Construction companies don't operate like most businesses. Revenue hits in uneven waves, expenses shift from job to job, and a single project can span months, or years, across multiple phases. Standard bookkeeping methods weren't built for this, and that's exactly why construction bookkeeping requires its own set of rules, tools, and strategies. Get it wrong, and you're flying blind on job profitability, cash flow, and tax obligations all at once.

Whether you're a general contractor running a crew of five or managing a growing firm with dozens of active projects, your books need to reflect the reality of how construction revenue is earned and how costs are incurred. That means understanding concepts like job costing, progress billing, the percentage-of-completion method, and retainage tracking, none of which show up in a generic accounting tutorial.

At Tax Experts of OC, our CPAs and Enrolled Agents work with contractors and construction business owners across all 50 states to bring order to their financial records, handle tax preparation and planning, and resolve issues with the IRS when things fall behind. We built this guide because we've seen firsthand how much money contractors leave on the table, or owe unexpectedly, when their bookkeeping doesn't match their operations.

This guide covers everything from foundational principles and chart of accounts setup to software selection, common mistakes, and when it makes sense to bring in professional help. If you're ready to take control of your construction company's finances, start here.

Why construction bookkeeping matters for contractors

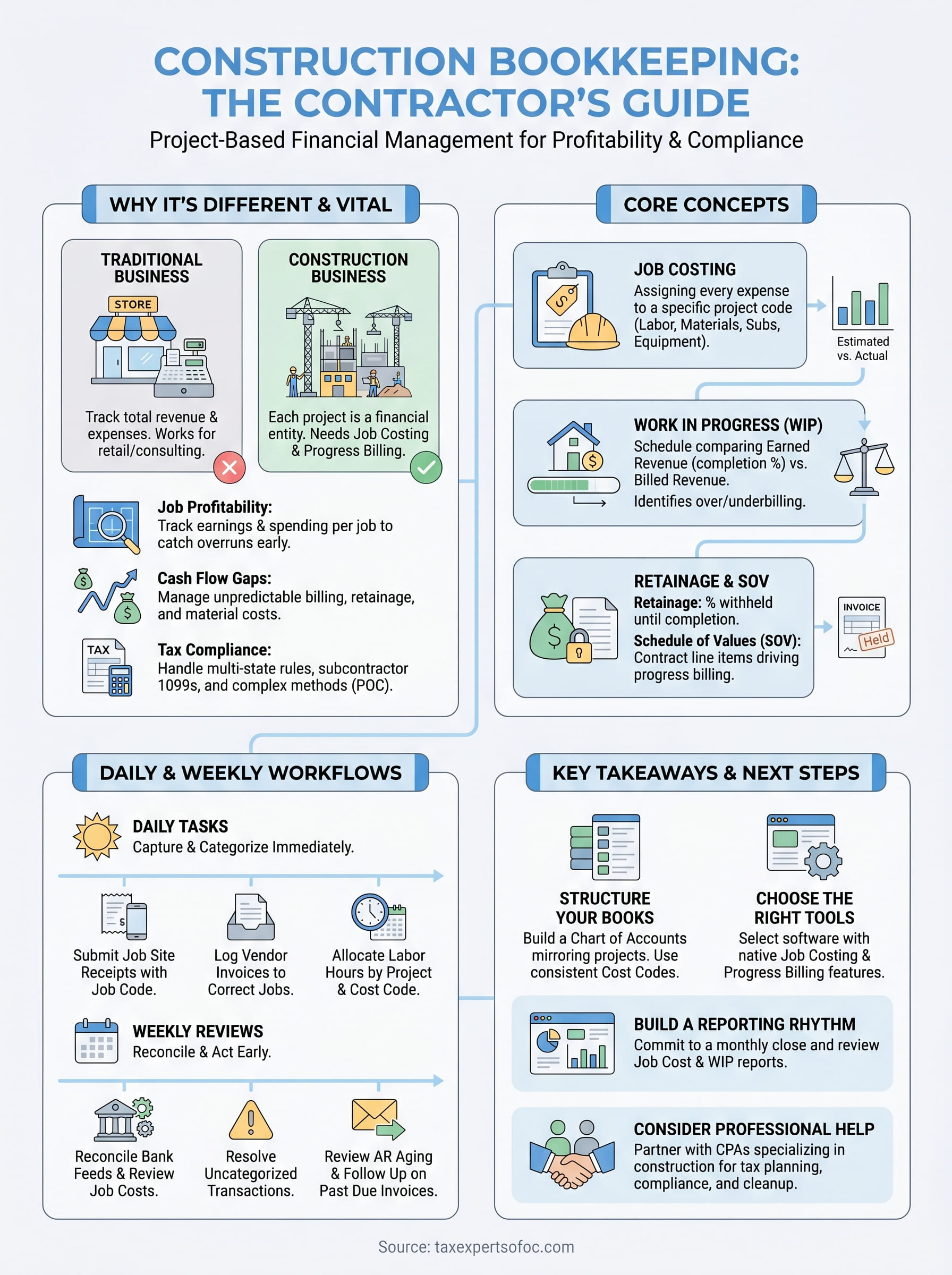

Most business owners track their overall revenue and expenses and call it a day. That approach works for a retail store or a consulting firm. It does not work for construction. Every project you take on is its own financial entity, with its own labor costs, material purchases, subcontractor payments, and billing milestones. If your books don't reflect that structure, you can show a profit on paper while individual jobs quietly drain your business.

Your profits are tied to individual jobs, not just total revenue

Construction work is project-based, and your financial health depends on how profitable each individual job performs, not just your company's total income at year-end. You can land three contracts in a single month and still lose money if one of those jobs runs over budget while the others are still in early phases. Accurate construction bookkeeping lets you track exactly what you're earning and spending on each project in real time, so you can catch cost overruns before they spiral.

Without job-level financial data, you're making decisions based on incomplete information, and in construction, that gap between what you think you're earning and what you're actually earning can be substantial.

When you know your actual cost-to-date on a project against your estimated budget, you can adjust crew schedules, renegotiate supplier terms, or flag a scope change before it becomes a dispute. That level of visibility is only possible if your books are structured to track costs at the project level from day one.

Cash flow gaps can sink a healthy company

