Filing taxes as a business owner is a different animal than dropping a W-2 into TurboTax. Between entity types, quarterly estimates, deductions, and ever-shifting IRS rules, finding reliable business tax filing help can mean the difference between a clean return and a costly mistake. And with the 2026 filing deadline bearing down, the pressure to get it right is real.

This guide breaks down the full process, from choosing your filing method and gathering documents to understanding costs and knowing exactly when it makes sense to hire a professional. Whether you're a sole proprietor filing for the first time or an LLC owner juggling multi-state obligations, you'll walk away with a clear action plan instead of more questions.

At Tax Experts of OC, our CPAs and Enrolled Agents help business owners across all 50 states file accurately and on time, and step in when things get complicated. We built this guide from the same firsthand experience we bring to client work every day, so you're getting practical advice rooted in real tax resolution and preparation knowledge, not recycled theory.

What business tax filing help covers

Business tax filing help is not a single service. It describes a range of support that spans preparation, compliance, and problem-solving, depending on where you are in the tax cycle. For a sole proprietor, it might mean getting someone to complete a Schedule C accurately. For an S-corp owner, it might mean coordinating payroll tax filings, quarterly estimates, and the 1120-S return all at once. Understanding what falls under this umbrella helps you identify exactly what kind of help you actually need.

The right type of business tax help depends entirely on your entity structure, your revenue complexity, and whether you have any outstanding issues with the IRS.

Preparation and compliance

Tax preparation is the most common reason business owners seek filing help. It covers the actual assembly and submission of your return, including choosing the correct form, reporting income accurately, and applying the deductions you qualify for. Compliance goes a step further, making sure you meet ongoing obligations throughout the year: quarterly estimated payments, payroll tax deposits, sales tax remittances, and information returns like 1099-NECs.

Most business owners need both, not just help at year-end. If you only focus on the annual return, you risk penalties for missed quarterly payments or late payroll deposits, which the IRS assesses separately from income tax. A solid compliance setup during the year makes the final filing significantly easier and cheaper.

Tax planning

Strategic tax planning sits upstream of filing. It involves decisions you make before the tax year ends, such as timing equipment purchases to capture Section 179 deductions, structuring owner compensation to reduce self-employment tax, or electing S-corp status at the right time. Planning and filing are separate activities, but they feed each other directly. The choices you make during the year affect what your return looks like when you file it.

Many business owners skip planning until they see the tax bill and regret it. Pulling in a CPA or Enrolled Agent mid-year, rather than waiting until March, gives you room to act on advice before the window closes.

Resolution and representation

When something has already gone wrong, such as unfiled returns, IRS notices, back taxes, audits, or liens, you need resolution help rather than standard preparation. This is a distinct category, and it requires professionals with the authority to represent you before the IRS. Enrolled Agents and CPAs hold that authority under IRS Circular 230; most general tax preparers do not.

If you have a letter from the IRS on your desk right now, get resolution help before you file anything else. Submitting a return with unresolved issues can sometimes make the situation harder to settle. Resolution and preparation often go hand in hand for business owners coming back into compliance after a gap in filing.

What the process actually involves

At a practical level, business tax filing help touches several moving parts regardless of who provides it:

- Reviewing your bookkeeping records and correcting errors before you file

- Selecting the correct federal and state forms for your entity type

- Calculating deductible expenses and applicable credits accurately

- Verifying that payroll tax deposits match what you report on your return

- Filing on time and arranging payment or an installment plan if you owe

Each of these steps carries its own risk of error, and a mistake in one area often creates problems in another. That interconnection is exactly why many business owners find it worth paying for professional oversight rather than navigating it alone.

