If you're self-employed, every dollar you earn hits your bank account untouched by withholding, which feels great until tax season arrives. Between federal income tax and the 15.3% self-employment tax, the bill adds up fast. The good news? The tax code gives you real tools to fight back. Knowing which self employed tax deductions you qualify for is the single most effective way to keep more of what you earn.

The problem is that most self-employed people either miss deductions entirely or claim ones they shouldn't. Both mistakes cost money. Overlooked write-offs mean you're overpaying the IRS. Aggressive claims without proper documentation mean you're inviting an audit. The line between the two is where a lot of freelancers, contractors, and solo business owners get stuck, and where having qualified guidance makes a measurable difference.

At Tax Experts of OC, our CPAs and Enrolled Agents work with self-employed clients across all 50 states who deal with exactly this. We prepare returns, plan ahead for next year's liability, and step in when the IRS has questions. This article breaks down 16 deductions available in the 2026 tax year, explains who qualifies, and flags the details that trip people up. Whether you're a first-year freelancer or a seasoned independent contractor, this list will help you build a stronger, more accurate return.

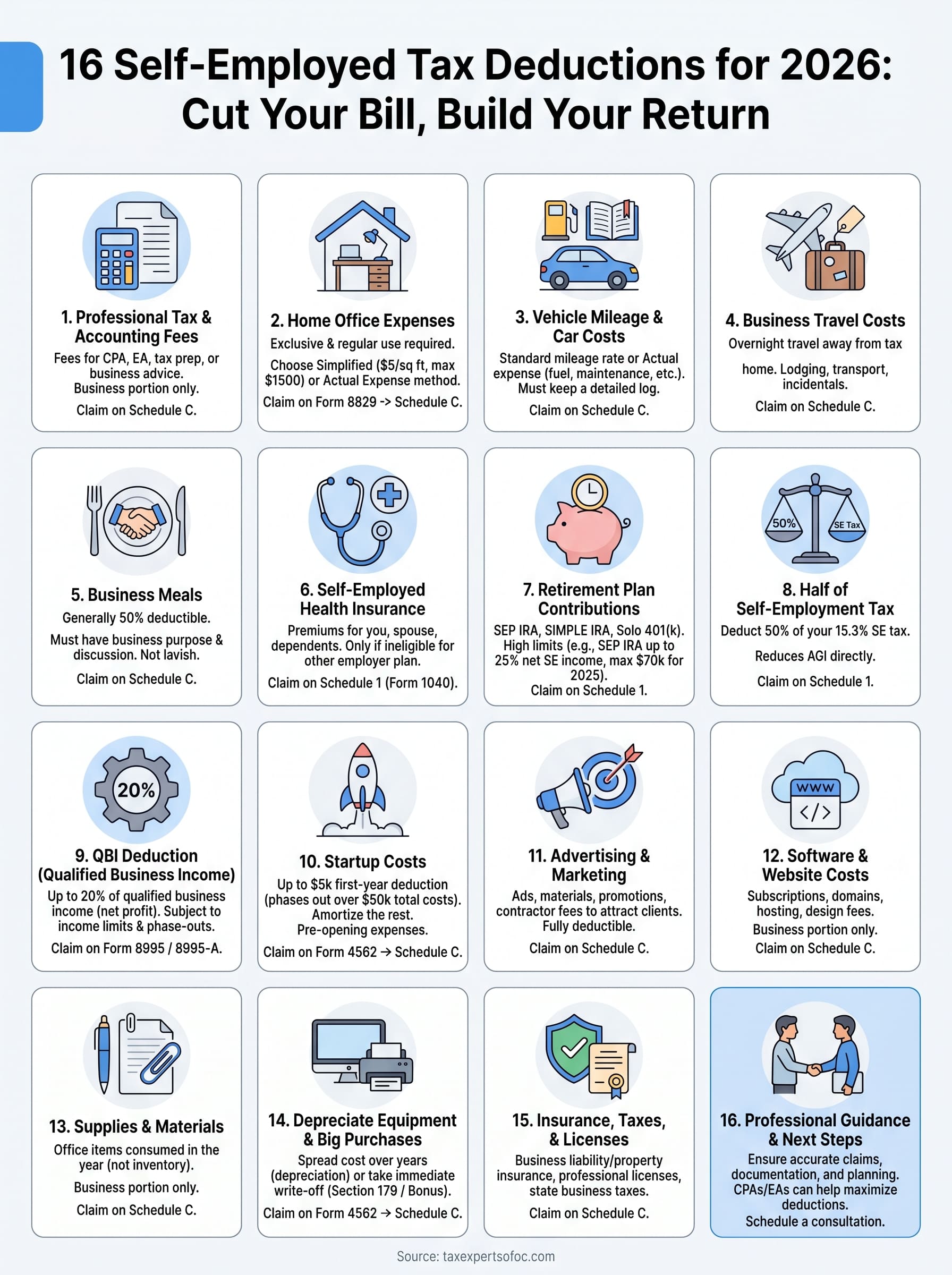

1. Deduct professional tax and accounting fees

The IRS allows you to deduct ordinary and necessary business expenses, and fees you pay to a CPA, Enrolled Agent, or tax attorney fall squarely in that category. If you hire a professional to prepare your business taxes, represent you before the IRS, or advise on tax strategy, those costs reduce your taxable income directly.

What counts as a deductible professional fee

Tax preparation fees tied directly to your business return are fully deductible. That includes fees for preparing Schedule C, filing payroll tax returns, handling a business audit, or getting advice on quarterly estimated payments. If you pay a bookkeeper to maintain your business records throughout the year, those bookkeeping and accounting fees qualify as well. Legal fees for business-related tax matters, such as negotiating an IRS installment agreement or defending a tax dispute, also count.

One important boundary: fees paid for the personal portion of your tax return do not qualify. If you pay one flat fee for a combined personal and business return, you need to allocate the cost between the two portions and only deduct the business share.

