Running a small business means wearing too many hats, and bookkeeping is usually the one that fits the worst. Between tracking expenses, reconciling accounts, and keeping up with tax deadlines, the financial side of your business can quietly consume hours you don't have. That's exactly why outsourced bookkeeping for small business owners has become a practical solution: it hands the work to qualified professionals while you focus on actually running your company.

Most business owners start searching for outsourced bookkeeping when they hit a wall, maybe the books are a mess, tax season is a nightmare, or growth has made DIY accounting unsustainable. The real question isn't whether you need help. It's whether outsourcing makes more sense than hiring in-house, how much it actually costs, and what you should expect from a provider. Those are the questions this article answers, with specific numbers and honest trade-offs.

At Tax Experts of OC, our CPAs and Enrolled Agents provide bookkeeping and accounting support on a monthly, quarterly, or annual basis to small and mid-sized businesses across all 50 states. We built this guide from that hands-on experience, working directly with business owners who needed reliable financial records without the overhead of a full-time bookkeeper. Below, you'll find a clear breakdown of what outsourced bookkeeping includes, what it costs, and how to decide if it's the right move for your business.

What outsourced bookkeeping includes

Before you commit to a provider, you need a clear picture of what you're actually buying. Outsourced bookkeeping for small business covers a wider range of tasks than most owners expect, but it also has boundaries that are worth understanding upfront. Knowing what falls inside and outside the service prevents billing surprises and helps you compare providers on equal footing.

