Owing money to the IRS puts you in a stressful position, but it's one that thousands of Orange County residents and business owners deal with every year. Whether you're facing wage garnishments, tax liens, or a growing pile of unfiled returns, IRS tax resolution in Orange County starts with understanding what options are actually available to you, and what each one costs. The good news: the IRS has formal programs designed to help taxpayers settle or reduce their debt, and you don't have to figure them out alone.

At Tax Experts of OC, our CPAs and Enrolled Agents work directly with the IRS on behalf of individuals and businesses across Orange County and nationwide. We've helped clients negotiate installment agreements, submit offers in compromise, and lift active collections actions, all with transparent pricing and a free 30-minute consultation to assess where you stand.

This guide breaks down the main resolution paths, what they typically cost, and the steps involved in moving from IRS trouble to a clear plan forward. If you're weighing your options, this is the right place to start.

What IRS tax resolution means in Orange County

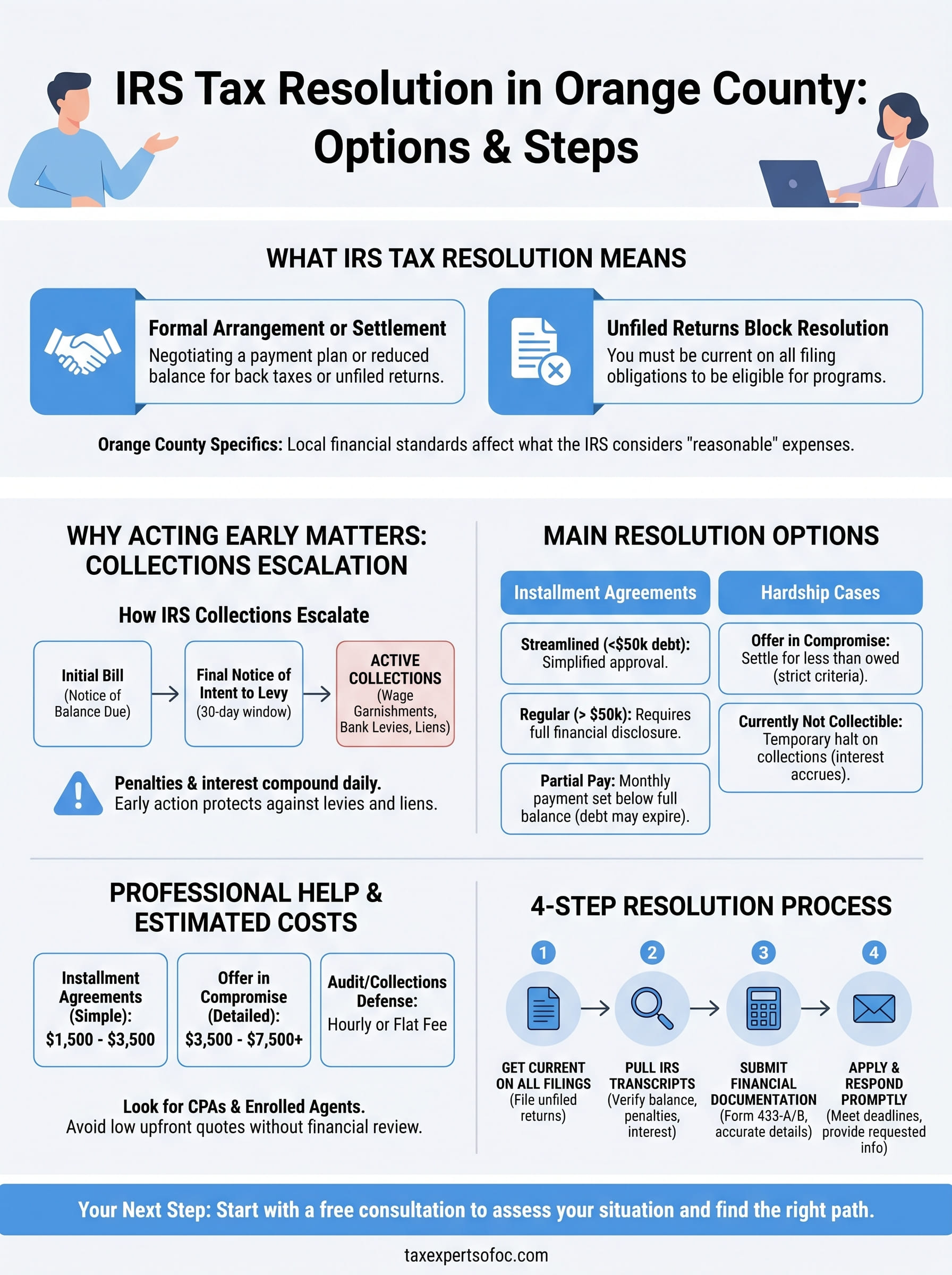

IRS tax resolution is the process of negotiating a formal arrangement or settlement with the Internal Revenue Service when you owe back taxes, have unfiled returns, or are facing active collections. It's not a single program but a category of tools the IRS makes available to taxpayers who need to address outstanding debt. For anyone pursuing IRS tax resolution in Orange County, the federal rules are the same as anywhere else in the country, but California-specific obligations and local financial standards add layers that directly affect which options fit your situation best.

