Tax software works fine, until it doesn't. For straightforward W-2 returns with a standard deduction, DIY filing makes sense. But there's a point where the cost of getting it wrong far exceeds the cost of hiring a professional. Knowing when to hire a CPA for taxes can be the difference between a clean filing and a costly mistake that follows you for years.

The tricky part is that most people don't realize they've outgrown DIY until they're already in trouble, an unexpected IRS notice, a missed deduction worth thousands, or a business structure that's bleeding money in unnecessary taxes. These aren't hypothetical scenarios. They're the exact situations our CPAs and Enrolled Agents at Tax Experts of OC help clients resolve every week, both locally in Orange County and across all 50 states.

Here are five specific situations where hiring a CPA stops being optional and starts being the smartest financial move you can make.

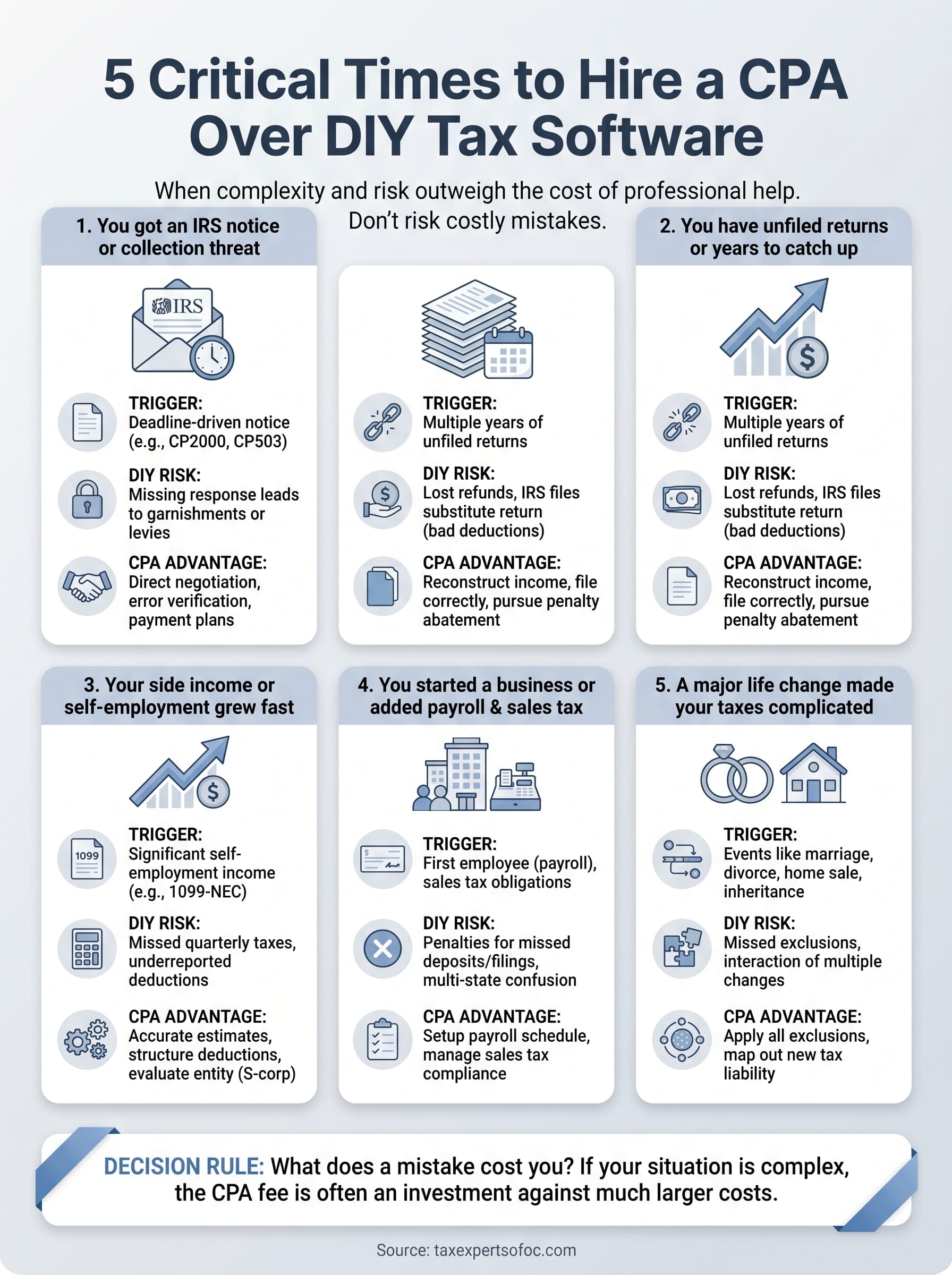

1. You got an IRS notice or collection threat

An IRS notice sitting on your kitchen table is not something you can safely ignore or handle with tax software. Every notice carries a response deadline, and missing it can escalate a manageable issue into a serious collection action involving wage garnishments or bank levies.

What usually triggers this

IRS notices arrive for many reasons: underreported income, discrepancies between your return and third-party data like W-2s or 1099s, or unpaid balances from prior years. CP2000 notices are among the most common, flagging a mismatch between what you filed and what employers or financial institutions reported to the IRS. Others, like CP503 or CP504, signal that active collection is already underway.

Why DIY often breaks down

Tax software helps you file a return, but it cannot respond to the IRS on your behalf or negotiate a resolution. When a notice arrives, the IRS expects a specific written response that addresses their exact concern with supporting documentation. Most people either ignore the notice out of stress or send an incomplete response that makes the situation worse.

The IRS treats silence as agreement, which means an ignored notice almost always results in a larger bill.

What a CPA will do differently

A CPA or Enrolled Agent can communicate directly with the IRS using a Power of Attorney, review your full tax history, and determine whether the notice is even accurate. They identify errors in IRS calculations, pull together the right documentation, and negotiate payment plans or penalty abatement where appropriate.

What to gather before you call

Bring every notice you have received, copies of the tax returns in question, and any W-2s, 1099s, or financial statements tied to the years involved. The more complete your records, the faster a CPA can assess the situation and build a response.