Construction cash flow is unpredictable by nature. Progress billing cycles, delayed owner payments, retainage holdbacks, and front-loaded material purchases all create stretches where your expenses outpace what's coming in. Many contractors who go out of business aren't unprofitable on paper; they simply run out of cash while waiting to get paid.

Your books need to show you not just what you've invoiced but what you've actually collected, what's still owed, and how your upcoming payroll and supplier obligations line up against expected receipts. A well-maintained set of books gives you enough lead time to arrange a line of credit, delay a discretionary purchase, or push for faster payment from a slow-paying client. Without that data, you're reacting to cash crunches instead of preventing them.

Proper bookkeeping also makes it easier to work with lenders and bonding companies. When you apply for a construction bond or a business line of credit, the lender will review your financial statements closely. Organized, accurate financials signal that your business is managed well, which directly affects the terms and limits you can access.

Tax compliance depends on accurate project records

Construction businesses face tax obligations that most industries don't deal with at the same scale. You may have workers operating in multiple states, subcontractors who need 1099s, sales tax rules that vary by material and jurisdiction, and the option to use the percentage-of-completion or completed-contract method for reporting long-term project income. Each of these requires clean, detailed records tied to specific jobs and time periods.

The IRS pays close attention to construction companies because the mix of cash transactions, subcontractor payments, and deferred income creates opportunities for errors, both unintentional and intentional. Detailed project records protect you during an audit and ensure you're claiming every legitimate deduction, from equipment depreciation to job-site supplies, without overstating costs that could draw scrutiny.

Bookkeeping vs construction accounting

These two terms get used interchangeably, but they describe different layers of financial management. Bookkeeping handles the day-to-day recording of transactions: income, expenses, invoices, receipts, and payroll entries. Accounting takes that recorded data and turns it into analysis, tax strategy, and financial reporting. Both matter for a construction company, but confusing one for the other leads contractors to either over-rely on their bookkeeper for decisions that require a CPA, or underpay for accounting help they actually need.

What bookkeeping handles in a construction context

In a construction business, bookkeeping tasks include recording vendor bills, posting payments from clients, categorizing labor costs to specific jobs, tracking subcontractor invoices, and reconciling bank accounts. These are recurring, transactional tasks that need to happen consistently, often weekly, to keep your records accurate. Construction bookkeeping specifically requires that these entries link to job codes rather than getting dumped into general expense categories, which is a critical distinction from standard bookkeeping.

