Working a side gig, picking up seasonal shifts, or holding down two part-time positions all have one thing in common: taxes with multiple jobs get complicated fast. Each employer withholds taxes as if that paycheck is your only income, which usually means not enough is taken out overall. The result? A surprise tax bill in April that hits harder than expected.

The good news is this is entirely manageable once you understand how the pieces fit together. You need to know how multiple income sources affect your tax bracket, how to fill out your W-4 correctly at each job, and how to file everything on a single return without overpaying or underpaying.

This guide walks you through each step, from adjusting your withholdings today to filing accurately next season. And if your situation feels too tangled to sort out alone, Tax Experts of OC helps multi-job filers across all 50 states get their returns right and their withholdings dialed in. Our CPAs and Enrolled Agents work with people in exactly this situation, offering a free 30-minute consultation to review where you stand.

What changes when you work multiple jobs

When you add a second or third employer to the mix, the tax system does not automatically adjust. Each employer uses your W-4 to calculate how much federal income tax to withhold, but they only see their slice of your income. That means every employer treats your pay as if it's your sole source of income, calculating withholdings based on a lower tax bracket than you actually fall into once all of your paychecks are added together.

The withholding problem explained

This is the core issue with taxes with multiple jobs: each employer withholds independently. Say Job A pays you $30,000 a year and Job B pays $25,000. Job A withholds based on a $30,000 annual income, and Job B withholds based on $25,000. But when you file your return, the IRS sees $55,000 in combined income, which pushes you into a higher bracket than either employer accounted for. The result is that you owe more tax than was collectively withheld.

When each employer withholds separately, the gap between what was taken out and what you actually owe can easily reach hundreds or even thousands of dollars by filing time.

Here is a straightforward example of how that bracket gap works:

| Income Source | Annual Pay | Bracket Each Employer Uses | Actual Combined Bracket |

|---|---|---|---|

| Job A | $30,000 | 12% | 22% |

| Job B | $25,000 | 12% | 22% |

| Combined total | $55,000 | Varies by employer | 22% |

How Social Security, Medicare, and deductions behave

Social Security and Medicare taxes, known collectively as FICA, operate differently from income tax. Each employer withholds 6.2% for Social Security up to the annual wage base ($176,100 for 2025) and 1.45% for Medicare on every dollar you earn. If your combined wages across all jobs exceed the Social Security wage base, you will have over-withheld on that tax, and you can claim that excess as a refundable credit when you file. Medicare has no cap, but if your total income tops $200,000 as a single filer, you owe an additional 0.9% surtax.

Your standard deduction and filing status do not multiply across employers either. You receive one set of deductions on a single return, regardless of how many W-2s you collect. That fixed deduction, spread across a larger combined income, is another reason your effective tax rate climbs as you take on more work.

