Owing money to the IRS can feel like carrying a weight that gets heavier every month. Between penalties, interest, and collection notices, the balance keeps growing, and so does the stress. But here's something many taxpayers don't realize: you may be able to settle IRS tax debt for less than what you owe through a program the IRS itself offers. It's called an Offer in Compromise (OIC), and it exists specifically for people who can't realistically pay their full tax balance.

The catch? Not everyone qualifies, and the application process is detailed. The IRS evaluates your income, expenses, assets, and future earning potential before accepting any offer. Submit the wrong numbers or miss a step, and your application gets rejected, sometimes costing you months of effort and the non-refundable application fee. That's why understanding eligibility requirements and each step of the process matters before you file anything.

At Tax Experts of OC, our CPAs and Enrolled Agents help clients across all 50 states navigate IRS debt relief options, including OIC applications. This guide breaks down who qualifies for an Offer in Compromise, how the IRS decides what to accept, and the exact steps to apply, so you can make an informed decision about whether this path is right for your situation.

What it means to settle IRS tax debt

When you settle IRS tax debt, you're negotiating with the IRS to accept a lump sum or short-term payment that's less than the full amount you owe, including penalties and interest. This is not a loophole or a technicality. The IRS created the Offer in Compromise program specifically because collecting a partial payment from a struggling taxpayer is often more practical than collecting nothing at all. The program exists as an official resolution tool, and the IRS processes thousands of accepted offers each year.

The IRS is more likely to accept a settlement offer when your realistic ability to pay is genuinely lower than your total tax balance.

How the IRS calculates what you can realistically pay

The IRS doesn't look at your total balance and pick a number. Instead, it calculates your Reasonable Collection Potential (RCP), which is the core figure used to determine whether to accept your offer. Your RCP is based on the value of your assets (bank accounts, real estate, vehicles, and investments) plus your future income potential after subtracting IRS-approved living expenses.

For example, if you owe $40,000 but your countable assets total $5,000 and your monthly income barely covers your allowable expenses, your RCP might land around $8,000. The IRS will generally not accept an offer below that figure, but they could accept one close to it if your numbers are fully documented and verified. That calculation is where most applications succeed or fail.

What an accepted offer actually covers

When the IRS accepts your OIC, it resolves the entire tax liability for the years included in your offer, meaning the original tax, accrued penalties, and interest are all settled for the agreed amount. No further collection action applies to that debt once you fulfill the terms of the agreement, including staying current on future tax filings and payments for five years.

However, the settlement only covers the specific tax periods you listed on your application. If you have other unfiled years or separate liabilities not included, those remain open and fully collectible. This is a detail many applicants miss, and it's one reason reviewing your complete tax history before filing an OIC is worth doing carefully.

How settling compares to other IRS relief options

Settling your debt through an OIC is one of several ways to resolve what you owe, but it's the only option that reduces the actual balance rather than restructuring how you pay it. An installment agreement, for instance, lets you pay over time, but you still pay the full amount plus ongoing interest. Currently Not Collectible (CNC) status pauses collection activity but doesn't eliminate the debt, and the IRS can resume collection once your financial situation improves.

Penalty abatement can reduce what you owe by removing certain penalties if you qualify, but it does not touch the base tax amount. An OIC is the only resolution path that can bring your total liability down to a fraction of what was originally assessed, which makes it the most sought-after option for taxpayers carrying balances they have no realistic path to pay in full.