If you assign a material purchase to the wrong job, or post a subcontractor payment without tying it to a project, you lose the job-level visibility that makes your financial data useful. Good construction bookkeeping is less about transaction volume and more about precision and structure at the job level.

The quality of your accounting reports is only as good as the bookkeeping data underneath them.

What accounting adds to your financial picture

Accounting goes beyond the transaction log and answers the bigger questions: Are your jobs priced correctly? What's your true overhead rate? How should you recognize revenue on a long-term project? Your accountant or CPA uses the data your bookkeeper records to prepare financial statements, advise on tax elections like the completed-contract or percentage-of-completion method, and help you make decisions about growth, hiring, or equipment purchases.

For construction companies, accounting also includes analyzing work-in-progress schedules, reviewing job cost reports against original estimates, and ensuring your financial statements meet the standards required by bonding companies and lenders. This level of analysis is not something a bookkeeper is trained or positioned to provide, which is why most growing construction firms need both roles covered, either by separate people or through a firm that offers both services under one roof.

Core concepts: job costing, WIP, retainage, SOV

Construction bookkeeping runs on a set of concepts that don't exist in standard small business accounting. If you're new to the industry, or if your books have been managed by someone without construction experience, these terms may not appear anywhere in your records. That's a problem, because each one represents a category of financial information that directly affects whether your business stays profitable and compliant.

Job costing

Job costing is the practice of assigning every expense to a specific project rather than lumping costs into broad general categories. Labor hours, materials, equipment rentals, and subcontractor invoices all get tagged to a job code so you can measure each project's actual cost against the original estimate. Without job costing, you have no way to know which projects made money and which ones didn't.

Knowing your total company revenue means very little if you can't see which jobs drove profit and which ones quietly cost you more than you billed.

The goal of job costing isn't just historical tracking. It helps you build better estimates on future bids by showing you where your actual costs consistently run over your projections.

Work in progress (WIP)

A WIP schedule measures how much revenue you've earned on an active project compared to how much you've billed. If you've billed more than you've earned based on project completion, you're overbilled. If you've earned more than you've billed, you're underbilled. Both conditions affect your financial statements and tax position, and lenders and bonding companies look at WIP schedules closely when evaluating your business.

Keeping an accurate WIP schedule requires updated cost-to-date figures and honest completion percentages on every open job. This is one of the areas where imprecise bookkeeping creates the biggest downstream problems.

Retainage and schedule of values (SOV)

Retainage is the percentage of each progress payment that an owner withholds until the project reaches substantial completion. A typical retainage rate is five to ten percent, and it can sit in accounts receivable for months or years. Your books need to track retainage separately from standard receivables so it doesn't distort your cash flow picture.

A schedule of values breaks a contract into line items with assigned dollar amounts, and it drives each progress billing application. When your SOV is accurate and your progress billing reflects actual completion, your invoices are harder to dispute and your revenue recognition stays clean.

