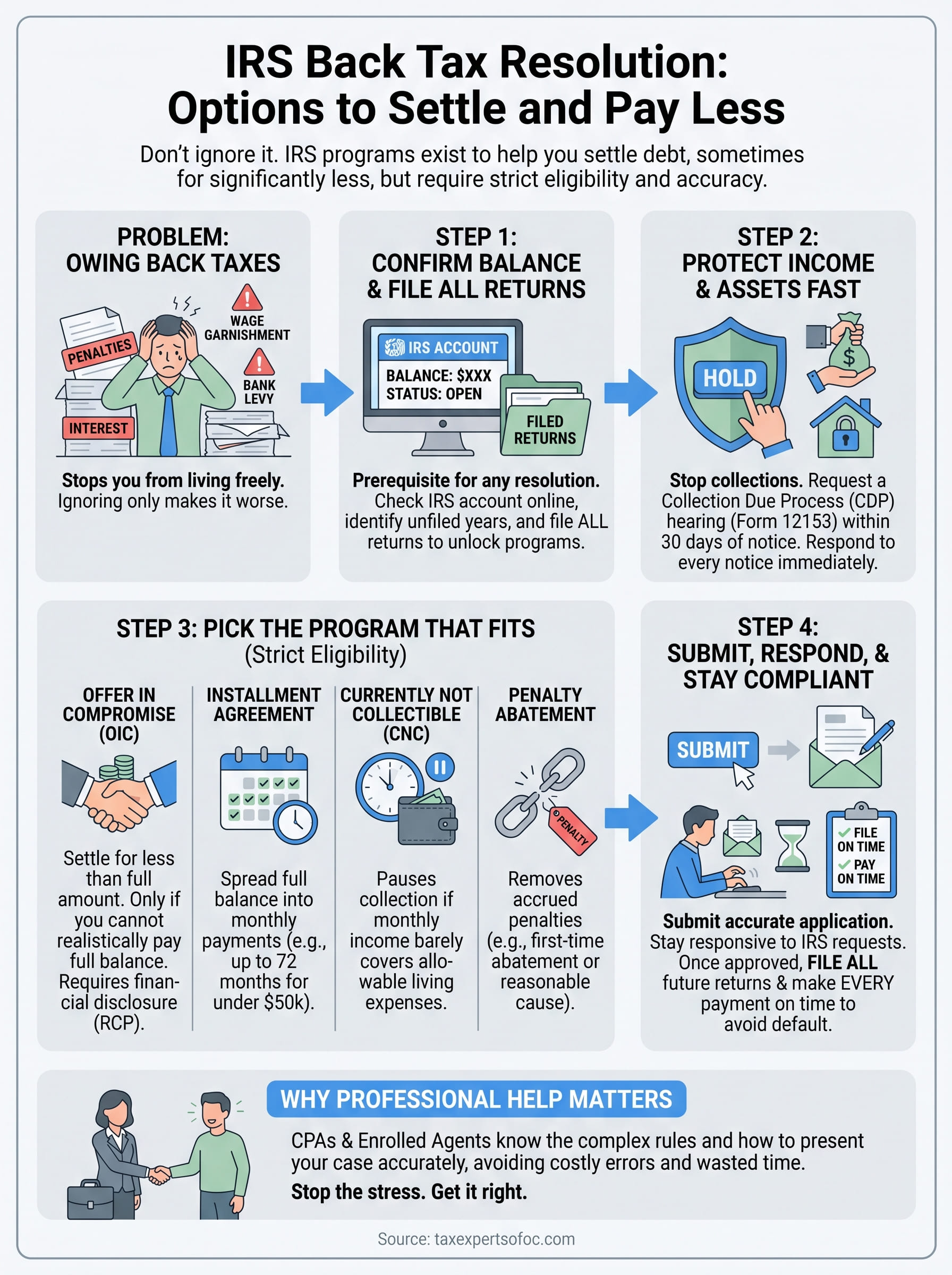

Owing back taxes to the IRS is stressful, and ignoring the problem only makes it worse. Penalties stack up, interest compounds, and the IRS has powerful collection tools, from wage garnishments to bank levies, that can disrupt your life without warning. But here's what many taxpayers don't realize: IRS back tax resolution programs exist specifically to help you settle your debt, sometimes for significantly less than you owe.

The IRS actually wants to work with you. Programs like Offer in Compromise, installment agreements, and the Fresh Start Initiative give taxpayers real paths forward, if you know how to use them. The catch is that each program has strict eligibility requirements, and the application process demands accuracy. One mistake can mean a denial and months of wasted time.

At Tax Experts of OC, our CPAs and Enrolled Agents help individuals and business owners across the country resolve back tax issues through these exact programs. This guide breaks down your options for settling IRS back taxes, walks you through how each program works, and explains when it makes sense to get professional help rather than going it alone.

What IRS back tax resolution really means

Most people assume the IRS will never reduce what you owe. That assumption is wrong. IRS back tax resolution is the formal process of working with the IRS to settle or restructure your tax debt through one of several approved programs. It is not a loophole, and it is not forgiveness handed out freely. It is a structured negotiation backed by federal tax law, and the IRS has clear rules about who qualifies and for how much.

The IRS resolved hundreds of thousands of accounts through installment agreements and settlements last year alone, which means real taxpayers secured real relief.