Key rules and common mistakes

The deduction applies in the year you pay the fee, not the year the service covers. So if you pay your accountant in January 2026 for your 2025 return preparation, you claim that expense on your 2026 taxes. That timing trips up a lot of self-employed filers who assume the deduction belongs to the year the work relates to.

Do not deduct fees tied to personal financial planning, estate planning, or investment advice, even if your accountant bundles all of it into one meeting or invoice.

A common mistake is claiming 100% of a bundled invoice when it includes personal services. Ask your tax professional to itemize their work so you have clear documentation that supports the business allocation. Vague invoices become a real problem if the IRS ever questions your return, so getting a detailed billing statement upfront is worth the extra ask.

Where to claim it and what records to keep

You report these fees on Schedule C, Line 17 under "Legal and professional services." Keep every invoice, receipt, and bank or credit card statement confirming payment. If the fee covers both business and personal work, keep a written breakdown from your provider that explains the split.

These costs rank among the most straightforward self employed tax deductions available, and skipping them means paying the IRS more than you owe.

2. Deduct home office expenses

Working from home has a real tax benefit when you set it up correctly. The home office deduction lets self-employed individuals write off costs tied to the part of their home used exclusively for business, and it can produce a meaningful reduction in taxable income.

Check the regular and exclusive use rules

The IRS requires your home office to meet two conditions before it qualifies: regular use and exclusive use. Regular means you use the space consistently for business, not just occasionally. Exclusive means that space serves only business purposes. A dedicated room used only for client calls, project work, and business storage qualifies. A desk in a shared living space or a guest bedroom that doubles as an office does not.

If your workspace fails the exclusive use test, the entire deduction is disallowed, so confirm this before you claim anything.

Choose the simplified method or actual expense method

Two calculation methods are available, and you pick the one that works better for your situation:

- Simplified method: $5 per square foot, up to 300 square feet, for a maximum of $1,500. Less recordkeeping, quicker math.