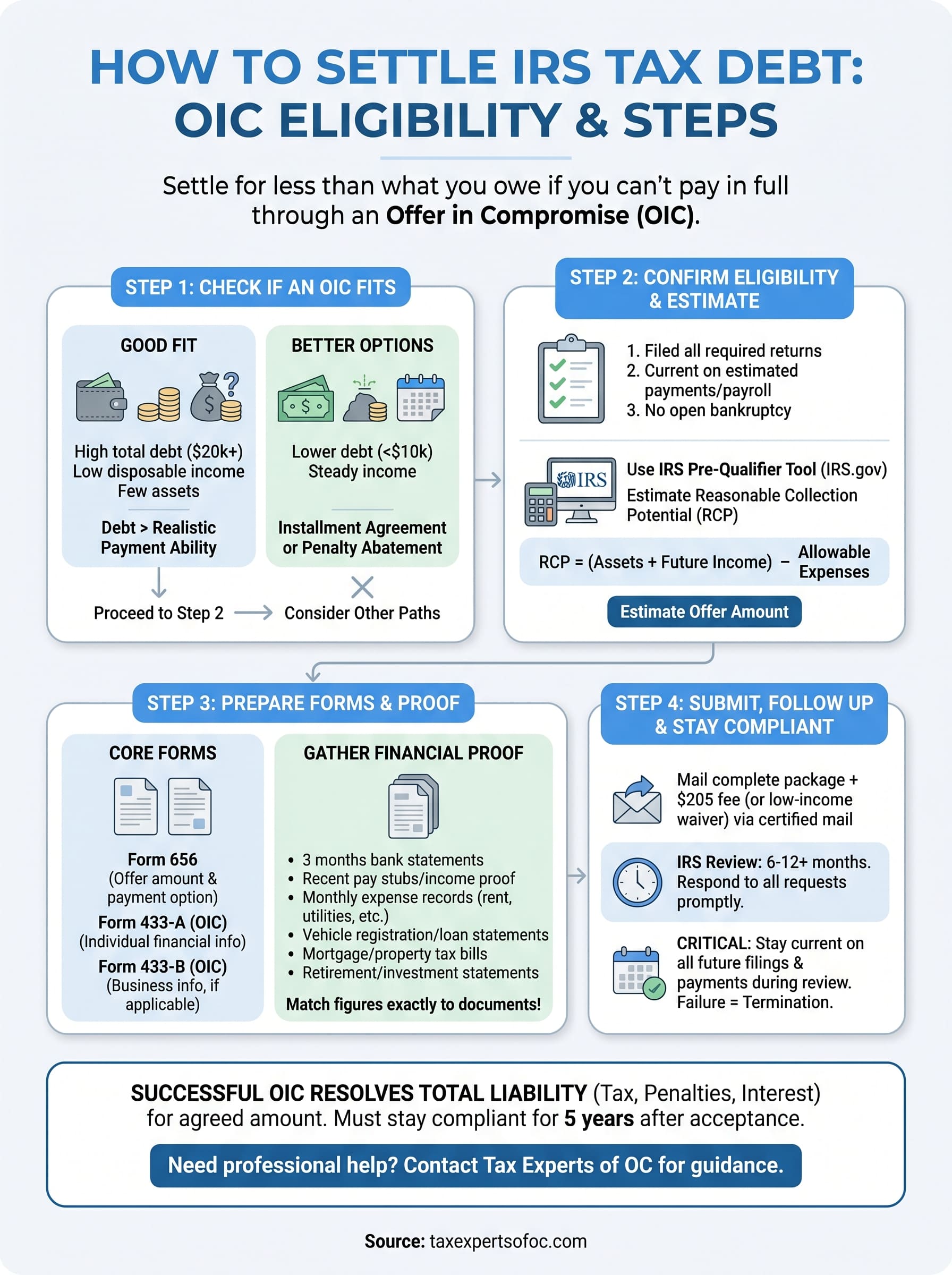

Step 1. Check if an offer in compromise fits

Before you start gathering documents or filling out forms, you need to determine whether an OIC is actually the right resolution path for your situation. The IRS accepts offers on three grounds: doubt as to collectibility (you genuinely can't pay the full balance), doubt as to liability (you dispute what you owe), and effective tax administration (paying in full would create an exceptional hardship). The vast majority of accepted offers fall under doubt as to collectibility, which is the path this guide focuses on.

Applying for an OIC without first confirming it fits your situation is one of the most common reasons applications get rejected and fees are lost.

When an OIC is likely the right fit

An OIC tends to be the strongest option when your total tax debt significantly exceeds what you can realistically pay from your assets and income within the IRS collection window, which is generally 10 years from the assessment date. If you carry a balance of $20,000 or more and your monthly disposable income after allowable expenses is minimal, an OIC application is worth pursuing.

Consider a self-employed individual who owes $35,000 but holds $3,000 in savings, drives an older vehicle with minimal equity, and clears $200 per month after IRS-approved living expenses. Their RCP would sit well below their total balance, which is exactly the scenario where the IRS will consider an offer to settle IRS tax debt for a reduced amount rather than pursue full collection.

Signs another option may fit better

If you owe less than $10,000 and have consistent employment income, an installment agreement likely resolves your situation faster and with far less paperwork. You should also evaluate penalty abatement first if penalties, rather than the base tax, make up the bulk of your balance, since removing those penalties alone can bring your debt down to a manageable level.

| Your situation | Likely better option |

|---|---|

| Manageable debt with steady income | Installment agreement |

| Penalties make up most of what you owe | Penalty abatement |

| You dispute the amount the IRS assessed | OIC (doubt as to liability) |

| Low assets and cannot pay the full balance | OIC (doubt as to collectibility) |

Step 2. Confirm eligibility and estimate your offer

Once you've decided an OIC fits your situation, verify that you meet the IRS's baseline requirements before investing time in a full application. The IRS rejects applications upfront when specific conditions aren't satisfied, so confirming eligibility early saves you both the $205 non-refundable application fee and several months of processing time.

Meet the basic eligibility criteria

To qualify for an Offer in Compromise, you must satisfy several non-negotiable conditions before submitting anything. You need to have filed all required tax returns for prior years, have no open bankruptcy proceedings, and be current on any required estimated tax payments for the current year if you're self-employed or receive non-wage income. If you own a business with employees, all required federal payroll tax deposits must also be current.