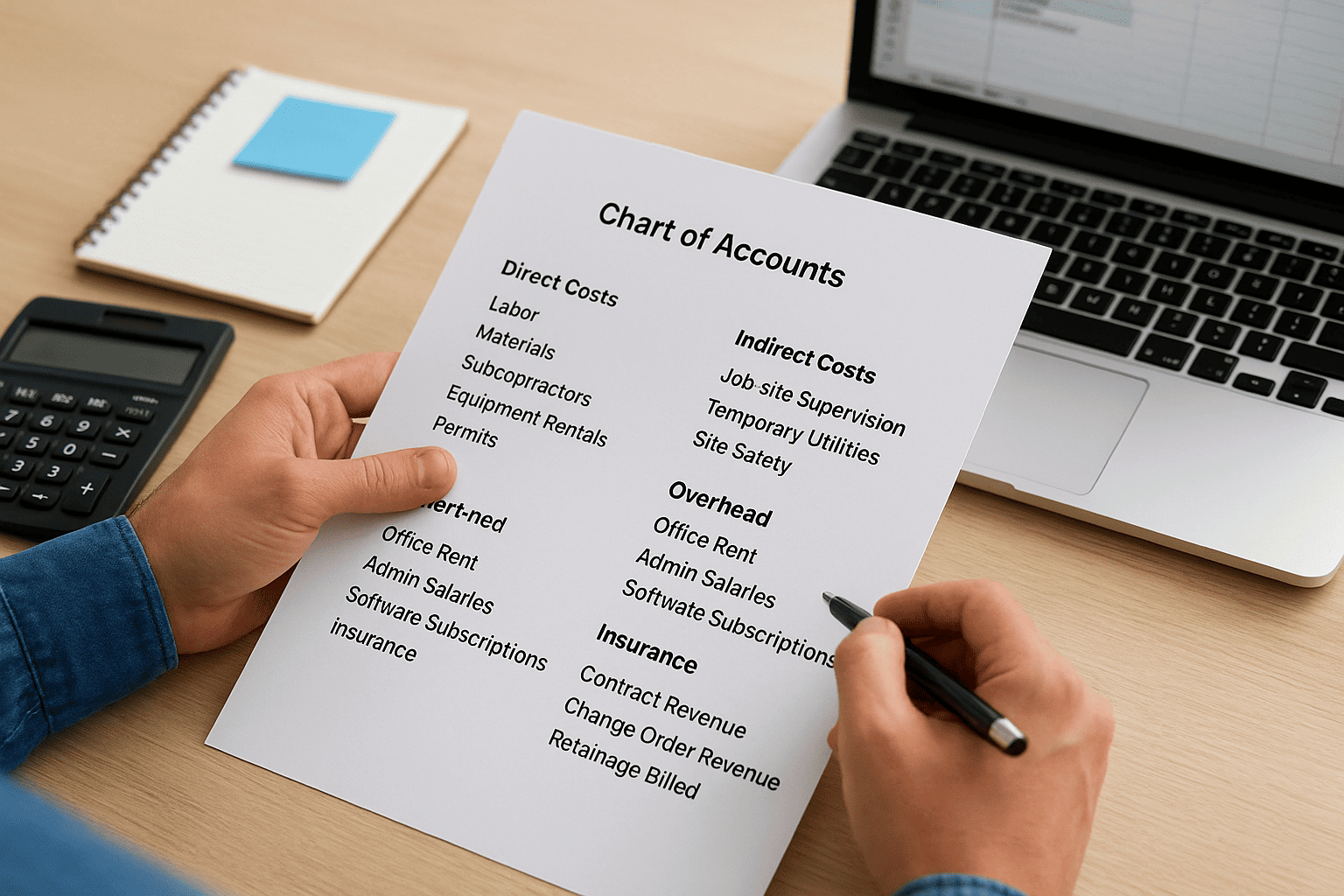

Setting up your chart of accounts and cost codes

Your chart of accounts is the foundation of your entire financial system. In standard bookkeeping, a simple list of income and expense categories is enough. In construction bookkeeping, that list needs to reflect how your business actually operates: by project, by cost type, and by phase. Setting this up correctly from the start saves you from resorting to manual reconciliation when you need to pull job-level reports for a lender, a bonding company, or your own planning.

Build a chart of accounts that mirrors your projects

Most generic accounting templates group all expenses under broad headings like "cost of goods sold" or "operating expenses." That structure tells you nothing useful about how individual jobs performed. Your construction chart of accounts should separate direct job costs from overhead expenses, and within direct costs, break out labor, materials, subcontractors, and equipment as distinct line items.

A well-structured chart of accounts is the difference between a report that helps you make decisions and a report that just confirms money moved.

Here is a basic structure that works for most construction businesses:

- Direct costs: Labor, materials, subcontractors, equipment rentals, permits

- Indirect costs: Job-site supervision, temporary utilities, site safety

- Overhead: Office rent, admin salaries, software subscriptions, insurance

- Revenue accounts: Contract revenue, change order revenue, retainage billed

You can expand each category as your business grows, but starting with this separation keeps your reports readable and your tax filings accurate.

Use cost codes consistently across every job

Cost codes are the layer beneath your chart of accounts. They let you tag every transaction to a specific phase or task within a project, such as framing, electrical rough-in, or concrete work. When you apply cost codes consistently across every job, you can compare actual costs to estimated costs at a granular level and spot which trade or phase regularly runs over budget.

