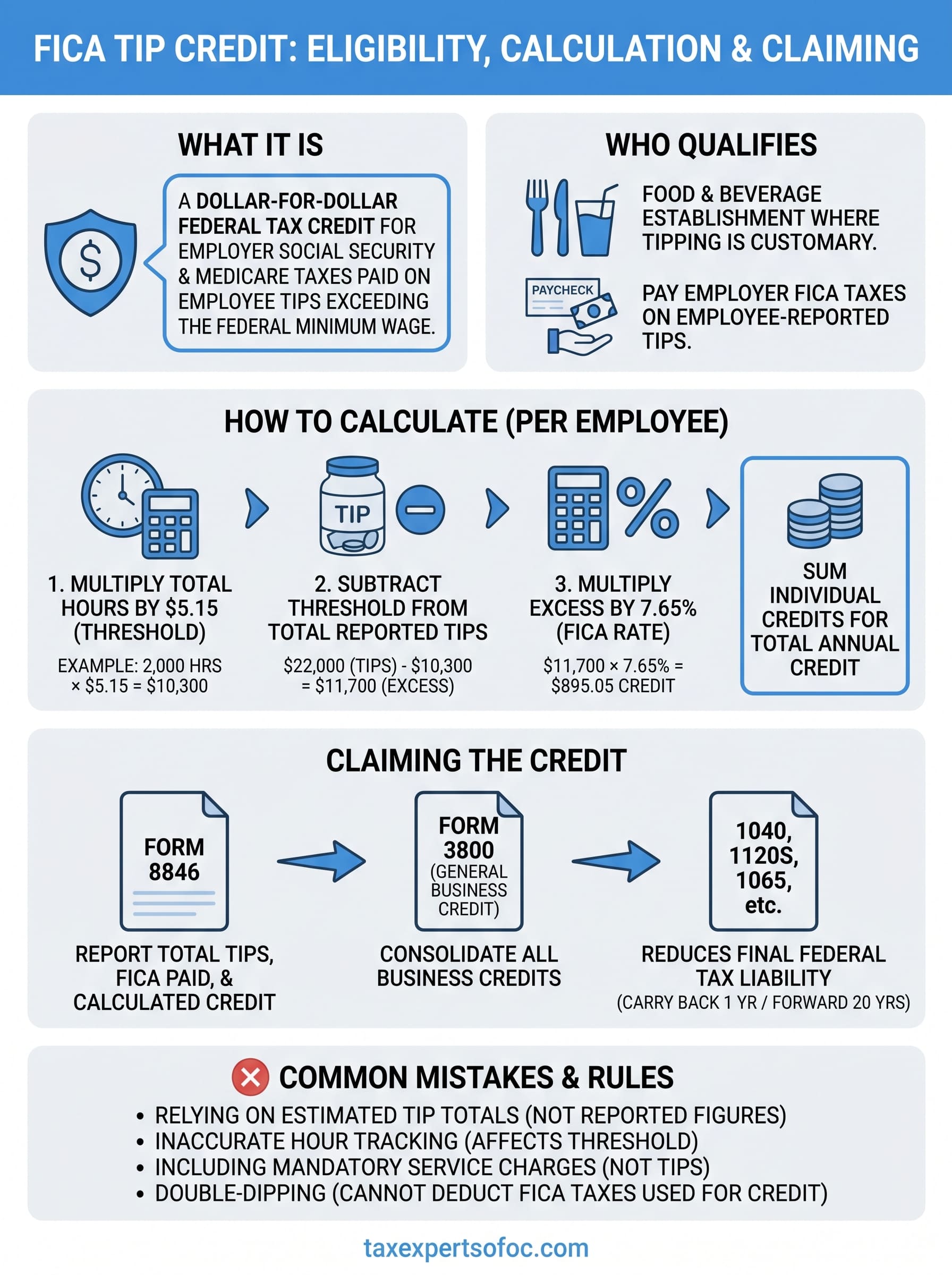

If you own or manage a restaurant, bar, or any food and beverage establishment where employees earn tips, you may be leaving money on the table at tax time. The FICA tip credit lets eligible employers claim a dollar-for-dollar tax credit for the Social Security and Medicare taxes they pay on employee tips that exceed the federal minimum wage. It's one of the most underused credits in the industry, often because business owners either don't know it exists or find the calculation process confusing.

