If you earned income as a freelancer, gig worker, or 1099 contractor this year, nobody withheld taxes from your paychecks. That means the full responsibility of calculating, filing, and paying independent contractor taxes falls on you, and the IRS expects you to stay on top of it throughout the year, not just in April.

Getting it wrong can lead to underpayment penalties, surprise tax bills, or worse, a growing balance with the IRS that triggers collections activity. The self-employment tax alone sits at 15.3%, and that's before federal and state income taxes even enter the picture. Many independent contractors don't realize how much they actually owe until it's too late, and by then, the penalties and interest have already started compounding.

This guide breaks down exactly how self-employment taxes work, how to calculate what you owe, when quarterly estimated payments are due, and which deductions can legitimately reduce your tax burden. At Tax Experts of OC, our CPAs and Enrolled Agents help independent contractors across all 50 states file accurately, claim every deduction they're entitled to, and resolve any existing tax issues with the IRS, so if you need hands-on help, we offer a free 30-minute consultation to get you started.

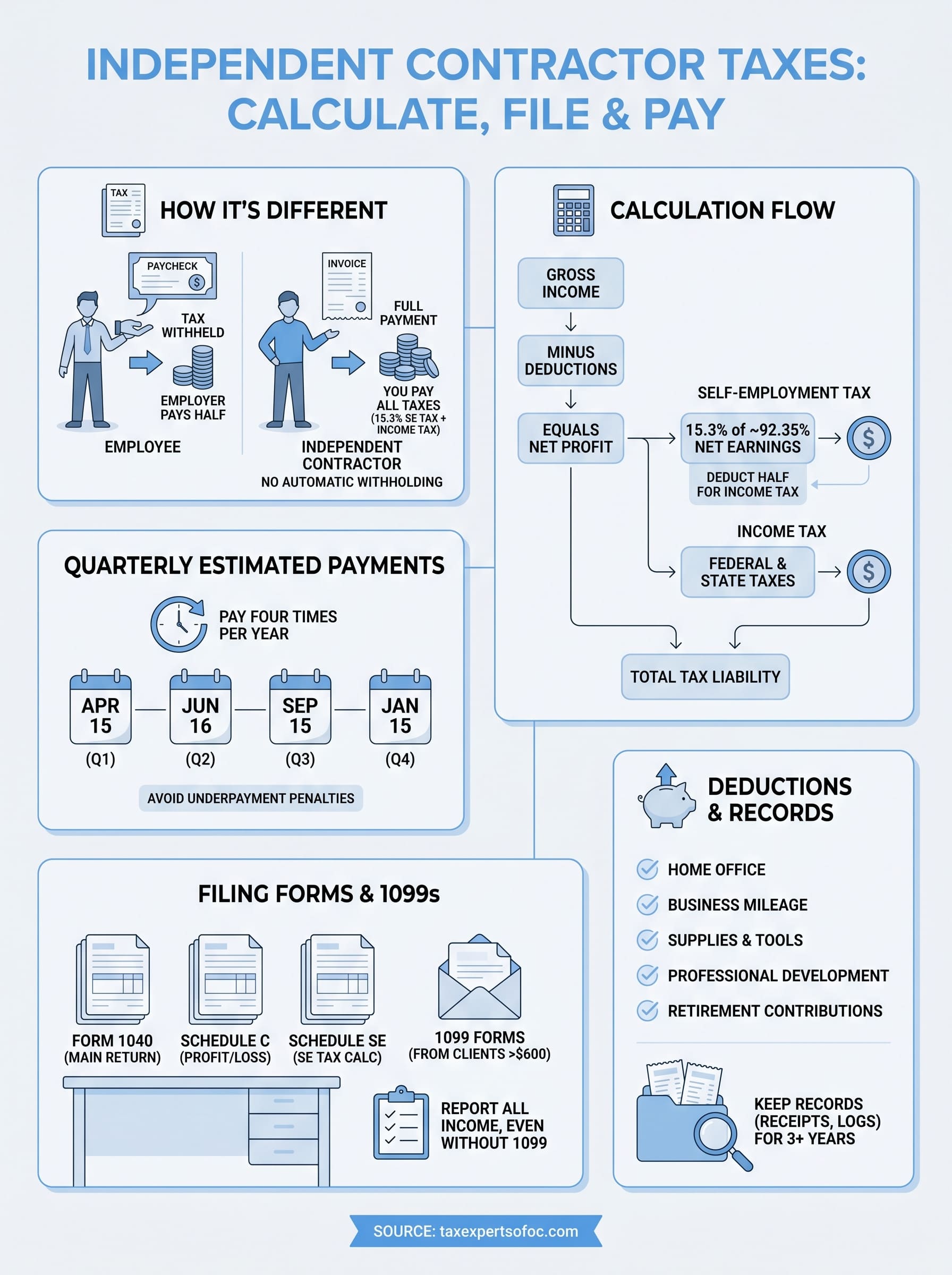

Why independent contractor taxes work differently

When you work as an employee, your employer handles a significant portion of tax administration on your behalf. They withhold federal and state income taxes from each paycheck and split the cost of Social Security and Medicare taxes with you. As an independent contractor, none of that happens. Your clients pay your full invoice amount with no withholding, and the entire tax burden lands squarely on you.

No automatic withholding from your clients

Every payment a client sends you is gross income with zero taxes removed. A traditional employee earning $80,000 per year might take home around $60,000 after federal and state withholding. If you earn $80,000 as an independent contractor, you receive the full amount, but you still owe the same taxes, plus more. Many people interpret that full payment as money they can spend freely, which leads to a painful surprise when the tax bill arrives.

Setting aside 25% to 30% of every payment you receive is a practical baseline, though your actual rate may be higher depending on your income level and state.

You pay both sides of the payroll tax

This is where independent contractor taxes get significantly more expensive than many people expect. Employees pay 7.65% of their wages toward Social Security and Medicare, and their employer pays another 7.65% on top of that. When you work for yourself, there is no employer to cover the other half. You pay the full 15.3% self-employment tax on your net earnings, which breaks down to 12.4% for Social Security on the first $176,100 of net earnings in 2025 and 2.9% for Medicare with no income cap.

The IRS does allow you to deduct half of your self-employment tax when calculating your adjusted gross income, which provides some relief. That deduction reduces your taxable income, but it does not lower the self-employment tax itself.

