Running a nonprofit means every dollar carries a responsibility, to your donors, your board, and your mission. That's exactly why bookkeeping for nonprofits demands a different approach than what most for-profit businesses use. You're not just tracking revenue and expenses; you're managing restricted funds, grant obligations, and public accountability all at once.

If you've been trying to apply standard business accounting methods to your 501(c)(3), you've probably already hit some walls. Fund accounting, functional expense reporting, and donor-imposed restrictions create layers of complexity that QuickBooks defaults weren't built to handle. Understanding these differences isn't optional, it's what keeps your tax-exempt status intact and your organization audit-ready.

At Tax Experts of OC, we provide bookkeeping and accounting services for nonprofits across all 50 states, with CPAs and Enrolled Agents who understand the specific compliance requirements your organization faces. This guide breaks down how nonprofit bookkeeping actually works, covers fund accounting fundamentals, and gives you practical tips to keep your financial records clean and accurate, whether you handle them in-house or bring in professional support.

Why nonprofit bookkeeping works differently

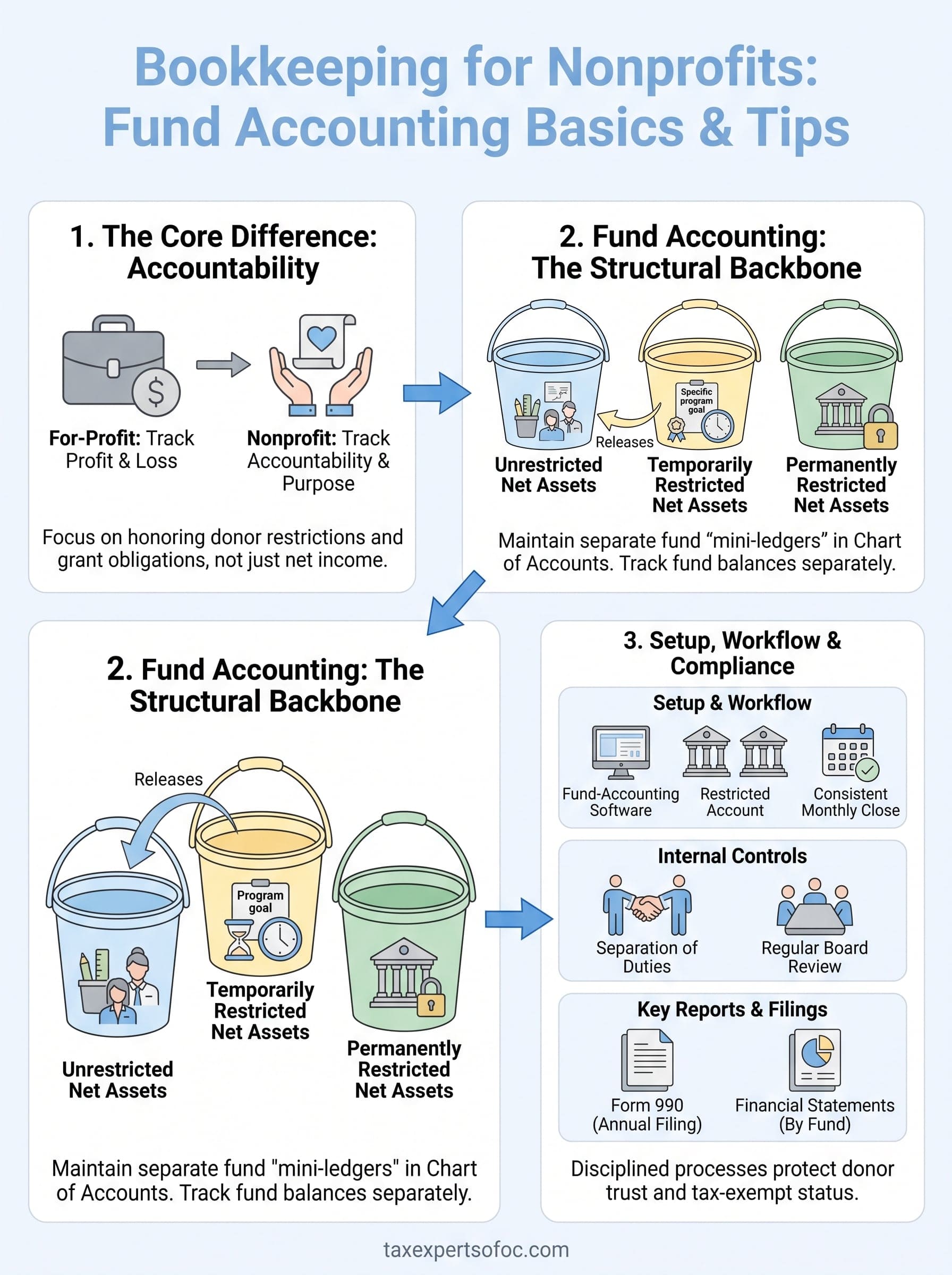

The core difference between nonprofit and for-profit accounting comes down to one word: accountability. In a standard business, you track profit and loss to measure success. In a nonprofit, you track whether you spent money the way you said you would, because your donors, grantors, and the IRS all have a stake in that answer. This shift in purpose changes almost every aspect of how you record, report, and manage financial data.

Accountability to donors, not shareholders

When someone donates to your organization, they often attach conditions to that gift. A foundation might fund a specific program. A donor might restrict their contribution to equipment purchases only. Donor restrictions are legally binding, and you must be able to show, through your books, that you honored them. This is fundamentally different from for-profit accounting, where money is largely fungible once it enters the business.

Your bookkeeping system needs to track each restricted gift separately from your general operating funds. If you mix restricted and unrestricted money in the same account without clear record-keeping, you risk violating donor intent, which can trigger legal liability and damage your organization's reputation. Bookkeeping for nonprofits isn't just a best practice; it's a fiduciary obligation that runs alongside every transaction you record.