The credit is claimed through IRS Form 8846, and when done correctly, it can reduce your federal tax liability by thousands of dollars each year. But eligibility rules, tip allocation thresholds, and proper documentation all need to be airtight, or you risk missing out on the credit entirely.

This guide breaks down who qualifies for the FICA tip credit, how the calculation works step by step, and what you need to file Form 8846 accurately. At Tax Experts of OC, our CPAs and Enrolled Agents help restaurant and hospitality business owners across all 50 states claim every credit they're entitled to, this one included. If the math feels overwhelming, that's exactly where we come in.

What the FICA tip credit is and why it exists

When an employee receives a tip, the IRS treats it as taxable wages. That means you, the employer, owe Social Security and Medicare taxes (commonly called FICA taxes) on those tips, just as you do on regular hourly or salaried wages. For restaurants, bars, and similar food and beverage businesses where tipping is a standard part of the customer experience, this creates a recurring tax obligation that grows in direct proportion to how much your customers tip, a cost that is entirely outside your control.

The tax burden employers carry on tips

The employer FICA tax rate is 7.65%, which breaks down to 6.2% for Social Security and 1.45% for Medicare. On paper, that percentage sounds manageable. But when you apply that rate across dozens of tipped employees working hundreds of shifts throughout the year, the total employer FICA cost on tip income alone can climb into tens of thousands of dollars annually for a mid-sized restaurant or bar. You never touch that tip money directly, customers hand it to your employees, yet you are still responsible for the tax liability attached to every dollar tipped.

This dynamic puts food and beverage employers in an unusual position compared to most other industries. Your payroll tax obligation scales with customer generosity rather than with any wage or compensation decision you make internally.

Why Congress created the credit

Congress introduced the FICA tip credit in 1993 as part of the Omnibus Budget Reconciliation Act. The purpose was straightforward: tip income was being reported and taxed more consistently than it had been in prior decades, and lawmakers recognized that employers were bearing a real financial cost on money they never actually received. The credit was designed to offset a portion of that burden and give employers a concrete reason to encourage accurate tip reporting across the industry.

The FICA tip credit does not reduce your taxable income the way a deduction does. It reduces your actual federal tax bill, dollar for dollar, which makes it significantly more valuable than a standard business deduction of the same amount.

What makes this credit different from a deduction

Many business owners treat tax credits and tax deductions as interchangeable concepts, but they operate very differently. A deduction reduces the income you pay tax on. So a $10,000 deduction saves you roughly $2,200 if you are in the 22% bracket. A credit, by contrast, reduces your final tax liability directly, dollar for dollar, regardless of your tax bracket. If you qualify for a $10,000 FICA tip credit, you subtract $10,000 straight from what you owe the IRS.

The FICA tip credit is classified as a general business credit, which means it flows through IRS Form 8846 and then onto Form 3800 if you are combining it with other business credits. If the credit exceeds your tax liability for the year, you are not out of luck. You can carry it back one year or carry it forward up to 20 years, which means the benefit does not evaporate if your current-year bill happens to be low. That carry-forward provision makes it worth claiming even in lower-revenue years.

Who qualifies and what tips count

Not every tipped business qualifies for the FICA tip credit. The IRS restricts this credit to employers in the food and beverage industry where customers routinely tip as part of normal service. Restaurants, bars, cafes, hotel restaurants, and similar food service establishments fit that description clearly. A nail salon or barbershop where clients tip workers does not qualify under this provision, even though tipping happens there on a regular basis.