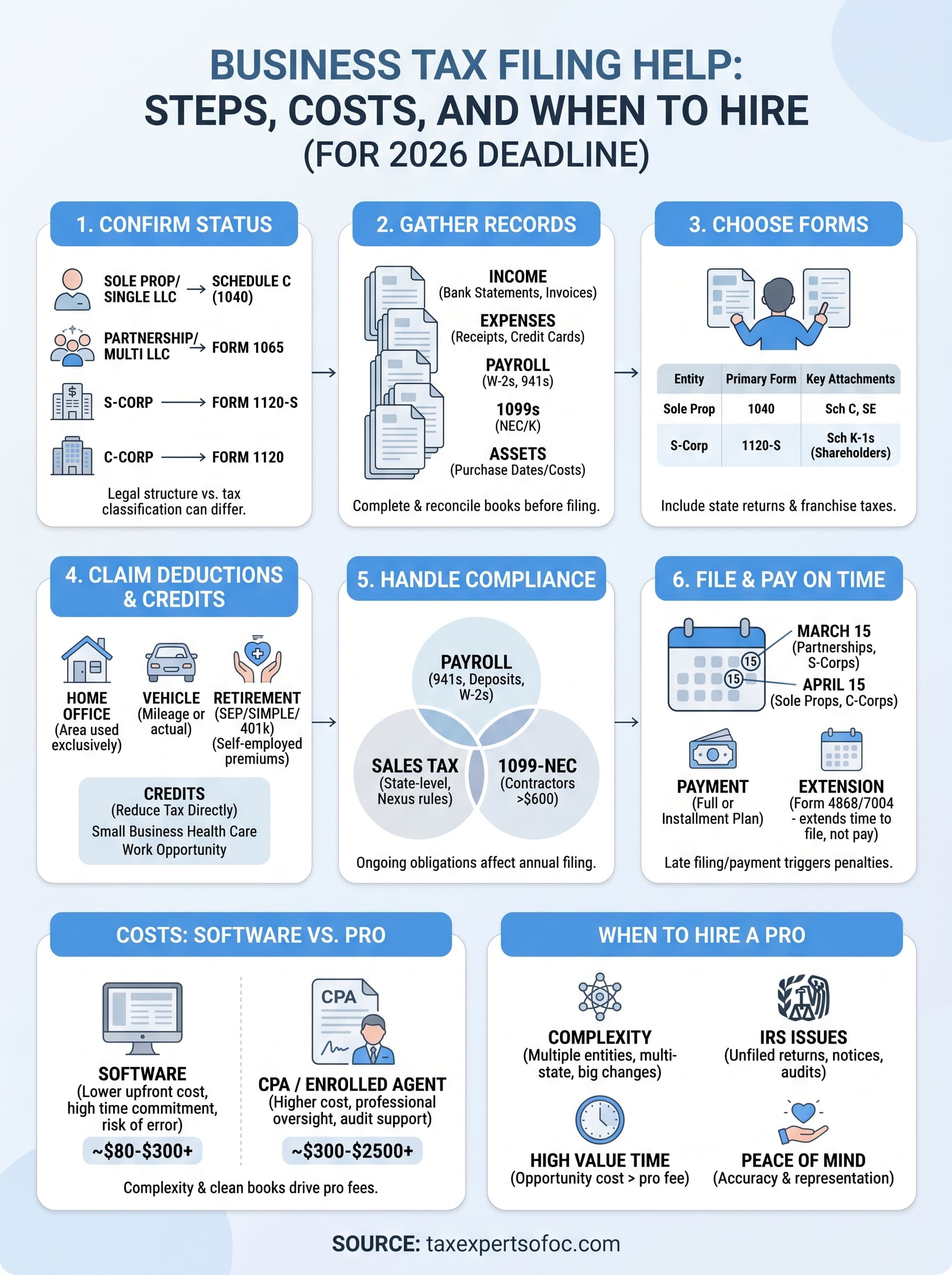

Step 1. Confirm your business tax status

The first thing you need to do before seeking any business tax filing help is confirm exactly what type of entity you are in the IRS's eyes. Your legal structure and your tax classification are not always the same thing, and filing under the wrong status will send your return down the wrong path entirely.

How your entity type determines your forms

Your entity type dictates which federal return you file, what rates apply, and who bears the tax liability. A sole proprietor files a Schedule C attached to their personal Form 1040. A partnership files Form 1065. A C-corporation files Form 1120, and an S-corporation files Form 1120-S. LLCs are the most common source of confusion because they can be taxed as any of these depending on how many members they have and what elections they have made.

| Entity Type | Default Tax Classification | Primary Federal Form |

|---|---|---|

| Sole Proprietor | Individual | Schedule C (Form 1040) |

| Single-Member LLC | Disregarded entity | Schedule C (Form 1040) |

| Multi-Member LLC | Partnership | Form 1065 |

| LLC (S-corp election) | S-Corporation | Form 1120-S |

| Partnership | Partnership | Form 1065 |

| S-Corporation | S-Corporation | Form 1120-S |

| C-Corporation | C-Corporation | Form 1120 |

If your LLC made an S-corp election but you never filed Form 2553, the IRS may not recognize that status, which means your return and the IRS's records will not match.