Misusing restricted funds is one of the fastest ways to lose donor trust and invite regulatory scrutiny, even when the error was unintentional.

Tax-exempt status creates unique obligations

The IRS granted your 501(c)(3) status based on specific promises about how you operate and use your funds. Your financial records are the evidence that you're keeping those promises. The Form 990, which most nonprofits must file annually, requires you to report program expenses, officer compensation, and revenue sources in considerable detail. If your books are disorganized, completing Form 990 accurately becomes a significant challenge that can delay filing or produce errors that draw unwanted attention.

Beyond the 990, your records need to hold up under audit conditions. State attorneys general in many states carry oversight authority over charitable organizations, meaning your financial records may be subject to review at the state level as well. Clean, organized books aren't a luxury when your tax-exempt status depends on your ability to demonstrate transparency at any point the IRS or a state regulator requests it.

The role of restricted vs. unrestricted funds

Understanding the difference between restricted and unrestricted funds sits at the heart of why nonprofit accounting operates the way it does. Unrestricted funds are dollars your board can direct toward any organizational need, from salaries to office supplies. Restricted funds, by contrast, are tied to a specific purpose defined by the donor or grantor, and you cannot spend them outside that purpose without written permission.

Temporarily restricted funds become available once a condition is met, such as completing a program milestone or reaching a matching gift threshold. Permanently restricted funds, like endowments, generate income you can use, but the principal must stay intact indefinitely. Your chart of accounts and fund structure need to reflect these categories clearly so that every dollar has a home and a purpose recorded in your system.

Without that structure, you lose the ability to produce accurate reports on how each dollar was used. That information is something your board, external auditors, major donors, and grantors will request regularly. Setting up the right framework from the start saves significant time and prevents costly corrections later.

Fund accounting basics you must get right

Fund accounting is the structural backbone of bookkeeping for nonprofits. Instead of organizing your books around a single pool of money, you maintain separate funds that act like individual mini-ledgers, each with its own balance and purpose. Getting this structure right from the beginning determines whether your reports will hold up under audit scrutiny or fall apart when a grantor asks for a financial accounting.

