Hiring your first employee is a milestone. But the excitement fades fast when you realize you need to figure out how to set up payroll, and get it right from day one. Miss a filing deadline or misclassify a worker, and the IRS will come knocking with penalties that can sting a small business hard.

The good news: payroll setup isn't as complicated as it looks once you break it down into clear steps. You need the right registrations, the right forms, and a reliable system to calculate wages, withhold taxes, and submit payments on time. Skip a step, though, and you're building on a shaky foundation.

At Tax Experts of OC, we help small business owners across all 50 states handle payroll, tax compliance, and everything that comes with being an employer. Our CPAs and Enrolled Agents work directly with clients, no runaround, no generic advice. This guide walks you through the full payroll setup process, from obtaining your EIN to running your first pay cycle, so you can pay your team with confidence and stay on the right side of the IRS.

What you need before you set up payroll

Before you touch a single payroll calculation, you need to gather specific information and complete key registrations. Trying to figure out how to set up payroll without these in place leads to filings with missing numbers, incorrect withholdings, and penalties that accumulate fast. Getting organized before day one saves you from scrambling to fix mistakes after employees have already been paid and tax deposits are overdue.

Your federal and state employer IDs

Your Employer Identification Number (EIN) is the foundation of everything payroll-related. The IRS uses it to track your payroll tax deposits, match your quarterly filings, and identify your business as an employer. If you don't have one yet, apply for free directly at IRS.gov. You'll receive it immediately upon completing the online application, so there's no reason to wait.

Most states also require a separate state employer tax ID to remit state income tax withholdings and pay state unemployment insurance (SUTA). Each state manages this registration differently, so check your state's department of revenue or department of labor website to find the correct portal, forms, and deadlines before you hire anyone.

Register for both your federal EIN and state employer ID before you run your first payroll. Depositing taxes without these numbers in place creates reporting problems that take significant time and professional help to untangle later.

Employee documents you must collect

Every employee needs to complete two federal forms before their first day of work. The Form I-9 verifies that the person is legally authorized to work in the United States, and you must review their supporting documents in person or through an authorized remote verification process. The Form W-4 tells you exactly how much federal income tax to withhold from each paycheck based on the employee's filing status and withholding adjustments.

Here's what to collect from every new hire before processing their first paycheck:

- Completed Form W-4 (Employee's Withholding Certificate)

- Completed Form I-9 with valid supporting identity documents

- Direct deposit authorization form with bank routing and account number

- State withholding form, if your state collects income tax

Store these documents securely and keep them accessible for at least three years after the employment date. Both the IRS and the Department of Homeland Security can request them during an audit or worksite inspection.

Your payroll structure decisions

Two practical decisions need to be locked in before you run payroll: a dedicated business bank account and a defined pay schedule. Running payroll from a personal account blurs your financial records and creates bookkeeping headaches that grow more painful at tax time. Open a separate payroll account so every tax deposit and paycheck clears through a clean, traceable ledger.

Your pay frequency also needs to be set upfront. Options include weekly, biweekly, semimonthly, or monthly. Some states set minimum pay frequency requirements by law, so verify your state's labor regulations before deciding. Once employees know their schedule, changing it mid-employment requires advance notice and, in some states, regulatory approval.