How to check or change your status

You can verify your current IRS tax classification by reviewing the Entity Classification Election you filed on Form 8832 or by checking your original business registration alongside any subsequent elections. If you filed Form 2553 to elect S-corp status, confirm the IRS accepted it in writing before you file Form 1120-S. If you never received an acceptance letter, call the IRS Business and Specialty Tax Line at 1-800-829-4933 to verify what is on file.

Changing your tax classification mid-stream is possible but carries strict timing restrictions. The IRS generally requires you to submit Form 8832 or Form 2553 by the 15th day of the third month of the tax year for the election to take effect that year. Missing that window pushes the effective date to the following year, which means you file under your current status for the period you are in now.

Step 2. Gather records and close your books

Before you touch a single tax form, your financial records need to be complete and accurate. Filing with incomplete books is one of the most common reasons business owners end up amending returns or facing IRS scrutiny. This step is where solid bookkeeping pays off directly, and where gaps in your records become visible before they cause damage.

The records you need to pull together

Gathering documents before you start any business tax filing help process saves you significant back-and-forth time, whether you are working with a CPA or preparing the return yourself. You need records that cover every dollar that came in and every deductible dollar that went out during the tax year.

Here is the core document checklist for most small business owners:

- Income records: bank statements, invoices, payment processor reports (Square, Stripe, PayPal), and sales receipts

- Expense records: receipts, credit card statements, and vendor invoices organized by category

- Payroll records: W-2s issued to employees, payroll tax deposit confirmations, and Form 941 filings

- 1099s received: Form 1099-NEC or 1099-K from clients or platforms if you received $600 or more

- Asset records: purchase dates and costs for any equipment, vehicles, or property placed in service during the year

- Loan and interest records: year-end statements showing interest paid on business loans or lines of credit

- Prior year return: your previous filed return to confirm carryovers, depreciation schedules, and any elections still in effect

Missing even one category, especially asset records or payroll confirmations, can force you to file an extension or submit an amended return later.

Closing your books before you file

Closing your books means reconciling every bank and credit card account against your accounting records so that your profit and loss statement reflects what actually happened during the year. If your bookkeeping software shows a different revenue figure than your bank deposits, you have a discrepancy that needs to be resolved before you file.

Run a bank reconciliation for every account through the last day of your tax year. Then pull a profit and loss statement and a balance sheet dated December 31 (or the last day of your fiscal year). Check that your accounts payable and receivable balances are current, and confirm that any loans on your books match your actual outstanding balances. These two reports are what your tax preparer will use to build your return, so accuracy here drives accuracy everywhere else.

Step 3. Choose the right forms for your entity

Once your books are closed and your entity status is confirmed, you need to match your situation to the correct IRS forms before you file anything. Using the wrong form is not a minor technicality. The IRS can treat a misfiled return as though it was never submitted, which triggers late-filing penalties even if you sent everything in on time.

Federal forms and their attached schedules

Each entity type comes with a primary return and supporting schedules that you complete depending on your specific activity. Sole proprietors and single-member LLCs attach Schedule C to Form 1040, but they also need Schedule SE to calculate self-employment tax on net profit. Partners in a multi-member LLC or partnership receive a Schedule K-1 from the partnership's Form 1065 return and report that income on their personal returns.

S-corp owners must file both Form 1120-S for the business and a personal Form 1040 that includes their K-1 income, plus payroll returns if they draw a reasonable salary.

Here is a reference for the most common entity-form combinations you will encounter when seeking business tax filing help:

| Entity | Primary Return | Key Schedules or Attachments |

|---|---|---|

| Sole Proprietor | Form 1040 | Schedule C, Schedule SE |

| Single-Member LLC | Form 1040 | Schedule C, Schedule SE |

| Multi-Member LLC / Partnership | Form 1065 | Schedule K-1 for each partner |

| S-Corporation | Form 1120-S | Schedule K-1 for each shareholder |

| C-Corporation | Form 1120 | Varies by deductions and credits claimed |

State returns and additional filing requirements

Your federal return is only part of the picture. Most states with an income tax require a separate business return, and some impose a minimum franchise tax regardless of whether your business turned a profit. California, for example, requires LLCs to pay an $800 annual minimum franchise tax plus an additional fee based on gross receipts above $250,000. Check your state's department of revenue website to confirm what your entity owes at the state level before you file anything federally.