Build your chart of accounts around fund categories

Your chart of accounts is the foundation everything else sits on, and for a nonprofit, it must reflect your fund structure directly. Each fund category needs its own set of revenue and expense accounts so you can produce accurate reports by fund without manual sorting at the end of the month. The three main categories you need to represent are unrestricted net assets, temporarily restricted net assets, and permanently restricted net assets, which align with how the Financial Accounting Standards Board (FASB) requires nonprofits to present their financial statements under ASC 958.

A well-structured chart of accounts makes it straightforward to pull the numbers a foundation needs when reviewing your grant compliance. It also makes your annual Form 990 preparation significantly less painful, because the data is already organized the way the IRS expects to see it.

A chart of accounts built around fund categories saves hours of cleanup every reporting period and reduces the risk of misclassifying restricted dollars.

Track fund balances separately to protect donor intent

Once your chart of accounts is in place, your day-to-day entries must consistently code each transaction to the correct fund. A grant payment comes in? It goes directly into the designated restricted fund, not your general operating account. A program expense gets paid? You draw it from the fund that authorized it. Every entry needs a fund designation, not just an expense category.

You also need a process to recognize fund releases, the moment a restriction lifts because you've met the condition attached to a grant or donation. Properly recording a release moves money from temporarily restricted to unrestricted net assets and keeps your financial statements accurate. Skipping this step causes your restricted fund balances to appear overstated, which misleads your board and can create problems during an external audit.

How to set up your nonprofit bookkeeping system

Setting up your system correctly before transactions start flowing in saves you from painful cleanup later. The decisions you make at this stage, from software selection to account structure, will shape how accurately you can report on fund balances, donor restrictions, and program expenditures for years to come.

Choose accounting software built for the task

General-purpose accounting software often lacks the fund-tracking features that bookkeeping for nonprofits requires. Look for software that supports fund accounting natively, meaning it lets you assign transactions to specific funds and generate fund-level reports without manual workarounds. Many nonprofits use platforms designed with a nonprofit chart of accounts already built in, which reduces setup time and lowers the risk of miscategorizing revenue.

Your software choice will either simplify your reporting or complicate it every month, so evaluate fund-tracking capability before you commit.

Some software providers offer discounted or donated licenses to qualifying 501(c)(3) organizations through programs like Google for Nonprofits. Verify what reporting formats the software produces before committing, because your board and auditors will expect standard nonprofit financial statements, specifically the statement of activities and the statement of financial position, not the profit-and-loss reports that for-profit software defaults to.

Separate your bank accounts by fund type

Your bank account structure needs to mirror your fund structure, at least for significant restricted funds. Keeping grant dollars in a dedicated account rather than your general operating account makes it far easier to demonstrate to a grantor that you spent their dollars appropriately. You reduce the risk of accidentally using restricted funds for operating costs, and monthly reconciliation becomes more straightforward as a result.

For smaller restricted gifts, a sub-ledger tracking system within your accounting software can work in place of separate bank accounts, provided your entries are disciplined and consistent. The key requirement is that your records show a clear trail from every dollar received to every dollar spent within a given fund.

Assign a dedicated bookkeeper to your accounts

Without a single accountable owner for your books, entries get delayed, errors go uncorrected, and fund balances drift out of alignment with your actual financial position. Whether you hire an in-house bookkeeper or outsource the function, one person needs to be responsible for keeping your records current. Define their responsibilities in writing, including how often they reconcile accounts, who reviews their work, and how they document and record fund releases when grant conditions are met.

Monthly workflow and internal controls

A consistent monthly routine is what separates clean, reliable books from a financial mess you discover right before an audit. Without a defined workflow, transactions pile up, reconciliations get skipped, and fund balances drift far from reality. Bookkeeping for nonprofits requires discipline at the monthly level because errors compound quickly when restricted funds and grant deadlines are in play.

Establish a consistent monthly close process

Your monthly close should follow the same sequence every time so nothing falls through the cracks. Start by reconciling every bank account and credit card statement against your internal records before you do anything else. Once reconciliation is complete, review each fund's balance to confirm that restricted dollars are sitting where they should be and that no unrestricted expenses were accidentally coded to a grant fund.

