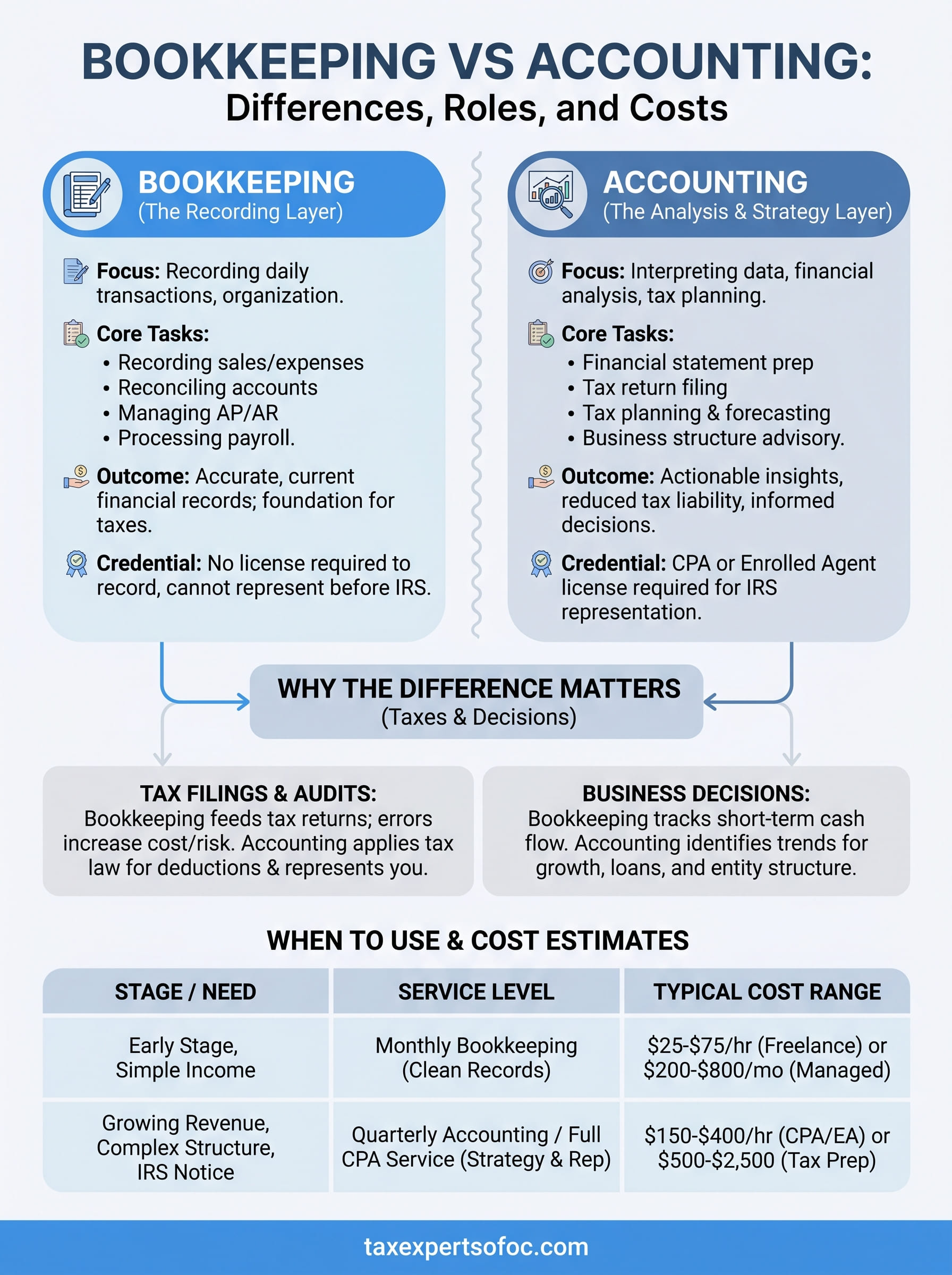

Most business owners use the terms interchangeably, but bookkeeping vs accounting describes two distinct functions that serve different purposes in your financial operation. One focuses on recording transactions; the other interprets what those numbers mean. Confusing the two can lead to hiring the wrong help, overpaying for services you don't need, or missing strategic opportunities that save you money at tax time.

