Owing the IRS is stressful. Whether you missed a filing deadline, underreported income, or simply couldn't afford to pay what you owed, the balance doesn't go away on its own. Penalties and interest stack up, and the IRS has collection tools, wage garnishments, bank levies, tax liens, that most creditors can only dream of. If you're searching for how to resolve back taxes, you're already taking the right first step: figuring out what options actually exist before the situation gets worse.

The good news is that the IRS offers several formal programs designed to help taxpayers settle or manage unpaid debt. Installment agreements, offers in compromise, penalty abatement, and currently not collectible status are all on the table, but qualifying for each one depends on your specific financial picture and filing history.

This guide walks you through every major option available in 2026, the steps involved, and what to expect along the way. At Tax Experts of OC, our CPAs and Enrolled Agents resolve back tax cases for clients across all 50 states, so we've built this resource around what actually works in practice, not just what the IRS website tells you in theory.

What back taxes are and why you must act

Back taxes are any federal or state taxes that you owed in a prior year but did not pay in full by the original due date. The term covers a wide range of situations: a balance left unpaid after filing, a return you never filed at all, or an amount the IRS assessed after auditing your records. Understanding exactly what you're dealing with is the first move in figuring out how to resolve back taxes in a way that protects your finances and your long-term standing with the IRS.

What the IRS considers back taxes

The IRS treats unpaid taxes as a debt that grows over time. Penalties and interest begin accruing the day after your payment was due, and they don't stop until the balance is paid in full or formally resolved. Two main penalty types drive up your balance faster than most people expect:

- Failure-to-file penalty: 5% of the unpaid tax for each month your return is late, capped at 25% of the unpaid amount.

- Failure-to-pay penalty: 0.5% of the unpaid tax per month, also capped at 25%.

On top of those penalties, the IRS charges interest compounded daily at the federal short-term rate plus 3 percentage points. As of early 2026, that combined rate sits at 7%. A $10,000 balance can grow beyond $12,500 within two years without you receiving a single new assessment from the IRS.

The longer you wait to address back taxes, the smaller your resolution options become, because several IRS programs require your balance or your income to fall within specific thresholds.

What the IRS can do to collect

Unlike most creditors, the IRS can take collection action against you without going to court first. Once it issues a Notice of Intent to Levy, a wide range of tools become available almost immediately. That power is what makes back taxes different from other debts and why acting early puts you in a much stronger position.

Here is what the IRS can do once collection activity starts:

| IRS Collection Action | What It Means for You |

|---|---|

| Federal Tax Lien | A public claim against your property, including real estate and financial accounts |

| Wage Garnishment | The IRS contacts your employer directly and takes a portion of each paycheck |

| Bank Levy | The IRS freezes and seizes funds from your bank account |

| Passport Denial | Seriously delinquent debt over $62,000 in 2026 can trigger passport revocation or denial |

| Asset Seizure | The IRS can seize and sell physical property to satisfy the debt |

The 10-year collection window

The IRS generally has 10 years from the date of assessment to collect a tax debt, a deadline known as the Collection Statute Expiration Date (CSED). This rule sounds like built-in relief, but it rarely works the way people hope. The clock pauses during any period when the IRS cannot legally collect, including while an installment agreement is pending, during bankruptcy, or while an Offer in Compromise is under review. In practice, waiting out the clock keeps you in a state of financial uncertainty for a decade or more, with liens on your credit and collection notices arriving at any time. Resolving the debt directly and deliberately is almost always the faster path to financial stability.