- Actual expense method: Deduct the real costs of your home, including rent or mortgage interest, utilities, and insurance, multiplied by the percentage of your home the office occupies. More paperwork, but typically a larger deduction.

Where to claim it and what records to keep

Report the home office deduction on Form 8829, then carry that figure to Schedule C. Keep photos of the dedicated workspace, floor plan measurements confirming the square footage, and receipts for all related home expenses. Strong documentation is what protects these self employed tax deductions if the IRS reviews your return.

3. Deduct vehicle mileage and car costs

If you drive for business, the IRS lets you deduct those costs using one of two methods. Tracking your use accurately and choosing the right calculation method is how you convert real vehicle expenses into a legitimate tax write-off.

Pick standard mileage or actual expenses

Your choice of method determines how you calculate the deduction. The standard mileage rate lets you multiply a set per-mile rate by your total business miles driven for the year, with minimal recordkeeping required. The actual expense method covers real operating costs like fuel, insurance, maintenance, and depreciation, proportional to your business-use percentage. Run both calculations before you file to confirm which one produces the larger deduction.

You must elect the standard mileage rate in the first year you place the vehicle in service for business, or you lose the option to use it for that vehicle going forward.

Know what qualifies as business driving

Client visits, job site travel, and supply runs all count as business driving. Commuting between your home and a fixed regular workplace does not, even if you work from home part of the time. Every qualifying trip needs a recorded date, destination, and business purpose to hold up if the IRS reviews your return.

Common qualifying trips include:

- Driving to meet clients or attend business appointments

- Travel between two or more business locations in a single day

- Trips to purchase supplies or equipment for your business

- Driving to a bank, post office, or government office on business matters

Where to claim it and what records to keep

Report vehicle costs on Schedule C, Part II, Line 9, then complete Part IV of that same form, which asks about total miles and personal versus business use. Keep a mileage log that records the date, destination, miles driven, and business purpose for every trip. These self employed tax deductions depend on that log, so update it on the day of each drive rather than guessing at year-end.

Supporting records to maintain:

- Mileage log updated the day of each business drive

- Total annual odometer readings for the vehicle

- Receipts for fuel, insurance, maintenance, and repairs if you use the actual expense method

4. Deduct business travel costs

Business travel deductions cover more ground than most self-employed people realize. When your work takes you away from your tax home overnight, the IRS lets you write off a broad range of travel-related costs, and those expenses can add up to a meaningful reduction in your taxable income.

What qualifies as business travel away from home

Your tax home is the city or general area where your primary place of business is located, not necessarily where you live. To qualify as deductible travel, the trip must take you far enough away that you need sleep or rest before you can return to your regular work duties. Day trips within your local area do not meet this test. The travel must also be ordinary, necessary, and directly tied to your business operations.

If a trip mixes personal and business activity, only the costs directly tied to the business portion of your travel are deductible.

Deduct transportation, lodging, and incidentals the right way

Airfare, train tickets, rental cars, and taxis to your business destination are fully deductible. Your hotel and lodging costs are deductible for each night the business purpose requires you to stay away from home. Incidental expenses such as Wi-Fi fees, tips for service workers, and dry cleaning during the trip qualify as well. The IRS disallows lavish or extravagant lodging, so keep accommodations reasonable relative to the nature of your work.

Where to claim it and what records to keep

Report business travel costs on Schedule C, Part II, Line 24a. These self employed tax deductions require solid documentation, so keep receipts, booking confirmations, and a written record of the business purpose behind each trip. A brief note with the destination, dates, and reason for travel is enough to support your claim if the IRS asks.

5. Deduct business meals

Meals with clients, prospects, and business partners are deductible, but the IRS applies specific limits and conditions that you need to follow. Getting this deduction right means understanding the 50% cap, knowing what documentation protects your claim, and recognizing the narrow exceptions where you can deduct the full cost.

Apply the 50% rule and identify exceptions

The standard rule allows you to deduct 50% of the meal cost, whether you're eating with a client or buying your own meal during a qualifying business trip. That cap applies to both the food and any related taxes and tips. A small number of situations allow a full 100% deduction, including meals provided at company events open to all employees or meals that qualify as a taxable fringe benefit to the recipient.