Many states also require separate withholding registrations or annual report filings that have nothing to do with income tax. Missing these is a common mistake for business owners who focus entirely on federal compliance and assume the state automatically follows. Build state obligations into your filing calendar from the start so you avoid preventable penalties and keep your business in good standing across every jurisdiction where you operate.

Step 4. Claim deductions and credits correctly

Deductions reduce your taxable income, while credits reduce the actual tax you owe dollar-for-dollar. Both matter, but they work differently, and claiming them incorrectly is one of the most common reasons business owners end up with an amended return or an IRS notice. Whether you are handling business tax filing help on your own or working with a professional, you need to know what you qualify for before you file.

Common deductions business owners miss

Most business owners know they can deduct rent and supplies, but several deductions get overlooked or miscalculated every year. The home office deduction, for example, requires that you use a specific area of your home regularly and exclusively for business. You can calculate it using the simplified method ($5 per square foot, up to 300 square feet) or the regular method based on actual expenses proportional to your office space. The regular method typically produces a larger deduction but requires more documentation.

Here are the deductions most frequently underclaimed or misapplied by small business owners:

- Vehicle expenses: You can deduct actual vehicle costs or use the IRS standard mileage rate (67 cents per mile for 2024). You must keep a mileage log with dates, destinations, and business purposes.

- Section 179 and bonus depreciation: You can deduct the full cost of qualifying equipment in the year you place it in service rather than depreciating it over several years.

- Health insurance premiums: Self-employed owners can deduct 100% of premiums paid for themselves and their families, subject to income limits.

- Retirement contributions: Contributions to a SEP-IRA, SIMPLE IRA, or solo 401(k) reduce your taxable income and are fully deductible up to annual IRS limits.

- Professional services: Fees paid to accountants, attorneys, and consultants for your business are fully deductible in the year you pay them.

Business tax credits to check before you file

Credits reduce your tax liability directly, making them more valuable than equivalent deductions. The Small Business Health Care Tax Credit is available to employers with fewer than 25 full-time equivalent employees who pay at least half of employee premium costs. The Work Opportunity Tax Credit rewards you for hiring workers from specific groups, including veterans and long-term unemployment recipients.

Do not confuse a tax credit with a deduction. A $5,000 credit cuts your tax bill by $5,000; a $5,000 deduction only reduces the income on which your tax is calculated.

Check the IRS credits and deductions page for businesses to confirm which credits your entity type qualifies for before you finalize your return.

Step 5. Handle payroll, sales tax, and 1099s

Three compliance areas sit outside your income tax return but directly affect your annual filing: payroll taxes, sales tax, and information returns like 1099s. Missing any of these is one of the fastest ways to generate IRS notices and state agency penalties before your main return is even reviewed. Sorting them out before you file is a critical part of getting solid business tax filing help.

Payroll taxes and quarterly deposits

If you pay employees, you owe federal payroll taxes that you must deposit on a schedule the IRS determines based on your total tax liability. Most small employers deposit monthly or semi-weekly, using the Electronic Federal Tax Payment System (EFTPS). You also file Form 941 each quarter to report wages paid and taxes withheld.

Confirm each of the following before you file your annual return:

- All Form 941 filings for Q1 through Q4 are submitted and match your deposit records

- W-2s were distributed to employees by January 31 and filed with the Social Security Administration

- Federal and state unemployment tax returns (FUTA/SUTA) are current and fully paid

If your payroll tax deposits do not match what you report on your annual return, the IRS will flag the discrepancy automatically.

Sales tax obligations

Sales tax is a state-level obligation, not a federal one, but it still affects your books and your filing accuracy. If you collect sales tax from customers and your accounting records do not match your state remittances, your revenue figures will appear inconsistent when you close the books. Check that every sales tax payment you made during the year is recorded correctly in your accounting software and reconciled against your state sales tax returns.

Your nexus obligations may extend beyond your home state if you sell products or services into other states above certain revenue or transaction thresholds. Several states enforced economic nexus rules following the 2018 South Dakota v. Wayfair Supreme Court decision, so confirm your exposure before assuming you only owe sales tax in one state.

1099-NEC filings for contractors

You must file Form 1099-NEC for every unincorporated contractor or freelancer you paid $600 or more during the tax year. These were due to recipients by January 31 and to the IRS by the same date if filed electronically. If you missed the deadline, file them now and expect a penalty per form, which the IRS assesses based on how late you submit.