If your business operates outside the food and beverage industry, the FICA tip credit is not available to you regardless of how much your employees earn in tips.

Employer eligibility requirements

To qualify, your business must satisfy two core conditions. First, you must operate a food or beverage establishment where tipping is a customary practice, meaning customers tip as a matter of course rather than as a rare occurrence. Second, you must pay employer FICA taxes on the tips your employees report to you. If you are already remitting Social Security and Medicare taxes on employee-reported tips as federal law requires, you meet that second condition automatically.

Your business entity type does not affect eligibility on its own. The credit is available to sole proprietors, partnerships, S corporations, and C corporations equally. Even if you operate multiple locations under one entity, you can still qualify as long as each location meets the food and beverage criteria. What matters is the nature of your business and whether you are correctly collecting and remitting FICA taxes on reported tip income.

What types of tips count

Cash tips left directly by customers and credit card tips that you pay out through payroll both count toward the credit, provided your employees report them to you in writing. Employer-imposed service charges, sometimes called mandatory gratuities added automatically to large-party bills, do not qualify as tips under this rule because they are not discretionary on the customer's part.

Beyond tip type, there is also a wage floor built into the formula. Only tips that push an employee's total hourly compensation above $5.15 per hour qualify for the credit calculation. That figure represents the federal minimum wage as it stood in 2007, and the statute froze it there. Tips that only bring an employee up to that threshold do not generate the credit, but you still owe FICA on the full reported tip amount either way.

How to calculate the FICA tip credit

The calculation follows a straightforward formula, but you need accurate payroll records for every tipped employee before you begin. Specifically, you need each employee's total reported tip income for the tax year and their total hours worked during that same period. Without those two data points per employee, any number you produce will be unreliable, and the IRS will have grounds to dispute your credit claim. You also run the calculation separately for each individual employee, not as a single lump sum across your entire team.