Do not try to claim 100% on ordinary client meals. The IRS is clear that the 50% limit applies in almost every business dining situation.

Meet the requirements for a valid business meal

The meal must have a clear and genuine business purpose. You, or one of your employees, must be present, and the meal cannot be lavish or extravagant relative to the circumstances. A business discussion must take place before or after the meal, whether that is a client negotiation, a project review, or a sales conversation. Social meals without a documented business purpose do not qualify.

Where to claim it and what records to keep

Report these self employed tax deductions on Schedule C, Part II, Line 24b. Keep your receipts, and for each meal write down the date, the people who attended, and the business topic discussed. Those four details are exactly what the IRS expects to see when it reviews meal deductions.

6. Deduct self-employed health insurance

Health insurance is one of the most expensive recurring costs you face as a self-employed individual, and the IRS gives you a direct way to recover part of that cost. Unlike most self employed tax deductions, this one is claimed on your personal return rather than Schedule C, which means it reduces your adjusted gross income before you even calculate your tax liability.

Confirm you qualify based on coverage eligibility

You qualify for this deduction only if you were not eligible to participate in an employer-sponsored health plan through a spouse or a separate employer during the months you're claiming. If you had access to subsidized coverage through another job, even if you declined it, the IRS considers you ineligible for that period.

This eligibility rule applies month by month, so if you gained access to employer coverage partway through the year, you can only deduct premiums from the months you had no other option.

Include medical, dental, and eligible long-term care premiums

You can deduct premiums for medical and dental insurance covering yourself, your spouse, your dependents, and children under age 27 at the end of the tax year. Qualifying long-term care insurance premiums are deductible up to age-based IRS limits that adjust annually. The deduction cannot exceed your net self-employment income for the year.

Where to claim it and what records to keep

Report this deduction on Schedule 1, Line 17 of Form 1040, not on Schedule C. Keep monthly premium statements and proof of payment from your insurer. If your plan covers both business and personal members of your household, document the full premium clearly so the deduction reflects the correct total.