Collect a Form W-9 from every contractor before you pay them, not after. Having W-9s on file eliminates the year-end scramble and ensures you have the taxpayer identification number you need to prepare accurate 1099s without delay.

Step 6. File and pay on time

Once your forms are complete and your records are reconciled, getting your return submitted by the correct deadline is the final piece of solid business tax filing help. Filing late triggers automatic failure-to-file penalties, which the IRS calculates at 5% of unpaid tax per month, up to 25%. A separate failure-to-pay penalty adds another 0.5% per month. Both run simultaneously if you file late and owe money, so the cost of missing a deadline compounds fast.

Know your deadlines by entity type

Your filing deadline depends on your entity type and the end of your tax year. Most small businesses operate on a calendar year ending December 31, which sets the following federal deadlines:

| Entity Type | Federal Filing Deadline | Extension Deadline |

|---|---|---|

| Sole Proprietor / Single-Member LLC | April 15 | October 15 |

| Partnership / Multi-Member LLC | March 15 | September 15 |

| S-Corporation | March 15 | September 15 |

| C-Corporation | April 15 | October 15 |

Partnerships and S-corporations face an earlier March 15 deadline because partners and shareholders need their K-1s before they can complete their own personal returns.

State deadlines do not always match federal ones, so check your state's department of revenue for the exact due dates that apply to your entity before you finalize your filing calendar.

What to do if you owe money you don't have

Owing more than you can pay in full does not mean you should skip filing. Filing on time and paying what you can stops the failure-to-file penalty from accumulating, which is the steeper of the two charges. Submit your return by the deadline, pay as much as you can with it, and then apply for an IRS payment plan using Form 9465 or through the IRS Online Payment Agreement tool at IRS.gov.

How to request an extension

Filing an extension gives you six additional months to submit your return, but it does not extend your time to pay any tax you owe. Use Form 4868 for individual and sole proprietor returns, and Form 7004 for partnerships, S-corporations, and C-corporations. Submit the extension by the original deadline and include a payment for your estimated tax liability to avoid the failure-to-pay penalty during the extension period. An extension filed without payment when you owe will not protect you from interest and penalties on the unpaid balance.

Costs: software vs CPA or enrolled agent

Understanding what business tax filing help costs before you commit to a method prevents surprises and helps you weigh the real trade-offs. The price gap between software and a professional is real, but it does not tell the whole story. What you save on preparation fees, you can easily lose through missed deductions, filing errors, or penalties that a qualified professional would have caught.

What tax software typically costs

Tax software handles straightforward returns well, and the upfront price is often the main reason business owners choose it. Most platforms charge a base fee plus an additional charge for business forms, state returns, and any add-ons you select during the filing process.

| Software Tier | Typical Cost Range | Best For |

|---|---|---|

| Self-employed / Schedule C | $80 to $130 | Sole proprietors, single-member LLCs |

| Partnership or S-corp returns | $170 to $300+ | Multi-member LLCs, S-corps with simple books |

| State return add-on | $40 to $60 per state | Any entity with state filing obligations |

Time is a real cost that these price tags do not reflect. If your books are messy or your situation is at all complex, you can spend 10 to 20 hours navigating software prompts, looking up IRS rules, and second-guessing your answers. That time has value, and mistakes made under pressure have a dollar amount attached to them too.

What a CPA or Enrolled Agent charges

Professional fees vary based on your entity type, the complexity of your return, and whether you need resolution work alongside standard filing. A straightforward Schedule C through a CPA typically runs between $300 and $600. An S-corporation return with payroll coordination and multiple K-1s can range from $900 to $2,500 or more.

The complexity of your books and your history of filing accurately are the two biggest factors that drive what a professional will charge you.

Enrolled Agents often charge similar rates to CPAs for tax preparation work, and they hold the same authority to represent you before the IRS. If your primary concern is accuracy and IRS representation rather than broader financial advisory work, an Enrolled Agent delivers strong value at a competitive price point. Many firms, including Tax Experts of OC, offer transparent upfront pricing and payment plans for clients who owe and cannot pay the full preparation fee at once.

When you should hire a pro

Software handles clean, simple returns well. But your situation may have moved past what a self-service tool can manage safely. Recognizing when to bring in a CPA or Enrolled Agent for business tax filing help is not about admitting defeat; it is about protecting your money, your business, and your time from errors that carry real financial consequences.