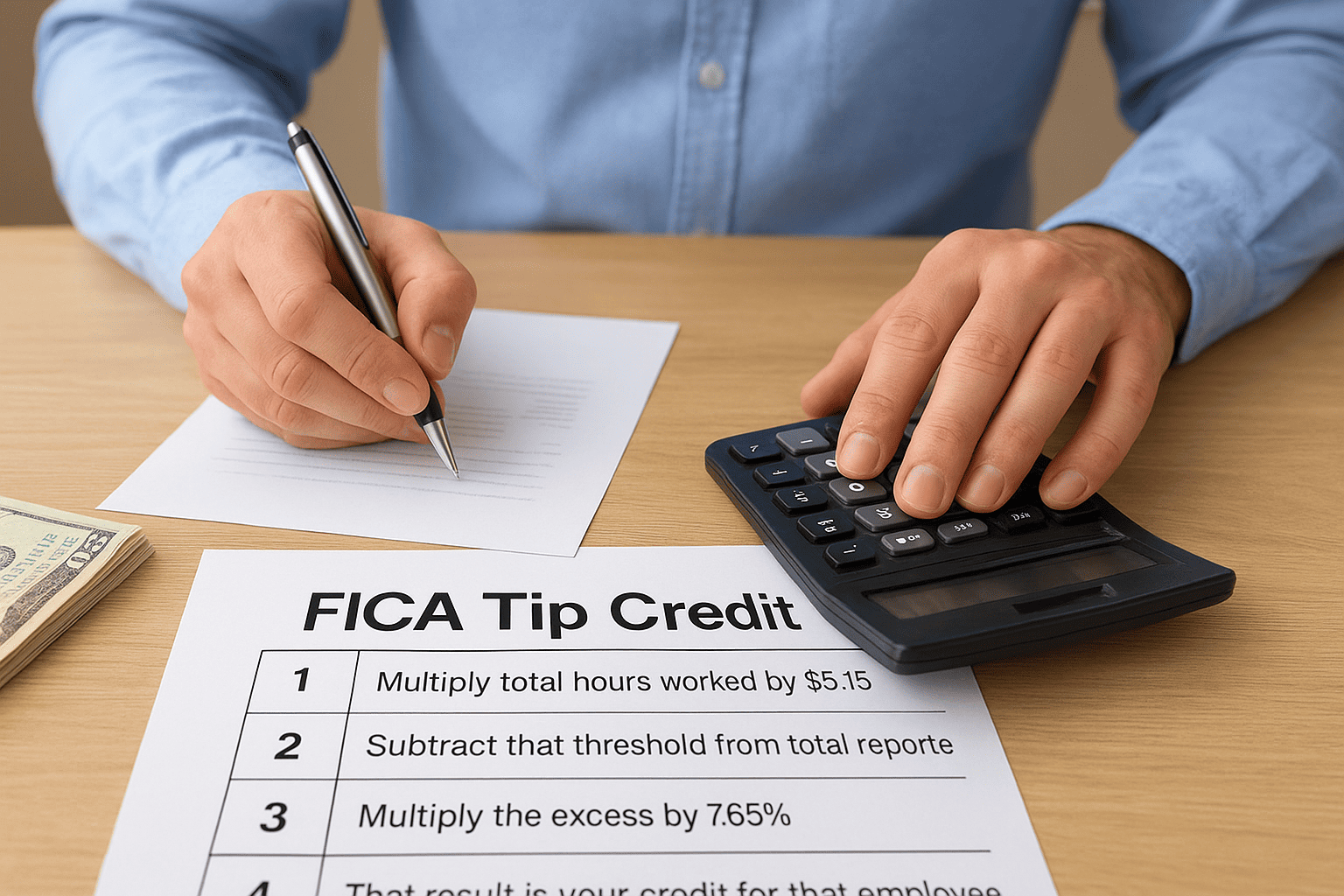

The core formula

The IRS limits the FICA tip credit to the employer FICA taxes paid on tips that push an employee's hourly compensation above $5.15. That $5.15 figure represents the federal minimum wage as it stood in 2007, and the statute governing this credit froze it there permanently. The three-step calculation works as follows: multiply the employee's total hours worked for the year by $5.15 to find the threshold amount. Subtract that threshold from the employee's total reported tips for the year. Then apply the 7.65% employer FICA rate to the remaining excess. The dollar result is the credit attributable to that one employee. Part-time and seasonal employees follow the same process, just with fewer total hours in the threshold calculation.

| Step | What you do |

|---|---|

| 1 | Multiply total hours worked by $5.15 |

| 2 | Subtract that threshold from total reported tips |

| 3 | Multiply the excess by 7.65% |

| 4 | That result is your credit for that employee |

Run this calculation separately for every tipped employee on your payroll, then add all individual results together to arrive at your total annual credit.

A worked example

Suppose one of your servers worked 2,000 hours during the year and reported $22,000 in tips. Multiply 2,000 by $5.15 to get a threshold of $10,300. Subtract $10,300 from $22,000 to find $11,700 in qualifying excess tips. Multiply $11,700 by 7.65%, and the credit for that one employee comes to $895.05.

Extend that math across a restaurant with 15 tipped employees earning similar tip volumes, and your total annual credit can reach $12,000 or more. Worth noting: you still owe employer FICA on the full reported tip amount, including the portion below the $5.15 threshold. You just do not get credit for that lower portion. Keeping clean payroll records, accurate tip reports, and verified hour counts for every employee throughout the year is where most businesses run into real trouble with this credit.