At Tax Experts of OC, our CPAs and Enrolled Agents work with both sides of this equation every day, organizing financial records for clients across all 50 states and turning that data into actionable tax strategies. We see firsthand how understanding this distinction helps business owners make smarter decisions about where to invest their resources.

This article breaks down the specific differences between bookkeeping and accounting, including what each role handles, what they typically cost, and how to determine which service your business actually needs. Whether you're a solo entrepreneur deciding between DIY software and a professional, or a growing company weighing when to bring on higher-level financial support, you'll walk away with a clear framework for making that call.

Why the difference matters for taxes and decisions

When you treat bookkeeping and accounting as the same thing, you typically end up with incomplete records or missing financial analysis at the worst possible moment, right before a tax deadline or during an IRS audit. The distinction shapes who you hire, what they actually do for you, and how much leverage you have when making major business decisions.

How each function affects your tax filings

Your books feed directly into your tax return. If your transaction records are incomplete or categorized incorrectly, your accountant has nothing reliable to work with. A CPA or Enrolled Agent may need to reconstruct your records before they can even prepare your return, which adds time and increases your cost significantly. Clean, current bookkeeping prevents that problem before it starts.

Accurate books are the foundation of every tax strategy. Without them, even the most qualified tax professional is working blind.

Accounting takes those clean records and applies tax law, allowable deductions, and forward-looking planning that a bookkeeper is not trained or licensed to handle. If you skip the accounting layer entirely, you risk leaving substantial deductions unclaimed, and that pattern tends to repeat itself year after year without anyone flagging it.

How the bookkeeping vs accounting gap affects business decisions

Beyond taxes, accounting provides the financial analysis you need to make informed decisions about growth, cost reduction, or taking on debt. Lenders and investors review financial statements that an accountant prepares, not raw transaction logs that a bookkeeper produces. That distinction matters when you apply for a business loan or bring on a partner.

Your bookkeeper tracks cash flow, accounts payable, and receivables week to week, which tells you whether you can cover expenses next month. Your accountant reads trends across multiple quarters, identifies risks, and advises you on whether your current business structure is costing you unnecessarily in self-employment or entity-level taxes. Both roles answer different questions, and both questions matter.

What bookkeeping covers in a business

Bookkeeping is the process of recording every financial transaction your business makes in a systematic, organized way. It is the daily maintenance layer of your financial operation. Without it, you have no reliable data for anything else, including tax filings, payroll, or vendor payments.

Core bookkeeping tasks

A bookkeeper handles the day-to-day recording and categorization of income and expenses, reconciles your bank accounts, manages accounts payable and receivable, and processes payroll entries. When you compare bookkeeping vs accounting, bookkeeping is focused on accuracy and consistency, not financial analysis.

Disorganized books create downstream problems across every area of your finances, from your tax return to your ability to secure a business loan.

Common bookkeeping tasks include:

- Recording sales, payments, and expenses

- Reconciling bank and credit card statements monthly

- Tracking accounts payable and receivable

- Processing payroll data

- Maintaining a general ledger

When bookkeeping alone falls short

Your bookkeeper keeps records current, but they do not interpret trends, advise on tax strategy, or prepare your tax return. Once your revenue grows or your financial situation becomes more complex, you need the analysis layer that a licensed CPA or Enrolled Agent provides.

Relying solely on bookkeeping means you may miss significant deductions and entity-level tax planning opportunities that only surface through formal financial analysis.

What accounting covers and when you need it

Accounting picks up where bookkeeping stops. While a bookkeeper records transactions, an accountant analyzes those records, prepares formal financial statements, and applies tax law to your specific situation. When you compare bookkeeping vs accounting, accounting requires a deeper level of professional training and licensing, which is why CPAs and Enrolled Agents can represent you before the IRS while bookkeepers cannot.

