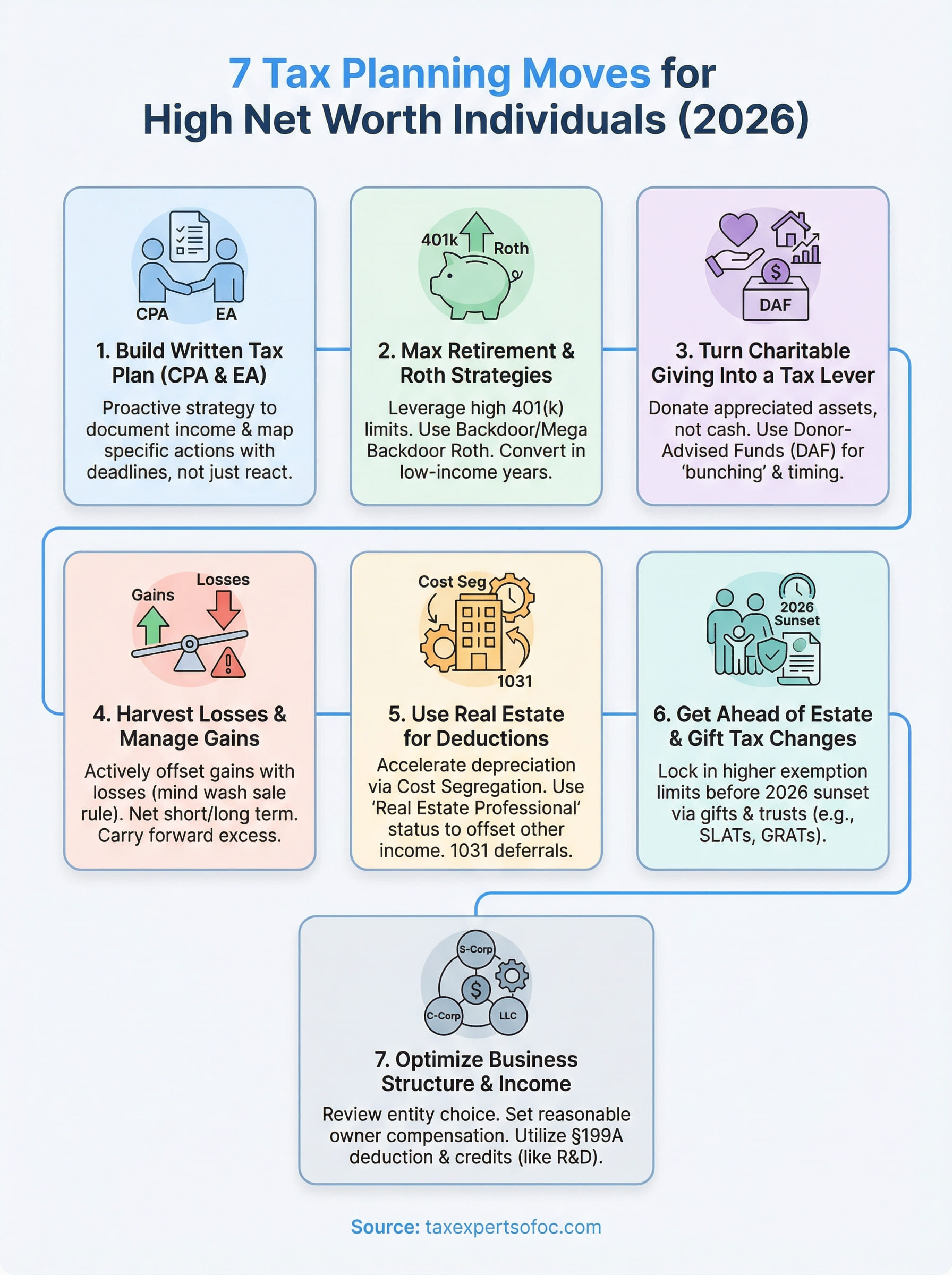

1. Build a written 2026 tax plan with a CPA and EA

A written tax plan gives you something most wealthy taxpayers lack: a documented strategy that connects your income, investments, and entities to specific actions with deadlines. Without one, you make tax decisions in isolation, and that's where expensive mistakes happen. Partnering with both a CPA and an Enrolled Agent (EA) combines accounting expertise with IRS representation authority, giving your plan technical depth and a clear line of defense if your positions are ever challenged.