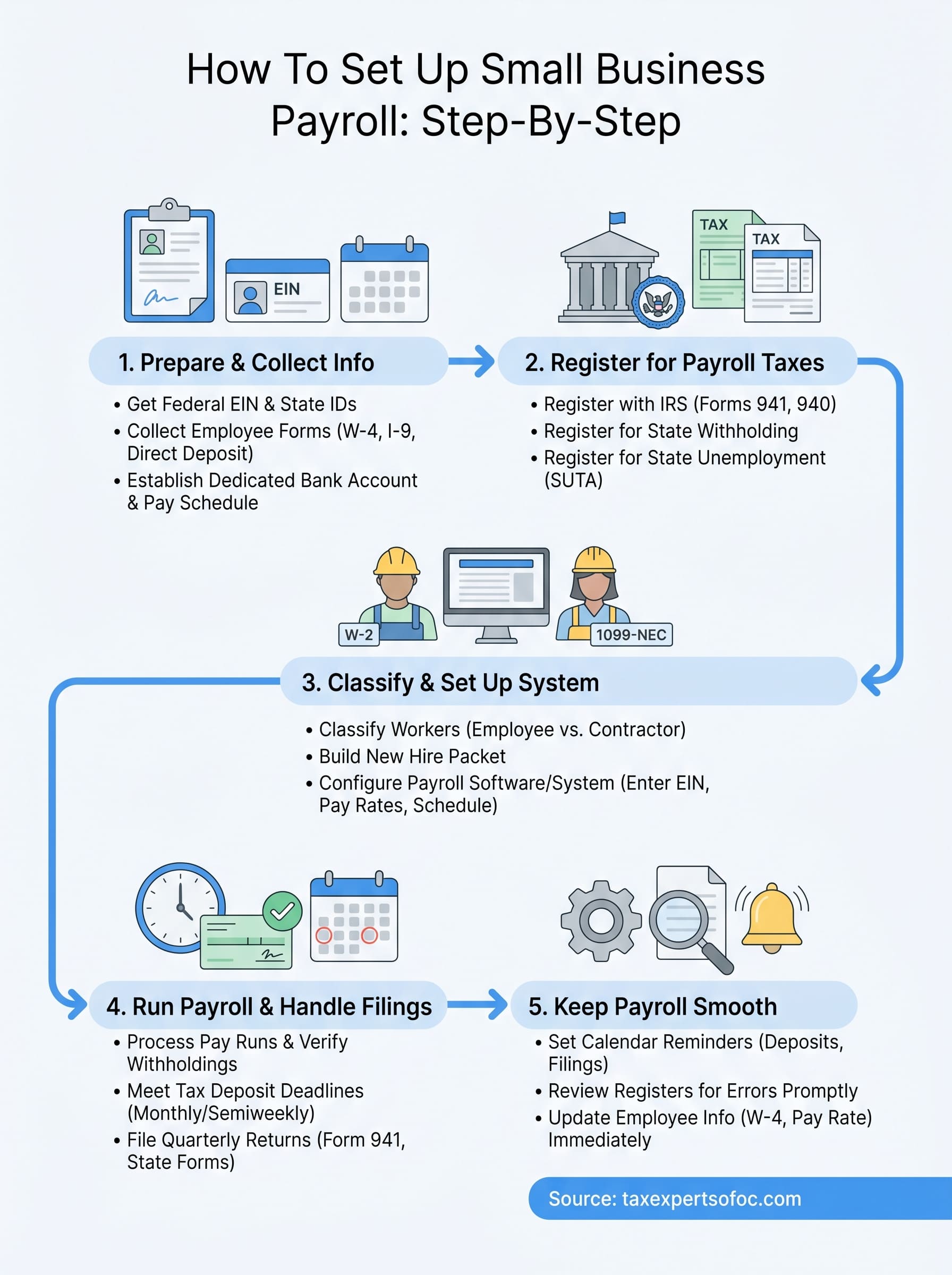

Step 1. Register your business for payroll taxes

Registration is the first concrete action you take when figuring out how to set up payroll. Without the correct accounts in place, you have nowhere to remit your tax deposits and no account number to put on your federal and state filings. Complete this step before you process a single paycheck.

Register with the IRS

Your federal registration is straightforward: if you already have an EIN from setting up your business, you are ready to go. The IRS automatically associates payroll tax obligations with your EIN once you start filing employment tax returns. If you do not have an EIN yet, apply at IRS.gov and receive your number immediately upon completing the online form.

Once you have your EIN, you need to know which federal payroll tax forms apply to you:

- Form 941 (Employer's Quarterly Federal Tax Return): filed four times a year to report withheld income tax, Social Security, and Medicare taxes.

- Form 940 (Employer's Annual FUTA Tax Return): filed once a year to report your federal unemployment tax liability.

- Form W-2: issued to each employee by January 31 each year, summarizing their annual wages and withholdings.

Missing a Form 941 deadline triggers a penalty of 5% of the unpaid tax per month, up to 25%, so calendar every deposit and filing due date the moment you hire your first employee.

Register with your state

State registration requirements vary significantly depending on where your business operates. Most states require you to register separately for two obligations: state income tax withholding and state unemployment insurance (SUTA). Visit your state's department of revenue to open a withholding account and your state's department of labor to register for unemployment insurance.

Several states, including Florida and Texas, impose no state income tax, so you only handle the SUTA registration there. Confirm both requirements before your first pay date to avoid late registration fees and frozen accounts.

Step 2. Collect employee info and classify workers

Collecting the right information upfront is one of the most important parts of learning how to set up payroll correctly. If you skip classification or collect forms out of order, you risk withholding the wrong amounts, missing required filings, and exposing your business to IRS penalties for misclassification.

