Hiring someone new, or taking on work yourself, raises an immediate question: what are the tax implications? The distinction between employee vs independent contractor taxes affects everything from how income is reported to who pays what share of Social Security and Medicare. Get the classification wrong, and you could face IRS penalties, back taxes, and interest that add up fast.

For workers, the classification determines whether taxes are withheld from each paycheck or paid out of pocket every quarter. For businesses, it shapes payroll obligations, filing requirements, and potential legal exposure. Neither side can afford to guess, the IRS scrutinizes worker classification closely, and misclassification audits have been a consistent enforcement priority.

At Tax Experts of OC, our CPAs and Enrolled Agents help both individuals and business owners across all 50 states navigate these exact issues, whether that means correcting a past misclassification, responding to an IRS notice, or structuring new working relationships the right way from the start. This guide breaks down the key tax differences between employees and independent contractors, explains how the IRS makes its determination, and outlines what you need to do to stay compliant on either side of the equation.

Why worker classification matters for taxes

Worker classification is the starting point for almost every tax obligation in a working relationship. Whether you are an employer, a worker, or both, the label attached to that relationship determines who withholds taxes, who files which forms, and who is responsible when something goes wrong. The difference between employee vs independent contractor taxes is not a technicality; it is the foundation that shapes your entire tax picture for a given year.