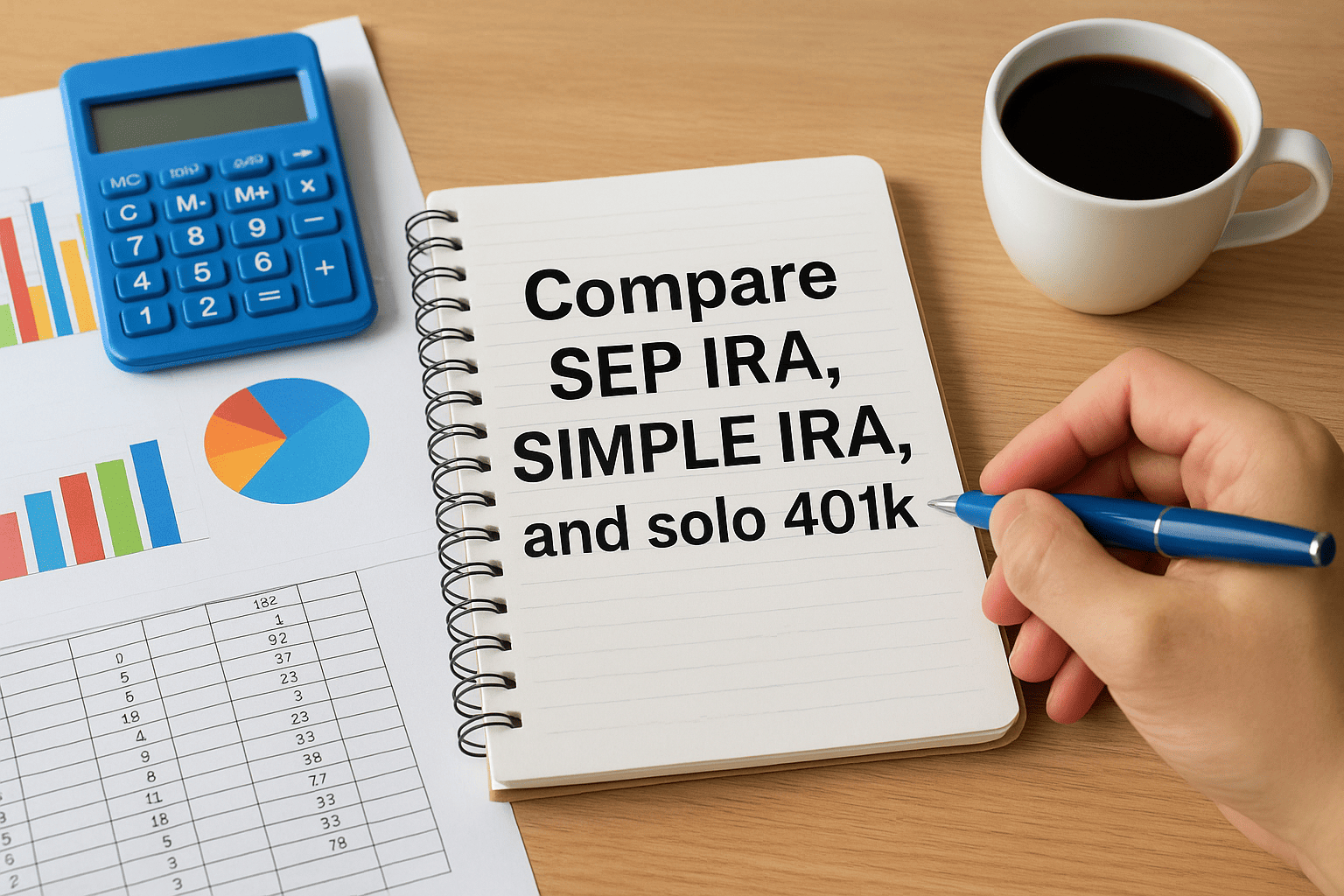

7. Deduct retirement plan contributions

Setting aside money for retirement does two things at once: it builds your financial future and cuts your current tax bill. Self-employed retirement plan contributions are fully deductible, and the IRS offers several qualified plan types that let you shelter a substantial portion of your income before taxes touch it.

Compare SEP IRA, SIMPLE IRA, and solo 401k

Each plan structure works differently, and the right choice depends on your income level and how much administrative complexity you're willing to manage. Here is a quick comparison:

| Plan | 2025 Contribution Limit | Best For |

|---|---|---|

| SEP IRA | Up to 25% of net self-employment income, max $70,000 | High earners who want simplicity |

| SIMPLE IRA | Up to $16,500 ($20,000 if age 50+) | Lower-income self-employed with employees |

| Solo 401(k) | Up to $70,000 combined employee and employer contributions | High earners who want maximum flexibility |

Understand contribution limits and timing

Contribution limits adjust annually, so confirm the current figures directly from the IRS before you finalize your return. For a SEP IRA, you calculate the maximum based on 25% of net self-employment earnings after subtracting half of your self-employment tax. You can make SEP IRA contributions up to your filing deadline, including extensions, which gives you extra runway to maximize the deduction.

A solo 401(k) requires you to establish the plan by December 31 of the tax year, even though you can fund it after that date.

Where to claim it and what records to keep

Report these self employed tax deductions on Schedule 1, Line 16 of Form 1040. Keep annual contribution statements and account records that confirm each deposit amount and the date it was made.

8. Deduct half of self-employment tax

When you work for an employer, payroll taxes get split down the middle: your employer pays half and you pay the other half. As a self-employed person, you cover both sides of that split, which means your self-employment tax runs 15.3% of net earnings up to the Social Security wage base, plus 2.9% on everything above it. The IRS acknowledges this burden by letting you deduct half of what you pay, which directly reduces your adjusted gross income before your income tax is even calculated.