The IRS will automatically reject your application if any of these conditions are unmet. Check your tax transcript at IRS.gov to confirm which years are filed and which are missing before you move forward. If you have unfiled returns, file them first, even if you can't pay the balance owed.

Use the IRS pre-qualifier tool to estimate your offer

The IRS provides a free OIC Pre-Qualifier tool on IRS.gov that walks you through a series of questions about your income, expenses, assets, and liabilities. It applies the same Reasonable Collection Potential formula the IRS uses during review and returns an estimated offer amount based on your inputs.

Running this tool before filing your application tells you whether your proposed offer is realistic and what financial documentation you'll need to support it.

Work through the tool using actual figures from your bank statements and pay stubs rather than rough estimates. If the result shows your RCP sits close to your full balance, an OIC may not reduce your liability enough to justify the effort, and another option to settle IRS tax debt might be more practical. If the estimated offer is significantly lower than what you owe, you have a solid foundation to build your application on.

Step 3. Prepare the forms and financial proof

Once you confirm your eligibility and estimate your offer amount, you move into the most document-intensive part of the process. The IRS requires specific forms and supporting financial records to evaluate your application. Submitting incomplete or inaccurate paperwork is one of the top reasons applications to settle IRS tax debt get rejected before anyone reviews the numbers.

Every figure you report on your OIC forms must match your supporting documents exactly, since the IRS cross-checks both during review.

Complete the core OIC forms

Your application requires two primary forms. Form 656 is the actual offer document where you state the amount you're proposing and select your payment option. Form 433-A (OIC) is the Collection Information Statement for individuals, capturing a full picture of your income, expenses, assets, and liabilities. If you own a business, you also need Form 433-B (OIC) to report business assets and financials separately.

Both forms are free downloads from IRS.gov. Fill them out using your actual figures, not estimates. The IRS compares your reported numbers against bank records, tax transcripts, and third-party data, so accuracy at every line directly affects your outcome.

Gather your financial documentation

The IRS requires supporting documents to verify every figure you enter on Form 433-A. Organize these before you start filling out the forms to avoid delays:

- Last three months of bank statements for all personal and business accounts

- Recent pay stubs or proof of self-employment income for the past three months

- Monthly expense records covering rent or mortgage, utilities, insurance, and vehicle costs

- Vehicle registration and loan statements to establish current equity

- Most recent mortgage statement or property tax bill if you own real estate

- Retirement and investment account statements showing current balances

Keep copies of everything you submit. The IRS may request additional verification during review, and having your records organized by category speeds up your response time considerably.

Step 4. Submit, follow up, and stay compliant

After organizing your forms and documents, you're ready to submit your application package to the IRS. At this stage, the process shifts from preparation to patience, but there are specific actions you must take throughout the review period to protect your application and avoid an automatic rejection.

Submit your package to the correct IRS address

Mail your completed Form 656, Form 433-A (OIC), supporting documents, and the $205 application fee together in one package. The mailing address depends on your state of residence. Refer to the Form 656 instructions on IRS.gov for the correct address for your location. Send everything via certified mail with return receipt so you have dated proof of submission.

Include a check or money order made payable to the "United States Treasury." If your income falls at or below 250% of the federal poverty level, you qualify for the low-income certification, which waives both the application fee and the required initial payment. Check the appropriate box on Form 656 to claim this waiver.

What happens after you submit

Once the IRS receives your package, it assigns your case to an Offer Examiner who reviews your financial information against your reported figures. This process typically takes 6 to 12 months, sometimes longer. During that time, the IRS pauses most collection activity tied to the debt included in your offer.

The IRS may contact you for additional documentation during review, so respond to any requests within the timeframe given to avoid automatic rejection.

If the examiner proposes a different settlement amount, you can accept, negotiate, or reject it. If the IRS rejects your offer outright, you have 30 days to file an appeal using Form 13711, Request for Appeal of Offer in Compromise.

Stay compliant while the IRS reviews your offer

To settle IRS tax debt successfully, you must remain current on all filing and payment obligations throughout the review period. File every return on time and make all required estimated tax payments. If you fall out of compliance, the IRS automatically terminates your offer, regardless of how well-documented your application was.

If you want help, here's what to do next

The steps to settle IRS tax debt are clear, but executing them correctly takes time, accurate financial documentation, and a solid understanding of how the IRS evaluates your offer. One mistake on your forms or a missed filing requirement can cost you months and a non-refundable fee. If you want a qualified professional to handle the process from start to finish, Tax Experts of OC can help.

Our CPAs and Enrolled Agents work with clients across all 50 states to evaluate eligibility, calculate a realistic offer amount, prepare complete documentation, and represent you through the full IRS review process. You get direct access to qualified professionals, not general staff, along with transparent upfront pricing and flexible payment options if you're currently facing financial hardship.

Start with a free 30-minute consultation to review your situation and find the right resolution path for your balance. Schedule your free consultation with Tax Experts of OC today.