A single missed payroll tax deposit or misclassified worker can trigger IRS penalties that stack up fast. For small and mid-sized businesses, staying on top of federal, state, and local payroll obligations is one of the most demanding parts of running a company, and one of the most consequential when things go wrong. That's exactly where payroll compliance services come in, giving business owners a structured way to meet every filing deadline and tax requirement without doing it all themselves.

This article breaks down what payroll compliance services actually include, why they matter, and how to evaluate whether your business needs outside help. We'll cover the specific regulations involved, the risks of non-compliance, and what to look for in a provider.

At Tax Experts of OC, our CPAs and Enrolled Agents handle payroll services for businesses across all 50 states, from tax deposits and filings to year-end reporting. If payroll compliance has been a source of stress or confusion, this guide will give you a clear starting point.

What payroll compliance services include

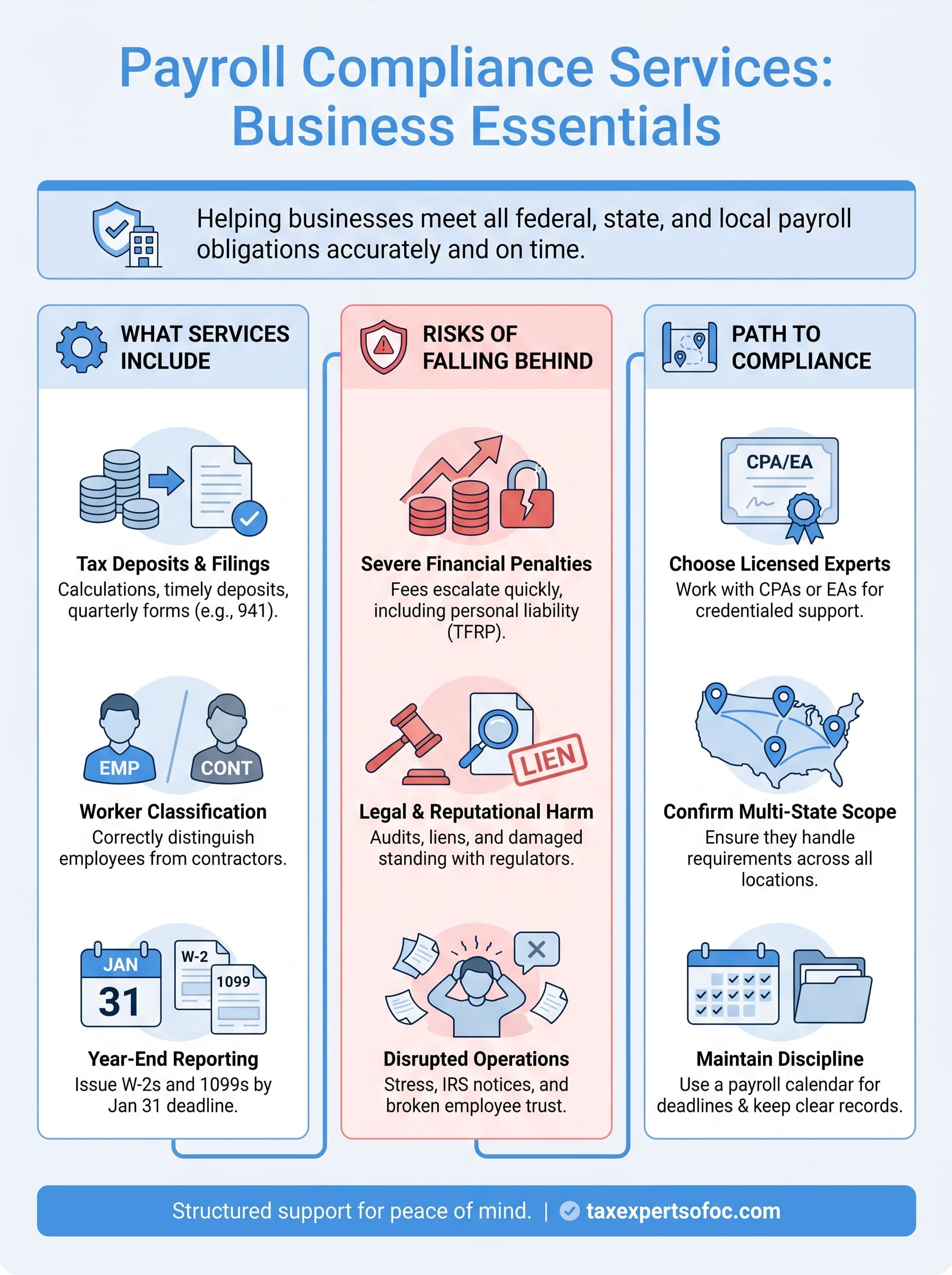

Payroll compliance services cover every recurring task that keeps your business aligned with federal, state, and local payroll regulations. These services go beyond cutting paychecks. They include calculating withholding amounts, submitting tax deposits on time, filing required forms, and maintaining records that satisfy both the IRS and Department of Labor standards.