Understand what self-employment tax covers

Self-employment tax funds Social Security and Medicare, the same programs that standard payroll taxes support for traditionally employed workers. You calculate it on Schedule SE based on your net self-employment earnings, which is your gross business income minus your deductible business expenses. The 15.3% rate applies to net earnings up to $176,100 for the 2025 tax year, and the 2.9% Medicare portion continues above that threshold with no upper cap.

If your net self-employment earnings exceed $200,000 as a single filer, an additional 0.9% Additional Medicare Tax applies on the amount above that threshold.

Calculate the employer-equivalent deduction

The deduction equals exactly 50% of your total self-employment tax liability for the year. Once Schedule SE produces your full tax figure, you divide it in half and carry that number directly to Form 1040. This is one of the few self employed tax deductions that the IRS calculates mechanically, so no estimation or judgment is involved.

Where to claim it and what records to keep

Report this deduction on Schedule 1, Line 15 of Form 1040. Your completed Schedule SE is the primary supporting document, so retain it with your filed return. No additional receipts are necessary because the deduction flows directly from your calculated tax liability.

9. Claim the QBI deduction

The Qualified Business Income (QBI) deduction lets eligible self-employed individuals deduct up to 20% of their qualified business income directly from their taxable income. Introduced under the Tax Cuts and Jobs Act, it remains one of the most valuable self employed tax deductions available because it reduces your tax liability without requiring you to spend any money to earn it.

Identify what counts as qualified business income

Qualified business income is the net amount of income, gain, deduction, and loss from your domestic trade or business. In practical terms, it is your Schedule C net profit after subtracting your allowable business expenses. Capital gains, dividends, interest income, and reasonable compensation you pay yourself do not count toward QBI and must be excluded from your calculation.

Watch for income limits and service business rules

Your total taxable income determines whether you receive the full 20% deduction or a reduced one. For the 2025 tax year, the phase-out range begins at $197,300 for single filers and $394,600 for joint filers. Once you exceed those thresholds, the rules become significantly more restrictive, especially for specified service trades or businesses, which the IRS defines as fields like law, consulting, healthcare, and financial services.

If your business falls into the specified service category and your income exceeds the full phase-out range, the QBI deduction is eliminated entirely, so confirm your business classification before assuming you qualify.

Where to claim it and what records to keep

Report the QBI deduction on Form 8995 if your situation is straightforward, or Form 8995-A if your income triggers the phase-out rules. Keep your Schedule C and all supporting business income records that document the qualified income figure you report.

10. Write off startup costs

Starting a business costs money before it ever generates income. The IRS recognizes this and allows you to recover qualifying startup expenses through a combination of an immediate first-year deduction and multi-year amortization. Understanding how these rules work puts one of the more overlooked self employed tax deductions to work for new business owners.

Separate startup costs from ongoing expenses

Startup costs are expenses you paid or incurred before your business opened and that you would otherwise deduct as regular business expenses once operations begin. Common examples include market research, legal fees for setting up your business structure, and costs to recruit and train employees before launch. Once your business is active, those same types of costs shift to ordinary operating expenses and get deducted in the year they occur instead.

Do not mix pre-opening costs with ongoing expenses on your return, because the IRS treats them under different rules and combining them creates a documentation problem that can follow you into an audit.

Apply the first-year deduction and amortization rules

The IRS lets you deduct up to $5,000 in startup costs in the first year your business is active, provided your total startup costs do not exceed $50,000. Any remaining balance gets amortized over 180 months starting from the month your business begins operations. If your total startup costs run above $50,000, the $5,000 first-year deduction phases out dollar for dollar above that threshold until it disappears entirely at $55,000.

Where to claim it and what records to keep

Report startup cost amortization on Form 4562, then carry the result to Schedule C. Keep dated receipts and invoices for every pre-opening expense, along with a clear written record of the date your business officially began operations.