Employees vs. independent contractors

Worker classification determines everything: which taxes you withhold, which forms you file, and what your legal obligations are as a payer. Employees receive a W-2 at year-end, and you withhold federal income tax, Social Security, and Medicare from each paycheck. Independent contractors receive a Form 1099-NDA only if you pay them $600 or more in a calendar year, and you do not withhold any taxes on their behalf.

The IRS uses a behavioral control, financial control, and relationship test to determine classification. Misclassifying an employee as a contractor can result in back taxes, interest, and penalties covering all the payroll taxes you should have withheld.

Use this table to quickly distinguish between the two:

| Factor | Employee | Independent Contractor |

|---|---|---|

| Tax withholding | You withhold and remit | They handle their own |

| Work schedule control | You set it | They set it |

| Tools and equipment | You typically provide | They use their own |

| Year-end form | W-2 | 1099-NEC (if $600+) |

Build a new hire packet

Once you confirm a worker is an employee, collect their required documents before processing their first paycheck. A complete new hire packet keeps your records clean and your filings accurate from the start.

Your packet should include:

- Form W-4 (federal withholding elections)

- Form I-9 with valid identity documents reviewed by you

- State withholding form, if applicable

- Direct deposit authorization with bank routing and account numbers

- Emergency contact and benefits enrollment forms, if applicable

Keep all completed documents in a secure personnel file for a minimum of three years after the employment end date.

Step 3. Choose a payroll system and set it up

The system you use to run payroll determines how accurately and consistently you process wages, withhold taxes, and meet filing deadlines. This is the part of how to set up payroll where your earlier preparation pays off. You already have your EIN, your state IDs, and your employee documents. Now you need a reliable method to turn those inputs into correct paychecks and accurate tax deposits on every single pay date.

Manual processing vs. payroll software

Manual payroll means calculating gross wages, tax withholdings, and net pay yourself using IRS Publication 15-T withholding tables and your state's equivalent. It costs nothing in software fees, but the margin for error is high. A single miscalculation in federal income tax withholding compounds across every pay period and creates reconciliation problems when you file your quarterly Form 941.

Payroll software automates tax calculations, generates pay stubs, handles direct deposit, and often files federal and state payroll taxes on your behalf. For most small businesses with even one or two employees, software saves more time than it costs.

If you have employees in more than one state, manual payroll becomes impractical fast. Each state has different withholding tables, unemployment rates, and filing schedules that software handles automatically.