The biggest mistake contractors make is applying cost codes inconsistently, either skipping them when things get busy or using different codes for the same type of work across different jobs. That inconsistency makes your historical data unreliable for future estimating. Set a standard code list at the beginning of each year, train anyone who enters transactions to use it, and audit your job reports monthly to catch miscategorized entries before they compound.

Daily and weekly workflows that keep books clean

Inconsistent data entry is the root cause of most construction bookkeeping problems. When receipts pile up, transactions go unrecorded, and job codes get applied in batches at the end of the month, your books drift from reality. Clean books don't happen by accident; they're the result of small, consistent habits built into your team's routine at both the daily and weekly level. The goal isn't perfection in each individual entry; it's a system that catches errors fast enough to correct them before they compound into a larger mess.

Daily tasks that prevent backlogs

Every day that passes without recording a transaction makes that transaction harder to categorize accurately. Job site expenses like material deliveries, equipment fuel, and small tool purchases happen fast, and if your crew doesn't capture them the same day, the details get blurry quickly. Require anyone who spends company money to submit a receipt, a job code, and a cost category before the end of their shift. This single habit eliminates most month-end reconciliation headaches.

Your daily routine should also include reviewing any new vendor invoices that arrived and logging them to the correct job in your accounting system. Don't let vendor bills sit in an inbox waiting for a payment run. Entering them immediately gives you an accurate picture of committed costs on each active project, even before the invoice comes due.

Weekly reviews that catch problems early

One weekly review does more to keep your books clean than any amount of catch-up work at month-end. Set aside one hour each week to reconcile your bank feed, review job cost summaries, and confirm that all labor entries from the previous week landed on the right projects. This is also the time to flag any transactions sitting in an uncategorized holding account and resolve them before they multiply across multiple pay periods.

A weekly review isn't just a cleanup task; it's your early warning system for jobs that are trending over budget before the damage becomes difficult to reverse.

Use that same weekly session to check your accounts receivable aging report and follow up on any invoice that's past its due date. In construction, slow payment is common, but a consistent follow-up rhythm shortens your average collection time and keeps your cash flow projections accurate throughout each project's lifecycle.

Progress billing, change orders, and invoicing

Construction projects rarely involve a single payment at the end. Instead, you bill clients in stages as work progresses, which means your invoicing process and your actual job costs need to stay in sync at every phase. When your construction bookkeeping doesn't reflect the current billing status of each project, you end up with receivables that don't match your bank account and income figures that misrepresent where each job actually stands.