11. Deduct advertising and marketing

Money you spend to attract clients, promote your services, and build your brand is fully deductible as an ordinary business expense. The IRS allows you to write off a wide range of advertising and marketing costs, and for most self-employed individuals, these expenses appear throughout the year in several different forms.

Deduct common marketing costs that drive sales

Most paid promotional activities tied directly to your business qualify for a full deduction. The category is broad, which means you have room to capture a meaningful amount of spending that often goes untracked. Common qualifying expenses include:

- Online ads placed through platforms like Google

- Printed materials such as business cards, brochures, and mailers

- Email marketing platform fees

- Fees paid to designers, copywriters, or freelance marketing contractors

- Sponsored content and brand partnerships tied to your business

Avoid personal and nondeductible promotion expenses

Not every cost with a promotional angle clears the bar. Political contributions and lobbying expenses are explicitly nondeductible, regardless of any business benefit you might argue. Sponsoring a community event can qualify if your business name and contact information appear in a documented, public-facing way, but a goodwill donation with no promotional return does not meet the IRS standard.

If you're unsure whether a specific cost qualifies, write down the business purpose at the time of the expense rather than trying to reconstruct it later.

Where to claim it and what records to keep

Report these self employed tax deductions on Schedule C, Part II, Line 8. For each expense, retain a note confirming the business purpose and intended audience so you can support the claim if the IRS reviews your return. Useful records to keep include:

- Invoices and receipts from vendors and contractors

- Screenshots or billing statements from ad platforms

- Copies of printed materials or campaign assets tied to specific expenses

12. Deduct software and website costs

Digital tools are a core operating expense for most self-employed workers, and nearly every business-related software or website cost qualifies as a deductible ordinary and necessary expense. The IRS treats these the same way it treats any other business tool you pay to use, which means you can write them off fully in the year you pay for them as long as the primary purpose is your work.

Deduct subscriptions, apps, and online tools

Monthly and annual subscriptions to business software are deductible in the year the payment clears. That covers accounting platforms, project management tools, cloud storage services, video conferencing software, scheduling apps, and any other application you use primarily to run your business. If you use a tool for both personal and business purposes, you can only deduct the percentage that reflects actual business use, so track your usage if the split is not obvious.

Do not deduct a subscription just because you occasionally use it for work if the primary purpose is personal; the IRS expects the business use to be genuine and documented.

Deduct domain, hosting, and website services

Domain registration fees and web hosting charges are fully deductible as ordinary business expenses. If you pay a developer or designer to build or update your site, those contractor fees qualify as well, and you report them the same way. SSL certificates, e-commerce plugins, and content delivery services all count if they serve a direct business function. Keep billing statements from every provider as documentation for these self employed tax deductions. Report all software and website costs on Schedule C, Part II, Line 22 for supplies or Line 27a for other expenses, depending on how your return is structured.

13. Deduct supplies and materials

Day-to-day supplies are a legitimate business expense, and the IRS lets you deduct them in the year you pay for them as long as you use or consume them within that same tax year. For most self-employed workers, office supplies and materials add up to a consistent and deductible cost across every month of the year.

Separate office supplies from inventory and cost of goods sold

Office supplies are items you use to operate your business, such as printer paper, pens, and postage. These differ from inventory, which consists of goods you purchase to resell, and from raw materials that go into products you manufacture. Inventory and cost of goods sold follow separate accounting rules on Schedule C, so mixing those costs with your regular supply purchases creates a documentation problem you will need to untangle later.

If your business both sells products and uses internal supplies, keep those purchasing records completely separate from day one.

Handle mixed personal and business use correctly

When you buy supplies for both personal and business purposes, you can only deduct the portion tied to business activity. Purchasing business supplies separately from personal shopping is the simplest way to avoid splitting invoices and keeps your records clean throughout the year.

Tracking your business use percentage at the time of each purchase is far easier than estimating it later. A brief note on each receipt confirming what the items were used for gives you a solid paper trail without requiring complicated accounting.