The financial stakes for employers

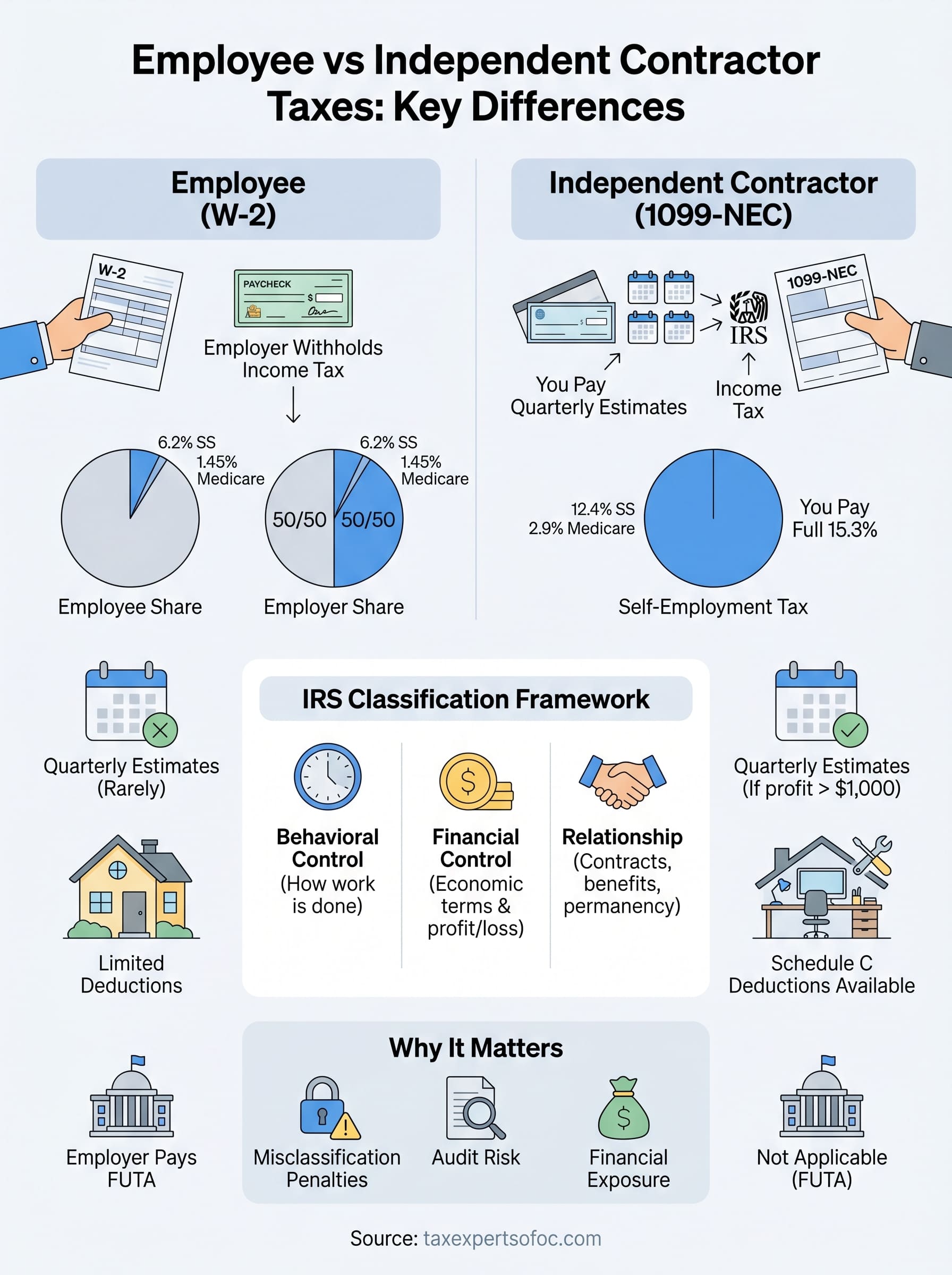

When you bring someone on as an employee, your obligations go well beyond writing a paycheck. You must withhold federal and state income taxes, withhold and match Social Security and Medicare taxes (FICA), pay federal unemployment tax (FUTA), and file quarterly payroll reports. That payroll tax match alone adds 7.65% to the cost of every dollar you pay in wages, and you are responsible for issuing W-2 forms by January 31 each year.

Misclassifying an employee as a contractor does not remove these obligations. It delays them until the IRS or a state agency discovers the error, and by then penalties and interest have already started building.

Independent contractor payments work differently. You skip payroll taxes on those payments, file a Form 1099-NEC for any contractor you pay $600 or more in a calendar year, and your obligation largely ends there. The contractor takes responsibility for their own taxes from that point.

The financial stakes for workers

If you are classified as an employee, your employer withholds income tax from every paycheck and covers half of your FICA obligation. You receive a W-2 that makes filing straightforward, and your tax burden is distributed across the year in manageable amounts rather than arriving as a surprise in April.

As an independent contractor, the full weight of self-employment tax lands on you. That means paying 15.3% on your net self-employment income to cover both the employee and employer share of Social Security and Medicare, plus making estimated quarterly tax payments to avoid underpayment penalties. You also need to track every deductible business expense yourself, because no employer is doing that on your behalf.

Why the IRS scrutinizes classification closely

The IRS loses substantial tax revenue when workers are misclassified, whether the mistake is intentional or not. Employers avoid payroll taxes, and workers who receive 1099s rather than W-2s are more likely to underreport income without proper guidance. This revenue gap is why the IRS dedicates enforcement resources to auditing worker classification and has published detailed guidance to help businesses make the correct call.

Both sides carry real financial exposure when the classification does not match the actual working relationship. Correcting a misclassification after the fact almost always costs more than addressing it correctly from the start, which is why understanding these rules before you sign a contract or submit a filing matters.

Employee taxes and employer responsibilities

When you hire someone as an employee, the tax obligations start on their first day. Understanding employee vs independent contractor taxes from the employer side means knowing exactly which taxes you collect, which you pay yourself, and when each filing is due. Missing any of these steps can trigger IRS penalties that compound quickly over time.

What gets withheld from employee paychecks

You are required to withhold federal income tax from every paycheck based on the employee's Form W-4 elections. Beyond income tax, you also withhold the employee's share of Social Security (6.2%) and Medicare (1.45%), which together make up their half of the FICA obligation. State income tax withholding applies in most states as well, depending on where your employee works.

Getting W-4 information from every new hire before their first paycheck is not optional; without it, you are required to withhold at the highest single rate, which creates problems for the employee at filing time.

At year-end, you issue a W-2 form that reports all wages paid and taxes withheld. This form must reach employees by January 31, and copies go to the Social Security Administration on the same deadline.

What employers owe on top of wages

Your obligations do not stop at withholding. You must also match the employee's FICA contribution, meaning you pay an additional 6.2% for Social Security and 1.45% for Medicare out of your own pocket for every dollar of wages. On top of that, you pay federal unemployment tax (FUTA) at 6% on the first $7,000 of each employee's wages, though credits for state unemployment payments reduce this in most cases.

Filing requirements add another layer. You submit Form 941 quarterly to report payroll taxes withheld and deposited throughout the quarter. If your total payroll tax liability exceeds $2,500 per quarter, you follow a monthly or semi-weekly deposit schedule rather than paying at filing time, and the specific schedule depends on your lookback period.

Independent contractor taxes and self-employment rules

As an independent contractor, you take on the tax responsibilities that an employer would normally handle. Understanding employee vs independent contractor taxes from the contractor side means knowing what you owe, when you owe it, and how to reduce your liability legally. There is no employer withholding your taxes automatically, so the entire compliance burden falls on you.

Self-employment tax: what you owe

Independent contractors pay self-employment (SE) tax at 15.3% on their net earnings. This rate covers both the employee and employer share of Social Security (12.4%) and Medicare (2.9%). You calculate this on Schedule SE, which you attach to your Form 1040 each year. One partial offset is available: you can deduct half of your SE tax as an adjustment to income on your federal return, which slightly lowers your adjusted gross income.

Missing this deduction is a common and costly mistake, so confirm you are claiming it every year you have self-employment income.

Estimated quarterly payments and deductions

Because no employer withholds taxes from your payments, you are responsible for making estimated quarterly tax payments to the IRS using Form 1040-ES. Payments are due four times a year, typically in April, June, September, and January. If your total tax liability for the year exceeds $1,000 after credits and withholding, skipping these payments triggers an underpayment penalty on top of whatever you already owe.

