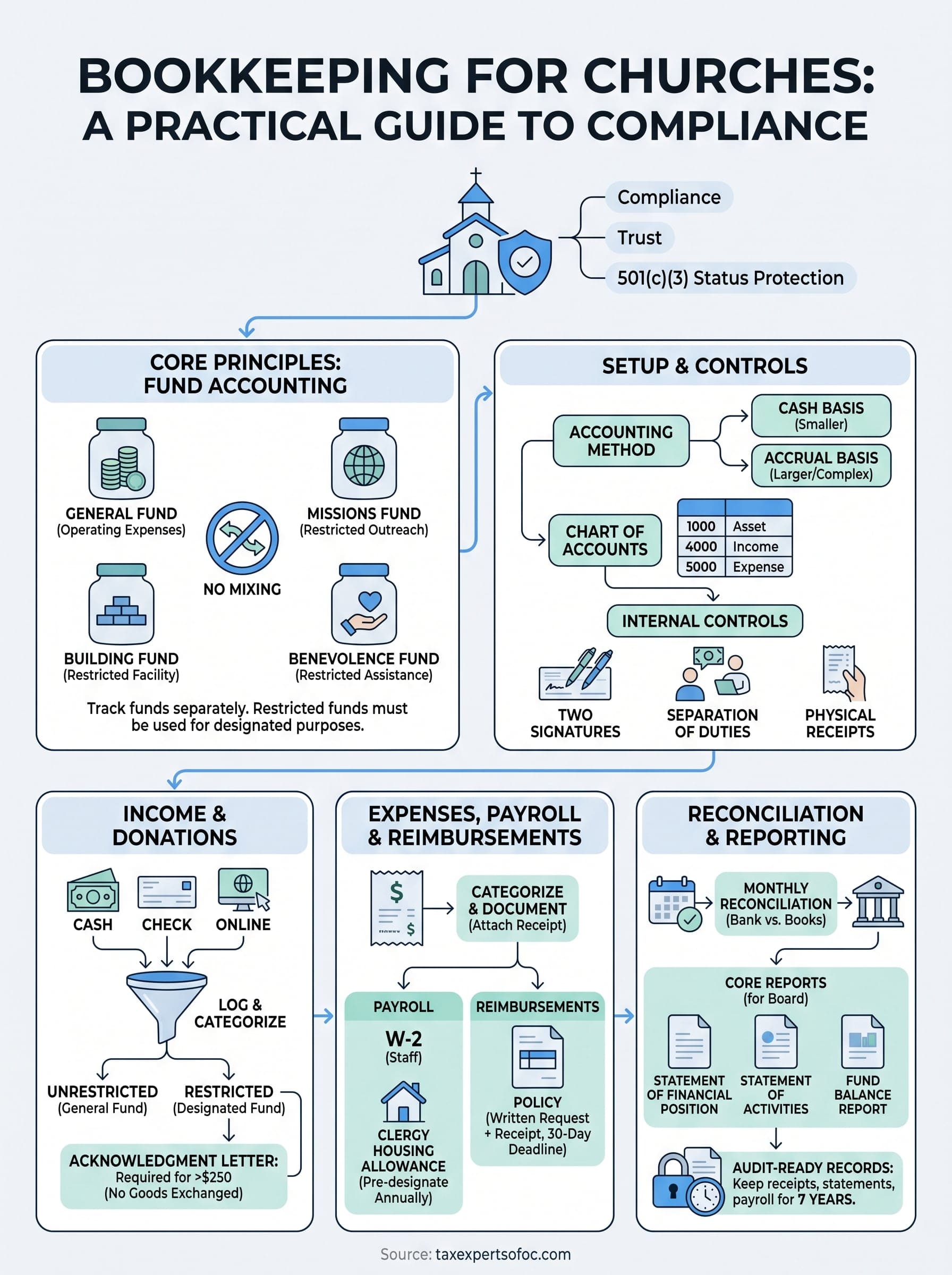

Churches handle tithes, donations, grants, and designated funds, all of which come with strict reporting obligations that most for-profit businesses never deal with. Poor bookkeeping for churches doesn't just create messy records; it can threaten a congregation's tax-exempt status and erode the trust of every member who gives.

The challenge is that many churches rely on volunteers or part-time staff to manage their finances. Without a clear system, transactions get misclassified, donor records fall out of compliance, and year-end reporting becomes a scramble. These aren't minor inconveniences, they're risks with real financial and legal consequences.

This guide walks you through the core principles of church bookkeeping, from fund accounting and internal controls to staying compliant with IRS requirements. At Tax Experts of OC, we work with non-profit organizations across all 50 states, helping them build accurate financial records and meet their reporting obligations. Whether your church handles its books in-house or needs professional support, this article gives you a practical foundation to work from.