How progress billing works

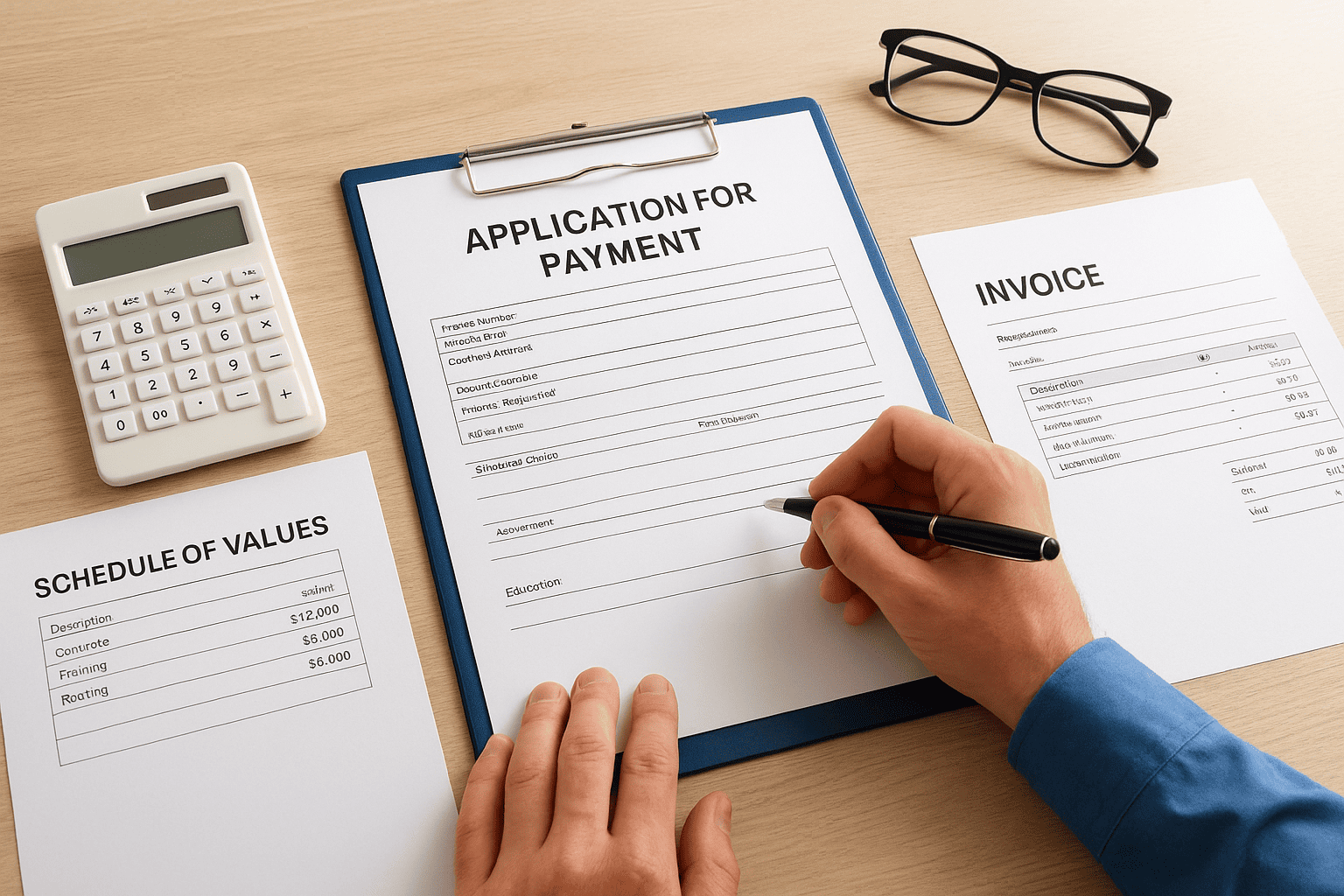

Progress billing ties each invoice to a percentage of work completed or a milestone defined in the contract. Your application for payment documents what you've completed to date, what you've previously billed, and what you're requesting in the current draw. Most general contractors use a standard AIA-style billing format, which references the schedule of values you established at contract execution.

If your schedule of values doesn't accurately reflect how costs will distribute across the project, every billing application you submit will misrepresent your actual earned revenue.

Each billing cycle should tie back to updated cost-to-date figures in your books. That alignment keeps your WIP schedule accurate and protects you if an owner disputes the amount you've requested.

Tracking change orders before they become disputes

Change orders are one of the most common sources of billing problems in construction. When a client requests additional scope, you need to document it, price it, and get it approved in writing before you absorb the cost. Many contractors do the work first and fight over payment later, which puts you in a weak position and leaves your books with costs that have no matching revenue.

Your bookkeeping system should include a change order log for every active project. Track the date requested, the scope description, the estimated cost, the approval status, and the amount billed. When a change order gets approved, update your schedule of values and issue a revised billing application before that work starts showing up in your job cost reports.

Keeping your invoicing consistent

Send invoices on a fixed schedule tied to your contract terms, whether that's monthly, at defined milestones, or upon phase completion. Inconsistent invoicing extends your collection cycle and makes cash flow harder to manage. Always attach backup documentation to every invoice to reduce owner disputes and shorten your approval process. That package should include:

- A current schedule of values showing completion percentages

- A cost summary for the current billing period

- Copies of all approved change orders included in the draw

- Any lien waivers the owner requires as a condition of payment

Payroll, subs, 1099s, and job-related compliance

Labor is typically your largest cost in construction, and how you record it determines whether your job cost reports reflect reality. Payroll in construction isn't a single line item you post to overhead and move on. Every hour your employees work needs to attach to a specific project and cost code, or your job-level data becomes meaningless the moment you try to evaluate profitability.