Your deductible business expenses are one of the most powerful tools available to you. Legitimate deductions reduce the net income on which both SE tax and income tax are calculated. Common examples include home office costs, equipment, software subscriptions, vehicle use for business, and professional development. Tracking these throughout the year rather than reconstructing them in April keeps your records clean and your liability accurate. Good recordkeeping is not just helpful at tax time; it is your first line of defense if the IRS ever questions a return.

How the IRS decides employee vs contractor status

The IRS does not rely on job titles or what a written contract says when making a classification decision. What matters is the actual working relationship, and the IRS evaluates it through a three-category framework. Getting this wrong is one of the most direct routes to an audit involving employee vs independent contractor taxes, so understanding how each category works protects you before a problem starts.

Behavioral control

Behavioral control focuses on whether you have the right to direct how work gets done, not just the final result. If you set the worker's hours, require specific methods, or provide training on how to complete tasks, those factors signal an employment relationship to the IRS.

Contractors control their own work methods and schedule even when you define what you need by a set deadline. The more control you exercise over the process rather than the outcome, the stronger the IRS's case for treating that worker as your employee.

Financial control

This category examines who controls the economic terms of the working relationship. Employees receive a regular wage or salary, while contractors typically negotiate a flat fee or project-based rate tied to specific deliverables.

If a worker can profit or incur a loss on individual jobs, supplies their own equipment, and markets their services to multiple clients at once, those facts support contractor status. Workers whose income depends entirely on your decisions, rather than their own business choices, look much more like employees under this test.

Type of relationship

The IRS weighs written contracts, whether you offer benefits such as health insurance or paid leave, and how open-ended the arrangement is. A worker engaged on a continuous basis with no defined end date signals a permanent employment relationship regardless of what the paperwork says.

Labeling someone a contractor in a contract does not override how the relationship actually functions in practice.

A clear project scope with a defined completion point supports contractor status more than an ongoing arrangement with no finish line. If you need a formal ruling before filing or restructuring a working relationship, Form SS-8 lets you request an official IRS determination in writing.

Common tax questions and side-by-side examples

Two forms of work often overlap in the same tax year, and the treatment changes significantly depending on which label applies. The comparison below puts the core employee vs independent contractor taxes differences side by side so you can see exactly where your obligations land and what forms you should expect.

What happens when you receive both a W-2 and a 1099?

Many people hold a salaried job and take on freelance work simultaneously, and both income streams show up on the same return. Your W-2 income already has federal income tax and FICA withheld, so that portion of your tax bill is largely managed for you throughout the year. Your 1099 income works differently: you owe self-employment tax at 15.3% plus ordinary income tax calculated at whatever rate your combined earnings produce.

If your freelance net profit exceeds $1,000 for the year, you need to make estimated quarterly payments to avoid an underpayment penalty at filing time, even if your W-2 withholding looks sufficient on its own.

You can still claim deductible business expenses on Schedule C against your 1099 income while also receiving a W-2, which reduces the net amount subject to self-employment tax. Keeping those two income streams organized separately throughout the year makes the calculation cleaner and reduces errors on your return.

Side-by-side tax comparison

The distinctions between the two classifications affect nearly every line of your tax picture, from the forms you receive to who cuts the check for payroll taxes.

| Tax factor | Employee | Independent Contractor |

|---|---|---|

| Form received | W-2 | 1099-NEC |

| Income tax withholding | Employer withholds | You pay via quarterly estimates |

| Social Security and Medicare | Split 50/50 with employer | You pay the full 15.3% |

| Quarterly estimates required | Rarely | Yes, if net profit exceeds $1,000 |

| Business expense deductions | Very limited | Schedule C deductions available |

| Unemployment tax (FUTA) | Employer pays | Not applicable |

Reviewing this table against your actual working arrangement each year helps you catch classification gaps before they trigger IRS scrutiny. If any row looks misaligned with how your work actually functions, that discrepancy is worth addressing with a qualified tax professional before you file.

Key takeaways

The distinction between employee vs independent contractor taxes shapes your entire tax picture, from who withholds your income tax to who covers the employer share of Social Security and Medicare. Misclassification carries real penalties for both businesses and workers, so getting the label right from the start saves you money and avoids IRS enforcement down the road.

Your classification determines which forms you receive, what deductions you can claim, and whether you owe quarterly estimated payments throughout the year. Contractors carry the full 15.3% self-employment tax burden and manage their own compliance, while employees split FICA with their employer and have taxes withheld automatically from every paycheck.

If you need help resolving a past misclassification, responding to an IRS notice, or structuring a new working relationship correctly, Tax Experts of OC offers a free 30-minute consultation with a CPA or Enrolled Agent who can walk you through every step.