Typical cost range and what affects it

IRS representation typically runs between $1,500 and $5,000 depending on the complexity of the issue, how many tax years are involved, and whether penalties need to be disputed. Cases involving audits or appeals will land at the higher end of that range.

2. You have unfiled returns or years to catch up

Having one or more unfiled tax returns puts you in a precarious position with the IRS. The agency can file a substitute return on your behalf using only the income data they have, which almost never reflects your actual deductions.

What usually triggers this

Life gets complicated fast. A job loss, a health crisis, or a chaotic business stretch can push filing to the back burner for a year, then two, then more. Many people also delay because they know they owe and don't have the money to pay.

Why DIY often breaks down

Tax software is built for the current tax year. Filing multiple prior-year returns through consumer software is difficult because older versions may be unavailable, and the software won't help you understand your options for reducing penalties.

The IRS holds your refunds from unfiled years, and the three-year window to claim those refunds closes whether or not you file.

What a CPA will do differently

A CPA pulls wage and income transcripts directly from the IRS, reconstructs your deductions across each unfiled year, and files returns in the correct sequence. They also pursue penalty abatement wherever possible to reduce your final balance.

What to gather before you call

Collect everything you still have from the years in question and bring it to your first call. Your CPA can also request IRS wage and income transcripts to fill any gaps.

- W-2s, 1099s, and bank statements from affected years

- Prior tax returns if available

- Any IRS notices you received

Typical cost range and what affects it

Expect to pay $300 to $600 per unfiled year for straightforward individual returns, with higher costs when business income or complex deductions are involved.

3. Your side income or self-employment grew fast

When freelance work or a side hustle starts generating real money, your tax situation changes significantly. Self-employment income introduces quarterly estimated taxes, self-employment tax, and deductible business expenses that most DIY filers consistently underreport or miscalculate.

What usually triggers this

The most common trigger is a 1099-NEC that arrives in January for work you did throughout the prior year. Many people don't realize they owe taxes on that income until filing season, which means they've already missed four quarterly payment deadlines and face underpayment penalties.