Your return involves complexity that software cannot navigate safely

Tax software follows a decision tree. It does not advise you, flag planning opportunities, or catch problems that fall outside its programmed prompts. You need a professional when your return involves multiple entity layers, such as an S-corp owned partly by a trust, or when you have partners in multiple states, depreciation recapture, or a change in ownership structure during the year.

Here are the clearest signals that your situation requires a professional rather than software:

- You run more than one business entity and transactions flow between them

- You converted your LLC to an S-corp during the year and need to file a short-year return

- You have employees in multiple states with split payroll tax obligations

- You sold a business asset and need to calculate capital gain or depreciation recapture

- You missed quarterly estimated payments and expect to owe penalties and interest

- Your gross revenue exceeds $500,000 and your deductions involve significant documentation

If any one of these applies to you, the cost of a professional will almost always be lower than the cost of the mistake you would otherwise make.

You have outstanding IRS issues

Unfiled prior-year returns, IRS notices, liens, or levies require representation, not just preparation. The IRS allows only Enrolled Agents, CPAs, and tax attorneys to represent clients directly before the agency. A general preparer or software product cannot negotiate on your behalf, respond to an audit, or set up an installment agreement with the authority those credentials carry.

Your time has a dollar value

Spending 15 hours navigating a complex business return through software costs you more than a professional's fee once you account for your hourly rate and the opportunity cost of time pulled from your business. Calculate what one hour of your time is worth, multiply it by a realistic estimate of how long the return will take you, and compare that figure against what a qualified preparer charges. For most business owners dealing with anything beyond a single-entity, single-state return, hiring a pro nets out ahead financially, even before you account for deductions you would have missed on your own.

If the IRS contacts you after filing

Getting a letter from the IRS after you submit your return does not automatically mean you did something wrong. The agency sends notices for dozens of reasons, ranging from a simple math adjustment to a formal audit request. Reading the notice carefully before you respond is the single most important first step, because the type of correspondence you received determines what action you need to take and how quickly you need to take it.

What different IRS notices mean

Not every IRS letter carries the same weight, and treating them all as emergencies wastes your time while ignoring them creates real problems. The IRS uses CP and LT series codes to categorize its correspondence. A CP2000 notice, for example, means the IRS found income reported by a third party, such as a 1099, that does not match what appears on your return. An LT11 or CP90 is a notice of intent to levy, which carries urgent legal deadlines you cannot miss.

Here are the most common post-filing notices and what they signal:

| Notice | What It Means | Urgency |

|---|---|---|

| CP2000 | Income mismatch; IRS proposes changes | Respond within 60 days |

| CP501 / CP503 | Balance due reminder | Pay or respond promptly |

| CP504 | Intent to levy state tax refund | Act within 30 days |

| LT11 / CP90 | Final notice before levy | Respond immediately |

| CP75 | Audit of specific credits such as EIC | Respond with documentation |

How to respond without making things worse

Never ignore an IRS notice, regardless of how minor it looks. Ignoring correspondence does not make the issue disappear; it triggers escalating collection actions, including liens and levies, that are far harder and more expensive to resolve than the original problem. Read the response deadline stated in the notice, confirm whether the IRS's position is actually correct, and gather any documentation that supports your return as originally filed.

If the IRS is wrong, you have the right to dispute their proposed changes in writing with supporting evidence before any adjustment becomes final.

When the notice involves an audit, a levy threat, or a significant balance, professional business tax filing help shifts from useful to essential. An Enrolled Agent or CPA can respond directly on your behalf, handle all IRS communication, and negotiate outcomes such as penalty abatement or an installment agreement. Reach out to a qualified representative before you respond to any notice that involves money owed or a formal examination of your return.

Next steps

You now have a complete roadmap for handling business tax filing help from start to finish, covering entity status, recordkeeping, correct forms, deductions, payroll compliance, deadlines, costs, and what to do when the IRS reaches out. The path forward is straightforward: confirm your entity classification, close your books, match your situation to the right forms, and file by your deadline. If any step in that sequence involves complexity you are not equipped to handle alone, bring in a qualified professional before you file rather than after a problem surfaces.

Your next action depends on where you are right now. If your books are clean and your return is simple, use this guide as your checklist. If you have unfiled returns, IRS notices, or a complicated entity structure, get professional representation before the April 15 or March 15 deadline passes. The Tax Experts of OC team is available for a free 30-minute consultation to help you figure out exactly what you need.