Core accounting responsibilities

A licensed accountant handles tasks that require technical judgment and regulatory knowledge that go well beyond data entry. This includes preparing income statements, balance sheets, and cash flow statements that lenders and investors rely on when evaluating your business. Your accountant also identifies allowable deductions, credits, and entity-level strategies that reduce your overall tax burden year over year.

Core accounting functions include:

- Preparing and filing federal and state tax returns

- Financial statement preparation and analysis

- Tax planning and multi-year forecasting

- IRS audit representation

- Business structure and entity advisory

When you need to bring in an accountant

If your revenue is growing, your entity structure is changing, or you have received an IRS notice, engaging a licensed accountant immediately is the right move.

You should bring in a licensed accountant any time your financial situation involves regulatory complexity or significant tax exposure. A sole proprietor managing straightforward income might manage with bookkeeping software for a period, but once you form an LLC, take on partners, or face an IRS inquiry, professional accounting representation becomes non-negotiable.

How to choose services and estimate the cost

When you compare bookkeeping vs accounting for your business, the right choice depends on your current complexity and what decisions you need to make with your financial data. A startup with straightforward income and no employees likely needs basic bookkeeping first. A company with multiple revenue streams, payroll, and multi-state obligations needs both functions working together from the start.

Matching the service to your business stage

Your business stage is the clearest signal for determining the service level you actually need. Early-stage businesses typically start with monthly bookkeeping to keep records clean and ready for tax season. As your revenue grows or your entity structure changes, you layer in quarterly accounting reviews to catch tax exposure before it compounds into a larger problem.

Starting with clean books is always the right first move, regardless of where your business is heading next.

Understanding typical cost ranges

Costs vary based on transaction volume, service scope, and professional credentials. Freelance bookkeepers generally charge $25 to $75 per hour, while firms offering managed bookkeeping run $200 to $800 per month depending on volume. Accounting services from a licensed CPA or Enrolled Agent typically range from $150 to $400 per hour, with tax preparation for small businesses running $500 to $2,500 per filing.

Paying more for a qualified accountant delivers measurable value when your situation involves IRS exposure, entity structuring, or multi-state filings. In those cases, the cost of professional guidance is considerably lower than the cost of errors left uncorrected over several tax years.

Bookkeeping vs accounting FAQs and gray areas

Several questions come up repeatedly when people research bookkeeping vs accounting, and many involve situations where the line between the two is not obvious. Understanding these gray areas helps you avoid hiring the wrong service or assuming one professional can handle everything your business requires.

Can a bookkeeper prepare and file my taxes?

A bookkeeper can organize your records and generate reports, but filing your tax return requires a licensed professional. Only a CPA, Enrolled Agent, or tax attorney is authorized to represent you before the IRS if your return is questioned.

Relying on an unlicensed person to prepare your taxes creates risk that compounds quickly. The exposure becomes especially significant if you face an IRS audit, since only licensed professionals can legally respond and advocate on your behalf.

The credential matters because it determines what your professional can legally do on your behalf, not just what they know.

What happens when my bookkeeper also calls themselves an accountant?

Titles in this industry are not always regulated, so some individuals use both terms loosely. What matters more than the label is licensure and scope of work. If someone is not a CPA or Enrolled Agent, they cannot legally represent you before the IRS, regardless of what they call themselves.

Always verify credentials before you hand over your financial records. The IRS Preparer Directory lets you confirm whether someone holds a valid designation recognized by federal tax authorities.

Next steps for getting your finances in order

Understanding bookkeeping vs accounting gives you a practical framework for deciding where to invest your resources right now. If your records are behind, start there. Catching up on disorganized books before tax season is always more manageable and less costly than reconstructing months of transactions under deadline pressure.

Once your records are current, determine whether your situation requires licensed professional oversight. If you have received an IRS notice, operate across multiple states, or carry significant tax debt, you need more than a bookkeeper. You need a CPA or Enrolled Agent who can analyze your exposure, represent you if needed, and build a plan that reduces your liability going forward.

Tax Experts of OC works with individuals and businesses at every stage of this process, from organizing records to resolving IRS disputes nationwide. Start with a free 30-minute consultation and get a clear picture of where you stand by reaching out to Tax Experts of OC today.