Owing the IRS more than you can realistically pay puts you in a difficult position, but it doesn't mean you're out of options. The IRS Offer in Compromise program exists specifically for taxpayers who can't settle their full tax debt, allowing them to negotiate a reduced amount and move forward. The catch? The application process is detailed, documentation-heavy, and unforgiving of mistakes. That's where working with an offer in compromise CPA makes a real difference.

At Tax Experts of OC, our CPA and Enrolled Agents have guided clients across all 50 states through the OIC process, from determining whether they actually qualify to assembling the financial documentation the IRS requires. We know what the IRS looks for when evaluating these cases, and we know how to position your application for the strongest possible outcome.

This article breaks down what the Offer in Compromise process involves, who's eligible, and what you should expect when working with a qualified tax professional to settle your debt for less than you owe.

Why an offer in compromise matters

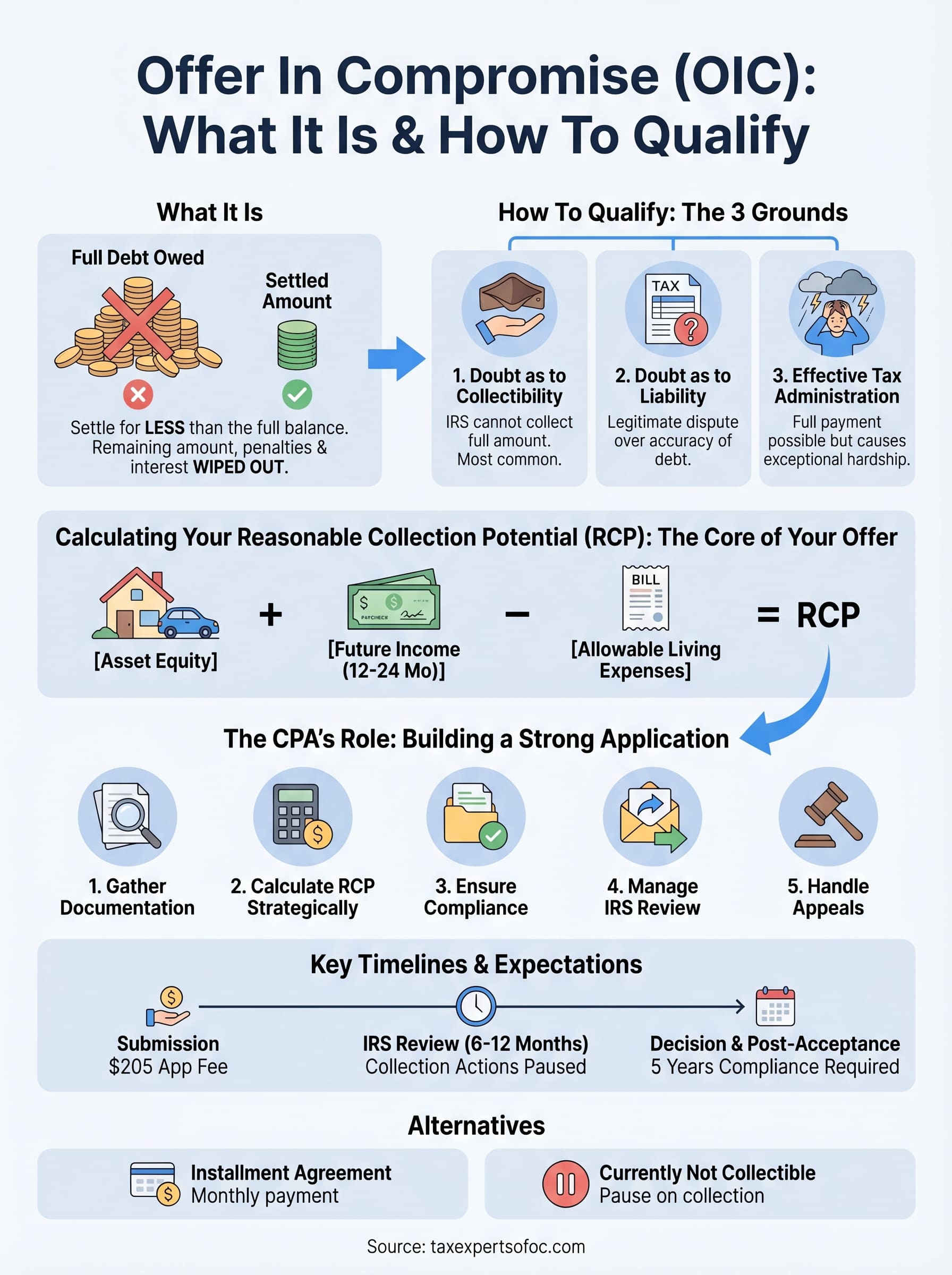

For most people carrying a large IRS tax debt, the default assumption is that they owe every penny and simply have to figure out how to pay it. That assumption is often wrong. The Offer in Compromise program is an official IRS mechanism that allows qualifying taxpayers to settle their tax liability for less than the full balance owed when paying in full would cause genuine financial hardship. Understanding what this program can do for you is the first step toward getting out from under a debt that may feel impossible to escape.