What to cover in a high-net-worth tax plan

Your written plan should account for all income sources including wages, pass-through income, dividends, capital gains, and rental income, and map each one to applicable deductions and deferral strategies. It also needs to address your entity structure, estate exposure, and any planned liquidity events such as a business sale or large stock option exercise. At minimum, document the following:

- Estimated income by category for 2026

- Projected tax liability under your current approach

- Specific reduction strategies with dollar-range estimates

- Action items, responsible parties, and completion deadlines

How proactive planning differs from tax prep

Tax preparation looks backward. Your CPA takes what happened and places it into the correct forms. Proactive tax planning for high net worth individuals looks forward, identifying opportunities to shift income, time deductions, and restructure holdings before transactions close. Once a year-end passes, most of those options are gone permanently.

The IRS doesn't reward good intentions. Strategies only reduce your tax bill if you execute them before the deadline, not just discuss them.

Questions to ask before you implement strategies

Before acting on any strategy, ask your advisor how it interacts with your other income and deductions, whether it creates passive loss limitations, and what happens if your income shifts significantly before December 31st. You should also clarify documentation requirements and whether the strategy triggers any elections or separate filings beyond the main return itself.

Records and numbers to bring to the first planning meeting

Walk into your first planning meeting with your prior year's full tax return, current-year income projections by source, and a list of planned transactions for the rest of 2026. Include brokerage statements, K-1s received to date, and details on any real estate you own or plan to acquire. The more complete your financial picture, the more specific and actionable your plan becomes.

2. Max out retirement and use Roth strategies

Retirement accounts remain one of the most reliable tools in tax planning for high net worth individuals. The right combination of pre-tax, after-tax, and Roth contributions can dramatically reduce your current-year liability while building tax-efficient wealth for the future.

401k and profit-sharing limits that matter in 2026

In 2026, the 401(k) elective deferral limit sits at $23,500, with a $7,500 catch-up contribution for those 50 and older. If you own a business, profit-sharing contributions can push the total to $70,000 per participant, making this one of the largest single-year deductions available to you.

Backdoor Roth and mega backdoor Roth basics

High earners phase out of direct Roth IRA contributions, but the backdoor Roth, which is a nondeductible traditional IRA contribution followed by a conversion, remains available. If your plan allows after-tax contributions, the mega backdoor Roth lets you convert up to the full 415 limit minus employer contributions into Roth funds.

Confirm your 401(k) plan document explicitly allows in-plan Roth conversions before attempting the mega backdoor strategy.

When Roth conversions make sense for high earners

Conversions work best when your current-year income is temporarily lower than normal, such as in a year with large deductible losses or business write-downs. Converting in those windows locks in a lower effective rate on the converted amount permanently.

Mistakes that trigger unexpected taxes

The pro-rata rule catches many taxpayers who hold pre-tax IRA balances when attempting a backdoor Roth, treating a portion of the conversion as taxable income. Watch for net investment income surtax exposure and confirm your modified adjusted gross income before executing any conversion.

3. Turn charitable giving into a tax lever

Charitable giving is one of the most flexible tools in tax planning for high net worth individuals, but only if you structure gifts correctly. Most high earners donate cash, which is the least efficient method available. Shifting how and when you give can produce a meaningful reduction in your taxable income without changing how much you give in total.