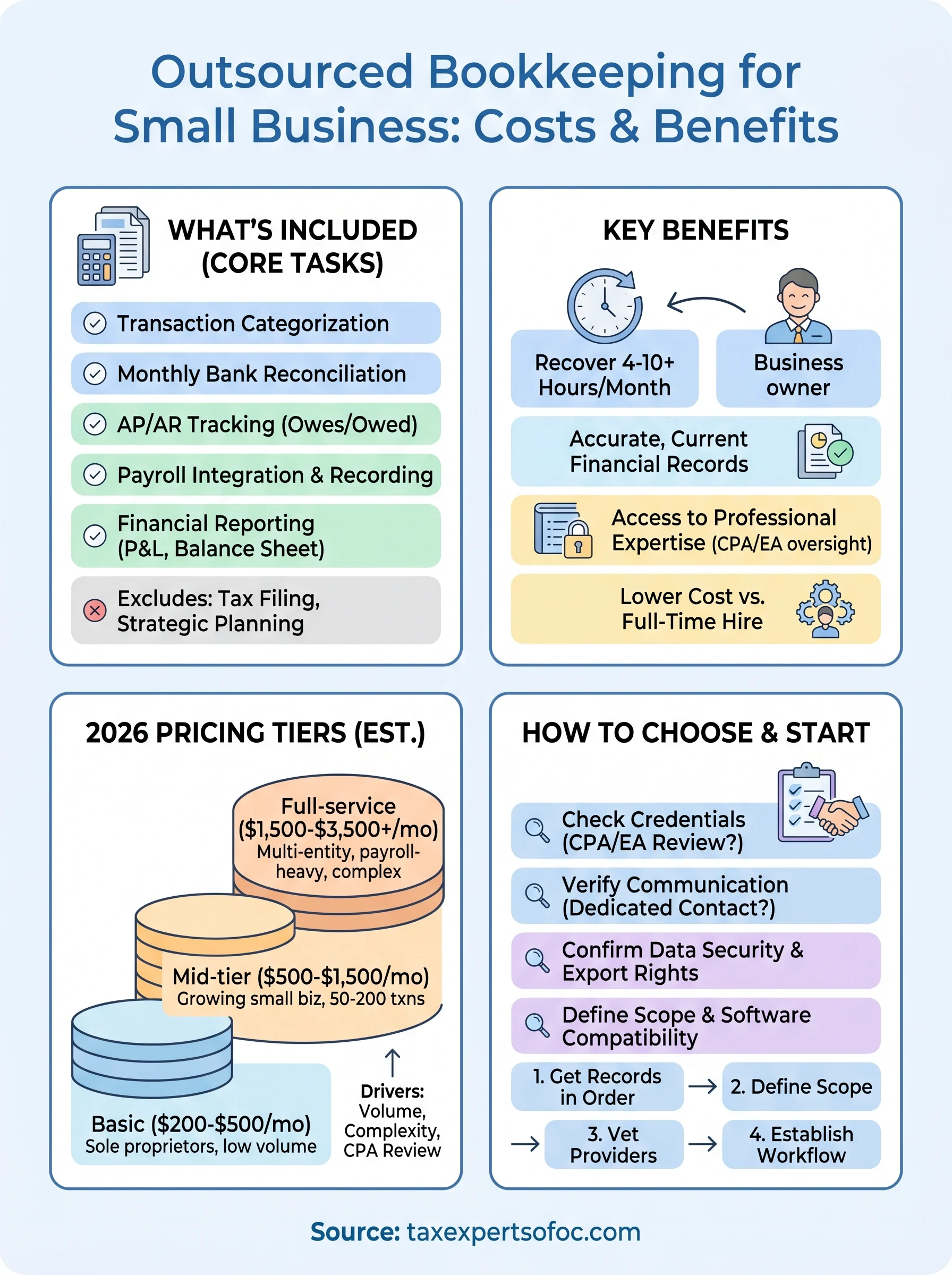

Core day-to-day bookkeeping tasks

The foundation of any bookkeeping service is transaction management. Your provider records every income and expense that flows through your business, categorizes each transaction against your chart of accounts, and keeps your general ledger accurate and current. Bank reconciliation is done on a regular schedule, usually monthly, so your books match your actual bank and credit card statements. This alone catches errors, duplicate charges, and fraud that otherwise go unnoticed for months.

Beyond transaction entry, most providers also handle accounts payable and accounts receivable tracking, which means they monitor what you owe vendors and what customers owe you. Some services include invoicing support and vendor payment scheduling, though the level of involvement varies by plan. If your business carries inventory, a qualified provider will also maintain inventory records and reconcile physical counts against your accounting software.

Accurate, reconciled books are the single most important thing you can get from a bookkeeping service, because every other financial decision you make depends on them.

Financial reporting and tax readiness

A bookkeeper's job doesn't end at data entry. Monthly financial statements, including a profit and loss statement, balance sheet, and cash flow statement, give you a real-time view of your business health. These reports let you spot trends, identify problem areas, and make decisions based on actual numbers rather than guesses.

Tax readiness is where clean books pay off the most. When your income and expenses are properly categorized throughout the year, your tax preparer or CPA can file faster, with fewer corrections, and with a lower chance of triggering IRS scrutiny. Many outsourced bookkeeping firms, including Tax Experts of OC, coordinate directly with the tax filing side of the business so there's no gap between your records and your return.

Payroll integration is another piece that frequently comes with bookkeeping packages. Your provider ensures payroll entries are recorded correctly, employer tax liabilities are tracked, and the numbers tie back to your quarterly payroll tax filings. This matters especially if you've ever had a mismatch between your books and your 941 forms.

What outsourced bookkeeping typically does not include

Understanding the limits of the service is just as important as knowing what it covers. Most bookkeeping packages do not include tax preparation or filing. Bookkeeping produces organized financial records; tax preparation uses those records to calculate and file your returns. These are separate services, and providers price them separately.

Strategic tax planning, IRS representation, and audit defense also fall outside standard bookkeeping. If you receive an IRS notice or face a compliance issue, you need a CPA or Enrolled Agent who can represent you directly, which goes beyond what a bookkeeper is licensed to do. Some firms bundle these services under one roof, which simplifies things considerably.

CFO-level guidance, such as cash flow forecasting, financial modeling, or growth strategy, is a separate tier as well. Bookkeeping keeps your records accurate; advisory work interprets those records to help you make higher-level business decisions. If you need both, look for a firm that explicitly offers both rather than assuming one includes the other.