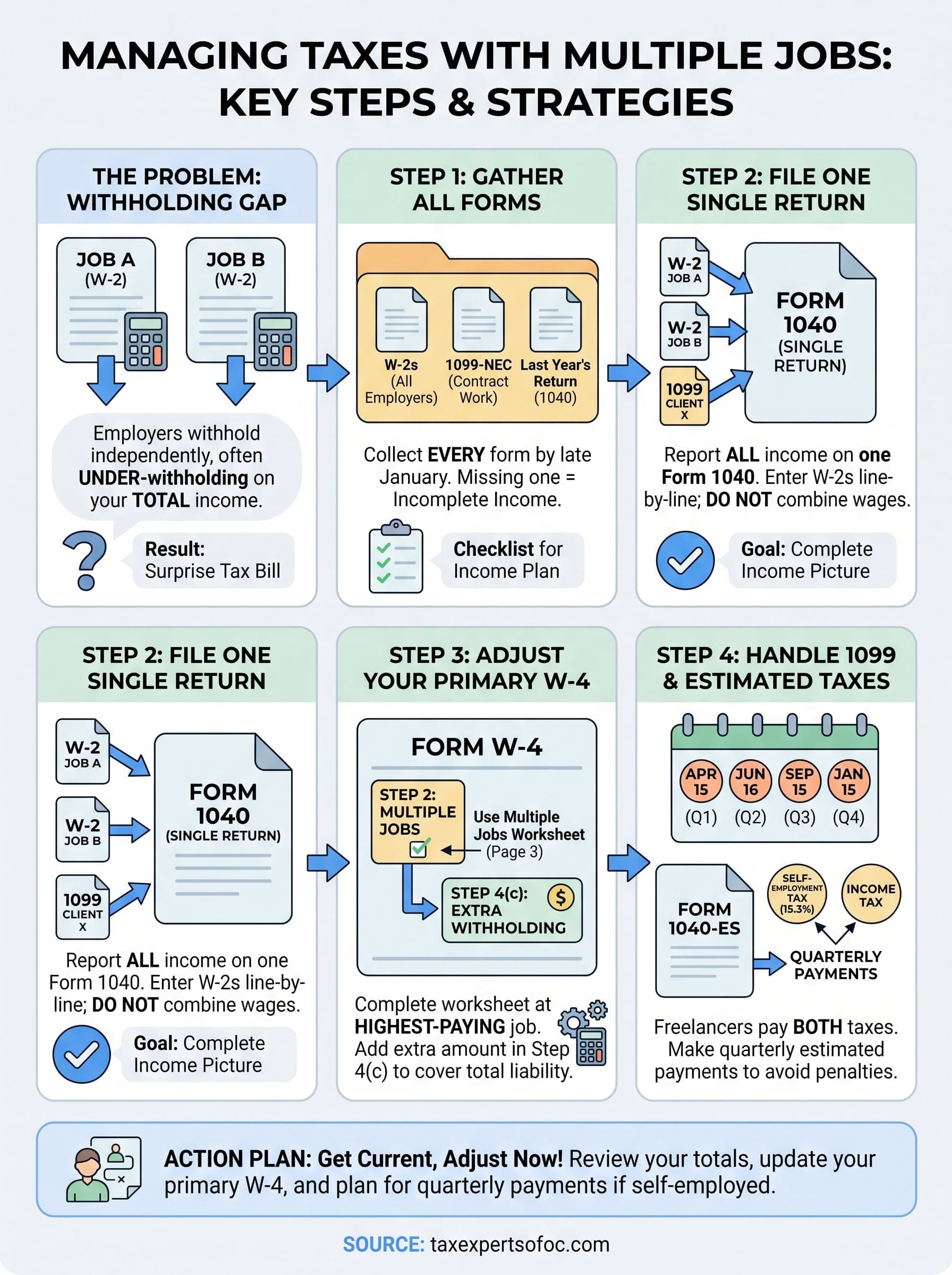

Step 1. Gather the right tax forms and numbers

Before you can file accurately, you need everything in one place. When taxes with multiple jobs are involved, you will receive a separate W-2 from each employer, and all of them must appear on your single federal return. Missing even one W-2 means you are reporting incomplete income, which can trigger an IRS notice or a penalty.

What documents to collect

You need every W-2 that arrives in your mail or email by late January. Each form shows your gross wages from that employer and the exact amount withheld for federal income tax, Social Security, and Medicare. If you also did any freelance or contract work, expect a 1099-NEC for each client that paid you $600 or more during the year.

Here is a checklist of what to have ready before you sit down to file:

- W-2 from every employer you worked for during the year

- 1099-NEC or 1099-MISC for any contract or freelance income

- Last year's tax return, which confirms your prior adjusted gross income for e-filing verification

- Social Security numbers for yourself, your spouse, and any dependents

- Bank routing and account numbers for direct deposit of any refund

If an employer does not send your W-2 by February 15, contact them directly, then call the IRS at 1-800-829-1040 if the form still does not arrive.

Numbers to track before you start filing

Pull the total gross income from each W-2 or 1099 and add them together. Use this simple table to keep your numbers organized:

| Form | Payer | Gross Income | Federal Tax Withheld |

|---|---|---|---|

| W-2 | Job A | $30,000 | $3,200 |

| W-2 | Job B | $25,000 | $2,100 |

| 1099-NEC | Client X | $5,000 | $0 |

| Total | $60,000 | $5,300 |

Knowing your combined withheld amount upfront tells you immediately whether you are likely to owe or receive a refund before you enter a single line on your return.

Step 2. File one return and report all income

No matter how many employers paid you, you file one federal return that includes every dollar you earned. The IRS matches your return against every W-2 and 1099 it receives from your employers and clients, so leaving one out will generate an automatic notice. When handling taxes with multiple jobs, the goal is a single, complete picture of your income on one Form 1040.

How to enter multiple W-2s on your return

Your tax software or preparer will prompt you to add each W-2 separately. Enter the numbers exactly as they appear on each form, line by line. Do not add the wages together and type in a combined figure, because the IRS cross-references each employer's EIN and reported amount individually.