Resolution vs. simple repayment

These two things are not the same. Simple repayment means you pay the full balance owed, including all accrued penalties and interest, over time through a standard payment plan. True resolution means you use an approved IRS program to reduce the total amount, stop active collection actions, or lock in terms you can actually sustain long-term. The goal of resolution is to close the account on terms that work for your financial situation, not just delay the problem.

What the IRS actually considers

When the IRS reviews your case, it looks at three core factors: your ability to pay, your monthly income and allowable expenses, and the equity in your assets. If you genuinely cannot pay the full amount, programs like Offer in Compromise or Currently Not Collectible status may apply to you. Your case follows a formula, not a guess. Understanding that formula is the first step toward knowing which resolution path gives you the best possible outcome.

Step 1. Confirm the balance and filing status

Before you can pursue any IRS back tax resolution path, you need to know exactly what you owe and whether all your returns are filed. The IRS will not approve an Offer in Compromise or installment agreement if you have unfiled returns, so treat this step as the foundation of everything that follows.

Check your IRS account online

The IRS offers a free account portal at IRS.gov where you can view your current balance, penalties, interest, and tax year breakdowns. Log in with an ID.me account and pull your full account transcript. Look at both your balance due and your filing history to confirm which years have been assessed and which still carry open balances.

If your account shows a balance for a year you already filed, the IRS may have made an adjustment, so compare your transcript against your original return line by line.

Identify any unfiled years

Check your personal records for every year you may have skipped. You can request wage and income transcripts directly from the IRS to reconstruct missing returns accurately. Filing all open years, even late, resets your standing with the IRS and unlocks every resolution program available to you.

Step 2. Protect income and assets fast

Once you know your balance, your next priority is stopping the IRS from taking action against your income or property. The IRS can issue a levy on your wages or bank account with relatively short notice, and a federal tax lien can attach to your property the moment an assessment is made. Moving quickly puts you in control rather than letting the IRS dictate the terms.

Request a hold on collections

You can request a Collection Due Process (CDP) hearing by filing Form 12153 within 30 days of receiving a Final Notice of Intent to Levy. This formally pauses collection activity while your case is reviewed. During this window, work on your irs back tax resolution strategy so you enter any IRS negotiation with a clear plan already in place.

Filing Form 12153 on time is one of the most effective ways to stop a levy before it starts.

Respond to every IRS notice immediately

Each IRS notice carries a specific response deadline, and missing it can trigger automatic enforcement. When you receive a notice, take these steps right away:

- Note the response deadline printed on the notice

- Confirm your current mailing address on file with the IRS

- Send your reply by certified mail and keep a copy

Step 3. Pick the IRS program that fits

Once your returns are filed and collections are on hold, you can match your situation to the right IRS back tax resolution program. Each option carries different eligibility rules, so choosing the wrong one wastes time and risks an outright denial.

Applying to the wrong program does not just delay your case; it can also reset IRS negotiation timelines and cost you months.

Offer in Compromise

This program lets you settle your tax debt for less than the full amount owed. The IRS approves an OIC when it determines you cannot realistically pay the full balance. Your offer must equal or exceed your Reasonable Collection Potential (RCP), which the IRS calculates using your assets and projected future income. Use the free pre-qualifier tool at IRS.gov to check eligibility before you invest time in a full application.

Installment Agreement and Other Paths

If an OIC does not fit, you have additional structured options, and each one targets a different financial situation:

- Currently Not Collectible (CNC): Pauses collection activity if your monthly income barely covers allowable living expenses

- Installment Agreement: Spreads your full balance into monthly payments, up to 72 months for balances under $50,000

- Penalty Abatement: Removes accrued penalties if you qualify under first-time abatement or a documented reasonable cause

Step 4. Submit, respond, and keep it fixed

Submitting your application is not the finish line; it is the start of an active review process. The IRS will verify your financial disclosures, cross-check your income data, and may send a written request for additional documentation within 30 to 60 days. Staying responsive throughout this phase is what determines whether your irs back tax resolution case gets approved or rejected.

Missing a single IRS information request during the review process can result in automatic rejection of your application.

What to include when you submit

Your submission package must be complete and accurate from day one because incomplete filings are the most common reason the IRS rejects applications outright. Include these required documents for an Offer in Compromise:

- Form 656 (Offer in Compromise) with the $205 application fee

- Form 433-A (OIC) with full financial disclosure

- Supporting records: pay stubs, bank statements, and asset documentation

Stay compliant after approval

Approval gives you a formal agreement with the IRS, but it also comes with strict ongoing conditions. You must file all future tax returns on time and make every scheduled payment without exception. One missed payment or unfiled return can void your agreement and restore the full original balance immediately.

Your next steps

You now have a clear picture of how IRS back tax resolution works and which programs match different financial situations. The path forward starts with two concrete actions: pull your IRS account transcript to confirm your exact balance and filing status, then match that information to the program that fits your situation. Whether that means an Offer in Compromise, an installment agreement, or a penalty abatement request, moving fast protects your income and limits what the IRS can take.

Getting the details wrong on these applications costs you time and money, and one incomplete form can set you back months. Working with a licensed CPA or Enrolled Agent gives you a significant advantage because they know exactly what the IRS looks for and how to present your case accurately. If you are ready to stop the stress and start resolving your tax debt, schedule a free consultation with Tax Experts of OC today.