Allocating payroll costs to the right jobs

Your payroll system needs to capture time by project rather than just total hours worked for the pay period. When employees split their week across multiple jobs, you need timesheets that break down hours by job code so that labor costs land on the right project in your books. This is where construction bookkeeping differs most sharply from standard business payroll: the allocation step isn't optional.

If you post payroll as a lump sum without job-level allocation, every job cost report you pull will understate actual labor costs, and your profitability numbers will be wrong from the start.

Beyond allocation, your payroll records also need to account for burden costs, which include payroll taxes, workers' compensation, and benefits. These costs add a meaningful percentage on top of base wages, and if you're not factoring them into your job cost estimates and actual cost tracking, you're consistently undercounting what labor really costs per project.

Managing subcontractor payments and 1099s

Subcontractors represent a significant portion of most contractors' project costs, and they come with their own compliance requirements. Before you pay any sub, collect a completed W-9 form and verify their business structure. If you pay a non-incorporated subcontractor $600 or more during the calendar year, you're required to issue a 1099-NEC by January 31 of the following year.

The IRS takes 1099 compliance seriously, and missing or incorrect filings carry penalties. Keep a running log throughout the year that tracks each sub's name, tax identification number, total payments, and job assignments. Waiting until December to gather this information creates errors and delays.

Certified payroll and multi-state obligations

If you work on publicly funded projects, most contracts require certified payroll reports that document wages paid, hours worked, and worker classifications in compliance with prevailing wage laws. These reports are separate from your standard payroll records and must be submitted on a fixed schedule. Missing a certified payroll submission can hold up your progress payments or put the contract at risk.

Working across state lines adds another layer of payroll tax obligations, since each state has its own withholding rules, unemployment insurance rates, and registration requirements for employers. Track which employees worked in which states during each pay period so your withholding stays accurate and your year-end filings don't trigger notices.

Choosing software and building a reporting rhythm

The right software doesn't fix bad bookkeeping habits, but it does make good habits far easier to sustain. Construction bookkeeping requires a platform that supports job costing, progress billing, and payroll allocation at the project level. Generic small business accounting tools can technically record transactions, but they lack the project-layer structure that construction financial management demands.

Picking software that fits construction workflows

Not every accounting platform handles the project-based complexity of construction work. When evaluating your options, focus on whether the software supports job costing by cost code, integrated subcontractor tracking, and progress billing that links directly to your schedule of values. Platforms built specifically for construction embed these features natively, while general-purpose tools require manual workarounds that introduce errors over time.

The best software for your business is the one your team will actually use consistently, not the one with the longest feature list.

Before committing to any platform, test how it handles payroll allocation across multiple jobs and whether it produces a WIP schedule without manual intervention. These two capabilities separate a construction-capable tool from software that will create more reconciliation work than it saves.

Building a monthly reporting rhythm

Collecting data in your software is only half the job. The other half is reviewing that data on a fixed schedule so you can act on what it shows you. A monthly reporting rhythm gives you a structured opportunity to compare actual job costs against estimates, review your cash position, and catch any entries that slipped into the wrong account or project during the previous weeks.

Your monthly close should produce at least four core reports: a job cost summary for every active project, a WIP schedule, an accounts receivable aging report, and a profit and loss statement. Run these in sequence each month-end and compare them against the previous period. Patterns in the data, like a specific cost code that consistently runs over budget or a client who always pays late, only become visible when you review these reports consistently over time.

Set a hard deadline for your monthly close, such as the tenth of the following month, and hold your team to it. Delayed closes push your reporting cycle back and leave you making decisions with data that is weeks out of date.

Next steps for cleaner construction books

Clean books don't happen in a single afternoon, but the path forward is straightforward once you know what needs to change. Start by auditing your current chart of accounts to confirm it separates direct job costs from overhead, then verify that your team applies cost codes consistently on every active project. If those two foundations are missing, fix them before you invest time in anything else.

From there, build the weekly review habit described in this guide and commit to a fixed monthly close date. Those two routines do more for the accuracy of your construction bookkeeping than any software upgrade or process overhaul.

If your books are already behind, or if you're facing an IRS notice on top of disorganized records, professional help gets you back on track faster than working through it alone. Schedule a free consultation with Tax Experts of OC to get a clear picture of where your finances stand and what to do next.