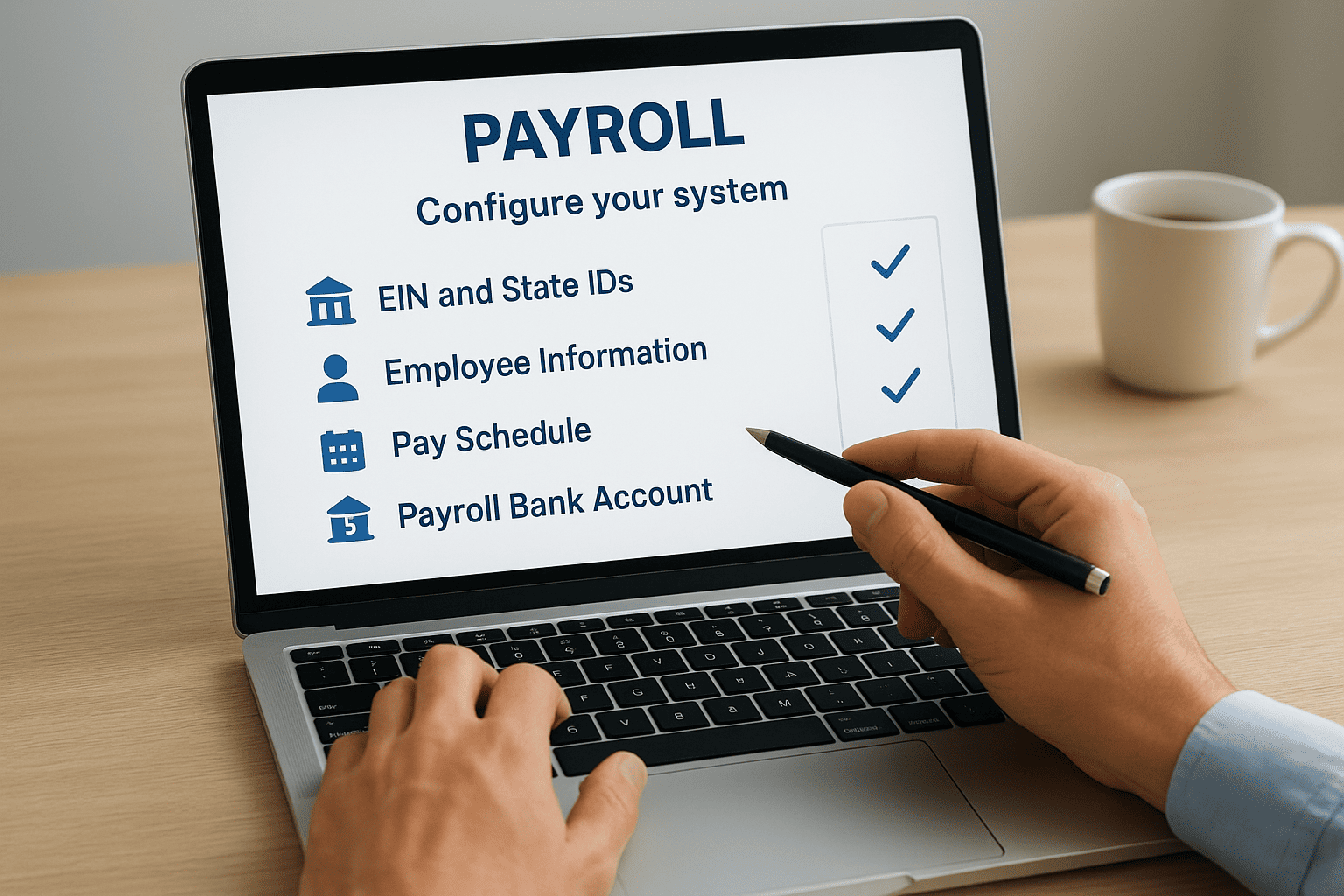

Configure your system before the first pay run

Once you pick a method, you need to enter your setup data accurately before running a single paycheck. Missing or incorrect entries at this stage cause withholding errors that affect every subsequent pay period.

Work through this configuration checklist before your first pay run:

- Enter your EIN and state employer tax ID numbers

- Add each employee's W-4 elections and pay rate

- Set your pay schedule (weekly, biweekly, semimonthly, or monthly)

- Connect your payroll bank account for direct deposit and tax deposits

- Confirm federal and state tax deposit frequencies based on your lookback period

Step 4. Run payroll and handle filings on time

Understanding how to set up payroll means nothing if you drop the ball on execution. Running payroll on every scheduled pay date, depositing taxes by the correct deadline, and submitting your quarterly returns on time are the three actions that determine whether your payroll compliance record stays clean or starts attracting IRS attention.

Process each pay run

Every pay run requires you to verify hours, calculate gross wages, apply withholdings, and confirm net pay before any funds move. Salaried employees have a predictable gross wage each period, but hourly employees require you to review and approve time records first. A single unchecked error in a time entry can throw off your Social Security and Medicare calculations for that entire pay period.

Work through this checklist on every pay date:

- Confirm total hours worked for hourly employees

- Verify any salary changes, bonuses, or one-time deductions since the last run

- Review calculated withholdings against each employee's W-4 elections

- Approve the direct deposit batch or prepare physical checks

- Save a copy of the payroll register for your records

Meet your deposit and filing deadlines

Tax deposits are not optional, and they are not due at the same time as your returns. The IRS assigns you a deposit schedule based on your lookback period: either monthly or semiweekly for Form 941 taxes. New employers default to the monthly schedule automatically.

Missing a federal tax deposit, even by one day, triggers a penalty that starts at 2% and scales up to 15% depending on how late the deposit arrives.

Keep these key deadlines on your calendar every quarter:

| Obligation | Due Date |

|---|---|

| Form 941 deposit (monthly schedule) | 15th of the following month |

| Form 941 quarterly filing | Last day of the month after quarter ends |

| State unemployment (SUTA) | Varies by state, typically quarterly |

| Form W-2 to employees | January 31 |

Keep payroll running smoothly

Now you know how to set up payroll from the ground up, but the real work is maintaining it. Set calendar reminders for every deposit deadline, every quarterly Form 941 due date, and every January 31 W-2 deadline. Consistent habits prevent the late penalties and interest charges that catch small business owners off guard after months of smooth operations.

Review your payroll register after each pay run to catch errors before they compound. When an employee updates their W-4, enters a new pay rate, or leaves the company, update your system the same day. Stale records cause withholding mismatches that you will have to reconcile manually, and that takes time you do not have.

If payroll compliance feels like too much to manage alongside running your business, working with a professional keeps your filings clean and your attention on growth. Talk to a payroll and tax expert at Tax Experts of OC to get started.