Donate appreciated assets instead of cash

When you donate long-term appreciated stock or real estate directly to a qualified charity, you avoid paying capital gains tax on the appreciation while still deducting the full fair market value. This double benefit makes appreciated asset donations significantly more valuable than writing a check for the same amount.

Use a donor-advised fund for timing and bunching

A donor-advised fund (DAF) lets you contribute a large amount in one tax year to capture a big deduction, then distribute grants to charities over multiple years. Bunching two or three years of planned giving into a single DAF contribution lets you clear the standard deduction threshold and itemize when it counts most.

Contribute to your DAF before December 31st to claim the deduction in the current tax year, even if you don't designate recipient charities until later.

Coordinate gifts with a high-income year or liquidity event

If you're selling a business or exercising stock options, time your largest contributions to offset the income spike in that same year. Pairing a significant DAF contribution or direct asset gift with a liquidity event can neutralize a substantial portion of the resulting tax bill.

Substantiation rules and valuation pitfalls

The IRS requires written acknowledgment from the charity for any cash donation of $250 or more, and non-cash gifts over $500 require Form 8283. Donations of property valued above $5,000 generally need a qualified appraisal, and overvaluation is one of the most reliable ways to draw IRS scrutiny.

4. Harvest losses and manage capital gains on purpose

Managing gains and losses intentionally is a core part of tax planning for high net worth individuals with large brokerage positions. Rather than letting market movement dictate your tax bill, you can actively control your net gain exposure through deliberate decisions about what to sell and when.

Tax-loss harvesting and the wash sale rule

Tax-loss harvesting means selling positions at a loss to offset realized gains elsewhere in your portfolio. The IRS wash sale rule blocks you from repurchasing the same or substantially identical security within 30 days before or after the sale, so plan your reinvestment carefully to preserve the deduction.

Buying a similar but not identical fund immediately after a sale lets you maintain market exposure while keeping the harvested loss intact.

Netting rules for short-term vs long-term gains

The IRS requires you to net short-term losses against short-term gains first, then long-term losses against long-term gains. Since short-term gains are taxed at ordinary income rates, offsetting them first delivers the highest after-tax benefit for most high earners. Apply losses in the order that eliminates your highest-rate exposure first.

How to carry losses forward and use the $3,000 rule

When net capital losses exceed your gains, you can deduct up to $3,000 against ordinary income per year. Any remaining balance carries forward indefinitely, making a large harvested loss in a high-gain year a durable multi-year tax asset worth tracking.

Year-end checklist for brokerage accounts

Review your accounts each November and complete these steps before December 31st:

- Identify unrealized losses large enough to offset recognized gains

- Confirm estimated tax payments are current on all gains already realized

- Verify no wash sale violations are pending from purchases in the prior 30 days

5. Use real estate to create deductible losses and deferrals

Real estate offers some of the most powerful deduction tools available in tax planning for high net worth individuals. When structured correctly, property ownership can generate paper losses that offset real income, turning appreciation into a deduction engine rather than a tax liability.

Depreciation basics and what cost segregation changes

Standard depreciation spreads a residential property's cost over 27.5 years and commercial property over 39. Cost segregation accelerates this by reclassifying components like fixtures and land improvements into 5, 7, or 15-year schedules, front-loading large deductions into the early years of ownership.

Bonus depreciation phase-down considerations for 2026

Bonus depreciation allows immediate expensing of eligible assets identified through cost segregation. The rate has been phasing down from 100%, and 2026 planning must account for the current applicable percentage to accurately project your first-year deduction before it declines further.

Commission a cost segregation study before year-end if you acquired commercial or residential rental property in 2026.

Real estate professional and passive loss limits

The IRS classifies rental losses as passive by default, limiting deductibility against ordinary income unless you qualify as a real estate professional. To meet that status, you must spend more than 750 hours and more than half your total working time in real property trades or businesses, and you must document those hours carefully.