Tax deposits and payroll tax filings

Every time you run payroll, your business owes FICA taxes (Social Security and Medicare) plus any federal income tax withheld from employees. The IRS assigns your deposit schedule, either semi-weekly or monthly, based on your total tax liability. Missing a deposit or submitting the wrong amount triggers failure-to-deposit penalties that start at 2% and climb to 15% depending on how late the payment lands.

According to the IRS, failure-to-deposit penalties are among the most frequently assessed payroll-related penalties against small businesses, and they accumulate quickly once a business falls behind.

Beyond federal deposits, you need to file Form 941 every quarter to report wages paid, taxes withheld, and employer contributions. Most states add their own parallel filing requirements on top of the federal schedule, each with separate deadlines and formats.

Worker classification and wage laws

Misclassifying an employee as an independent contractor is one of the costliest errors a business can make. If the IRS or Department of Labor reclassifies your workers after the fact, your business becomes liable for all the payroll taxes that should have been withheld, plus interest and back penalties that can stretch back several years. A compliance provider helps you apply the correct classification standards before those problems develop.

Your business also needs to follow federal and state wage and hour laws, including minimum wage requirements, overtime rules under the Fair Labor Standards Act, and state-specific rules that frequently exceed federal minimums. A compliance provider tracks these changes as they happen, so you are not responsible for monitoring every regulatory update across multiple jurisdictions.

Year-end reporting and recordkeeping

At year-end, your business must issue W-2 forms to all employees and 1099-NEC forms to qualifying contractors, both due by January 31. These documents also go to the Social Security Administration and the IRS. Even minor errors, like a transposed Social Security number, can generate IRS correction notices that take weeks to resolve and distract from running your business.

Consistent recordkeeping throughout the year is what makes year-end reporting manageable. A payroll compliance provider maintains organized records of wages, withholdings, and tax deposits so that when January arrives, you have everything ready to file accurately and on time rather than scrambling through a year's worth of disorganized data.

Why payroll compliance matters for your business

Payroll compliance is not optional, and the consequences of falling short reach further than most business owners expect. Federal and state tax agencies have clear authority to assess fines, place liens on your business, and hold you personally liable for unpaid payroll taxes. Understanding what is at stake helps you direct the right level of attention and resources toward this responsibility.

The financial cost of falling behind

When payroll taxes go unpaid or filings arrive late, the penalties compound quickly. The Trust Fund Recovery Penalty allows the IRS to hold you personally liable for 100% of the unpaid payroll taxes withheld from employees, even if your business operates as an LLC or corporation.

The IRS treats withheld payroll taxes as funds held in trust for the government, which is why the Trust Fund Recovery Penalty can attach to owners, officers, and anyone else deemed responsible for the failure to pay.

Beyond the penalty itself, interest accrues daily on any outstanding balance, and the IRS can file a federal tax lien against your business, making it harder to secure credit or financing when you need it most.

How compliance protects your employees and your standing

Your employees depend on you to accurately withhold and remit their taxes. When your business fails to do so, workers may face problems when they file their own personal returns, even though the error originated on your end. Investing in payroll compliance services protects your team from that kind of unnecessary disruption.

Staying compliant also protects your business reputation. State labor boards can audit your wage and hour practices at any time, and a finding of non-compliance enters the public record. Keeping your business in good standing with regulators, lenders, and employees starts with getting payroll right every time.

Common payroll compliance risks and mistakes

Most payroll errors don't happen because business owners ignore the rules. They happen because payroll regulations are layered and complex, involving multiple agencies with overlapping requirements that change on a state-by-state basis. Knowing where the most common problems occur helps you avoid them before they become expensive.

Misclassifying workers

Worker misclassification is one of the most widespread payroll compliance mistakes, and it carries some of the heaviest consequences. When you treat an employee as an independent contractor, your business skips withholding payroll taxes, but if the IRS or a state agency reviews the arrangement and disagrees, they will assess all the back taxes, penalties, and interest that should have accumulated over the entire working relationship.

The IRS uses a multi-factor behavioral and financial control test to determine worker classification, and the burden falls on your business to demonstrate the classification was correct.