When outsourcing makes sense for small businesses

Outsourcing isn't the right move for every business at every stage, but there are clear trigger points that signal when the DIY approach stops working. Most small business owners only recognize these signs after they've already cost money, whether through missed deductions, late filing fees, or a tax return that required months of cleanup before anyone could even start on it.

Signs your current approach is costing you

The clearest sign that you need help is when bookkeeping tasks consistently get pushed to the back of your schedule. If you're reconciling months of transactions the week before your tax deadline, your books aren't working for you. Other warning signs include unexplained cash flow gaps, vendor payments that fall through the cracks, and financial statements you can't explain to your bank or a potential investor.

If you can't read your own financial statements with confidence, the problem isn't the numbers, it's the process generating them.

Growing businesses also hit a volume threshold where manual entry and spreadsheet tracking become unreliable. A single employee handling accounts receivable, payroll, and expense records in the same spreadsheet creates errors and blind spots. When your business processes more than a few dozen transactions a month, the risk of inaccuracies rises faster than most owners expect.

Business stages where outsourcing fits naturally

Outsourced bookkeeping for small business owners tends to deliver the most value at specific growth stages. Startups and early-stage businesses benefit because they get professional-grade financial infrastructure without committing to a full-time bookkeeper salary, which typically runs $40,000 to $55,000 per year before benefits. You get organized records from day one, which matters when you apply for a business loan or bring on investors.

Established small businesses that are scaling, adding employees, or expanding into new states also reach a point where complexity outpaces what a solo operator or general office manager can handle. Multi-state payroll, sales tax across multiple jurisdictions, and a growing vendor list all add layers that require specific accounting knowledge. At this stage, outsourcing keeps your books accurate while you direct your attention toward managing growth rather than managing paperwork.

Benefits you can expect from outsourced bookkeeping

The case for outsourced bookkeeping for small business owners comes down to concrete, measurable gains. You get back hours every week, your records become reliable, and you gain access to professional expertise without the cost of a full-time hire. These aren't abstract promises; they show up directly in your tax returns, your bank relationships, and your ability to make informed financial decisions for your business.

You recover time you can redirect to your business

Most small business owners spend 4 to 10 hours per month on bookkeeping tasks when they handle the work themselves. That number climbs quickly as your transaction volume grows. When you outsource, those hours return to you and you can direct them toward sales, operations, or managing your team. Time has a real dollar value, and pulling it away from low-skill administrative work is one of the more straightforward financial decisions a growing business can make.

When you calculate the hourly cost of your own time against what a bookkeeping service charges, outsourcing almost always wins on pure economics.

Your financial records become accurate and current

Accurate, reconciled books give you a clear picture of your cash position, profit margins, and outstanding liabilities at any given moment. When a professional reconciles your accounts monthly, you catch errors before they compound into larger problems. You also avoid arriving at tax season with months of disorganized transactions that require reconstruction from bank statements. Clean records mean your CPA or Enrolled Agent can file accurately and faster, with far less back-and-forth and a lower chance of triggering IRS scrutiny.

You gain access to professional expertise at a fraction of the cost

A full-time bookkeeper costs between $40,000 and $55,000 per year in base salary before benefits, payroll taxes, or software subscriptions. Outsourcing gives you access to that same level of skill at a monthly rate that scales with what your business actually needs. Many firms also pair bookkeeping with CPAs and Enrolled Agents who can catch problems a generalist would miss, such as misclassified expenses or payroll tax discrepancies that could create compliance issues later.

Smaller businesses benefit most from this structure because they get a professional-grade financial operation without the overhead of building an internal accounting department from scratch.

Common risks and how to reduce them

Outsourced bookkeeping for small business owners delivers real value, but it comes with risks you need to address before signing anything. Handing over sensitive financial data and relying on a third party to meet your deadlines are both legitimate concerns. The good news is that most of these risks are manageable with the right vetting process and a clear service agreement.