Why DIY often breaks down

Tax software walks you through a basic Schedule C, but it won't prompt you to deduct the full range of legitimate business expenses like home office costs, equipment, mileage, or health insurance premiums. It also won't flag when your income level makes an S-corp election worth exploring to reduce your self-employment tax burden.

Underpaying quarterly estimated taxes by even a small amount each quarter adds up to a meaningful penalty by year-end.

What a CPA will do differently

Knowing when to hire a CPA for taxes matters most when income is growing fast. A CPA structures your deductions correctly, sets accurate quarterly payment amounts, and evaluates whether your business entity type is costing you more than it should.

What to gather before you call

- All 1099-NEC forms received

- Bank statements showing business income and expenses

- Receipts for equipment, software, and home office costs

Typical cost range and what affects it

Self-employment tax preparation typically runs $400 to $900, with higher fees when multiple income streams or entity restructuring recommendations are involved.

4. You started a business or added payroll and sales tax

Starting a business introduces payroll withholding, sales tax collection, and quarterly business filings that DIY software isn't designed to handle together. When these obligations pile up, missing one deadline can trigger separate penalties from both the IRS and your state revenue department.

What usually triggers this

The most common trigger is hiring your first employee, which creates immediate obligations for payroll tax deposits, Form 941 filings, and unemployment insurance registration. Adding sales tax collection to a product-based business creates a second compliance track with rules that vary by state.

Why DIY often breaks down

Consumer tax software handles personal returns, not multi-entity payroll and sales tax reconciliation. Most platforms won't alert you when payroll deposits are due or flag when you've crossed a sales tax nexus threshold in a new state.

What a CPA will do differently

Knowing when to hire a CPA for taxes matters most when payroll enters the picture. A CPA sets up your payroll tax deposit schedule, files Form 941 each quarter, and monitors your sales tax obligations across every state where you operate.

Missing a single payroll tax deposit triggers IRS penalties up to 15 percent of the unpaid amount.

What to gather before you call

- Payroll records and employee headcount history

- Sales revenue broken down by state

- Business entity documents and your EIN

Typical cost range and what affects it

Business tax preparation with payroll typically runs $800 to $2,000 per year, rising when multi-state sales tax registration or multiple business entities are involved.

5. A major life change made your taxes complicated

Life events can reshape your tax situation quickly. Marriage, divorce, a home sale, an inheritance, or the start of retirement distributions each introduces new obligations that standard software isn't built to handle well.

What usually triggers this

The most common triggers include selling a primary residence, receiving an inheritance, or starting IRA and 401(k) distributions. Each creates new reporting requirements that interact with your existing tax picture in ways that are easy to miss.

Why DIY often breaks down

Tax software treats these events as checkboxes, but it won't catch interactions between multiple life changes in the same year. A divorce and a home sale together, for example, create overlapping exclusions and deductions that require careful coordination to handle correctly.

Missing a single exclusion on a home sale can cost you tens of thousands in unnecessary capital gains tax.

What a CPA will do differently

Knowing when to hire a CPA for taxes matters most after a major life transition. A CPA maps out how each event affects your overall tax liability, applies every available exclusion, and flags any estimated payments you now owe going forward.

What to gather before you call

Bring complete documentation for every event that fell in the tax year. Gaps in records are the most common reason these returns get delayed and corrected after the fact.

- Settlement agreements or divorce decrees if applicable

- Home sale closing documents and original purchase records

- Retirement account statements and distribution summaries

Typical cost range and what affects it

Returns involving major life changes typically cost $500 to $1,200, rising when multiple events occur in the same year or state-level filings add another layer of complexity.

A simple way to choose between CPA and DIY

The decision comes down to one question: what does a mistake cost you? If your return involves a single W-2 and a standard deduction, DIY software is a reasonable choice. But the moment your situation involves IRS notices, unfiled returns, self-employment income, payroll obligations, or a major life change, the cost of getting it wrong almost always exceeds what a CPA charges to get it right.

Knowing when to hire a CPA for taxes is not about income level. It's about complexity and risk. If any of the five situations in this article sound familiar, the next step is a conversation with a qualified professional rather than another hour troubleshooting tax software on your own.

Schedule a free 30-minute consultation with Tax Experts of OC to get a clear picture of where you stand and exactly what it will take to resolve it.