What settling your debt actually means for you

An accepted OIC doesn't just reduce the dollar amount you owe. It wipes out the remaining balance entirely once you complete the agreed payment terms. That includes any associated penalties and interest that have accumulated on top of your original tax debt. For someone who owes $50,000 but can only demonstrate a reasonable collection potential of $8,000, a successful OIC means the IRS closes the case at $8,000 and writes off the rest permanently.

Once the IRS accepts an Offer in Compromise and you meet the payment terms, the remaining tax debt is gone for good, not deferred or paused.

Working with an offer in compromise CPA gives you the best chance of reaching that outcome because the IRS calculates your reasonable collection potential using a specific formula. If that number is presented incorrectly, the IRS will reject your offer or counter at a much higher amount, leaving you no better off than when you started.

The real cost of ignoring your tax debt

If you don't take action on a growing IRS balance, the agency has substantial collection tools available to it. It can place a federal tax lien on your property, which appears in public records and damages your credit standing. It can also issue a levy, which means it can legally seize funds directly from your bank accounts or wages without a court order.

Beyond the immediate damage, unpaid tax debt keeps growing on its own. Failure-to-pay penalties accrue monthly, and interest compounds daily on the outstanding balance. What started as a $20,000 liability can climb well past $30,000 within a few years if left unaddressed.

Your options for resolving IRS debt don't disappear overnight, but the window for pursuing programs like the OIC can narrow over time. The IRS operates under a 10-year statute of limitations for collections, which sounds generous until you factor in the ongoing penalties, the collection actions, and the financial stress of carrying an open IRS liability. Taking action now, with qualified professional help, is almost always more cost-effective than waiting and hoping the situation resolves itself.

How the IRS decides if you qualify

The IRS doesn't accept OIC applications based on hardship stories or good intentions. It uses a specific financial formula to determine whether accepting your offer is in the government's best interest. Before you submit anything, you need to understand the three grounds the IRS recognizes and how your overall financial profile determines whether your offer has a realistic chance of approval.

The three grounds for an OIC

The IRS accepts Offer in Compromise applications under three distinct categories. The most common is Doubt as to Collectibility, which applies when the IRS determines it cannot collect the full amount you owe within the remaining collection period. The second is Doubt as to Liability, used when there is a legitimate dispute about whether the assessed tax debt is actually accurate. The third is Effective Tax Administration, reserved for cases where full payment is technically possible but would create exceptional hardship that the IRS considers inequitable to enforce.

Most applicants qualify under Doubt as to Collectibility, and that is the category where an offer in compromise CPA provides the most direct value in structuring and presenting your case.

How the IRS calculates your reasonable collection potential

Your reasonable collection potential (RCP) is the core number the IRS uses to evaluate your offer, and presenting it accurately is what determines whether you get approved.

The IRS calculates your RCP by combining your net realizable assets with your projected future income, then subtracting allowable living expenses. Net realizable assets include equity in property, vehicles, bank accounts, and retirement funds, often valued at a discount. Your future income figure is based on your monthly disposable income multiplied by either 12 or 24 months, depending on your chosen payment option.

Comparing your submitted offer amount to this RCP figure is what drives the IRS decision. If your offer meets or exceeds the calculated RCP, the IRS has a clear reason to accept it. If your number falls short, the agency will typically reject the application or issue a counteroffer at a higher amount.

How a CPA builds a strong OIC application

Submitting an OIC without professional help is technically possible, but the IRS rejects a significant percentage of applications because the numbers are presented incorrectly or supporting documentation is incomplete. An offer in compromise CPA approaches your application as a financial case, not a form-filling exercise. Every figure submitted needs to reflect your actual situation while staying within the IRS's own calculation framework.

Gathering and organizing your financial documentation

Your application requires a full financial disclosure, and the IRS cross-references everything you submit. A CPA starts by collecting several months of bank statements, pay stubs, and asset documentation so nothing gets flagged as inconsistent. This includes real property equity, vehicle values, retirement account balances, and any business interests you hold.

The IRS uses standardized National and Local Expense Standards to cap certain living expenses like housing and transportation. A CPA reviews which of your actual expenses fall within those limits and which ones need supporting documentation to be counted at your real cost. Presenting this correctly keeps your allowable expenses as high as the IRS will accept, which directly lowers your calculated RCP.