The risk grows when you operate in states like California, where worker classification rules under AB5 are stricter than federal standards. A provider of payroll compliance services monitors both federal and state rules so your classifications hold up under scrutiny.

Missing deposit deadlines and filing errors

Late or incorrect tax deposits generate penalties that start immediately and grow with each passing day. Even a deposit made one day late can trigger a 2% penalty, and that figure rises sharply if the IRS needs to issue a notice before you act. Many businesses also make errors on Form 941, reporting incorrect wage totals or withholding amounts, which invites IRS correspondence that can delay resolution for weeks.

Errors in year-end W-2 reporting create a separate problem. Incorrect Social Security numbers, wrong wage figures, or missed deadlines result in penalties assessed per form, which adds up fast if you have more than a handful of employees on payroll.

How to choose the right payroll compliance provider

Not every payroll service offers the same level of expertise, and choosing the wrong one can leave your business just as exposed as handling it yourself. When you evaluate providers of payroll compliance services, focus on credentials, scope, and communication rather than price alone.

Look for licensed professionals

The person managing your payroll should carry recognized credentials such as a Certified Public Accountant (CPA) or an Enrolled Agent (EA). Both designations require demonstrated expertise and ongoing education. CPAs and EAs can also represent you before the IRS if a payroll issue escalates into a dispute, which a non-credentialed payroll processor cannot do.

Choosing a provider with CPA or Enrolled Agent credentials gives you a layer of protection that goes beyond routine filing, covering you in the event of an audit or penalty assessment.

Confirm they handle multi-state requirements

If your employees work across multiple states, your payroll obligations multiply. Each state has its own deposit schedules, tax rates, and reporting formats. A capable provider should demonstrate that they already manage multi-state payroll filings for other clients and stay current with state-level regulatory changes as they occur.

Ask directly how they track changes to state wage laws and minimum wage updates in the jurisdictions relevant to your business. A provider who relies solely on outdated software without human oversight may miss a state law change that triggers a penalty on your end.

Ask about year-end support

Year-end is when payroll compliance demands the most concentrated attention, with W-2 and 1099 filings converging in a narrow window. Confirm that your provider handles year-end reporting as part of their standard service rather than charging it as a separate add-on.

Before you commit, ask them to walk you through their specific year-end process and what happens if an error surfaces after submission. A provider with a clear, documented answer is one you can trust when the deadlines are real.

How to stay compliant with a simple process

Staying compliant doesn't require a complicated system, but it does require consistency and clear ownership. The businesses that avoid payroll problems aren't necessarily the largest ones; they're the ones that assign specific responsibilities to specific people or providers and follow through on the same schedule every pay period without exception.

Build a payroll calendar

A payroll calendar is the single most practical tool for avoiding late deposits and missed filings. Map out every deposit due date, quarterly filing deadline, and year-end reporting requirement at the start of each year so no deadline catches you off guard. Include both federal and state deadlines, since state deposit schedules frequently differ from the federal schedule and carry their own separate penalties.

Use your calendar as a running checklist by confirming each task as completed, including the deposit amount, the form filed, and the date submitted. This creates a basic audit trail that protects you if you ever receive an IRS or state inquiry about a prior period.

Work with qualified professionals

If payroll compliance services handle the mechanics of depositing and filing on your behalf, your role shifts from managing deadlines to reviewing and approving results. Set a brief monthly or quarterly check-in with your provider to confirm that all deposits cleared, filings went out on time, and no notices arrived from federal or state tax agencies.

Consistent communication with your payroll provider is what catches small errors before they become formal assessments, not the software alone.

When your workforce changes, such as hiring a new employee, adding a contractor, or expanding operations into a new state, notify your provider before the change takes effect. Waiting until after the fact creates gaps in withholding and classification that take far more effort to correct than they would have taken to prevent from the start.

Where to go from here

Payroll compliance is one of those responsibilities that rewards businesses who take it seriously early. Missed deposits, misclassified workers, and late filings don't resolve themselves, and each one tends to cost more the longer it sits. The good news is that the path forward is straightforward: assign clear ownership of your payroll obligations, build a filing calendar, and work with professionals who hold the credentials to back you up when it counts.

If your business needs structured support, payroll compliance services from a licensed CPA or Enrolled Agent give you consistent coverage across federal and state requirements without leaving you to track every regulatory change on your own. Tax Experts of OC works with businesses across all 50 states to manage payroll filings, deposits, and year-end reporting with the same attention your finances deserve. Schedule a free 30-minute consultation with our team at Tax Experts of OC and get a clear picture of where your payroll stands.