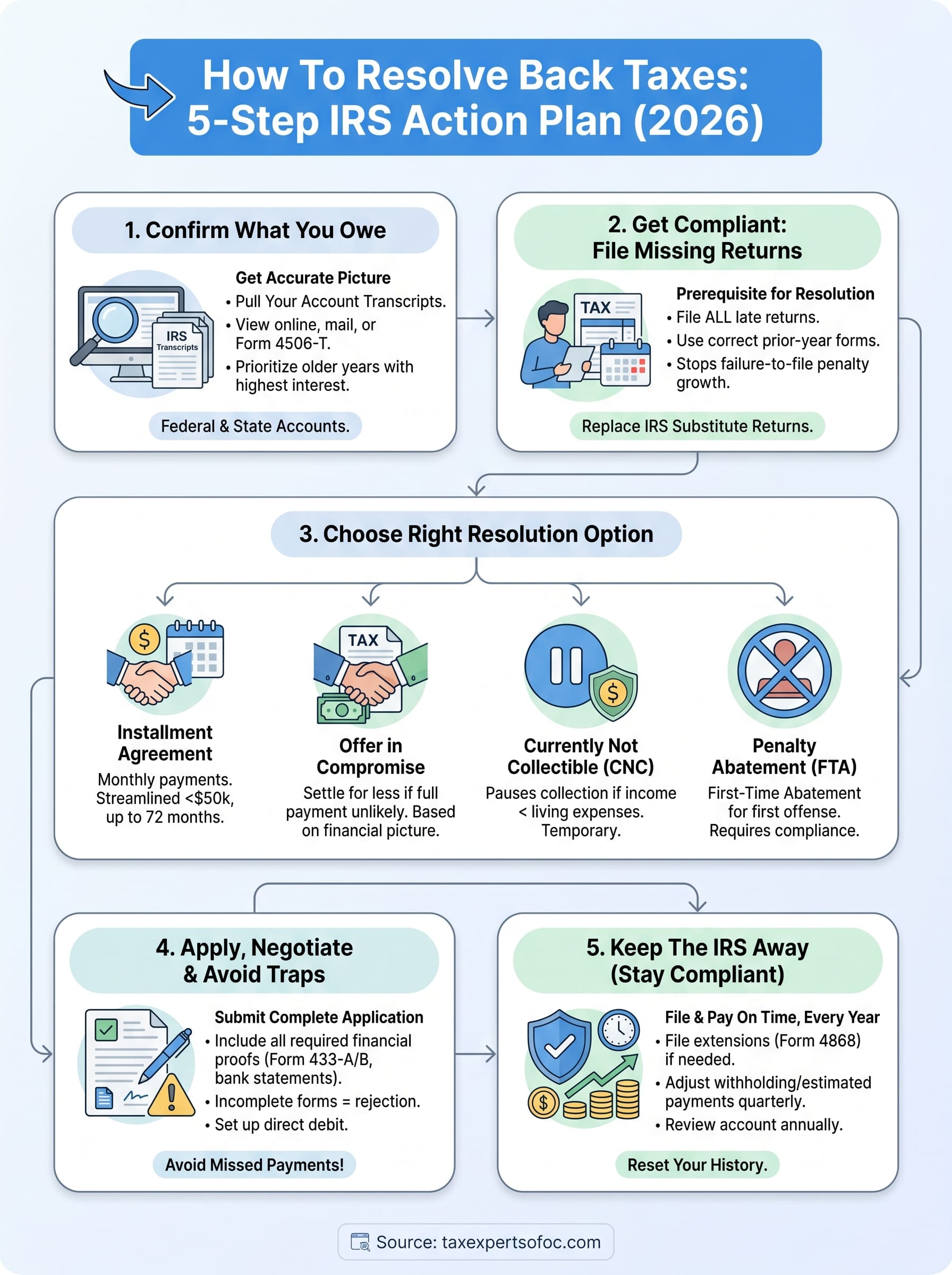

Step 1. Confirm what you owe and for which years

Before you can figure out how to resolve back taxes, you need an accurate picture of what the IRS says you owe. Many taxpayers guess at their balance or rely on outdated notices, which leads to applying for the wrong program or submitting incomplete paperwork. Getting the correct numbers from the IRS directly is where every successful resolution starts.

Pull your IRS transcripts

The IRS keeps a detailed record of every return filed, every assessment made, and every payment received under your Social Security number. Your account transcript is the most useful document for this step because it shows your balance by tax year, including all penalties and accrued interest. You can access transcripts in three ways:

- Online: Log in to IRS.gov and use the "Get Transcript" tool. You can view and download records immediately after verifying your identity.

- By mail: Request a mailed copy through the same portal or by calling 1-800-908-9946. Delivery takes 5 to 10 calendar days.

- Form 4506-T: Submit this form to request transcripts for business entities or to authorize a third-party representative to pull records on your behalf.

Pull transcripts for every year you are unsure about, not just the most recent one, because older balances carry the highest accrued interest and may have active liens attached.

Once you have your transcripts, list each tax year with an open balance, the original amount assessed, and the current amount due. This breakdown becomes the foundation for every conversation you have with the IRS or a tax professional going forward.