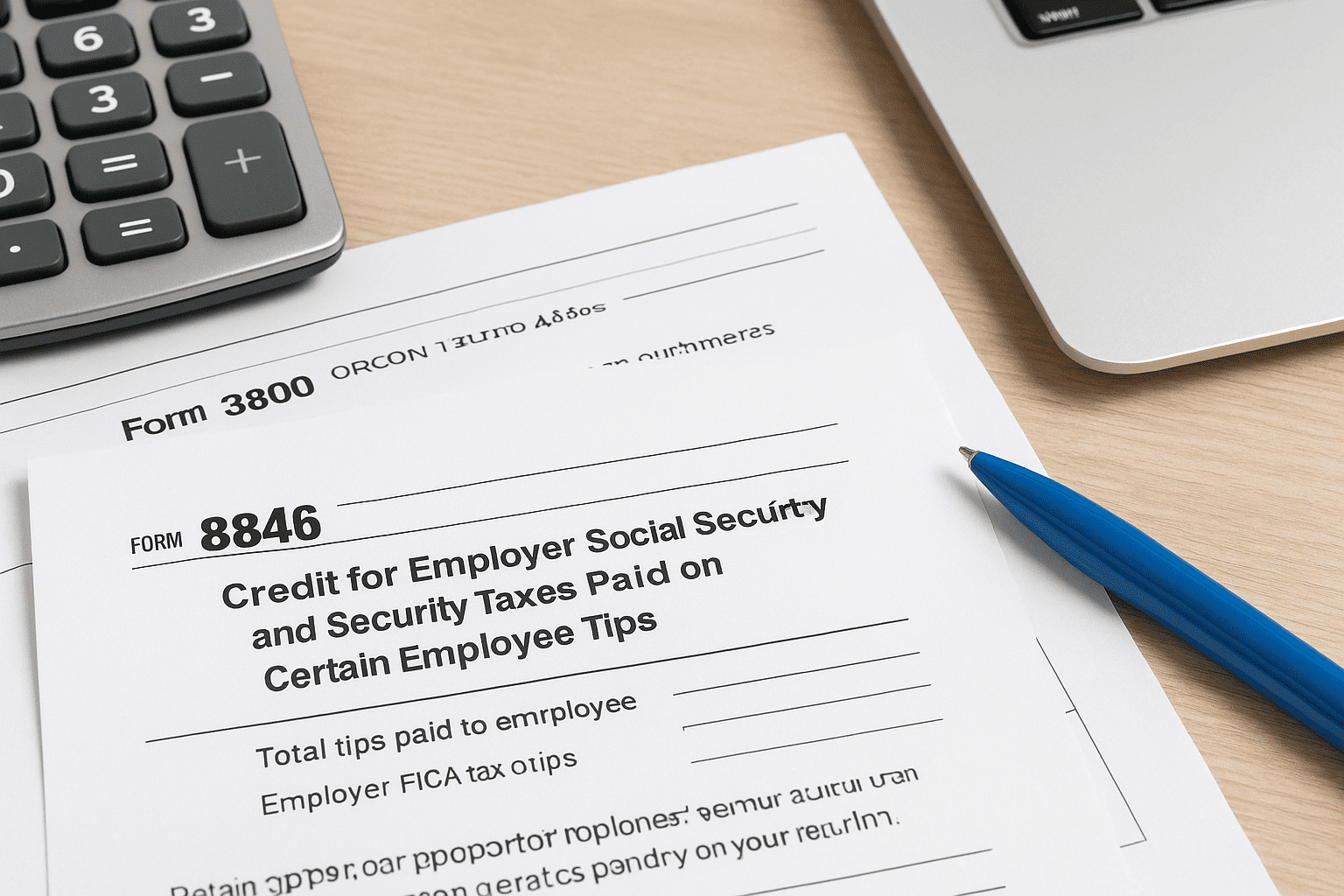

How to claim it with IRS Form 8846

Once you have completed the per-employee calculation and totaled your credit amount, you report the FICA tip credit using IRS Form 8846, officially titled "Credit for Employer Social Security and Medicare Taxes Paid on Certain Employee Tips." The form is straightforward by IRS standards, but the accuracy of what you enter depends entirely on the payroll data you compiled throughout the year. Filing an incorrect amount or using estimates instead of verified figures gives the IRS a clear reason to challenge your claim.