1031 exchanges and timing rules to plan around

A 1031 exchange lets you defer capital gains on the sale of investment property by reinvesting the proceeds into a like-kind replacement. You have 45 days to identify and 180 days to close on the replacement property, so start the process before you list the original asset.

6. Get ahead of 2026 estate and gift tax changes

The federal estate and gift tax exemption is currently elevated due to the Tax Cuts and Jobs Act, but that window may close in 2026 if Congress does not act. For high-net-worth families, this moment represents both a deadline and an opportunity to transfer wealth under rules that may not hold much longer.

Why the exemption sunset matters in 2026

The TCJA roughly doubled the estate and gift tax exemption, but the provision was set to expire. If no extension passes, the exemption reverts to roughly half its current level, adjusted for inflation. Gifts made before the sunset lock in that higher threshold permanently, according to IRS anti-clawback guidance.

Act on large transfers before December 31st if the current exemption aligns with your estate plan.

Annual exclusion gifting and intrafamily loans

Each year, you can give up to $19,000 per recipient in 2026 without touching your lifetime exemption. For married couples, gift-splitting pushes that to $38,000 per recipient. Intrafamily loans structured at the IRS Applicable Federal Rate let you transfer economic value at below-market rates without triggering gift tax.

Trust options to discuss with counsel

Irrevocable trusts like SLATs, GRATs, and IDGTs let you shift assets out of your taxable estate while preserving some benefit or control. Work with estate counsel alongside your CPA to match the right structure to your specific income and asset profile before year-end.

How to coordinate estate planning with income tax planning

Effective tax planning for high net worth individuals requires treating estate and income tax as a single integrated system. Shifting assets into trusts can affect your cost basis, passive loss calculations, and deduction eligibility, so confirm every estate move with your tax advisor before you execute it.

7. Optimize business income, payroll, and entity structure

If you own a business, your entity structure and compensation decisions directly affect your tax bill. Business owners control their taxable income in ways W-2 employees cannot, but that control only produces results when tax planning for high net worth individuals incorporates entity design from the start, not as an afterthought.

Choose the right entity for taxes and liability

S corporations, C corporations, and partnerships each carry different tax treatment for distributions, payroll obligations, and basis rules. Running the wrong structure can cost more than any single deduction you might claim. Review your entity election annually, especially when your income level or ownership composition has changed.

Reasonable compensation and payroll strategy for owners

The IRS requires S corporation owner-employees to pay a reasonable salary before taking distributions. Paying too little draws IRS scrutiny, and paying too much increases payroll tax exposure unnecessarily. Document a defensible compensation figure tied to your specific role and industry benchmarks before year-end.

Confirm your reasonable compensation calculation with your CPA each year to stay ahead of any IRS challenge.

Section 199A planning and deduction blockers

The qualified business income deduction under Section 199A can reduce pass-through income by up to 20%, but high earners face W-2 wage and capital limitations. Specified service businesses phase out of this deduction above income thresholds, so verify your eligibility before counting on it in your projections.

Deductions and credits high earners often miss

Section 179 expensing, R&D tax credits, and vehicle deductions are routinely overlooked by business owners regardless of income level. Review your full expense list with your advisor to surface deductible costs you have not been capturing, including software subscriptions, professional development, and documented home office use.

Next steps for 2026

The seven moves outlined here cover the core of tax planning for high net worth individuals, but reading about them and implementing them before December 31st are two different things. Every strategy on this list has a deadline, and most require documentation, professional coordination, or entity-level elections that take time to set up correctly.

Start by identifying the two or three strategies most relevant to your current income profile and planned transactions. Your biggest leverage points will depend on whether you own a business, hold appreciated assets, or face estate exposure that the 2026 exemption changes will affect. Bring a written list of those priorities to your first meeting with a qualified professional.

If you want a direct conversation with a CPA or Enrolled Agent who handles these exact issues, schedule your free 30-minute consultation with Tax Experts of OC and come prepared with your 2025 return and a clear summary of your planned 2026 transactions.