How the IRS defines "resolution"

The IRS considers your situation resolved when you either pay what you owe in full, enter an approved repayment arrangement, or qualify for a program that reduces or eliminates your balance. Each path has its own eligibility requirements tied to your income, your assets, and the nature of the debt itself. Not every program is available to every taxpayer, which is why understanding the criteria matters before you commit to any approach.

Your filing history is also a gating factor. Unfiled returns will block you from most resolution programs because the IRS requires you to be current on all filing obligations before it will negotiate any formal arrangement. That means your first move is often getting every return submitted, even when you can't pay the balance that comes with it.

Being current on your filings is a hard eligibility requirement for most IRS programs, not a suggestion you can work around later.

What makes Orange County cases distinct

California residents carry a layer of complexity that taxpayers in most other states don't face. When you owe the IRS, there's a strong chance you also owe the California Franchise Tax Board, which runs its own collections system entirely separate from the federal one. Settling with the IRS does not touch your state balance, and the FTB can pursue its own liens and levies on its own timeline.

Orange County's high cost of living also plays a role in how the IRS evaluates your case. When the agency reviews your finances for programs like an Offer in Compromise or an installment agreement, it uses national and local expense standards to decide what counts as a reasonable monthly cost. Those local figures can work in your favor, but only if someone who understands IRS financial analysis presents your numbers correctly.

What resolution is not

Resolution is not a pause button. Interest and penalties keep accumulating on your unpaid balance even while you're in active negotiations with the IRS, which is why the timing of your approach matters. It's also not a quick process. A properly structured resolution requires financial disclosure, supporting documentation, and in most cases, direct representation by a CPA or Enrolled Agent who can communicate with the IRS on your behalf and push the process forward without costly mistakes.

Why acting early matters with IRS collections

The IRS doesn't wait for you to be ready. Once you have unpaid tax debt, the agency follows a predictable escalation path, and each step it takes gives you fewer options and less leverage. The earlier you engage with the process, whether on your own or through a professional handling IRS tax resolution in Orange County, the more programs remain available to you and the lower your total cost tends to be.

How IRS collections escalate

The IRS starts with notices, but it moves quickly from paper to action. After an initial bill, the agency issues a Final Notice of Intent to Levy, which gives you 30 days to respond before it can legally seize wages, bank accounts, or other assets. If you miss that window, active collections begin and the options to pause or negotiate become significantly harder to access without professional representation.

Penalties and interest also compound daily on your unpaid balance. The failure-to-pay penalty runs 0.5% per month, and it stacks with failure-to-file penalties if your returns aren't current. That math works against you every day you delay, and there's no mechanism that pauses it while you figure out your next move.

The sooner you respond to IRS notices, the more resolution programs stay open to you and the less your total balance will have grown by the time you settle.

What early action actually protects

Acting before the IRS issues a levy or files a lien gives you the ability to request a Collection Due Process hearing, which places a hold on enforcement while you present your case. Once a levy is active, reversing it requires a separate process that takes more time and additional documentation to resolve.

A lien on your property creates a public record that damages your credit and complicates real estate transactions or business financing. Preventing a lien from being filed is significantly easier than removing one after it's recorded. Professionals who work regularly with the IRS know how to use the agency's own procedures to protect your assets while a resolution is being structured on your behalf.

IRS tax resolution options that actually apply

Not every IRS resolution program fits every situation, and applying to the wrong one wastes time and can trigger more scrutiny from the agency. Understanding the main programs available and the basic eligibility criteria behind each one helps you approach IRS tax resolution in Orange County with a clear target rather than a guess.

Installment agreements

An installment agreement lets you pay your tax debt in monthly payments over time rather than in one lump sum. The IRS offers streamlined agreements for balances under $50,000 that require less documentation and can often be approved without a full financial review. For larger balances, the agency requires a Collection Information Statement that breaks down your income, expenses, and assets before it sets a monthly payment amount.

Partial Pay Installment Agreements are a separate option worth knowing about. With this arrangement, your monthly payment is set below what would be needed to pay the balance in full by the collection statute expiration date, meaning some of your debt effectively expires unpaid. Qualifying requires detailed financial documentation, but it can lower your total outlay significantly compared to a standard installment plan.