Calculating and presenting your offer strategically

Once your assets and income picture is clear, your CPA calculates your reasonable collection potential before the IRS does. This lets you identify the lowest defensible offer amount and decide whether to apply under the 5-month lump-sum payment option or the 24-month periodic payment plan, which each use a different income multiplier.

Getting that calculation right before submission is what separates an application the IRS accepts from one it rejects outright.

Your CPA also reviews your compliance history to confirm you've filed all required returns and made any required estimated tax payments. The IRS will automatically return your OIC application if you're not current on your filing obligations, regardless of how well-prepared the rest of your package is. Handling this step before submission protects your application fee and avoids unnecessary delays.

What to expect during IRS review and after

Once you submit your OIC application, the IRS begins a formal review process that typically takes 6 to 12 months to complete. During this period, the IRS assigns your case to a revenue officer who evaluates your financial disclosures and submitted documentation to determine whether your offer amount meets the calculated reasonable collection potential. Collection actions are generally paused during this window, which gives you some breathing room while the review proceeds.

The IRS review timeline

The IRS will send you an acknowledgment letter once your application is received and confirmed as processable. From there, the assigned examiner may contact your offer in compromise CPA directly to request additional documentation or clarification on specific figures in your application. Responding promptly and accurately to any IRS requests is critical because delays on your end can slow the process or result in a rejection for non-responsiveness.

The IRS can take over a year to issue a final decision on an OIC, so patience and consistent communication with your CPA during this period are essential.

Your current tax filings and estimated payments must stay up to date throughout the entire review period. If you fall out of compliance while the IRS is reviewing your application, the agency will return your offer without processing it, and you'll need to start over from the beginning.

After the IRS issues a decision

If the IRS accepts your offer, you'll receive a formal acceptance letter outlining the agreed settlement amount and your payment terms. You must complete those payments on schedule and remain tax compliant for five years following acceptance, or the IRS can revoke the agreement and reinstate the full original debt plus penalties and interest.

A rejection doesn't end your options. You have the right to appeal the decision within 30 days of receiving the rejection notice, and your CPA can file that appeal through the IRS Office of Appeals with additional supporting arguments or documentation. Many OIC rejections are successfully overturned at the appeals stage, which is why professional representation throughout the entire process matters far more than just at the point of submission.

Costs, risks, and alternatives to consider

Working with an offer in compromise CPA comes with professional fees, and you should understand what you're paying for before you commit. Fees vary by case complexity, but most qualified tax professionals charge somewhere between $3,500 and $7,500 to prepare and submit a full OIC application. That range reflects the time required to gather documentation, calculate your RCP accurately, and manage IRS correspondence throughout the entire review period.

What the IRS charges to apply

The IRS requires a $205 application fee when you submit your OIC, along with an initial payment that varies based on your chosen payment option. If you qualify as a low-income taxpayer under IRS income thresholds, the agency waives both the fee and the initial payment requirement entirely. Your CPA can confirm whether you meet that threshold before you submit anything, so you're not spending money unnecessarily on an application that doesn't serve you.

Risks you need to understand before filing

Submitting an OIC with inaccurate or incomplete financial disclosures is not simply a reason for rejection. It can trigger additional IRS scrutiny of your broader tax situation. The agency reviews your entire financial picture when it processes your application, so inconsistencies between your submitted figures and your actual bank statements or tax records can create new problems on top of your original debt.

Filing an OIC also extends the IRS statute of limitations for collection, so if the agency rejects your application, it has additional time to pursue the full balance owed.

Alternatives if you don't qualify for an OIC

Not everyone meets the IRS threshold for a viable OIC, and knowing that before you apply saves you both the fee and the wait. If your reasonable collection potential is too high to support a reduced settlement, an installment agreement lets you pay your balance in IRS-approved monthly amounts over an extended period. Currently Not Collectible status is another option that pauses all collection activity when your income genuinely cannot cover basic living expenses and tax payments at the same time.

If you want help, here's what to do next

If your tax debt has reached a point where paying in full isn't realistic, the Offer in Compromise program may be your clearest path to a permanent resolution. The process requires accurate financial documentation, a correctly calculated RCP, and full IRS compliance before and during the review period. Getting any of those elements wrong is the most common reason applications get rejected.

Working with a qualified offer in compromise CPA gives you the best chance of submitting an application the IRS actually accepts. At Tax Experts of OC, our CPA and Enrolled Agents handle the entire process, from confirming your eligibility to managing IRS correspondence through to a final decision. You can start with a free 30-minute consultation to understand your options before committing to anything. Contact Tax Experts of OC today to talk through your situation with a professional who handles these cases every day.