After reconciliation, review any open invoices, pending donations, and outstanding reimbursements so your records reflect the true financial position of each fund at month-end. Document this review with a simple checklist your bookkeeper signs off on, because a dated record of your close process is exactly the kind of evidence an auditor wants to see. Require that checklist to be retained with your monthly financial files so it is available immediately if a grantor or regulator requests it.

A signed monthly close checklist creates an audit trail that demonstrates your organization maintains ongoing financial oversight, not just year-end scrambles.

Build internal controls that prevent errors

Internal controls are the procedures that protect your organization from both honest mistakes and intentional misconduct. For small nonprofits, even a handful of basic controls can dramatically reduce financial risk. The most important principle is separation of duties: the person who authorizes a payment should not be the same person who records it or signs the check.

Your board finance committee should receive and review financial statements every month, not just quarterly. Regular board-level review creates an independent check on what your bookkeeper is recording and ensures leadership spots irregularities before they grow into larger problems. Requiring two signatures on checks above a defined dollar threshold adds another layer of protection without creating much administrative burden.

Build a written policy document that spells out who can approve expenses, what documentation is required before a reimbursement gets recorded, and how your organization handles cash receipts. Having these procedures documented means the controls survive staff turnover and give new team members a clear standard to follow from day one.

Reports and filings that keep you compliant

Compliance for a nonprofit is an ongoing process, not a once-a-year event. Accurate bookkeeping for nonprofits produces the data that flows directly into your required filings, so the quality of your records determines the quality of your compliance. If your books are messy, your reports will reflect that, and regulators notice.

The Form 990: your annual accountability document

The IRS Form 990 is the most significant filing your organization produces each year, and it pulls directly from your bookkeeping records. Depending on your revenue, you will file the 990, 990-EZ, or 990-N, so confirm which version applies to your organization before the filing deadline. The full Form 990 requires a detailed breakdown of program expenses, officer compensation, revenue sources, and governance practices. If your chart of accounts isn't structured to match those reporting categories, assembling the form becomes a manual reconstruction project that increases the risk of errors.

Filing an inaccurate Form 990 can trigger IRS scrutiny and jeopardize your tax-exempt status, even when the error was unintentional.

Your 990 is also a public document, meaning any donor or journalist can request a copy. Treat it as both a compliance requirement and a transparency tool that represents your organization to anyone who looks.

Financial statements your board and donors expect

Your board needs accurate financial statements every month, not just at year-end. The two primary statements for nonprofits are the statement of financial position (the equivalent of a balance sheet) and the statement of activities (which shows how your revenue and expenses moved during a period). Both must present fund balances clearly so board members can see whether restricted and unrestricted assets are being managed appropriately.

Many grantors also require interim financial reports during a grant period, not just at the end. Your bookkeeping system needs to produce fund-specific reports quickly on request. If pulling a program-level expense report takes days of manual work, that is a signal your system needs restructuring before the next grant cycle begins.

State registration and charitable solicitation requirements

Most states require nonprofits to register before soliciting donations within their borders, and many require annual renewal filings with updated financial information. If your organization fundraises across multiple states, you may carry registration obligations in each of them. Your financial records need to be current and accurate to complete these filings on time, because late or incomplete submissions can result in fines and suspension of your solicitation authority.

Next steps for cleaner nonprofit books

Clean books start with a decision to treat your financial records as seriously as your mission. Bookkeeping for nonprofits requires the right account structure, disciplined monthly habits, and reports that give your board and donors a clear picture of how every dollar moves through your organization. If any part of your current system feels uncertain, the time to address it is before an audit request or a grant deadline forces the issue and creates additional pressure on your team.

Your organization deserves financial records that hold up under scrutiny and support the work you're doing every day. Tax Experts of OC works with nonprofits across all 50 states, providing bookkeeping, accounting, and tax compliance support from CPAs and Enrolled Agents who understand the specific requirements your 501(c)(3) faces. If you're ready to get your books in order, schedule a free consultation with our nonprofit accounting team and find out exactly where to start.