Programs for hardship cases

An Offer in Compromise allows you to settle your tax debt for less than the full amount owed if you can demonstrate that paying in full would create genuine financial hardship. The IRS evaluates your offer using a formula based on your remaining income after allowable expenses plus your asset equity. Acceptance rates are relatively low because the eligibility bar is strict, but for taxpayers who do qualify, the savings can be substantial.

The IRS rejects most Offer in Compromise submissions that arrive without complete, accurate financial documentation, which is why professional preparation matters.

Currently Not Collectible status is a different path for taxpayers whose income barely covers basic living expenses. The IRS can temporarily halt all collection activity, including wage garnishments and bank levies, while your account carries this status. Interest still accrues during this period, so it works best as a short-term bridge while you stabilize your finances and build a longer-term plan.

Costs and how to choose the right help

Professional IRS resolution help comes at a cost, and knowing what to expect upfront keeps you from getting surprised mid-process. Fees vary based on the complexity of your case, the programs involved, and the credentials of the person representing you. For anyone researching IRS tax resolution in Orange County, understanding the fee structure before signing any agreement is just as important as understanding the resolution options themselves.

What professional IRS help typically costs

Tax resolution fees generally fall into a few categories depending on what your case requires. Simple installment agreement setups might cost between $1,500 and $3,500. Offer in Compromise preparation, which involves detailed financial analysis and documentation, typically runs $3,500 to $7,500 or more because of the work involved. Audit representation and full collections defense are usually priced by the hour or structured as flat fees after an initial case review.

Be cautious of firms that quote low fees before reviewing your financials. A legitimate tax professional needs to see your full financial picture before they can give you an accurate estimate, and upfront quotes without a case review are often a sign that the price will climb once they learn more about your situation.

A qualified professional should explain what your case realistically involves before asking you to commit to any fee arrangement.

How to evaluate a tax resolution firm

Your representative's credentials matter more than their advertising. CPAs and Enrolled Agents are licensed professionals with the legal authority to represent you directly before the IRS. Tax attorneys carry that authority as well. Avoid anyone who cannot clearly state their credentials and explain how they plan to handle your specific situation from the start.

Check for transparent pricing and a written contract before any work begins. A reputable firm will explain exactly what the fee covers, how long the process typically takes, and what happens if your situation changes along the way. Asking about flexible payment options is reasonable if you are currently in financial hardship, and a professional firm should have a straightforward answer.

Step-by-step process to resolve IRS debt

Knowing your options is only useful if you know how to move from your current situation to an actual resolution. The process for IRS tax resolution in Orange County follows a consistent sequence, and skipping steps is the most common reason cases drag out longer than they should. Here is a practical breakdown of how a properly handled case moves from start to finish.

Step 1: Get current on all filings

Before the IRS will negotiate anything with you, every unfiled return must be submitted. This is a hard requirement, not a formality. Gather your W-2s, 1099s, and any business records that apply to the years in question and work with a professional to prepare accurate returns. Filing late returns does not automatically trigger additional penalties beyond what is already accumulating on your unpaid balance.

Step 2: Pull your IRS transcripts

Once your filings are current, request your Account Transcript and Wage and Income Transcript directly from the IRS. These documents show exactly what the agency has on file for you, including penalties, interest, and any credits already applied. Understanding your actual balance before applying to any program prevents you from underestimating what you owe or overpaying in a settlement.

Reviewing your IRS transcripts before any negotiation gives you an accurate starting point and prevents costly surprises mid-process.

Step 3: Submit your financial documentation

Most resolution programs require a completed Collection Information Statement (Form 433-A for individuals or 433-B for businesses). This form details your income, monthly expenses, and asset values. The accuracy of this document directly affects which programs you qualify for and what payment amount the IRS will accept. A CPA or Enrolled Agent can help you present your numbers correctly within the IRS's own allowable expense guidelines.

Step 4: Apply and respond to IRS correspondence

Submit your application for the program that fits your situation and respond to every IRS notice promptly. The IRS will often request additional documentation before issuing a decision. Missing a response deadline can restart the process entirely, so treat every piece of IRS mail as time-sensitive from the moment it arrives.

Your next step

If you have read this far, you already know enough to take a productive first step toward resolving your IRS debt. The process behind IRS tax resolution in Orange County is structured and manageable when you work with someone who knows the programs, the timelines, and the documentation the IRS actually requires. Waiting only gives penalties more time to compound and gives the IRS more room to escalate.

At Tax Experts of OC, a licensed CPA or Enrolled Agent will review your situation directly, not a general staff member or an automated intake form. You get a free 30-minute consultation to discuss your balance, your filing history, and the options that realistically fit your case. Flexible payment plans are available if you are currently in hardship.

Schedule your free IRS tax resolution consultation today and walk away with a clear picture of where you stand and what to do next.