What church bookkeeping covers and why it matters

Church bookkeeping goes well beyond recording deposits and writing checks. Accurate financial records protect your organization's 501(c)(3) status, satisfy donor expectations, and give church leadership the data they need to make sound decisions. When bookkeeping for churches is done correctly, it creates a clear paper trail that supports every budget decision and financial report your leadership team produces.

Fund accounting: the core difference from regular bookkeeping

Standard business accounting tracks one pool of money. Church accounting uses fund accounting, which means you track multiple restricted and unrestricted funds separately. A donation marked for the building fund, for example, cannot be used for general operations. If you mix those funds, even unintentionally, you expose your church to legal risk and donor complaints.

Each fund in your chart of accounts needs a separate ledger entry so transactions stay clearly attributed. Common funds include:

- General/Operating Fund: covers day-to-day expenses like utilities, salaries, and supplies

- Missions Fund: restricted to specific outreach or international programs

- Building Fund: designated for construction, renovation, or facility maintenance

- Benevolence Fund: used to provide direct assistance to individuals in need

- Memorial Fund: gifts given in honor of a person, often restricted by the donor's intent

Mixing restricted and unrestricted funds is one of the most common and costly mistakes churches make, and it can trigger IRS scrutiny or donor disputes that take months to resolve.

IRS requirements for tax-exempt organizations

As a 501(c)(3) organization, your church carries specific reporting obligations tied to that status. While most churches are not required to file Form 990, those with gross receipts above $50,000 must file Form 990-N (the e-Postcard) annually. Larger organizations file Form 990-EZ or the full Form 990 depending on their financial activity.

Beyond annual filings, you must issue written acknowledgment letters for any single donation of $250 or more. For non-cash gifts, IRS Form 8283 may apply. Failing to provide these substantiation documents puts your donors at risk of losing their tax deductions, which damages the relationship your church depends on.

Payroll and clergy compensation

Clergy compensation follows unique tax rules that differ from standard employee payroll. A pastor may receive a housing allowance that is excluded from federal income tax, but that allowance must be formally designated by the church board before the tax year begins. If your church employs non-clergy staff, you must also handle standard payroll taxes, W-2 filings, and quarterly deposits to the IRS.

Getting these details wrong creates back-tax liability and potential penalties, so this area of church bookkeeping demands careful attention from the very start.

Set up your church accounting system

Before you log a single transaction, you need the right structure in place. Bookkeeping for churches requires a system built around fund accounting, not the single-ledger approach most small businesses use. Getting this foundation right saves you from costly reclassifications later and makes your year-end reporting far easier to complete.

Choose the right accounting method

Most churches use cash-basis accounting, which records income when received and expenses when paid. This method works well for smaller congregations with straightforward finances. Larger churches with grants, loans, or significant accounts payable may benefit from accrual-basis accounting, which records transactions when they occur, regardless of when cash moves. Talk with a CPA to determine which method fits your current size and reporting obligations.

Switching accounting methods after the fact requires prior IRS approval, so choosing the right method from the start protects you from a complicated, time-consuming process down the road.

Build your chart of accounts

Your chart of accounts is the backbone of your financial system. Each fund, income type, and expense category needs its own account code so transactions stay organized and traceable. Here is a starter template you can adapt to your church's structure:

| Account Code | Account Name | Type |

|---|---|---|

| 1000 | General Checking | Asset |

| 2000 | Accounts Payable | Liability |

| 3000 | General Fund | Fund Balance |

| 4000 | Tithes and Offerings | Income |

| 4100 | Building Fund Donations | Income |

| 5000 | Pastoral Salaries | Expense |

| 5100 | Utilities | Expense |

| 5200 | Missions Giving | Expense |

Put internal controls in place

Internal controls prevent errors and reduce the risk of fraud, which is a real concern for any organization that handles cash donations. Start with these minimum safeguards to protect both your volunteers and your congregation:

- Require two authorized signatures on checks above a set dollar threshold

- Separate the person who receives donations from the person who records them

- Have a board member review bank statements every month

- Keep physical receipt copies for all cash offerings

Record income and donations correctly

Recording income accurately is one of the most critical tasks in bookkeeping for churches. Every donation that comes through your doors, whether it arrives as cash in an offering plate, a check, or an online transfer, needs to be logged with the correct date, amount, fund designation, and donor name before anything else happens. Without this discipline, your records will have gaps that are nearly impossible to reconstruct at year-end reporting time.

Categorize each donation by fund

When you receive a gift, the first question to answer is whether it is restricted or unrestricted. An unrestricted gift goes into your general operating fund and can be used at the church's discretion. A restricted gift, such as one marked "for the building fund," must be posted to the correct designated fund immediately. Never reclassify a restricted gift to cover a shortfall in another fund without written donor consent, because doing so puts your 501(c)(3) status at risk.

Posting a donation to the wrong fund, even temporarily, creates a compliance problem that is very difficult to explain to auditors or members later.