Check your state tax accounts

Federal back taxes and state back taxes are separate obligations, and the IRS transcript covers only federal debt. Most states run their own revenue agencies, issue separate notices, apply separate penalties, and collect independently. If you owe the IRS for a given year, there is a strong chance your state return for that same year carries a matching problem.

Log in to your state's official revenue department website to review your account balance. If you are unsure where to start, search for "[your state] department of revenue" to locate the correct government portal.

Step 2. Get compliant by filing missing returns

The IRS will not approve any resolution program, including installment agreements or an Offer in Compromise, until you have filed all required returns. Filing compliance is a non-negotiable prerequisite. If you skipped returns for multiple years, your first task is to get those filed before you take any other step toward resolving your debt. Understanding this requirement is central to knowing how to resolve back taxes without wasting time on applications the IRS will automatically reject.

Why unfiled returns block your resolution

When the IRS detects that you have unfiled returns, it often prepares a Substitute for Return (SFR) on your behalf using income data from W-2s, 1099s, and third-party reports. An SFR uses the least favorable filing status, takes no deductions beyond the standard deduction, and generates the highest possible tax bill. If the IRS filed an SFR for you, you can and should replace it with your own accurate return, which frequently results in a lower balance.

Replacing an IRS Substitute for Return with your own filing is one of the fastest ways to reduce the amount you owe before you even begin negotiating a resolution.

How to file your late returns

Filing a late return uses the same IRS forms as filing on time. The key difference is that you must use the version of each form published for the specific tax year you are filing. For example, a 2021 tax return requires the 2021 Form 1040, not the current year's version.

Follow these steps for each year with a missing return:

- Gather your income documents for that year: W-2s, 1099s, K-1s, and records of any deductible expenses.

- Download prior-year forms directly from the IRS forms archive at IRS.gov.

- Complete and sign each return for its specific tax year.

- Mail each return separately to the IRS address listed in the instructions for that form. The IRS does not accept prior-year returns through e-file for most older tax years.

- Keep a copy of everything you send, along with a dated mailing receipt as proof of submission.

Submitting your late returns stops the failure-to-file penalty from growing further and gives you an accurate balance to carry into the next step.

Step 3. Choose the right IRS resolution option

Once you've confirmed your balance and filed all missing returns, you're ready to match your situation to the right IRS program. Knowing which program fits your financial picture is the most critical decision in figuring out how to resolve back taxes, because applying for the wrong option wastes months and can leave collection actions in place longer than necessary.

Installment Agreement

An Installment Agreement (IA) lets you pay your balance in monthly payments over time. If you owe $50,000 or less in combined tax, penalties, and interest, you can apply online through the IRS Online Payment Agreement tool at IRS.gov without submitting any financial documentation upfront.

A streamlined installment agreement for balances under $50,000 gives you up to 72 months to pay, which keeps the monthly payment manageable for most taxpayers.

Offer in Compromise

The Offer in Compromise (OIC) lets you settle your debt for less than the full amount owed when the IRS determines that full collection is unlikely given your assets and income. The IRS calculates your Reasonable Collection Potential to decide whether to accept your offer.

| OIC Basis | What It Means |

|---|---|

| Doubt as to Collectibility | You cannot pay the full amount now or in the future |

| Doubt as to Liability | You dispute the assessed amount |

| Effective Tax Administration | Full payment would create a severe financial hardship |

Currently Not Collectible Status

Currently Not Collectible (CNC) status pauses all IRS collection activity when your monthly income does not cover your basic allowable living expenses. The IRS stops levies and garnishments while this status is active.

CNC is a temporary holding position, not a permanent fix. Penalties and interest continue to accumulate, and the IRS reviews your income regularly to determine whether to resume collection.

Penalty Abatement

First-Time Penalty Abatement (FTA) removes failure-to-file and failure-to-pay penalties for taxpayers who meet specific conditions. You can request FTA by calling 1-800-829-1040 or by submitting a written request that references your tax year and case number.