Federal and state income taxes still apply

Self-employment tax is separate from income tax, and both apply to your earnings. Your net profit from self-employment gets added to any other income you have, and the combined total determines which federal tax bracket you fall into.

Depending on where you live, you may also owe state income tax on top of that. California, for example, has a top marginal rate of 13.3%, which can push your combined effective tax rate well above 40% for higher earners. Knowing all three layers, self-employment tax, federal income tax, and state income tax, is the starting point for getting your numbers right.

How to calculate what you owe

Calculating independent contractor taxes starts with one number: your net profit. That's your total business income minus your allowable business deductions. The IRS taxes you on what's left, not on your gross revenue, so understanding this distinction can significantly change your final tax bill.

Step 1: Determine your net profit

Your net profit is gross business income minus deductible business expenses. If you brought in $90,000 and spent $15,000 on legitimate business expenses, your net profit is $75,000. That $75,000 is the figure you use to calculate both self-employment tax and federal income tax. Keeping accurate records throughout the year makes this step straightforward rather than stressful.

Step 2: Calculate your self-employment tax

Take 92.35% of your net profit (the IRS allows you to exclude 7.65% to approximate the employer portion) and multiply it by 15.3%. Using the $75,000 example, $75,000 x 0.9235 = $69,262.50. Multiply that by 0.153, and your self-employment tax is approximately $10,597. You can then deduct half of that amount, roughly $5,299, from your gross income before calculating your income tax.

This two-step approach, self-employment tax first and then income tax on the reduced amount, is exactly how the IRS calculates your liability on Schedule SE.

Step 3: Add your income tax liability

Your federal income tax is calculated on your adjusted gross income, which is your net profit minus the half-deduction for self-employment tax. Add your state income tax obligation on top of that. The total of these three figures, self-employment tax, federal income tax, and state income tax, is what you actually owe for the year.

How to pay quarterly estimated taxes

Because nobody withholds independent contractor taxes for you automatically, the IRS requires you to pay estimated taxes four times per year rather than waiting until April. If you skip these payments or consistently underpay, the IRS charges an underpayment penalty even if you pay the full balance when you file your return.

The four payment deadlines

The IRS sets four due dates for estimated tax payments each year, and the periods are not evenly spaced, so mark these on your calendar now. For the 2025 tax year, the deadlines fall on April 15, June 16, September 15, and January 15, 2026. Missing a deadline does not erase your obligation; it just means the penalty clock starts running from that date forward.