Use this input template to stay organized as you enter each form:

| Field | Job A W-2 | Job B W-2 |

|---|---|---|

| Box 1: Wages | $30,000 | $25,000 |

| Box 2: Federal tax withheld | $3,200 | $2,100 |

| Box 4: Social Security withheld | $1,860 | $1,550 |

| Box 6: Medicare withheld | $435 | $363 |

Your software totals all boxes automatically once every W-2 is entered, giving you the combined income figure that determines your actual tax.

What happens if your totals show you owe

Once your software adds all income sources, it calculates your true tax liability against your combined withholdings. If the withheld total falls short, you will see a balance due. Pay that balance by April 15 to avoid interest and late-payment penalties, even if you file for an extension.

Step 3. Set your W-4 for multiple jobs

Correcting your W-4 is the most direct way to prevent a large tax bill at filing time. When you handle taxes with multiple jobs, the redesigned W-4 (in use since 2020) includes a Step 2 section built specifically for people with multiple employers that you need to complete at your highest-paying job only.

Use the IRS Multiple Jobs Worksheet

Step 2 on your W-4 gives you three ways to account for extra income. The most accurate option is to complete the Multiple Jobs Worksheet on page 3 of the official W-4 form. You fill it out once, calculate a dollar figure, and enter that amount in Step 4(c) as additional withholding on your primary job's W-4. Leave Steps 2 through 4 blank on every other W-4 you submit to your remaining employers.

Completing the worksheet at your highest-paying job and leaving other W-4s blank keeps the math from stacking up and over-correcting your withholding.

Here is how each Step 2 option compares so you can pick the right one for your situation:

| Option | Accuracy | Effort |

|---|---|---|

| Multiple Jobs Worksheet (page 3) | High | Moderate |

| IRS Tax Withholding Estimator | High | Low |

| Check the box in Step 2(c) | Moderate | Minimal |

Add Extra Withholding as a Flat Dollar Amount

If your income shifts frequently, you can skip the worksheet entirely and enter a flat dollar amount directly in Step 4(c) of your W-4. Estimate your total tax liability for the year, subtract your projected combined withholdings, then divide the difference by the number of pay periods you have left. Submit an updated W-4 to your employer any time your income changes meaningfully.

Step 4. Handle 1099 income and estimated taxes

If any of your income comes from freelance work or contract gigs, 1099 income plays by different rules than your W-2 wages. No employer withholds taxes on your behalf, which means you are responsible for covering both income tax and self-employment tax entirely out of pocket.

Calculate your self-employment tax first

Self-employment tax sits at 15.3% of your net 1099 earnings, covering both the employee and employer shares of Social Security and Medicare. On W-2 income, your employer covers half of this cost. On 1099 income, you cover all of it. The good news is you can deduct half of your self-employment tax as an adjustment to income on Form 1040, which reduces your taxable income slightly.

Here is how to estimate what you owe on $5,000 in net 1099 income:

| Calculation | Amount |

|---|---|

| Net 1099 earnings | $5,000 |

| Self-employment tax (15.3%) | $765 |

| Deductible half of SE tax | $382.50 |

| Net income after SE deduction | $4,617.50 |

Make quarterly estimated payments to stay current

When you handle taxes with multiple jobs and one of those jobs is contract work, the IRS expects you to pay taxes on that 1099 income throughout the year using Form 1040-ES. The four quarterly payment deadlines are:

| Quarter | Coverage Period | Due Date |

|---|---|---|

| Q1 | January through March | April 15 |

| Q2 | April through May | June 16 |

| Q3 | June through August | September 15 |

| Q4 | September through December | January 15 (next year) |

Missing quarterly deadlines triggers an underpayment penalty even if you pay everything owed by April 15.

To calculate each payment, estimate your total 1099 income for the year, apply your combined income and self-employment tax rate, subtract any W-2 withholdings already covering part of that liability, and divide the remaining balance by four.

Next steps

Managing taxes with multiple jobs comes down to three things: knowing your combined income, adjusting your W-4 at your primary employer, and keeping up with estimated payments if you have any 1099 work. If you run through the steps in this guide, you will go into April with far fewer surprises.

Start now by pulling together your W-2s and any 1099s from the current year. Enter your totals into the IRS Tax Withholding Estimator, then submit an updated W-4 to your highest-paying employer with the correct additional withholding amount in Step 4(c). If you have self-employment income, set your next quarterly estimated payment on the calendar before you forget.

If your income mix is complicated or you already have a balance due from a prior year, the team at Tax Experts of OC can review your full picture and help you get current. Book your free 30-minute consultation today.