Where to claim it and what records to keep

Report these self employed tax deductions on Schedule C, Part II, Line 22. Keep every receipt tied to a supply purchase, and note the business purpose for each one at the time of purchase rather than reconstructing it months later.

Records to maintain:

- Receipts for every supply purchase, physical or digital

- A note confirming the business purpose for each item

- Bank or credit card statements that confirm payment dates

14. Depreciate equipment and big purchases

When you buy a major asset like a computer, specialized tools, or a piece of machinery for your business, the cost recovery rules matter. The IRS may require you to spread the deduction across several years, or it may let you take the entire write-off in year one. Knowing which path applies to each purchase helps you manage your tax liability more deliberately.

Decide between expensing and depreciation

Standard depreciation spreads the cost of an asset across its IRS-defined useful life. A computer falls into a five-year asset class, while office furniture falls into a seven-year class. Expensing lets you deduct the full purchase price in the year you place the asset in service, which produces a larger immediate deduction but removes future-year write-offs entirely.

Common asset classes and recovery periods:

- Computers and equipment: 5 years

- Office furniture and fixtures: 7 years

- Qualified improvement property: 15 years

Use Section 179 and bonus depreciation when they fit

Section 179 lets you deduct the full cost of qualifying business property in the year you buy it, up to the IRS annual limit. Bonus depreciation allows an additional percentage-based write-off on qualifying new and used assets placed in service during the year. Both are among the most powerful self employed tax deductions available to business owners making significant equipment purchases.

Section 179 cannot create a business loss, so if your deduction would push net income below zero, bonus depreciation may be the better option.

Qualifying property for both provisions includes:

- Machinery and equipment

- Business vehicles over 6,000 lbs GVWR

- Off-the-shelf software

Where to claim it and what records to keep

Report both Section 179 and standard depreciation on Form 4562, then carry those numbers to Schedule C. Keep purchase receipts and documentation confirming the exact date you placed each asset in service for business use.

15. Deduct insurance, taxes, and licenses

Several recurring business costs that protect your operations and keep you legally compliant qualify as fully deductible ordinary and necessary expenses. Insurance premiums, professional licenses, and certain taxes you pay throughout the year all fall into this category, and tracking them consistently is one of the simpler self employed tax deductions you can capture without complicated calculations.

Deduct business insurance premiums that protect your work

Business insurance premiums tied directly to your work are deductible in the year you pay them. That includes general liability insurance, professional liability or errors and omissions coverage, commercial property insurance, and business interruption policies. If you pay a single premium that covers both personal and business property, you must allocate the cost and deduct only the business portion.

Do not confuse business insurance with self-employed health insurance, which follows a separate deduction path on Schedule 1 rather than Schedule C.

Deduct licenses, permits, and business-related taxes

Professional licenses and permits required to legally operate your business are fully deductible. That covers state contractor licenses, occupational permits, and any certification fees your industry requires. State and local business taxes, including annual franchise taxes and business property taxes assessed on equipment you use in your work, also qualify. Federal income taxes and self-employment tax are not deductible in this category.

Where to claim it and what records to keep

Report insurance premiums on Schedule C, Part II, Line 15 and licenses on Line 23. For business taxes, use Line 23 as well. Keep premium invoices, renewal notices, and payment confirmations for every policy. For licenses, retain the original permit documentation and any renewal receipts that confirm the business purpose and payment date.

Next steps

These 16 self employed tax deductions cover the categories that reduce most self-employed filers' tax bills by the largest amounts. The challenge is not just knowing the list but applying each deduction correctly, documenting it properly, and catching the interactions between them before you file. A missed allocation or an undocumented expense can cost you more than the time it would have taken to get it right.

If your return involves multiple deductions, a mix of business and personal expenses, or an IRS notice you haven't addressed, working with a qualified professional removes the guesswork. At Tax Experts of OC, our CPAs and Enrolled Agents prepare self-employed returns, plan ahead to reduce next year's liability, and represent clients when the IRS has questions. Schedule a free 30-minute consultation with our team and find out exactly where your return stands. Talk to a self-employment tax expert today.