If a deadline falls on a weekend or federal holiday, the IRS automatically moves it to the next business day.

How to calculate each payment

Your goal is to pay enough across the four periods to avoid penalties. The safest approach is to pay at least 100% of last year's total tax liability spread across the four payments (or 110% if your prior-year adjusted gross income exceeded $150,000). Alternatively, you can estimate your current-year liability using the calculation method from the previous section and divide that total by four.

How to send your payment

The IRS offers several ways to submit your payments. The fastest and most reliable method is through the IRS Direct Pay portal, which pulls funds directly from your bank account at no cost. You can also pay via IRS Direct Pay, EFTPS, debit card, or credit card through the IRS website. Keep a record of every payment confirmation, because those figures reduce your total balance when you file your annual return.

How to file your return and forms

Filing independent contractor taxes uses the same April 15 deadline as employee returns, but the forms you complete are different. You report your self-employment income and expenses on Schedule C (Profit or Loss from Business), which attaches to your standard Form 1040. Your self-employment tax then gets calculated separately on Schedule SE, which also attaches to the same return.

The core forms for self-employed filers

Most independent contractors need to file three documents together: Form 1040, Schedule C, and Schedule SE. If you made quarterly estimated payments during the year, you also include Form 1040-ES payment vouchers or confirm those payments through the IRS records. Your software or tax professional pulls these together automatically, but knowing what each form covers helps you understand your return before you sign it.

You can download all of these forms directly from the IRS Forms and Publications page at no cost.

How 1099 forms factor in

Clients who paid you $600 or more during the year are required to send you a Form 1099-NDA by January 31 of the following year. You use these forms to verify your total gross income, but you are legally required to report all self-employment income regardless of whether a client issues a 1099. The IRS cross-references 1099s against your return, so any missing income creates a mismatch that can trigger a notice.

If you received multiple 1099s, add up the gross amounts from each form and reconcile them against your own income records before completing Schedule C. Discrepancies between your records and what clients reported are worth resolving before you file, not after.

Deductions and recordkeeping that lower taxes

The single most effective way to reduce independent contractor taxes is to claim every legitimate business deduction you're entitled to. Deductions reduce your net profit, which lowers both your self-employment tax and your income tax at the same time. Most contractors leave money on the table simply because they don't know what qualifies or they lack the records to back up their claims.

Common deductions independent contractors claim

You can deduct ordinary and necessary expenses you paid to run your business. The IRS defines these broadly, which works in your favor if you track everything consistently.

Common deductible expenses include:

- Home office (dedicated workspace used exclusively for business)

- Self-employed health insurance premiums (deducted directly from gross income)

- Business mileage at the IRS standard rate (67 cents per mile for 2024)

- Software, subscriptions, and tools used for client work

- Professional development, courses, and industry publications

- Retirement contributions to a SEP-IRA or Solo 401(k), which can substantially reduce taxable income

Contributing to a SEP-IRA lets you deduct up to 25% of net self-employment income, making it one of the most powerful tax reduction tools available to self-employed workers.

How to keep records that hold up

Strong recordkeeping is what separates a clean filing from one that falls apart under IRS scrutiny. You need documentation for every deduction you claim, including receipts, bank statements, and mileage logs. The IRS can audit returns up to three years after filing, so keeping organized records for at least that long protects you if questions arise.

A dedicated business bank account and credit card make recordkeeping far easier because all transactions stay separate from personal spending. Review and categorize your expenses monthly rather than scrambling at year-end.

Next steps if you want fewer tax surprises

Managing independent contractor taxes gets easier once you build a consistent routine around them. Set aside a percentage of every payment you receive into a separate account, make your quarterly estimated payments on time, track your deductions throughout the year, and reconcile your income records before you file. Each of these habits takes minimal time in the moment but prevents the kind of year-end scramble that leads to mistakes, penalties, and unnecessary stress.

If your situation involves back taxes, unfiled returns, IRS notices, or more complexity than standard software handles, working with a qualified professional saves you more than it costs. The CPAs and Enrolled Agents at Tax Experts of OC work with independent contractors in all 50 states, handle multi-state filings, and help clients resolve existing IRS problems before they escalate. Schedule your free 30-minute consultation today and get a clear picture of exactly where you stand.