Data security and ownership of your records

Your financial records contain sensitive information: bank account details, payroll figures, vendor contracts, and revenue data. When you share that information with an outside firm, you need to verify how they store, transmit, and protect it. Reputable providers use encrypted file sharing, secure cloud platforms, and role-based access controls. Ask directly about their data security practices and whether they carry professional liability insurance before you hand over a single bank statement.

The security of your financial data is non-negotiable; verify a provider's practices before you share anything.

Ownership of your data is equally important to confirm upfront. Some providers lock records inside proprietary systems that make it difficult to export your books if you decide to switch services. Before you sign, confirm that you hold full export rights and that your files will be available in a standard format your next provider or accountant can use without a conversion project.

Quality control and communication gaps

Some bookkeeping firms assign accounts to junior staff or rotate personnel frequently, which produces inconsistent work and recurring errors. To reduce this risk, ask upfront whether your account will have a dedicated point of contact and what their credentials are. Firms that have CPAs or Enrolled Agents in a supervisory role add a meaningful quality check because a licensed professional reviews the work before it reaches you.

Communication breakdowns are the other side of this problem. If your provider takes two weeks to answer a question or deliver a monthly report, you lose the real-time visibility that makes outsourcing worthwhile. Set clear response time expectations in your service agreement and ask prospective providers how they handle urgent or time-sensitive requests. A provider that struggles to answer basic questions during the sales process will not perform better once you are a paying client.

How much outsourced bookkeeping costs in 2026

The price you pay for outsourced bookkeeping for small business depends on your transaction volume, the complexity of your accounts, and the level of service you need. Most providers use a monthly flat-rate or tiered pricing model, which makes it easier to budget than hourly billing. Understanding the typical ranges before you shop prevents you from overpaying for services you don't need or underbuying and ending up with gaps in your coverage.

What pricing tiers look like

Monthly costs for outsourced bookkeeping generally fall into three bands based on business size and transaction volume. The table below shows what you can expect to pay in 2026 for each level of service.

| Service tier | Monthly cost range | Best for |

|---|---|---|

| Basic | $200 to $500 | Sole proprietors, low-volume businesses |

| Mid-tier | $500 to $1,500 | Growing small businesses, 50 to 200 monthly transactions |

| Full-service | $1,500 to $3,500+ | Multi-entity, payroll-heavy, or multi-state businesses |

Basic plans typically cover transaction categorization, monthly reconciliation, and standard financial statements. Mid-tier plans add accounts payable and receivable tracking, payroll integration, and more frequent reporting. Full-service plans bring in CPA or Enrolled Agent oversight, which adds a meaningful layer of accuracy and compliance review that basic plans skip entirely.

If your books require cleanup before a provider can take them over, most firms charge a one-time catch-up fee that ranges from $500 to $2,500 depending on how far behind your records are.

What drives your monthly rate higher

Several factors push your rate toward the upper end of any tier. High transaction volume is the most consistent driver because every additional transaction adds time and complexity to the reconciliation process. Businesses that process payroll for multiple employees, carry inventory, or operate in more than one state also pay more because each of those elements adds reporting requirements and reconciliation steps.

The credentials of the people handling your account also affect pricing. Firms where a CPA or Enrolled Agent reviews your books charge more than firms that assign accounts entirely to non-licensed staff. That additional cost is worth it because a licensed professional catches misclassifications and payroll tax discrepancies that a general bookkeeper might not flag, and those errors tend to surface at the worst possible time, typically during tax season or a bank review.

How to choose the right bookkeeping partner

Choosing the right provider for outsourced bookkeeping for small business owners is not just about finding the lowest monthly rate. The firm you select will have direct access to your financial records and will shape the accuracy of your tax filings, your ability to secure financing, and your understanding of your own business performance. Getting this decision right requires asking specific questions before you commit.