To qualify for FTA, you must meet all three of the following:

- Filed all required returns or filed a valid extension

- Paid, or arranged to pay, any tax currently owed

- Had no penalties assessed in the three prior tax years

Step 4. Apply, negotiate, and avoid common traps

Once you've selected the right IRS program, the application process itself becomes the next place where cases fall apart. Knowing how to resolve back taxes requires more than picking the right option; it requires submitting accurate, complete paperwork that matches the financial picture the IRS already has on file. Incomplete or inconsistent applications are the most common reason resolutions get delayed, returned, or rejected outright.

Submit a complete application

Every IRS resolution program has its own required forms, and submitting the wrong version or leaving fields blank triggers an automatic rejection or a lengthy back-and-forth correspondence cycle. For an Offer in Compromise, you will need Form 656 along with Form 433-A for individuals or Form 433-B for businesses. These financial disclosure forms require you to document every asset, income source, and allowable monthly expense, supported by actual documentation.

Attach bank statements, pay stubs, and proof of monthly expenses to your OIC application before you send it; missing documents are the top reason the IRS returns offers without processing.

For an installment agreement, gather the following before you start the online application at IRS.gov:

- Your most recent filed tax return

- Your Social Security number or Employer Identification Number

- The specific tax years and balances you owe

- Bank account details if you plan to use direct debit

Avoid these common traps

The IRS cross-references your financial disclosures on Form 433-A against third-party income data it already holds from employers, banks, and payment processors. Any inconsistency between what you report and what the IRS sees in its records will pause your case and may result in a lower counteroffer or outright denial. Report every income source, including freelance work, rental income, and retirement distributions, even when those amounts feel small relative to your total debt.

A second trap is missing a payment after the IRS approves your installment agreement. One missed payment puts the agreement into default, reinstates the full balance immediately, and removes the protections that were keeping levies and liens from escalating. Set up automatic direct debit when you apply so your payment processes without requiring action from you each month, and treat that amount as a fixed obligation that comes before any discretionary spending.

Step 5. Keep the IRS from coming back

Resolving your back taxes is only half the job. Once the IRS closes your case or approves your agreement, your compliance history resets, and any new missed filing or missed payment can restart the entire collection cycle from scratch. Knowing how to resolve back taxes matters less than never needing that knowledge again, so the final step is building habits that keep your account clean going forward.

File and Pay on Time, Every Year

The single most effective thing you can do after resolving a back tax issue is to file every return by the due date, even when you cannot pay the full amount owed. A timely filed return with a partial payment stops the failure-to-file penalty, which at 5% per month is ten times more expensive than the failure-to-pay penalty. If you need more time to file, submit Form 4868 before the April deadline to get an automatic six-month extension, but remember that an extension to file is not an extension to pay.

Submitting Form 4868 on time eliminates the failure-to-file penalty entirely, even if you still owe a balance when you eventually submit your return.

Adjust Your Withholding or Estimated Payments

Most people end up with back taxes because their withholding was too low or because they earned self-employment income without making quarterly estimated payments. Both problems are preventable with a small amount of planning. Use the IRS Withholding Estimator at IRS.gov to check whether your current W-4 settings will cover your liability for the year. If you are self-employed or receive investment income, set a reminder to pay estimated taxes quarterly on the following schedule:

| Quarter | Payment Due Date |

|---|---|

| Q1 (Jan 1 - Mar 31) | April 15 |

| Q2 (Apr 1 - May 31) | June 15 |

| Q3 (Jun 1 - Aug 31) | September 15 |

| Q4 (Sep 1 - Dec 31) | January 15 (following year) |

Review Your Account Annually

Pull your IRS account transcript at least once per year after your resolution is complete. Confirm that all payments have been credited correctly, that no new assessments have appeared, and that your installment agreement balance is decreasing as expected. Catching a discrepancy early costs you an hour; catching it two years later can cost you thousands.

A simple plan to finish strong

Knowing how to resolve back taxes comes down to five repeatable steps: confirm your balance, file every missing return, choose the right IRS program, submit a complete application, and stay compliant once the case closes. Each step builds directly on the one before it, so skipping ahead or guessing at your numbers will cost you time and money you cannot afford to lose.

Taking action now puts you in the strongest negotiating position with the IRS. The longer your debt sits unresolved, the more penalties and interest chip away at the options available to you. Whether you handle this yourself or work with a professional, the path forward is clear.

If your situation involves multiple years, disputed amounts, or active collection notices, the team at Tax Experts of OC can help you build a resolution plan that protects your finances and puts this behind you for good.