What Form 8846 requires

Form 8846 asks you to report your total tips paid to employees and the employer FICA taxes you paid on those tips. You enter your aggregate credit figure after running the individual employee calculations described in the previous section. The form also asks you to confirm the nature of your business, specifically that you operate a food or beverage establishment where tipping is customary. Keep all your supporting payroll records, tip logs, and employee hour totals on file, because the IRS can request documentation to verify any figure you report.

Retain tip reports, payroll registers, and hour records for at least three years after filing, since that window aligns with the standard IRS audit lookback period for most returns.

How Form 8846 connects to your return

Form 8846 does not stand alone on your tax return. The credit amount calculated on Form 8846 flows directly onto IRS Form 3800, the General Business Credit form, which consolidates all eligible business credits before they reduce your final federal tax liability. If you operate as a sole proprietor or single-member LLC filing on Schedule C, the combined credit from Form 3800 then transfers to your Form 1040. Partnerships and S corporations calculate the credit at the entity level and pass it through to partners or shareholders on Schedule K-1, who then claim it individually on their own returns.

Your tax preparer or software must generate both Form 8846 and Form 3800 correctly and link them to the right return type. A disconnect between those two forms is one of the more common filing errors the IRS flags when reviewing business credit claims. Getting the filing chain right from the start saves you from amended returns and potential penalties later.

Common mistakes and related rules to know

Even businesses that know the FICA tip credit exists often leave money unclaimed because of avoidable errors in record-keeping or filing. Understanding where other employers go wrong helps you stay on the right side of the IRS and protect the credit you earned throughout the year.

Errors that invalidate or reduce your claim

The most common mistake is relying on estimated tip totals rather than actual employee-reported figures. If your employees do not submit written tip reports each pay period, you have no verified basis for the numbers you enter on Form 8846, and the IRS can disallow your credit entirely during an audit. A close second is failing to track hours accurately. Since the formula multiplies each employee's hours by $5.15 to establish the threshold, even small errors in hour counts can shift your credit amount up or down in ways that draw scrutiny. Keep payroll registers and tip logs current throughout the year, not just at tax time.

Reconstructing tip records after the fact is difficult and rarely holds up under IRS review, so accurate tracking during the year is non-negotiable.

Another error involves mandatory service charges. Some restaurants add automatic gratuities to large-party bills and mistakenly include those amounts in the tip credit calculation. Because those charges are not discretionary, the IRS does not treat them as tips, and including them inflates your credit claim beyond what the law allows.

The wage deduction tradeoff

There is a related rule that catches many business owners off guard: you cannot deduct the same FICA taxes you use to calculate the credit. The IRS prohibits double-dipping, so the employer FICA taxes you claim through Form 8846 must be removed from your wage deduction on your business return. If you take both, you are effectively receiving the same tax benefit twice, which is a clear audit trigger.

Your total tax outcome still favors claiming the credit over the deduction in most cases, because a dollar-for-dollar credit reduces your tax bill more than a deduction of the same amount would. Running both numbers with a qualified tax professional confirms which approach puts more money back in your pocket for your specific situation.

Next steps

The FICA tip credit is a legitimate, dollar-for-dollar reduction in your federal tax bill, but only if you track tip income accurately, run the per-employee calculation correctly, and file Form 8846 in the right sequence with Form 3800. Miss any one of those steps, and you either leave money unclaimed or hand the IRS grounds to dispute your return.

Start by reviewing your current payroll records to confirm that every tipped employee is submitting written tip reports each pay period. From there, verify that your hour tracking is precise enough to support the $5.15 threshold calculation for each worker.

If any part of this process feels unclear, or if you want a qualified professional to review your prior returns for missed credits, the team at Tax Experts of OC can help. Our CPAs and Enrolled Agents work with food and beverage employers nationwide to make sure you claim every dollar you are entitled to.