Check credentials and who actually handles your account

The most important question you can ask a bookkeeping firm is who will actually work on your books. Many providers advertise CPA oversight but assign your account to non-licensed staff with minimal supervision. Ask directly whether a CPA or Enrolled Agent reviews your monthly financials before they are delivered to you. That licensing matters because a credentialed professional will catch misclassified transactions and payroll tax discrepancies that an entry-level bookkeeper will miss entirely.

A credential check takes five minutes and can prevent months of cleanup work later.

You should also verify that your account will have a dedicated point of contact rather than a rotating team. Consistency reduces errors because the person managing your books understands the patterns in your accounts and flags anomalies that a new person would overlook.

Evaluate their communication and reporting process

A bookkeeping partner who delivers your monthly reports two weeks late or takes days to answer a basic question undermines the value of the service. Before you sign anything, ask how they deliver monthly financial statements and what their standard turnaround time is. Find out whether you receive a profit and loss statement, a balance sheet, and a cash flow statement each month as a standard part of the package.

Software compatibility is another practical filter. Confirm that your provider works inside the accounting platform you already use, or that they can migrate your data without a billing premium. You should always retain full export rights to your files in a standard format so switching providers later does not become a project in itself.

Questions to ask before you sign

Use this checklist when you evaluate any bookkeeping firm:

- Are the people reviewing your books licensed CPAs or Enrolled Agents?

- What is their standard response time for questions or urgent requests?

- Do they carry professional liability insurance?

- How do they handle catch-up bookkeeping if your records are behind?

- Can you export your books at any time in a format your tax preparer can use?

How to outsource bookkeeping step by step

The transition to outsourced bookkeeping for small business owners goes smoothly when you follow a clear sequence. Jumping straight to signing a contract before your records are organized or your expectations are defined creates friction that delays the onboarding process and can lead to a higher setup fee. Work through these steps in order to get your books handed off correctly.

Get your current records in order first

Before you contact any provider, gather your existing financial records so you know exactly what state they are in. Pull your most recent bank statements, credit card statements, and any accounting software exports you have. If your books are behind by several months, acknowledge that now because most providers will charge a catch-up fee to reconstruct missing records before they can begin ongoing service.

Knowing the condition of your records before the first conversation with a provider puts you in a stronger negotiating position.

Define the scope of what you need

Write down the specific tasks you want your provider to handle each month. Be direct: transaction categorization, bank reconciliation, payroll integration, accounts receivable tracking, or some combination. Knowing your scope prevents you from paying for services you don't use and ensures you don't accidentally purchase a basic plan that leaves out something you need.

Also identify your accounting software so you can confirm compatibility before you commit. If you currently use QuickBooks, Xero, or another platform, your provider should work inside that system rather than migrating your data to a proprietary platform that limits your ability to leave.

Vet at least two or three providers

Contact multiple firms and ask the credential and communication questions outlined in the previous section. Compare monthly pricing, response time commitments, and who specifically reviews your books. Request a sample financial report so you can evaluate what you will receive each month. A provider that cannot produce a clean sample report before you sign will not produce clean reports after.

Set up access and establish a recurring workflow

Once you select a provider, give them access to your accounting software and bank feeds through secure, read-only or accountant-level permissions. Confirm the monthly close schedule, the date you will receive your financial statements, and the primary contact for ongoing questions. Setting these expectations in writing at the start eliminates the communication gaps that frustrate most outsourcing relationships within the first 90 days.

Next steps to get your books under control

Outsourced bookkeeping for small business owners works best when you start with a clear picture of where your records stand today. Pull your last three months of bank statements, note how far behind your books are, and list the specific tasks you need a provider to handle each month. That preparation takes less than an hour and puts you in a much stronger position when you compare providers.

From there, the decision comes down to credentials, communication, and cost. You want a firm where a licensed CPA or Enrolled Agent reviews your work, not just a general bookkeeper. If you need a provider who handles bookkeeping alongside tax preparation and IRS representation under one roof, Tax Experts of OC offers bookkeeping and accounting support on a monthly, quarterly, or annual basis. Start with a free 30-minute consultation to get a straight answer on what your business actually needs.