Use a weekly deposit log to capture every form of income before it goes to the bank. A basic template looks like this:

| Date | Donor Name | Amount | Fund | Method |

|---|---|---|---|---|

| 2026-01-05 | Jane Smith | $500 | General | Check |

| 2026-01-05 | Anonymous | $75 | Building | Cash |

| 2026-01-05 | John Doe | $200 | Missions | Online |

Send written acknowledgment for gifts of $250 or more

The IRS requires your church to provide a written acknowledgment letter for any single donation of $250 or more. That letter must include your church's name, the contribution date, the amount, and a statement confirming that no goods or services were exchanged (or a description of what was provided). Prepare these letters promptly after each qualifying gift rather than batching them at year-end, so donors have the documentation they need for their own tax filings.

Track expenses, payroll, and reimbursements

Tracking outgoing money with the same rigor you apply to donations is a core part of bookkeeping for churches. Every check, vendor payment, and staff reimbursement needs a corresponding receipt, a clear category, and a fund assignment before you close the books for that period. Skipping this step creates gaps that are painful to fill later and that can raise red flags during any financial review.

Categorize and document every expense

When you post an expense, assign it to the correct fund and category immediately. Paying your electric bill from the general fund is different from paying a missions conference fee from the missions fund. Use your chart of accounts to guide every entry and attach a digital or physical receipt to each transaction.

A simple expense log covers the basics:

| Date | Payee | Amount | Category | Fund | Receipt |

|---|---|---|---|---|---|

| 2026-01-10 | City Electric | $320 | Utilities | General | Yes |

| 2026-01-12 | Print Shop | $85 | Office Supplies | General | Yes |

| 2026-01-15 | Relief Agency | $500 | Benevolence | Benevolence | Yes |

Handle payroll and clergy housing allowance

Payroll is one of the most complex areas your church will manage. Non-clergy staff require standard W-2 withholding, Social Security contributions, and quarterly IRS deposits via Form 941. Clergy receive different treatment: a pastor's housing allowance is excluded from federal income tax, but your board must formally designate that amount in writing before January 1 of each tax year.

Missing the pre-year designation deadline means the housing allowance becomes fully taxable income for that year, which is a costly mistake to correct after the fact.

Manage reimbursements with a clear policy

Reimbursements without documentation create serious audit exposure. Require every staff member or volunteer who submits an expense to complete a written reimbursement request form that includes the date, purpose, amount, and an attached receipt. Set a 30-day submission deadline so expenses land in the correct accounting period. Any reimbursement that lacks a receipt and a clear business purpose should be denied and resubmitted correctly, because undocumented payments can be reclassified as taxable income by the IRS.

Reconcile, report, and stay audit-ready

Reconciliation is where bookkeeping for churches either holds together or falls apart. Every month, you need to match your accounting records against your bank statements so that errors, missing entries, and unauthorized transactions surface before they become serious problems. A discrepancy caught in January is a one-hour fix; the same discrepancy found in December becomes a full investigation.

Reconcile your accounts monthly

Pull your bank statement on the last day of each month and compare every transaction line by line against your accounting software records. Mark each item as cleared, flag anything that doesn't match, and resolve discrepancies before you close that month. If you find an entry in the bank statement with no corresponding record, trace it back to its source immediately. Unresolved reconciling items carry forward and compound, making future months progressively harder to close accurately.

Reconciling once a month keeps your books clean and gives your board a reliable financial picture every time they need to make a decision.

Produce financial reports for leadership

Your church board needs three core reports on a regular basis to make sound decisions. Provide these at every board meeting so leadership can see exactly where the church stands:

- Statement of Financial Position: your balance sheet showing assets, liabilities, and fund balances

- Statement of Activities: your income and expense summary broken down by fund

- Fund Balance Report: the current status of each restricted and unrestricted fund

Monthly reporting also creates a documented record that demonstrates transparency to your congregation and any external reviewers.

Keep records audit-ready

Staying audit-ready means you never scramble when someone asks for documentation. Store receipts, bank statements, payroll records, and donation acknowledgment letters for a minimum of seven years. Organize them by year and category so you can retrieve any document within minutes. If your church faces an IRS review or internal audit, complete and organized records are your strongest defense and your fastest path to resolution.

Next steps for your church finances

You now have a complete framework for bookkeeping for churches, from setting up fund accounts and recording donations correctly to reconciling monthly and keeping records audit-ready. Putting this system in place requires consistent effort, but the payoff is a financially transparent organization that protects its tax-exempt status and earns the ongoing trust of every person who gives.

Start by reviewing your current chart of accounts against the structure outlined in this guide. If your funds are not separated correctly, fix that first before you address anything else. From there, implement the internal controls, weekly deposit log, and monthly reconciliation process as a routine rather than a reaction to problems.

If your church needs professional support to get its books in order or resolve IRS compliance concerns, Tax Experts of OC works with non-profit organizations nationwide and offers a free 30-minute consultation to get you started.